This morning, investors don’t know

Exactly which way things will go

Unlike in the past

The die isn’t cast

So, some pundits will eat some crow

The question is how will the Fed

Explain how they’re looking ahead?

If Warsh has his way

There’s not much they’ll say

But others, more views, want to spread

As market participants prepare for today’s FOMC statement with the potential for a rate hike, as well as the ensuing press conference, I cannot help but marvel at the recent increase in analysts doing their jobs and being forced to think about what can happen. This is the healthiest thing about this process I believe. It is also a very different approach than some current FOMC members have taken as they seem quite dismissive of the process. For instance, in the WSJ article I cited yesterday, I want to highlight this paragraph;

“Governor Christopher Waller, a former economics professor with a reputation for saying what others won’t, put Warsh on the spot, according to several people familiar with the dinner. What’s the point of all this, he asked. Tell me who you’re putting on these groups, he said, and I’ll tell you what they’ll say. There were no brilliant ideas out there that everyone had somehow missed.”

This is the very definition of hubris, Governor Waller saying he already has all the ideas and, essentially, the task forces are a waste of time. Every member of the FOMC and every one of the 300+ or 500+ or however many PhDs who work there are Neo Keynesians and all see the world in exactly the same way. In fact, they clearly believe that their collective view is the ‘only’ view that is correct. And yet they have failed at their mission statement for more than 5 straight years. My take is they are all terribly frightened that other ideas will not only be more effective, but that they will demonstrate all the mistakes the current FOMC has made prior to Chairman Warsh’s appointment.

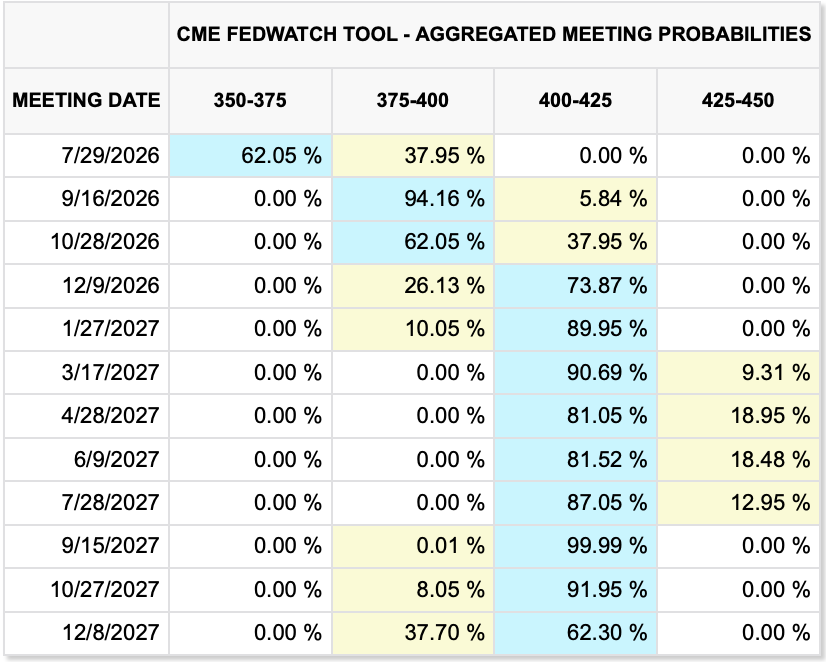

As of 6:45 this morning, the currently priced probability for a hike, as per the Fed funds futures market, is ~38%, an unusual amount of uncertainty on the day of the meeting. However, as you can see from the table below, there is virtual certainty of a hike in September and a high probability of one in December as well. Personally, I disagree they will hike at all this year, but that is what makes markets.

Source: cmegroup.com

It has been two years since there has been this much uncertainty ahead of the meeting, and back then it was a question of 25bps or 50bps as a cut, which I would argue is qualitatively different then determining if there would be any action at all. Otherwise, you need to go back quite a while to see this type of uncertainty, pre-GFC and the beginning of forward guidance.

Meanwhile, the other story of note is the Iranian attack on a US air base in Jordan and renewed fighting in the Gulf region, more than simply in Iran, which has oil prices rebounding sharply from yesterday’s lows, up 5.0% this morning. The biggest problem with the oil market, from a market perspective, is that it is all headline risk, whether more attacks, peace talks or some other comment from either President Trump or Iran. The one thing of which I am certain is that this conflict will not last forever and that when it is over, oil prices will fall back sharply and that over time, the Strait of Hormuz will see its transits decrease to ~5% of the global oil market, making it largely irrelevant to the conversation.

