One time on the FOMC

A guy was as ‘hawk’ as can be

But now that he’s gone

His view’s to call on

Chair Jay to cut, times, one, two, three

You may remember Jim Bullard as the president of the St Louis Fed for a very long time. While in that role, he had become the most hawkish FOMC member on the committee, consistently decrying the rise in inflation and the Fed’s delayed response during the ‘transitory’ phase. But he retired from that role last year to join Purdue University as president, and more power to him. The interesting thing is that despite the fact he is no longer part of the discussion, he feels it necessary to get his opinions out there anyway. Last night, at a conference in Hong Kong he explained that the Fed has stuck the landing, the soft landing that is, and that three cuts are appropriate.

The first thing I will point out is this is proof positive that FOMC members speak far too frequently. The fact that we know the names of ex-regional Fed presidents, as well as their monetary policy stances, seems crazy. We have already seen the damage that forward guidance has inflicted on the economy when after several years of ‘rates will never go up’, the Fed pivoted to hiking aggressively and blew up a number of regional banks while putting the commercial real estate market in dire straits. My observation is that these members have become so conditioned to being in the spotlight, and have grown to like it so much, that they cannot stop even when their views have no bearing on the conversation.

The second thing is that these comments seem to run counter to the evolving views of both recent Fed speakers and market pricing. A conspiracy theorist might think that the administration requested he add to the discussion because it seems like the Fed is moving away from that position, a position that the administration deems more beneficial to its reelection chances.

In the end, despite the headlines that drove this discussion, I don’t believe the market really cares very much what Jim Bullard has to say anymore. Tomorrow’s CPI is so much more important which is likely why there has been no discernible movement in anything in the wake of this ‘news.’

Ueda remains

More like a kite in the wind

Than a solid rock

Last night, in testimony to the Japanese parliament, BOJ Governor Ueda once again tried to imply that tighter policy could be coming but was unwilling to commit. He said, “We have to consider reducing the degree of monetary easing if the underlying price trend rises along with our outlook. We will carefully consider this at every policy meeting as it depends on incoming data.” So, does that mean they are going to tighten soon? Who knows! Funnily enough, I think that is a much better stance than the current Fed/ECB/BOE policy of trying to be so deterministic. At least he has not promised anything at all. Of course, in today’s zeitgeist, a central bank not promising is seen as quite the negative.

The upshot is that the lack of commitment for further policy tightening has focused attention on the fact that the yen, while unchanged this morning, remains just pips away from its 35-year lows (dollar highs) and the big round number of 152.00. Many in the market believe that the MOF is going to intervene if the dollar touches that level, although that view is starting to lose some adherents, at least based on a recent assessment of options positioning. Personally, I am inclined to believe FinMin Suzuki that their concern is not the level so much as it is the pace of decline and volatility. Say what you will about the yen being weak, but since March 19, the range for USDJPY has been less than 1%, hardly a sign of volatility.

Source: tradingeconomics.com

But that is all the barrel scraping I am going to do this morning to find stories of note. As we await tomorrow’s CPI data, markets are collectively holding their breath. Well, equity and FX markets are anyway. The inflation story is clearly impacting both bonds and commodities so let’s take a look.

After yesterday’s complete lack of movement in the US equity markets, the Nikkei (+1.1%) rallied, arguably on the idea that tighter policy is not a promise. The rest of Asia, though, was far less upbeat with a mix of modest gainers and losers. That also describes the European session, with some gainers and some laggards, although the laggards are a bit worse, down about -0.5% on average. US futures, though, are still in the doldrums, trading either side of unchanged all evening.

