Said Powell, the path is still clear

For cutting three times all this year

Though data’s been hot

We’ve certainly not

Decided no rate cuts are near

This was, of course, warmly embraced

By traders who bought shares post-haste

But do not forget

The very real threat

The dollar will, thus, be debased

Chairman Powell regaled us once again and yesterday he sounded far more like the December Powell than the March Powell. Notice in his comments that he has essentially dismissed the recent hotter than expected inflation data and instead insists they are on the right road to achieve their goal. He explained [emphasis added], “The recent data do not…materially change the overall picture, which continues to be one of solid growth, a strong but rebalancing labor market, and inflation moving down to 2% on a sometimes bumpy path.” And maybe he is correct. Maybe the January and February data points are the outliers, and the rate of inflation is going to reverse back lower.

But he has to know that when he coos like a dove, risk assets are going to rally sharply. The difference today is that the bond market is beginning to ignore all the Fed talk as we see despite these dovish tones, yields remain at their highest level (4.36%) since November, with no downward movement at all. In fact, perhaps the real concern that the Fed should have is that gold continues to rise strongly almost every day, trading to $2300/oz and showing no signs of slowing down.

I have been consistent in my view that if the Fed cuts despite the ongoing better than expected data the result would be a sharp decline in the dollar, a sharp decline in bond prices (rise in yields) and a sharp rise in commodity prices. I have also indicated that, at least initially, I expected equities to rally, but their medium-term outlook was more suspect. Well, yesterday, that was exactly how the market behaved with metals markets screaming higher, stocks trading well and bonds lacking any bids.

Yesterday’s data showed the ADP Employment number jumping 184K, well above expectations of 148K, but the ISM Services data was a bit soft at 51.4 (exp 52.7) and more importantly, the Prices sub-index fell to 53.4 down 5 points from last month. That was the set-up for Powell’s comments, and he jumped on board. It remains abundantly clear that the Fed is desperate to cut rates almost regardless of the economics. My take is the reason has more to do with the debt situation than the presidential election although there is a third possible explanation as well, a too-strong dollar.

Consider the following: the dollar remains the world’s reserve currency and the currency most widely used in trade and financing activity. Because of this, a large majority of the world’s total outstanding debt of approximately $350 trillion is denominated in dollars despite the fact that most companies and countries are not USD functional. The result of this situation is that all those non-USD functional debtors need to buy dollars in order to service and repay that debt. If you were looking for an underlying reason as to the dollar’s broad strength, this is another candidate in the mix.

As such, it is entirely realistic that Chairman Powell is feeling intense pressure from the international community to cut interest rates to weaken the dollar. While I don’t expect that a Plaza Accord type agreement is in the offing, it is possible that Powell sees this as an achievable outcome and one that would not result in global chaos. However, whatever the reason, as we watch commodities rally, while the dollar and bond market sell off, we are watching Fed credibility dissipate.

Ok, let’s peruse the overnight session to see how markets have responded to the dovish version of Powell. While US equities sold off late in the day yesterday, minimizing gains, the same was not true overseas. Though Chinese markets were closed for the Ching Ming Festival, pretty much everywhere else in Asia saw equity rallies of substance with the Nikkei’s 0.8% rise a good proxy for all. Meanwhile, in Europe the screens are all green as well, although not quite as impressively, more on the order of 0.25% – 0.5%. This performance is in accord with Services PMI data that was released this morning showing broadly better than expected outcomes across all the major nations as well as the Eurozone as a whole. Finally, US futures at this hour (6:45) are firmer across the board by 0.25%.

