Inflation remains

Ephemeral in Japan

Will Suga as well?

Leadership in Japan remains a fraught situation as highlighted this week. First, three by-elections were held over the weekend and the governing LDP lost all three convincingly. PM Yoshihide Suga is looking more and more like the prototypical Japanese PM, a one-year caretaker of the seat. Previous PM, Shinzo Abe, was the exception in Japanese politics, getting elected and reelected several times and overseeing the country for more than 8 years. But, since 2000, Suga-san is the 9th PM (counting Abe as 1 despite the fact he held office at two different times). In fact, if you remove Abe-san from the equation, the average tenor of a Japanese PM is roughly 1 year. Running a large country is a very difficult job, and in the first year, most leaders are barely beginning to understand all the issues, let alone trying to address whichever they deem important. In Japan, not unlike Italy, the rapid turnover has left the nation in a less favorable position than ought to have been the case.

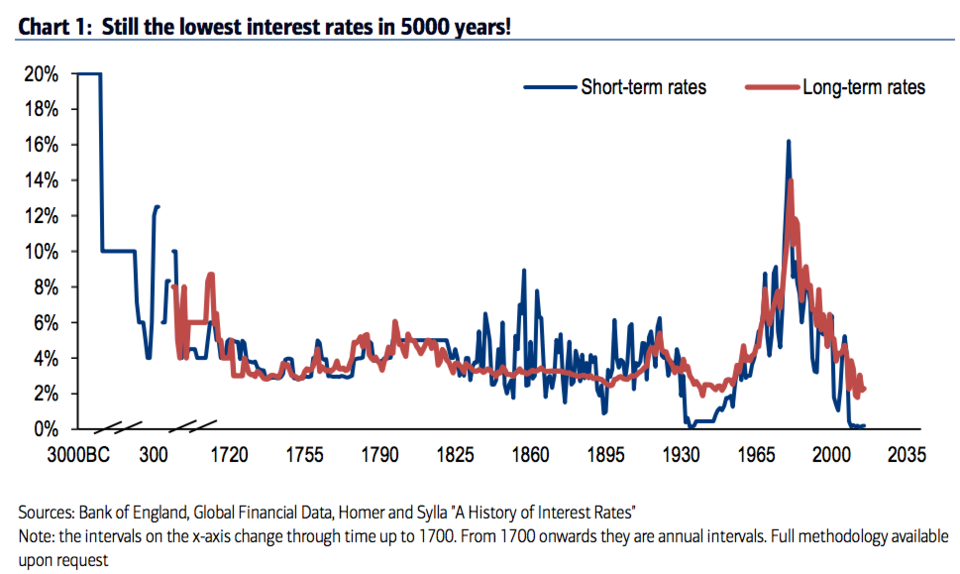

Of course, long tenure is no guarantee of success in a leadership role, just ask BOJ Governor Haruhiko Kuroda. He was appointed to the role in February 2013 and has been a strong proponent of ultra-easy monetary policy as a means to stoke inflation in Japan. The stated target is 2.0%, and for the past 8 years, the BOJ has not even come close except for the period from March 2013-March 2014 when a large hike in the Goods and Services Tax raised prices on everyday items and saw measured inflation peak at 3.7% in August. Alas for Kuroda-san, once the base effects of the tax hike disappeared, the underlying lack of inflationary impulse reasserted itself and in the wake of the Covid-19 pandemic lockdowns, CPI currently sits at -0.2%.

Last night, the BOJ met and left policy on hold, as expected, but released its latest economic and inflation forecasts, including the first look at their views for 2023. Despite rapidly rising commodity prices as well as a slightly upgraded GDP growth forecast, the BOJ projects that even by 2023, CPI will only rise to 1.0%. Thus, a decade of monetary policy largesse in Japan will have singularly failed to achieve the only target of concern, CPI at 2.0%.

Personally, I think the people of Japan should be thankful that the BOJ remains unsuccessful in this effort as the value of their savings remains intact despite ZIRP having been in place since, essentially, 1999. While they may not be earning much interest, at least their purchasing power remains available. But the current central bank zeitgeist is that 2.0% inflation is the holy grail and that designing monetary policy to achieve that end is the essence of the job. The remarkable thing about this mindset is that every nation has a completely different underlying situation with respect to its demographics, debt load, fiscal accounts and growth capabilities, which argues that perhaps the one size fits all approach of 2.0% CPI may not be universally appropriate.