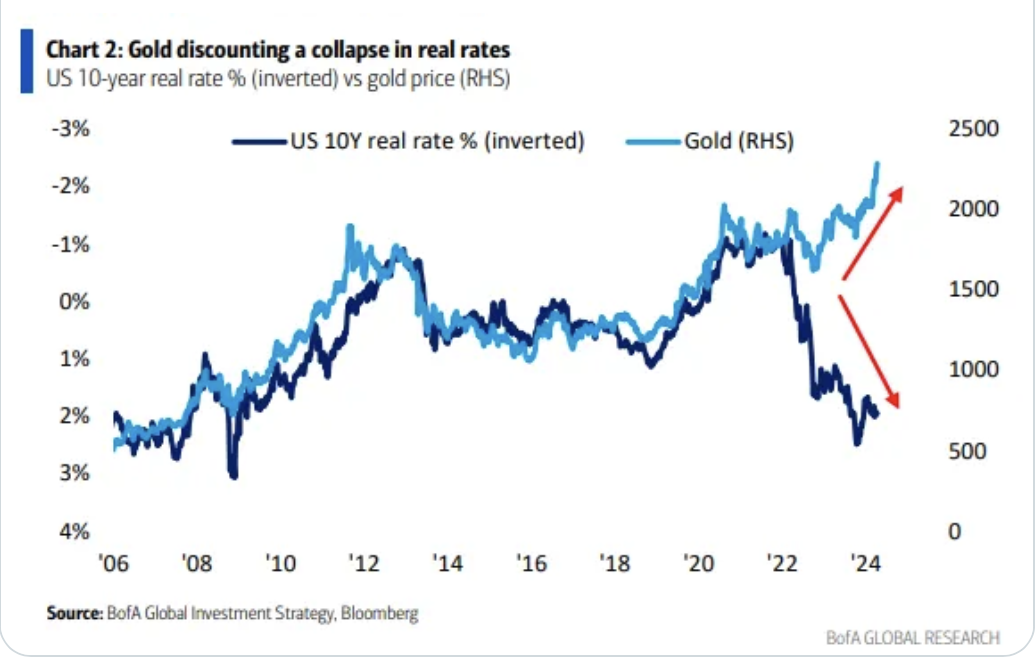

Bonds are a bigger story as yesterday saw the 10-year Treasury yield touch 4.465% although it has since backed off a few bps and is now right at 4.40%. However, the trend remains very much higher for US yields as market participants appear to be responding to several different concerns. The first is that the US economy continues to outperform, as evidenced by Friday’s blowout payroll data, so the need for rate cuts is dissipating, but the second is a bigger issue, the idea that monetary policy activities since the pandemic alongside massive fiscal stimulus has impugned the longer-term value of all fiat currencies and securities denominated in those currencies. This has investors looking elsewhere for effective stores of value like commodities and precious metals and is forcing a rethink of where interest rates are going to settle in the long-term. The Fed’s way to describe this is that the long-term neutral rate is much higher than had previously been thought. Recall, the last dot plot showed the long-term rate rising from 2.50% to 2.65%. Look for that number to continue to rise going forward and that will not help the bond market.

Speaking of commodities, while oil started the day lower yesterday, it rebounded and closed higher on the session by a small amount. This morning it is little changed, but one of the stories that had led to lower prices, a reduction in stress in the Middle East, seems to have faded this morning. At this point, there is no evidence that we have seen the top in oil prices. You won’t be surprised to hear that the metals markets are continuing their rally, with gold (+0.7%) making further new all-time highs while copper (+0.4%) continues its run and has crested $4.30/pound. There is ample room for these to continue higher, especially gold given the growing question of the value of holding fiat currencies at all.

Finally, in the fiat realm, the dollar is a touch softer this morning, although that seems a response to the commodity price strength we are seeing. Or perhaps, commodities are rallying because of the weak dollar although my sense is the commodities are driving things. At any rate, ZAR (+0.8%) is the leader in the clubhouse but we are seeing strength in AUD (+0.3%) and NZD (+0.5%) as well. Too, BRL (+0.3%) is showing a little strength after its slow decline all year. As to the euro and pound, both are slightly firmer and the yen remains unchanged, as discussed above.

On the data front, we have already received the NFIB Small Business Optimism Index, printing at 88.5, its lowest level in more than 12 years and well below expectations. The dichotomous economy continues to confound, with some aspects seeming to be doing well, while others are lagging badly. There are no Fed speakers on the docket today, so I expect there will be a bit of toing and froing as we all look forward to tomorrow’s CPI print.

Good luck

Adf