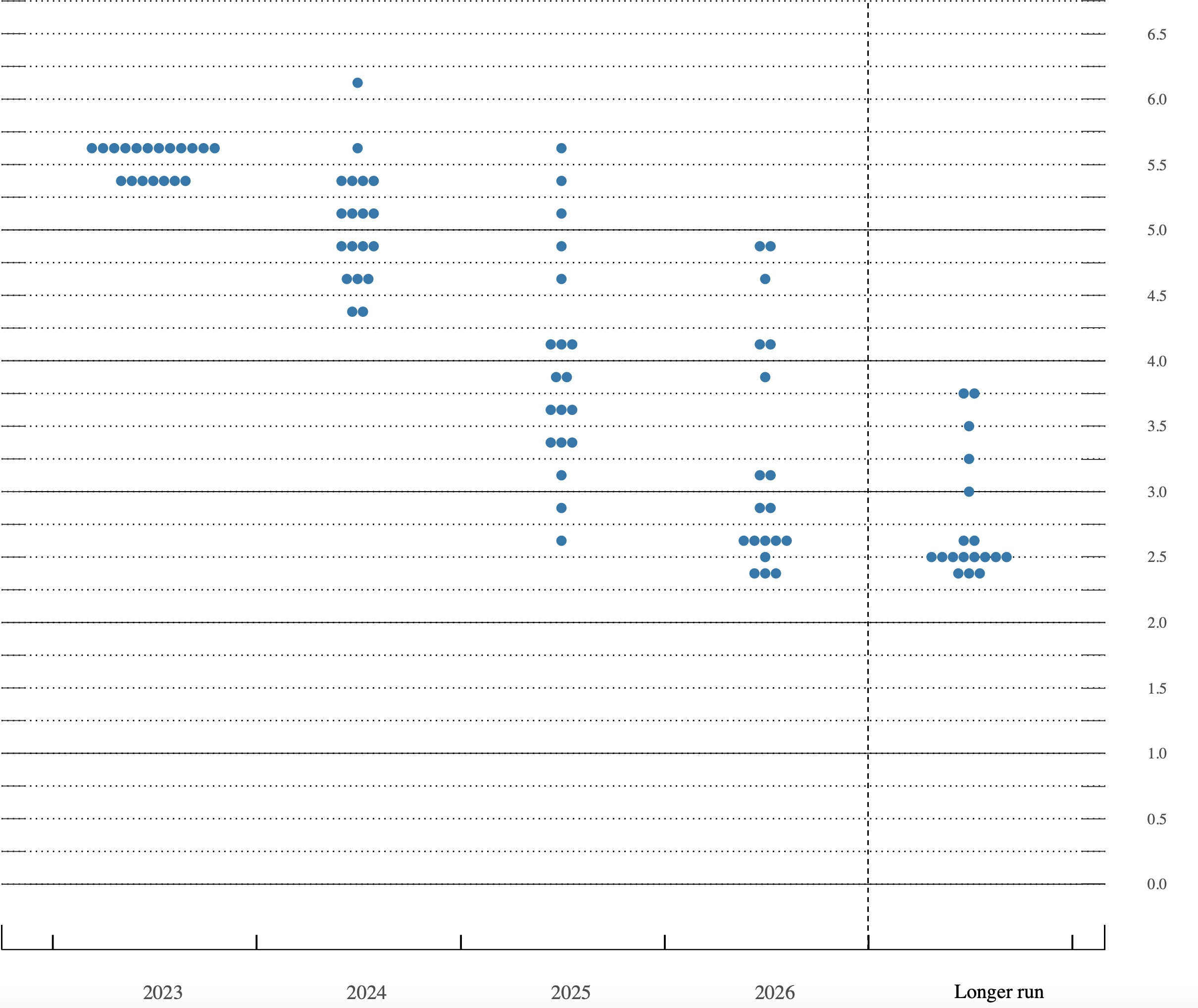

Watanabe-san, A previous Mr Yen, “No intervention”

As USD/JPY approaches the psychological level of 150.00, there is a growing belief in the market that the BOJ is soon going to intervene. Recall, last week we heard about the urgency with which the MOF is watching the exchange rate. Historically, the next step would be for the BOJ to ‘check rates’. This is when they call around to the big Tokyo bank FX trading desks and ask for levels. The implication is they are ready to sell dollars and defend the yen.

However, unlike the previous decline in the yen almost exactly a year ago, the recent movement has been somewhat more gradual as can be seen in the chart below (source tradingeconomics.com)

This was highlighted last night by Hiroshi Watanabe, the deputy FinMin in charge of currency policy from 2004 through 2007. He explained that after seeing the dollar remain in a 145-150 range for much of the past year, “I don’t think authorities are worried about the outlook as much as they were last year. There’s no sense of imminence because the dollar/yen level hasn’t changed much from a year ago, and it doesn’t seem like the yen will start to plunge even if it breaches the 150 mark.”

