The central bank mantra worldwide

Is ‘flation is set to subside

So, rate cuts remain

The path they’ll maintain

With alternate views all denied

But weirdly, despite these strong views

The data just seems to refuse

To show ‘flation slowing

In fact, it keeps showing

Their comments were kind of a ruse

Ask any central banker around the world their view on the path of inflation and I assure you they will claim it is slowing and will return to their 2% goal over time. They will point to obscure signals some months, and headline inflation prints other months, but nothing will dissuade them from this view.

Now, I am just an FX guy and so clearly don’t have the same expertise in econometric modeling that all those PhD’s in all those central banks have but…it does sort of seem like all their models simply have 2% as one side of the equation and they use goal-seek in Excel to create their outcomes. And anyway, how did 2% become the “natural” rate of inflation? After all, that inflation rate was literally pulled out of thin air by RBNZ Governor Donald Brash back in 1990 and has been copied by virtually every other central bank around the world since.

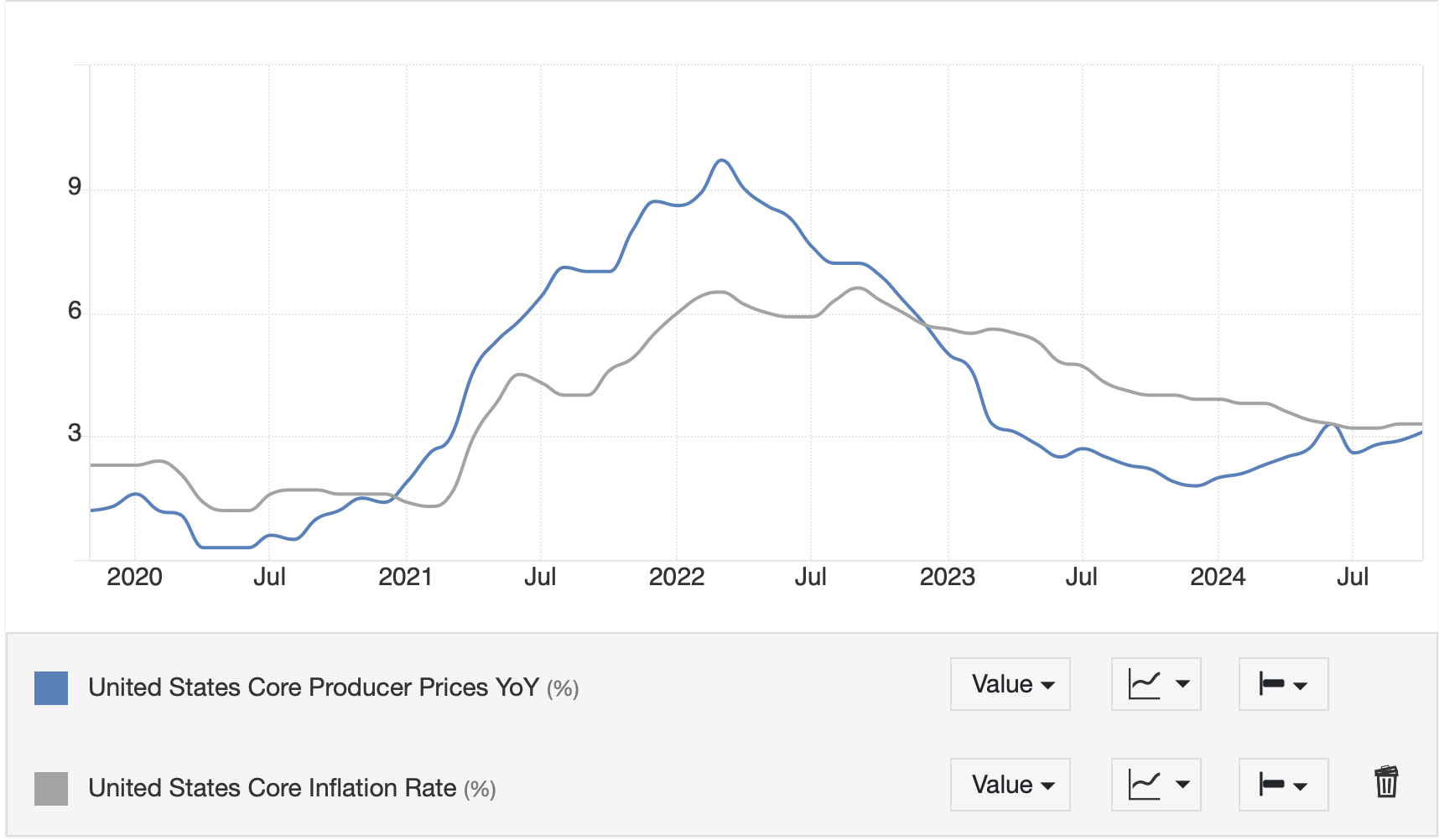

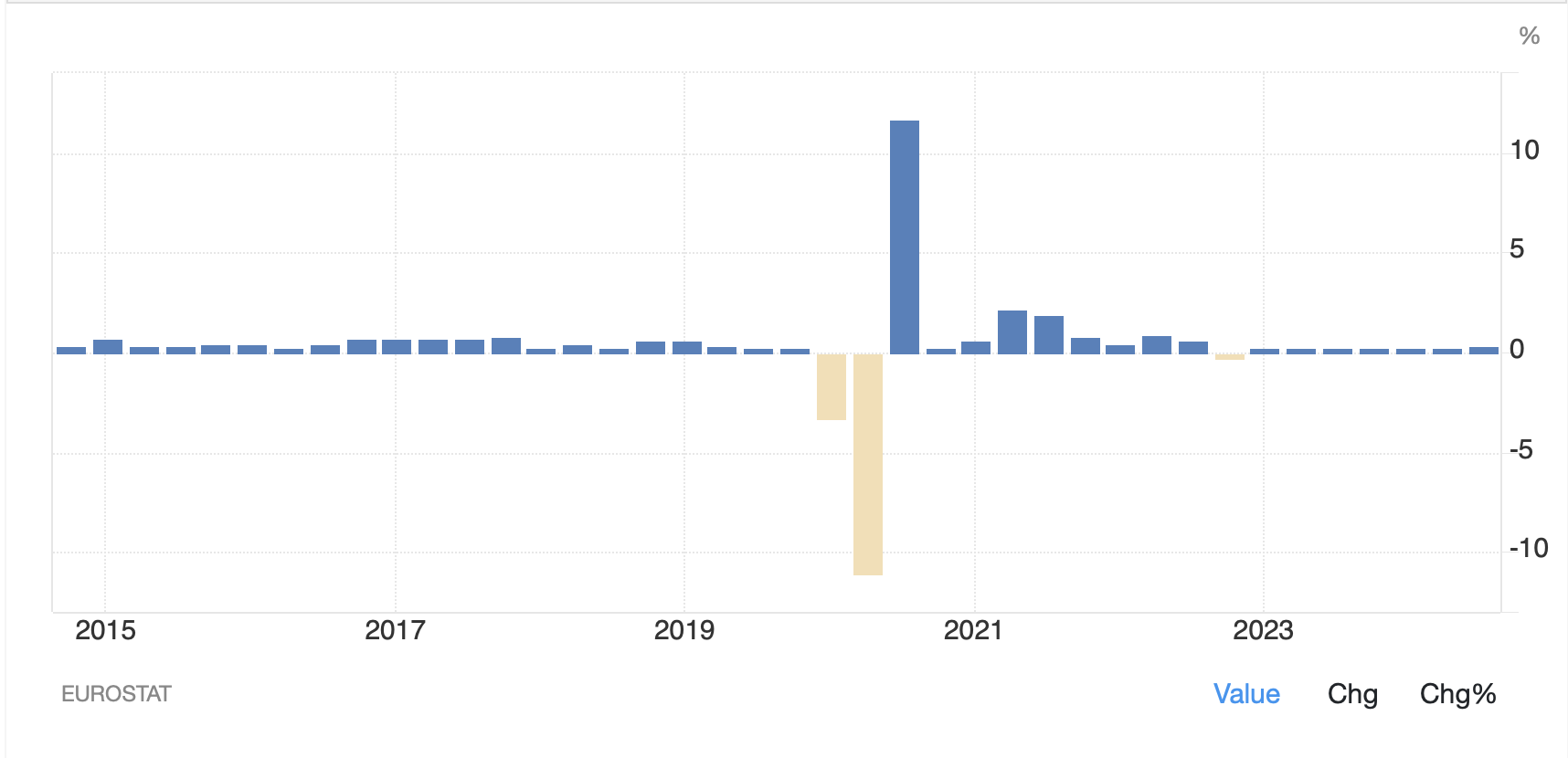

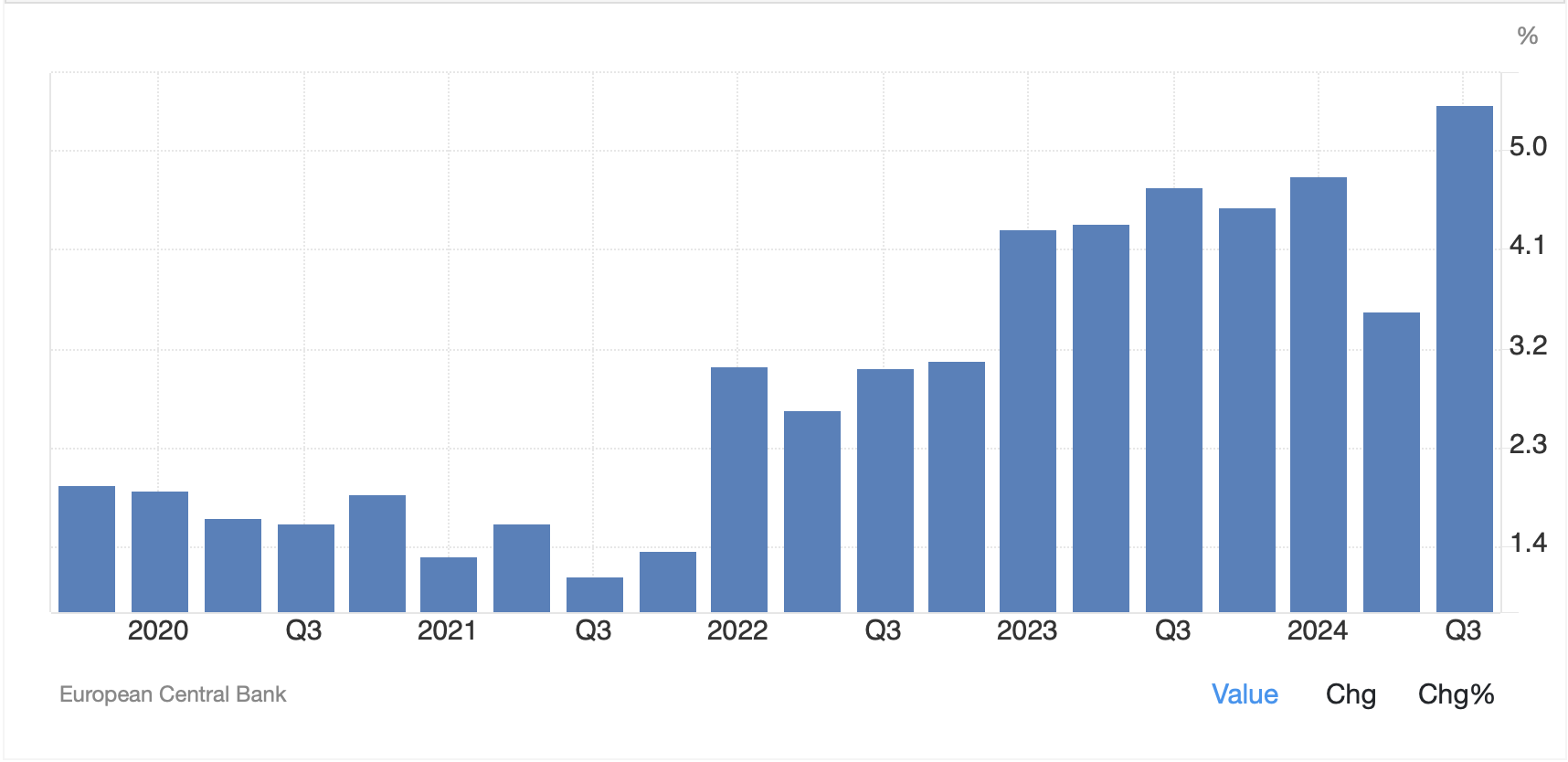

But, whatever the history, that is the goal and recent data from countries throughout the G10 show that prices are not really converging to this rate. The UK is the latest to release data with the Headline CPI rising 2.3%, a tick more than expected and Core rose 3.3%, 2 ticks more than expected. It seems that the same problems the Fed is having with services ex-shelter are being felt in many places around the world. This is the portion of the CPI basket that is most directly impacted by wages and wages continue to rise (which is a good thing for most people), just not necessarily quickly enough to keep up with inflation. For example, Eurozone Negotiated Wage Growth rose 5.42% in Q3, its fastest rise since the Eurozone was formally created as per the chart below. It strikes me that the ECB is going to find it very difficult to push prices lower absent causing a deep enough recession where layoffs are widespread, and wages fall. And my guess is that is not one of their goals.

Source: tradingeconomics.com

Of course, we all know the situation here in the States, where the CPI data has formed a base above 3% and seems far more likely to rise than fall, also absent a major recession.