In the end, though, 2.0% is the only number that matters to a central banker, and for now, virtually everyone worldwide is trying to design their policy to achieve it. As I have repeatedly discussed previously, here at home I expect that soon enough, Chairman Powell and friends will find themselves having to dampen inflation to achieve their goal, but for now, pretty much every G10 central bank remains all-in on their attempts to push price increases higher. That means that ZIRP, NIRP and QE will not be ending anytime soon. Do not believe the tapering talk here in the US, the Fed is extremely unlikely to consider it until late next year, I believe, at the earliest.

Delving into Japanese monetary policy seemed appropriate as central banks are this week’s story line and we await the FOMC outcome tomorrow afternoon. In addition to the BOJ, early this morning Sweden’s Riksbank also met and left policy unchanged with their base rate at 0.0% and maintained its QE program of purchasing a total of SEK 700 billion to help keep liquidity flowing into the market. But there, too, the inflation target of 2.0% is not expected to be achieved until 2024 now, a year later than previous views, and there is no expectation that interest rates will be raised until then.

What have these latest policy statements done for markets? Not very much. Overall, risk appetite is modestly under pressure this morning as Japan’s Nikkei (-0.5%) was the worst performer in Asia with both the Hang Seng and Shanghai indices essentially unchanged on the day. I would not ascribe the Nikkei’s weakness to the BOJ, but rather to the general tone of malaise in today’s markets. European equity markets have also been underwhelming with red numbers across the board (DAX -0.35%, CAC -0.2%, FTSE 100 -0.2%) albeit not excessively so. Here, too, apathy seems the best explanation, although one can’t help but be impressed with the fact that yet another bank, this time UBS, reported significant losses ($774M) due to their relationship with Archegos. As to US futures, their current miniscule gains of 0.1% really don’t offer much information.

Bond prices are also under very modest pressure with 10-year Treasury yields higher by 1.1bps and most of Europe’s sovereign market seeing yield rises of between 0.5bps and 1.0bps. In other words, activity remains light as investors and traders await the word of god Powell tomorrow.

Commodity prices, on the other hand, are not waiting for anything as they continue to march higher across the board. Oil (+0.8%) is leading the energy space higher, while copper (+1.1%) is leading the base metals space higher. Gold and silver have also edged slightly higher, although they continue to lag the pace of the overall commodity rally.

The dollar, which had been uniformly higher earlier this morning is now a bit more mixed, although regardless of the direction of the move, the magnitude has been fairly small. In the G10 space, the leading decliner is AUD (-0.2%) which is happening despite the commodity rally, although it is well off its lows for the session. That said, it is difficult to get too excited about any currency movement of such modest magnitude. Away from Aussie, JPY (-0.2%) is also a touch softer and the rest of the G10 is +/- 0.1% changed from yesterday’s closing levels, tantamount to unchanged.

EMG currencies have seen a bit more movement, but only TRY (+0.75%) is showing a substantial change from yesterday. it seems that there is a growing belief that the tension between the US and Turkey regarding the Armenian genocide announcement by the Biden administration seems to be ebbing as Turkish President Erdogan refrained from escalating things. This has encouraged traders to believe that the impact will be small and return their focus to the highest real yields around. But away from the lira, gainers remain modest (KRW +0.25%, TWD +0.2%) with both of these currencies benefitting from equity inflows. On the downside, ZAR (-0.35%) is the laggard as despite commodity price strength, focus seems to be shifting to the broader economic problems in the nation, especially with regard to a lack of power generation capacity.

Data this morning brings Case Shiller Home Prices (exp 11.8%) and Consumer Confidence (113.0), neither of which is likely to have a big impact although the Case Shiller number certainly calls into question the concept of low inflation. With the FOMC tomorrow, there are no Fed speakers today, so I anticipate a relatively dull session. Treasury yields continue to be the underlying driver for the dollar in my view, so keep your eyes there.

Good luck and stay safe

Adf