Each month there’s a Payrolls report

That pundits and traders exhort

To rise or to fall

Subject to their call

And whether they’re long or they’re short

But this month, there seems to be more

At stake, for the Fed’s tug-of-war

If joblessness rises

Each pundit advises

That rate cuts, this summer, we’ll score

Here we are on the first Friday of the month and, as almost always, markets remain quiet ahead of the release of the monthly Payroll report. For good order’s sake, here are the current median expectations:

| Nonfarm Payrolls | 185K |

| Private Payrolls | 170K |

| Manufacturing Payrolls | 5K |

| Unemployment Rate | 3.9% |

| Average Hourly Earnings | 0.3% (3.9% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 62.7% |

Recall, on Wednesday, the ADP Employment number was a bit softer at 152K while the ISM Employment sub-indices showed conflicting data between Manufacturing (much stronger at 51.1) and Services (weaker at 47.1). Ironically, the headline ISM data was the other way around, with Manufacturing weaker and Services stronger than expected. One other data point of note was the JOLTS Job Openings which shrunk about 300K to 8.059M, still high relative to the number of unemployed people, but with the ratio falling to 1.24 jobs/unemployed person. That ratio is down from nearly 2:1 shortly after the pandemic, but up from about 1:1 pre-pandemic.

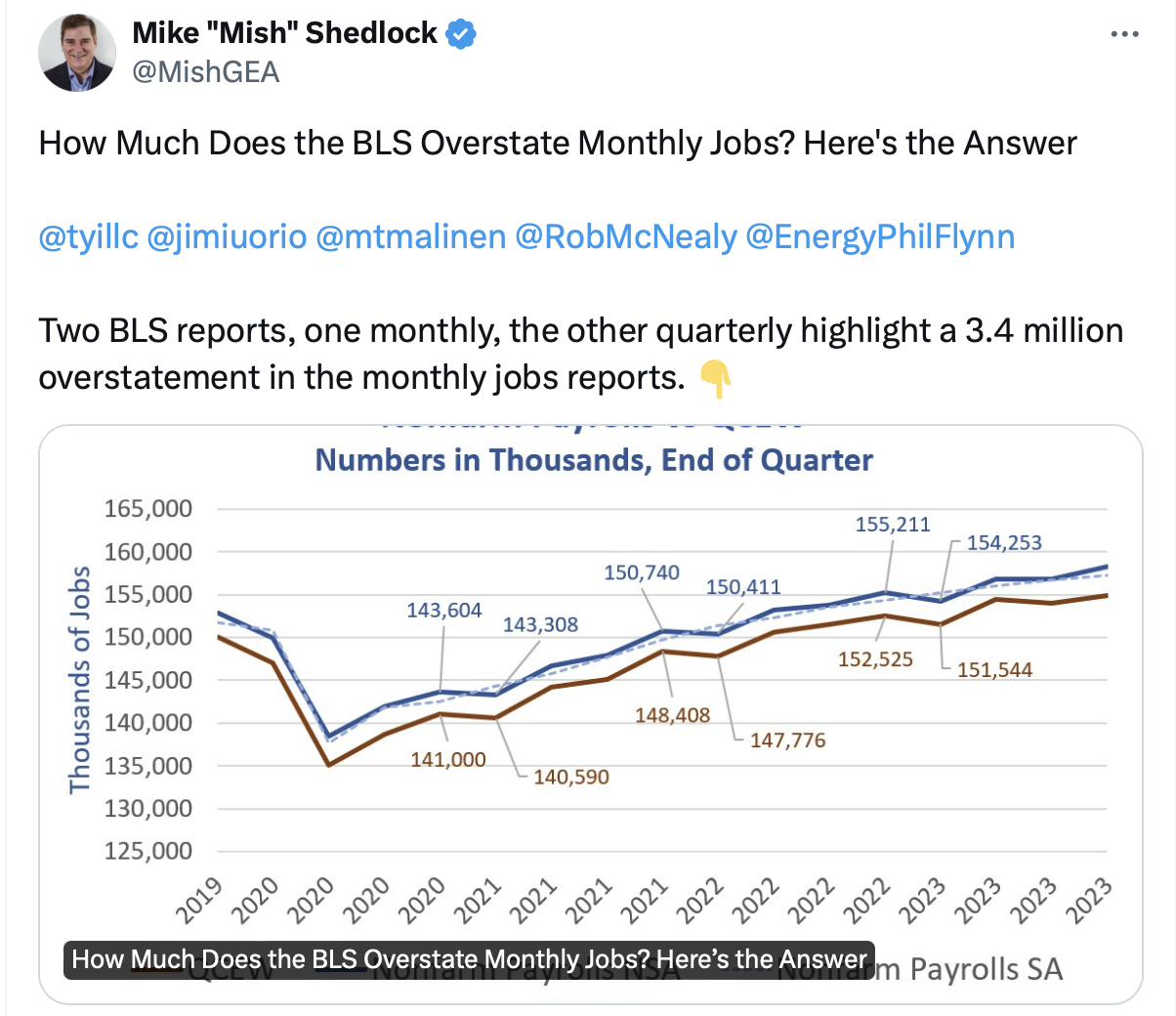

As with so much of the other data that we have seen over the past months, there is no clear direction here. Economy bulls can make the case that job growth remains solid and that there is no indication that a recession is on the way. While the no-landing thesis has lost adherents, there are still many soft-landing adherents to be found. At the same time, the economic bears have plenty of data to claim that a recession is around the corner, if we are not already in one. I saw an analysis by Mike Shedlock (@MishGEA), a well-respected economist, that claims the NFP data has overstated job growth by 3.4 million jobs as per the following Tweet:

Since the beginning of 2023, looking at BLS data, the initial NFP report has been revised down in twelve of the fourteen months where there has been a third revision, by a total of 496K. I created a chart to show the consistency of those revisions to help you get a better idea of the issue.

Source: data BLS, graph @fx_poet

Something that has always been true with respect to economic data, and NFP is no different than any other piece of information, is that the revisions tell an important story. When initial data gets revised lower on a consistent basis, it has been indicative of a slowing economy. Remember that when the NBER declares a recession, it is always a backward-looking effort, it is never in real-time. But revisions are a key part of that process. As well, given the fudge factors built into the BLS model, notably the birth/death factor for new businesses, history has shown that particular piece of the puzzle is always a lagging indicator as during a recession, more companies fail than are created, and that needs to be addressed via the revisions.

