While everyone’s waiting for Jay

And hope he’s got good things to say

No stories of note

Have lately been wrote

And bulls keep on getting their way

The only place that’s not been true

Is China, where, policies, new

Allow new home prices

To make sacrifices

And slide hoping sales follow through

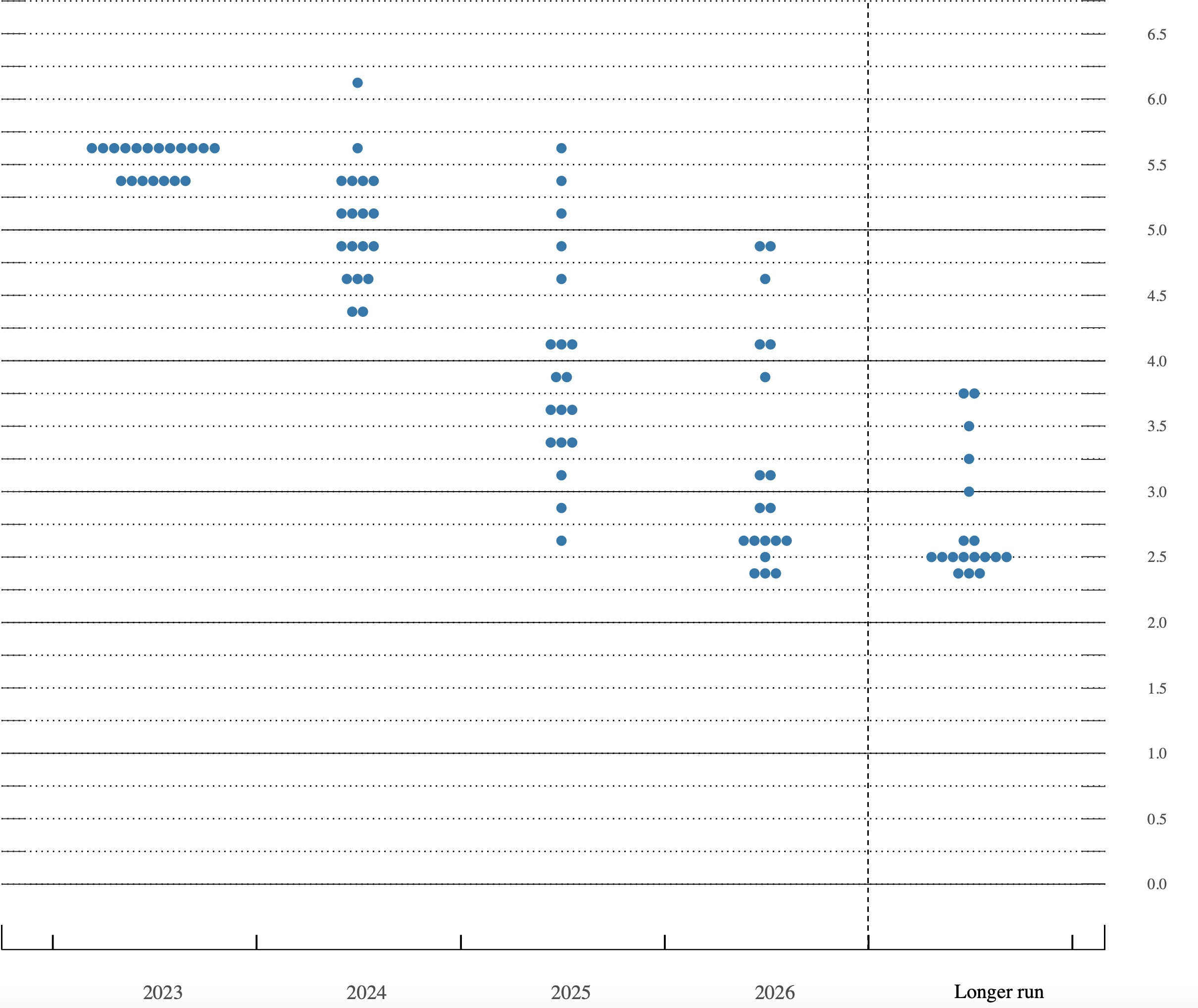

Although there has been a dearth of new information to drive activity, at least with respect to hard data, equity markets are mostly trading higher as the rebound from the early August correction continues. In the US this week, the big news won’t be out until Friday, when Chairman Powell speaks at the Jackson Hole symposium. Elsewhere, while we do see things like both Japanese and Canadian inflation as well as the flash PMI data, so much importance has been attributed to the Powell speech, it is hard for traders to get excited about very much. For instance, early this morning the Swedish Riksbank cut their policy rate by 25bps, as expected, and indicated that there could be another 3 cuts during 2024, but nobody really cared. In fact, the Swedish stock market is lower on the day, simply proving that rate cuts are not a stock market panacea.

