‘Bout Jay and the FOMC The market has come to agree The battle’s been won And hiking is done So, buy stocks with verve and with glee In Europe, though, Madame Lagarde Is finding that things are still hard Inflation’s not tamed And she will be blamed If prices, she cannot retard Meanwhile on the world’s other side Where growth has begun to backslide The PBOC More cash will set free As Xi tries to hold back the tide

When looking at the market activity yesterday, it is easy to conclude that the market believes the Fed has instituted their last hike. This was evident in the equity market’s performance where all three major indices rallied more than 1% and it was evident in the FX market where the dollar was pummeled, falling by 1% or more against 7 of its G10 counterparts as well as about half the EMG bloc. In addition, Treasury yields fell sharply as the idea that the Fed is going to continue hiking, as implied by Chairman Powell in his comments on Wednesday, seems to have faded from memory.

But that’s not all! While key markets are beginning to discount any further Fed activity, the ECB not only raised their rate structure by 25bps as expected, but Madame Lagarde essentially promised another hike in July and this morning the ECB’s hawks are circling and hinting that a September rate hike is quite possible as well.

Now, we already know that the Fed’s dot plot is calling for 2 more rate hikes this year, but the Fed funds futures market is not in accord with that view. Rather, it is pricing a 70% probability of a July hike as the final move. But, will they hike again? Clearly, between now and the end of July we will all have seen a great deal more data, including both an NFP and CPI report, and that will have a major impact on the Fed. But after yesterday’s US data dump, which showed Retail Sales holding up far better than expected while both the Import and Export Price Indices showed price declines, there has been a significant increase in the chatter of the Fed pulling off a soft landing after all. And, if the landing is soft, do they need to hike more?

Although the manufacturing side of the economy remains lackluster, Services have been killing it. There is one other reason to believe the Fed will remain on hold as well, and that is the employment situation. While we have seen a much hotter than forecast NFP print basically each month for the past year, we are starting to see Initial Claims data tick higher. Yesterday’s 262K was both higher than expected and the highest print since October 2021 when claims were tumbling during the post-pandemic recovery. More ominously, the 4-week and 13-week moving averages (analyzed to seek a trend and remove the weekly choppiness) are both clearly trending higher. If that number continues to rise, the Fed’s confidence in the economic recovery continuing is likely to be impaired. In fact, I think this is the feature that is most likely to cause the Fed to stop hiking.