In the end, the issue is no matter the actual data point this morning, it will almost certainly be revised substantially before the end of the summer and could well tell a very different tale. But today’s task is to understand what tale it is going to tell right now.

To that end, the narrative, the best that I can tell, is that we are seeing a gradual reduction in economic activity, but nothing dramatic. Recession is still a remote concern, perhaps for 2025 or 2026, but the slowdown in activity will open the door for the Fed to start to ease policy going forward. While the futures market is virtually certain that there will be no Fed action next week, the probability of a July cut has risen to 22.5% from less than 16% a week ago. Several big banks are calling for a July cut, including JPM and Goldman Sachs, and there is a group of analysts who maintain that the underlying data that has been released indicates we are already in recession, and that rate cuts are coming very soon.

Here’s the thing, this focus on the Fed cutting rates remains, IMHO, a bad indicator of future risk asset strength. Rather, as I showed earlier this week, when the Fed is cutting rates, it is usually because the economy is already in a recession and earnings are declining rapidly. So, while the first cut may be sweet, the second should be a serious warning of what is coming down the pike. I have already made my bed regarding my view that the top is in, but a softish number this morning, especially if the Unemployment Rate were to rise to 4.0% or 4.1%, would certainly increase the July cut probabilities, and almost certainly be followed by an equity market rally. However, I would call that the last leg of the move. As to my opinion of what today’s number will be, my sense, looking through my lens of further economic weakness (although still sticky inflation) is that it will be on the soft side, but not dramatically so. Maybe 130K-150K.

Ok, ahead of the data, a quick tour of the markets shows that stocks in Asia were mixed with Japan edging lower, China and Hong Kong seeing declines of about -0.5%, but South Korea (+1.2%) and India (+2.1%) having strong sessions. The same cannot be said for Europe, where every major index is lower by between -0.5% (Spain) and -1.0% (France) as German IP (-0.1%) continues to lag and the French Trade Balance (-€7.6B) fell into a deeper deficit than forecast. Not surprisingly, US futures are essentially unchanged ahead of the NFP.