Ultimately, it begs the question why we care about this data (other than the obvious reason we all have to live with rising prices) from a market perspective. To the extent that monetary policy is a key driver of markets around the world, and relative monetary policy is an important input into the value of different currencies, the relative inflation rates are a critical piece of the puzzle to try to figure out what is happening and how one can hedge their exposures. So, if inflation rates everywhere are slow to return to that sacred 2% level, then different central banks are going to behave differently in order to achieve their goals.

For instance, earlier this week we saw the Minutes of the RBA’s meeting where they were distinctly hawkish regarding the fact that inflation does not seem to be falling the way they hoped prayed for expected based on their models. As such, markets adjusted their pricing for interest rates to remain higher for longer and that helped support the AUD on a relative basis. This morning, amidst a broad-based dollar rally, the pound (-0.25%) is the second-best performer in the G10, after the dollar, as the higher than forecast CPI data has traders expecting the BOE to slow the pace of rate cuts to address the issue. And this is why we care.

Remember, too, while there is currently an extraordinary amount of digital ink being spilled as pundits around the world try to anticipate what President-elect Trump is going to do regarding fiscal policy and tariffs and how that is going to impact relative trade flows as well as monetary policy responses to these actions, my take is that is an enormous waste of time. The first thing we know is that nobody, not even Trump himself, really knows how this is going to play out as there are so many potential paths down which he can tread. And second, the situation seems akin to Keynes’ famous analogy to a beauty contest where you need to select the person who the crowd thinks is the most beautiful, not the one you may think fits that description. In other words, trying to predict the outcome implies understanding what everyone else is expecting, and right now, expectations are widely disparate.

It is for this reason that hedging is so critical, and having a consistent hedging plan is key. None of us has a crystal ball, and managing risk is far more about mitigating big drawdowns than capturing big gains.

Ok, a little long-winded this morning so let’s zip through the overnight market activities. Mixed is the best description for yesterday’s US session, with the DJIA sliding while the other two major indices rallied a touch. It also describes the Asian session overnight as the Nikkei (-0.2%) slipped along with Australia (-0.6%) while China and Hong Kong both managed modest 0.2% gains. The PBOC left Loan Rates unchanged last night, as widely forecast and I expect they will not do anything until Trump is in office and has his team in place. As to European bourses, they are all in the green this morning, but just barely so, with gains between 0.1% and 0.3%, hardly exciting. As to US futures, they are edging higher this morning by 0.1% or so as the most important news in the world, Nvidia earnings, are due to be released after the close today.

In the bond market, yesterday’s yield declines are being almost perfectly reversed this morning with Treasury yields higher by 3bps and European sovereign yields rising between 4bps and 6bps. Certainly, the higher inflation print in the UK has not helped sentiment and I suppose there is some reaction to some of Trump’s recently announced Cabinet picks, notably the Commerce Secretary choice, Howard Lutnick, who is by all accounts a major proponent of tariffs.

In the commodity markets, oil (+0.5%) is holding its recent gains although WTI remains below $70/bbl. My take is that a Trump presidency is going to be quite negative for the price of oil as reduced regulations on drilling along with access to more sites will see production increase. As to the metals markets, gold (-0.2%) has slowed its recent rebound, as has silver (-1.2%) although copper (+0.6%) is holding its own this morning. The last week has seen the metals markets recoup a substantial portion of the recent drawdown although all of them remain lower than levels seen a month ago.

Finally, the dollar is back in fine form this morning, rising against all its counterpart currencies. The laggards in the G10 are NOK (-0.8%) and SEK (-0.8%) although the euro (-0.5%) is under severe pressure again as it continues to probe toward the key 1.0500 technical level. In the EMG bloc, HUF (-1.0%) is the laggard although most of the bloc is softer by between -0.3% and -0.5%. We continue to see CNY (-0.25%) slide as the dollar pushes back above 7.25 this morning. That is the level that has held things in check for the past 5 years, and many believe that when Trump takes office, we could see the renminbi weaken much further once tariffs are imposed. Of course, one of the things the PBOC has been fighting for a long time is a chaotic slide in the renminbi as that does not suit President Xi’s goals of stability to encourage more use by other parties.

The only US data today is the EIA oil inventories with a modest build expected after last week’s large draws. Yesterday’s housing data was a touch weaker than expected and we have heard very little from Fed speakers since Powell explained he was sauntering toward the next rate cut rather than hurrying there. As of this morning, the market probability of that cut happening in December sits at 57%, which is the lowest it has been since the previous meeting.

There are many cross currents in the market narrative at this time with nothing remotely clear. The one thing we know about Donald Trump is he has the capacity to surprise absolutely everyone with his actions, regardless of his words. Again, this is what informs us that a consistent hedging program is the only way to mitigate against major surprises.

Good luck

Adf