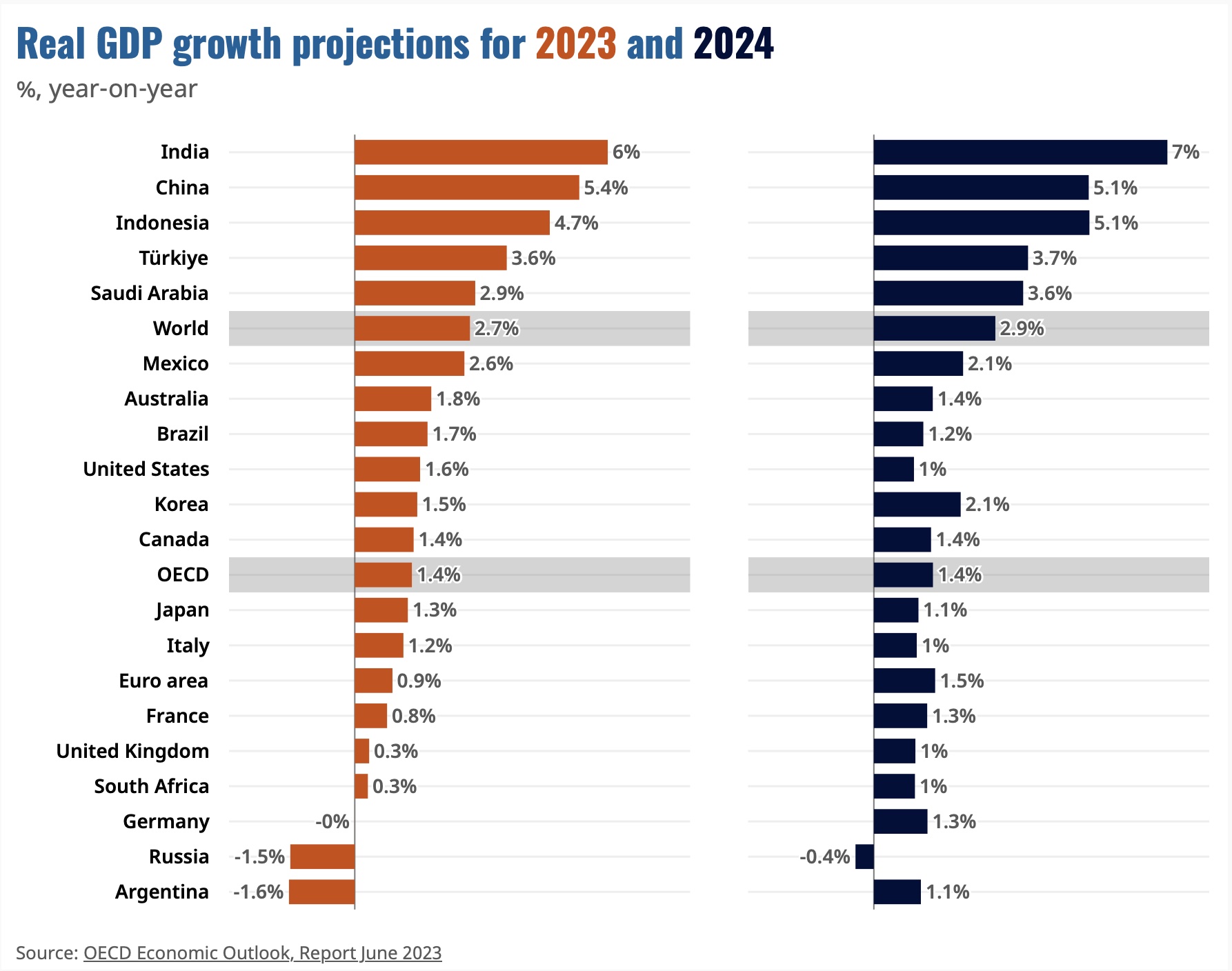

If we pivot to Asia for a moment, we see a completely different set of concerns in both China and Japan. Starting with China, after cutting their lending rates earlier this week, the PBOC is still struggling to figure out how to support what is a clearly softening economy. Although there has been much lip service paid to the fact that China will no longer prop up the property market and investment and is instead seeking to generate more domestic consumption, the fact that the youth unemployment rate is at a record 20.8% and that the only playbook the Chinese really understand is infrastructure spending and leveraged property speculation, they are falling back into that trap. Rumors abound that the government is going to put forth a CNY1 trillion (~$140B) spending package and that the PBOC is going to ease restrictions on property lending, removing the ban on second home purchases in small cities. Remember, property speculation was a critical part of China’s rapid growth as people there have little confidence in a social safety net and were using those second homes as an investment to secure their nest egg. Alas, with China’s population shrinking, that may no longer be an interesting investment for the middle class. So, while China’s problems are different, they are no less severe than those in the West.

Uncertainty is “Extremely high” over both Wages and prices So, Ueda-san Will keep liquidity flows Like flooding rivers

As to Japan, I’m old enough to remember when there was a growing belief that once Kuroda-san stepped down as BOJ head, his replacement would have free rein to tighten policy. Boy, were we ever wrong about that. After last night, while there was no policy adjustment as expected, Ueda-san’s comments can only be construed as strongly dovish and the market got the message. JGB yields slid a few basis points and are back below 0.40% while the yen is the only currency that is underperforming the dollar. Meanwhile, the Nikkei (+0.65%) continues its recent strong performance as the second best major index after only the NASDAQ.

The one thing that we know is that things do not seem to be evolving as per much of the consensus from earlier this year. While there is still a long way to go before this cycle ends, and I still expect a more significant economic slowdown globally, the possibility that Chairman Powell pulls off a soft landing cannot be dismissed. And as I saw on Twitter yesterday, if he does so, he will be hailed as the greatest Fed chair ever, even more so than Paul Volcker. Alas, I fear things will not work out that way. Remember that monetary policy works with long and variable lags, and I would contend that the economy is likely just beginning to feel the true impacts of tighter policy. Now, this may only happen in the manufacturing sector, where the cost of capital is such a critical input, but history has shown if that sector stumbles, it drags the economy down with it. Remember that so much of the service economy exists to service manufacturing, so the two are quite intertwined.

Remember, too, there are potential exogenous shocks, both positive and negative, that can have a big impact. What if the Ukraine war ended? What if China invaded Taiwan? What if there was an escalation of fighting in the Middle East with a dramatic reduction in oil production? All I am pointing out is that myopically focusing on just the economic data is not sufficient for a risk manager. Sh*t happens and it can matter a lot.

Ok, as to today, we already know that risk is on. The data coming out this morning is Michigan Sentiment (exp 60.0) and of the three Fed speakers, two have already commented with Governor Waller not talking economics or policy, but rather bank regulation and Bullard was more theoretical than policy focused, so really there has been nothing new there either. In a little while, Richmond’s Barkin will discuss inflation, so that could be interesting. But for right now, the market has made up its mind. Everything is right as rain so add risk. That means the dollar is likely to remain under pressure with a test of its lows (EUR 1.11, DXY 102) coming soon to a screen near you.

Heading into a bank holiday weekend, I expect positions to be lightened but the recent dollar weakening trend to remain intact.

Good luck and good weekend

Adf