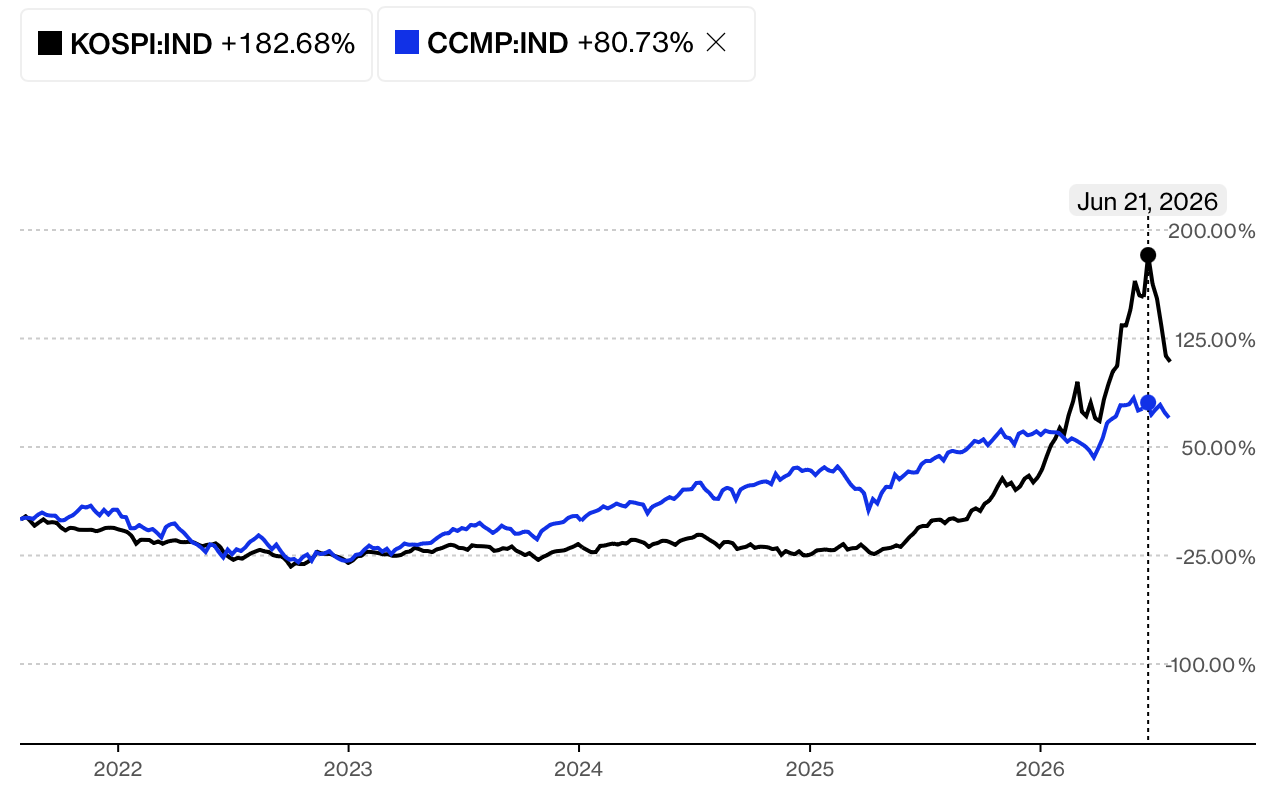

Which takes us to the market activity overnight. Semiconductor companies continue to have some serious problems as SK Hynix reported earnings last night, which, while they beat expectations, their guidance was weaker than expected. Given what we have seen from the sector lately, it cannot be a surprise that the KOSPI fell another -6.0% last night. The chart below shows the relative performance of the KOSPI and NASDAQ over the past 5 years, and I have highlighted the peak. As you can see, the KOSPI massively outperformed (and we thought the NASDAQ was a bubble!) although it is falling back to earth rapidly. In fact, YTD, it is only higher by 34.4%, after having nearly doubled at the peak.

Source: Bloomberg.com

Elsewhere in Asia, Taiwan (-3.8%) also suffered as did the Nikkei (-1.5%) although other Japanese indices held up just fine. China (+0.7%) and HK (+2.0%) had solid sessions and most of the rest of the region performed reasonably well. Remember, once we get past the Fed today, all eyes will turn to Tokyo for the BOJ meeting which comes Friday.

In Europe, it is a mixed picture with concerns over the rising oil price driving some of the concern as we have also seen yields back up a bit. Spain’s IBEX (-1.5%) is the laggard, but that appears to be a profit taking situation as the market there had rallied to record highs recently. Elsewhere, France (-0.5%) is soft while the UK (+0.3%) is picking up slightly after some positive housing news and Consumer Credit activity while the DAX is little changed. As to US futures, at this hour (7:40) they are edging higher, 0.25% or so.

As I mentioned, yields are backing up this morning with Treasuries (+2bps) outperforming vs. European sovereigns which are all higher by between 3bps and 4bps. This seems entirely a reaction to the rebound in oil prices as there has not been enough other news to matter.

Metals markets are having another session where the relationship with oil is askew. Gold is unchanged this morning while silver (+1.0%) has edged higher despite the oil rally. But these metals remain in a downtrend trading in virtual lockstep as per the chart below.

Source: tradingeconomics.com

Finally, the dollar is mixed this morning, depending on which counterpart you watch. The DXY (-0.1%) is a touch softer although there has not been much movement at all in the euro, pound or yen. In the G10, AUD (-0.5%) is the worst performer after inflation data overnight was cooler than expected and the probability of a rate hike fell even further. NOK (+0.3%) is responding to oil’s rebound and everything else is minimal. In the EMG, ZAR (-0.5%) is the laggard du jour on the higher oil prices although in fairness, it is holding its own vs. the gold price, having only declined about 2.5% in the past six months despite the sharp, 25% decline in the price of gold.

You can be sure that after the FOMC today, all eyes will turn to the BOJ and the yen as the next major discussion point for the FX markets.

And that’s really it today. The only data is the EIA oil inventories with a small draw expected. And of course, the FOMC this afternoon. My take is not much will happen ahead of 2:00, but remember, a large portion of the market has their bet wrong as to the outcome, so if nothing else, expect some volatility in the aftermath.

Good luck

Adf