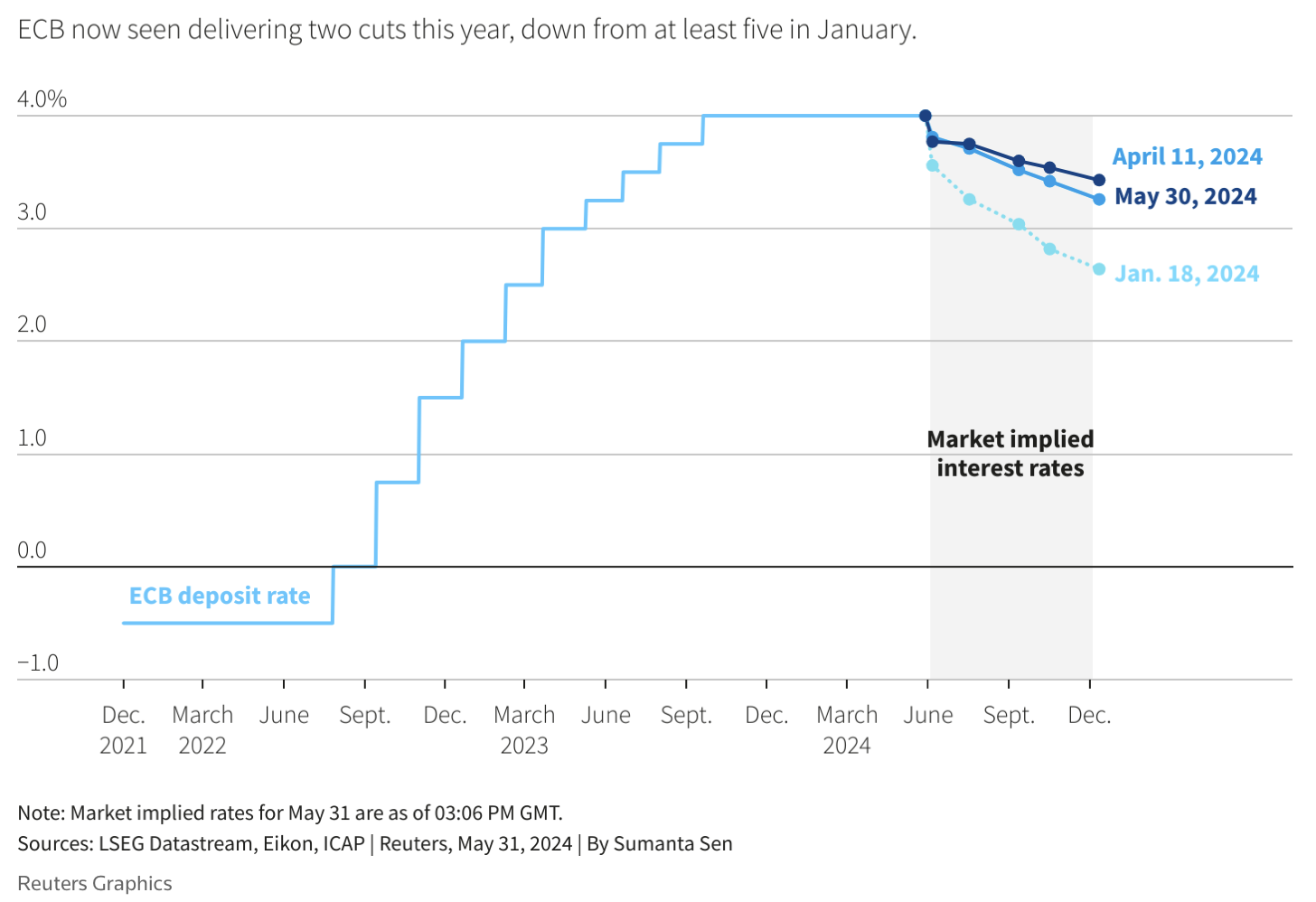

In the bond market, yields are edging up from their recent lows with Treasuries up 1bp and European sovereign yields higher by between 3bps and 5bps despite yesterday’s rate cut from the ECB. Or perhaps because of it as remarkably, the ECB raised its own inflation forecasts and then cut rates. The political imperative to cut interest rates is clearly growing quite strongly.

In the commodity markets, while oil (+0.7%) continues to rebound from its recent lows as OPEC+ worked to clarify their statements about future production, the big move today is in metals where gold (-1.8%) is selling off sharply after the news that the PBOC did not buy any additional metal during the month of May. As they have been one of the key supporters of the barbarous relic, their absence really was a surprise. Most pundits believe they are simply taking a break for now given the sharp rise in the price of the metal, but that they will return. However, the other metals have all sold off alongside gold, with silver (-3.0%) and copper (-2.25%) giving back a good portion of their gains from the past two sessions.

Finally, the dollar is basically unchanged ahead of the NFP data with none of the G10 currencies moving more than 0.1%. In the EMG bloc, though, ZAR (+0.9%) is the outlier, as despite the weakness in the gold price, the political situation seems to be getting better with a coalition government looking to be formed shortly.

In addition to the payroll data, we see Consumer Credit (exp $11B) this afternoon, and confusingly, despite the Fed being in its quiet period, Governor Lisa Cook is on the calendar to speak at noon today. I would guess this will not be a discussion on monetary policy, but you never know.

At this point, it’s all about the data. A hot number should see yields rise, stocks fall and the dollar bounce. A cool number the opposite as more and more people anticipate that first rate cut. Buckle up!

Good luck and good weekend

Adf