As is often the case when it comes to concerns about a currency’s value, the pace of its decline is far more important than the actual level. Most countries, or at least most finance ministries, feel they can handle slow and steady. It is the abrupt collapses that scare them. This move has been quite steady, and as long as both the Fed and BOJ maintain their current monetary policies, a continuation seems likely. Hedgers, keep that in mind.

Now, turning to yesterday’s trade A message was clearly conveyed As interest rates rise Risk appetite dies And people are much more afraid

The most pressing story in markets continues to be the US Treasury market where sellers outnumber buyers on a daily basis. Yields on the 10-year rose 10bps yesterday, touching 4.70% and are continuing higher by another 2bps so far this morning. The bear steepener continues to be the story with the 2yr-10yr spread falling to -40bps and looking for all the world like it is going to go positive before the end of the year, if not the end of the month. And it makes sense. There is still substantial demand for short-term paper yielding more than 5% (yesterday’s 3mo T-Bill auction cleared at 5.35%). Meanwhile, we are seeing money flee those assets with long duration over fears that inflation has not yet been quelled and that the structural issues (ongoing massive supply meeting limited demand) has investors pulling back quickly. Not only are Treasury bonds being sold aggressively driving yields higher, but yesterday saw utility stocks, often seen as a duration proxy given the high amount of debt on their balance sheets, fall nearly 5%.

This activity is having the knock-on effects that one would expect as well. Yields around the world continue to get dragged higher by Treasuries, the dollar continues to benefit, and commodity prices are suffering. In fact, yesterday saw a sharp decline in the price of oil and it has now retraced more than 6% from the peak last week. I had written about the simultaneous rise in yields, the dollar and oil as being a HUGE problem for global markets. Well, it seems that oil is starting to feel the pain of higher yields and a stronger dollar. As well, tomorrow OPEC meets in Vienna and there is some talk that the Saudis may increase their production, unwinding those unilateral cuts made back in June and continued since then.

But make no mistake, ongoing rises in Treasury yields will continue to underpin the dollar and that will be enough of a problem for economies elsewhere even if oil prices slide some more. And right now, there is no indication things are going to change. Yesterday we heard from two Fed speakers, Governor Bowman and Cleveland Fed President Mester with both maintaining the hawkish views. In fact, Bowman expressed the need for several more rate hikes in order to get inflation under control and both were clear that higher for longer was crucial. As long as that remains the Fed attitude, until we see a substantial change in the data stream, yields are going to continue to rise.

Now, this week brings the all-important NFP report on Friday, which has been a key driver of Fed policy. With inflation readings continuing far above the Fed’s target, as long as NFP remains positive and the Unemployment Rate remains either side of 4%, the Fed will have no reason to reconsider the current policy mix. In their minds, they have not yet broken anything, at least not so badly that it couldn’t be fixed. I’m sure they are straining their arms as they pat themselves on the back for the effectiveness of the Bank Term Funding Program (BTFP) which was created after the bank failures in March. In fairness, it seems to be working for now. However, I will warn that cans can only be kicked down the road for so long, and I fear the end of that road is nearing.

As to the rest of the session today, risk is decidedly on the back foot. Those equity markets in Asia that were open all fell pretty sharply with the Nikkei (-1.6%) and Hang Seng (-2.7%) leading the way lower. The story is similar in Europe with the major indices all lower by about -0.75% or so as they respond to the ongoing increase in interest rates around the world. Finally, US futures are lower by -0.45% at this hour (7:30) with concerns growing that yields will not stop rising.

Looking at European sovereign bonds, yields there are rising alongside Treasury yields with most of them higher by 3bps-4bps and Italy higher by 9bps. That Bund-BTP spread, currently at 193bps, is something we need to watch as 200bps is likely to be the first place the ECB really shows concern and if it heads higher than that, expect more direct actions. As to JGB yields, they remain static at 0.76%.

We already discussed oil prices and we are seeing serious weakness across the entire metals complex lately, although today’s declines are relatively muted, on the order of -0.2%, as the moves have already been pretty large. The lesson from the recent price activity is that yields continue to drive the market.

Finally, the dollar remains king with the euro below 1.05, USDJPY just below 150 and the pound making a run at 1.20. Last night, the RBA met and left rates on hold, as widely expected, but the tone of new governor Michele Bullock’s first meeting was seen as somewhat dovish leading to a nearly 1% decline in the Aussie. At the same time, the EMG bloc of currencies is also coming under pressure with declines today on the order of -0.5% across all three regions. There is a term, the dollar wrecking ball, which is quite apt. As it continues to rise it puts intense pressure on countries around the world as they scramble to get dollars to service the trillions upon trillions of dollars of debt outstanding. Nothing has changed my view that this has further to run.

On the data front today, the only release is JOLTS Job Openings (exp 8.8M) a number that remains significantly larger than the number of unemployed. We also hear from Atlanta Fed president Bostic this morning so it will be interesting if he is willing to push back against the ongoing hawkishness.

I see no catalysts to change the current trend in the dollar, so for all you receivables hedgers out there, keep that in mind.

Good luck

Adf