However, not every nation is using the same playbook right now, and while Japan may be the biggest outlier, attempting to tighten monetary policy, albeit not as successfully as they had hoped, China is taking a different approach to fiscal and economic policy. As I have mentioned before and has been widely reported for the past several years, the property market in China has been under severe stress. What has become a bit clearer in that time is that much of the Chinese growth miracle was the result of massive overinvestment in housing. The stories about ghost cities, that were built but where nobody lived, which had made the rounds for a while turned out to be true.

In essence, a key driver of the Chinese economy was the property market. Cities and states would sell land to property developers, using the funds to help themselves develop infrastructure. Meanwhile, property developers had a ready market for their homes (mostly condos in high rises) as the Chinese people felt more comfortable with property as a savings vehicle than banks or the stock market. Looking at the performance of the Shanghai Composite below, it is no wonder that people gravitated toward property. After a peak in the summer of 2015, the PBOC devalued the renminbi 2%, stocks fell nearly 50% in the ensuing six months, and have remained at that lower level ever since.

Source: tradingeconomics.com

But for the past four years, since China Evergrande, a major property developer, started to crumble, the desire of the Chinese people to own property has greatly diminished. This has had a major impact on Chinese local government finances as the demand for property they were selling to fund themselves collapsed. At this point, there is a glut of unfinished homes around as developers ran out of funding, so the country is in a bad spot. Not surprisingly, one of the problems is regulatory, as Chinese city and state governments have had restrictions on new home prices, trying to prevent them from declining thus keeping the cycle of new homes funding the cities ongoing. But recently, some major cities and states have relaxed those restrictions and suddenly, new home prices have fallen to make them competitive with resales. Remarkably, sales volumes are picking up. Who would have thunk?

It is ironic that Communist China is defaulting to market pricing activity to help markets clear while in the ostensibly capitalist US, we have a major party seeking to intervene in housing markets to achieve a social goal of home ownership, regardless of the fact it will push prices higher. At any rate, the upshot is that property prices in China continue to decline which is weighing on the share prices of those developers that have not already gone bust. And that is dragging down the entire Chinese stock market and adding to that underperformance we see above.

But you can tell it is a slow day if that is the most interesting story I can discuss! So, without further ado, let’s take a look at the overnight activity as we await the NY open. While the CSI 300 (-0.7%) and Hang Seng (-0.3%) were both in the red, the rest of Asia followed the US higher with Japan (+1.8%) and Korea (+0.8%) leading the way higher. As to European bourses, it is much less exciting as continental exchanges are all +/- 0.1% from yesterday’s close although the FTSE 100 (-0.6%) is under a bit of pressure with the energy sector weighing on the index amid the decline in oil prices. As to US futures, they are essentially unchanged at this hour (7:20).

In the bond market, the doldrums also describe the price action with Treasury yields unchanged on the day and the same virtually true across all of Europe and Asia. This is a situation where it is very clear that both traders and investors are waiting anxiously for Godot Powell.

While oil prices have stopped their slide this morning, they have fallen -6.0% in the past week as the slowing growth/recession story is on the minds of traders everywhere. Concerns over supply on the back of either Ukraine/Russia or Israel/Iran are clearly no longer part of the discussion. It feels to me like that is somewhat short-sighted, but I am not an oil trader. In the metals markets, the barbarous relic (+0.85%) continues to pull all metals higher as it is trading at yet another new all-time high this morning ($2525/0z) and dragging silver (+1.3%) and copper (+0.2%) along for the ride. While the silver movement makes some sense given it has precious characteristics, copper is wholly an industrial metal, so it is giving opposite signals to the oil market. They both cannot be right.

Finally, the dollar remains under pressure, with the euro (-0.1% today, +0.75% this week) pushing toward its end 2023 highs. Remember, back then, markets were pricing 6-7 Fed rate cuts this year, something which is clearly not going to happen. As well, we are seeing the strength in CHF (+0.3%), SEK (+0.3% despite the rate cut and threats of more) and JPY (+0.2%). Interestingly, in the EMG space, ZAR (-0.6%) and MXN (-0.6%) are both under pressure this morning despite the rally in metals markets. As well, I guess given the general malaise in China, it can be no surprise that the renminbi (-0.2%) has fallen. Perhaps a more interesting thing to consider is the fact that the renminbi fixing has been right around current market levels, an indication that pressure on the PBOC to devalue has faded, and a sign that the dollar is losing some fans. In fact, I suspect that this is a key feature of the dollar’s recent softness, and if the Fed does get aggressive, do not be surprised if the market pushes USDCNY to the other side of the +/- 2% trading band around the fix.

On the data front, there is no US data today at all, with the most interesting thing to be released being the Canadian inflation report (exp 2.5%). We do hear from two Fed speakers this afternoon, Atlanta Fed president Raphael Bostic and Governor Michael Barr, but with Powell on the horizon, it would be hard for them to get much traction in my view. As an aside, the Atlanta Fed’s GDPNow has fallen to 2.0% as of last Friday, down nearly 1% last week. This, of course, is another brick in the recession story.

Net, today seems like it will be a quiet one, with markets biding their time until Friday. Of course, given that these days, biding their time means equities will keep rallying and the dollar keep sliding, I think that seems like the best bet for now.

Good luck

Adf