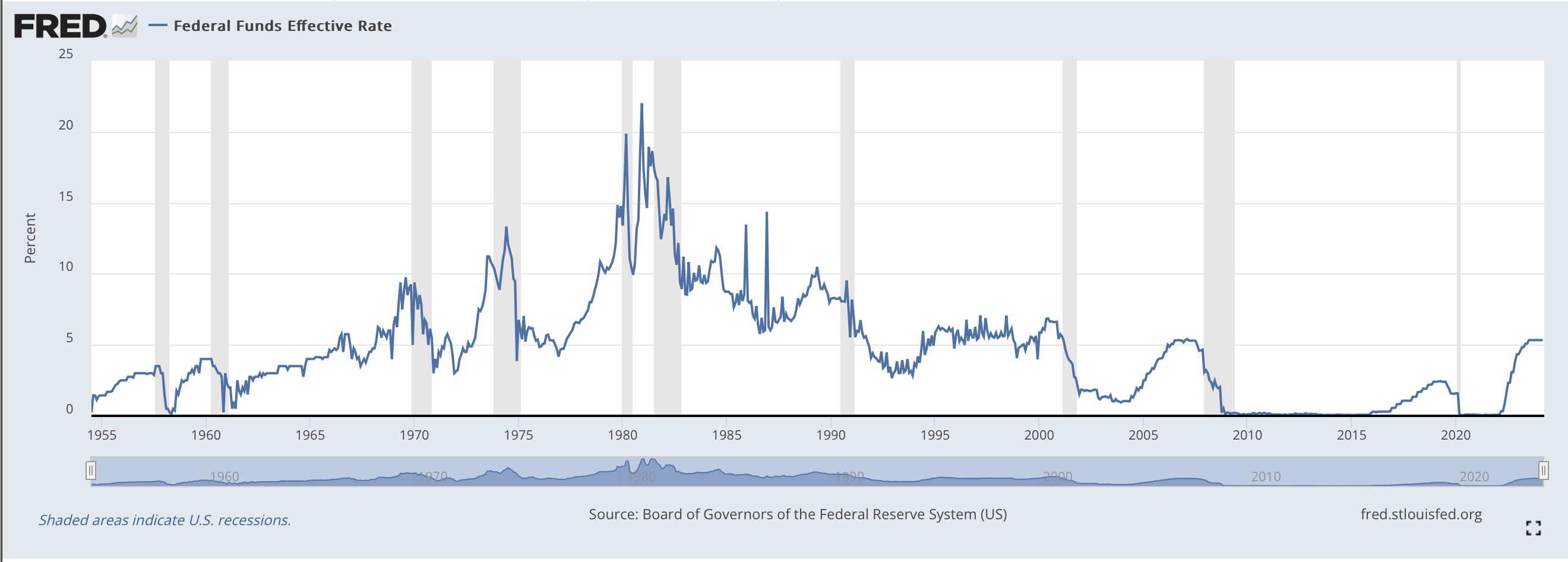

In the bond market, Treasury investors do not see the benefits of Powell’s dovish turn amid still high inflation. The ADP data is certainly a concern as all eyes turn toward tomorrow’s NFP report. In fact, what we are seeing is a bit of a curve steepening (less inversion) with the 10yr-2yr inversion now down to -31bps from its -40bp level that had been steady for the past several weeks. However, European sovereign yields are all a touch lower this morning, down between 2bps (Germany) and 6bps (Italy) as comments from Robert Holtzmann, Austrian central bank chief and the most hawkish ECB member finally conceded that a cut in June could be appropriate. Of course, now there is talk of a cut at the end of this month weighing on yields. Meanwhile, JGB yields crept higher by 1bp, but remain at 0.75%, showing no signs of running away higher.

Oil prices (-0.3%) are consolidating this morning after yet another positive session yesterday with WTI now trading above $85/bbl and Brent crude just below $90/bbl. OPEC reconfirmed that production would remain at current levels and two nations, Iraq and Kazakhstan have promised to cut back to bring their numbers back in line with quotas. As well, EIA data showed a build in crude but a much larger draw in gasoline stocks (which is why prices are rising at the pump) adding support to the market. Gold (-0.1%), too, is consolidating this morning but the trend remains strongly higher. At the same time, copper (+0.5% today, +5.75% this week) is continuing its rapid rise and is back to levels last touched in January of last year. It appears the broader growth story remains a driver here, especially with the idea that the Fed may be cutting rates and goosing it further.

Finally, the dollar is under a bit more pressure this morning after Powell’s dovish stance, sliding against most of its counterparts in both the G10 and EMG blocs. AUD (+0.65%) and SEK (+0.65%) are the leaders in the G10 space with most of the rest of the bloc following higher. One exception is CHF (-0.4%) which has fallen after CPI there fell to 1.0% Y/Y (0.0% M/M) and encouraged traders to bet on faster rate cuts from the SNB. The yen (-0.1%) too, is not following suit, which perhaps indicates we are seeing a reversion to the classic risk-on stance (higher stocks and commodities, weaker dollar and havens), at least for today. In the emerging markets, most currencies are firmer led by (CLP +0.6% on copper strength) and HUF (+0.4%) which is simply demonstrating its higher beta relative to the euro, although there are key currencies that are little changed like MXN, BRL and CNY.

On the data front, this morning brings the weekly Initial (exp 214K) and Continuing (1822K) Claims data as well as the Trade Balance (-$67.3B). As well we hear from five more Fed speakers (Barkin, Goolsbee, Mester, Musalem, and Kugler) to add to yesterday’s comments. The question I would ask is, even if some of them sound more hawkish, given what we just heard from Powell, will it matter? For instance, yesterday, Atlanta’s Raphael Bostic reiterated his stance that one cut was likely all that was necessary this year and nobody heard him speak, effectively. We would need to hear every one of them vociferously defend the current stance and call for zero cuts to have an impact. And that ain’t happening!

With Powell showing his dovish feathers, the dollar is going to remain under pressure while asset prices perform. I think that’s the most likely outcome ahead of tomorrow’s data, where a particularly hot number could change things. But we will discuss that then.

Good luck

Adf