Said Powell, the progress is real

And though there are many with zeal

To quickly cut rates

Our dual mandates

Explain we’ve not yet sealed the deal

Meanwhile, as the holiday nears

Investors, ‘bout some stuff, have fears

The UK will vote

And Labour will gloat

Then Payroll, on Friday appears

At this stage, the Payroll report

Is forecast to, last month, fall short

But if the U Rate

Once more does inflate

The doves, for rate cuts, will exhort

The Fed whisperer himself, the WSJ’s Nick Timiraos, did an excellent job covering the Chairman’s speech in Sintra, Portugal at a big ECB confab yesterday, so let me give it to you straight from him. [emphasis added]

“We’ve made a lot of progress,” Powell said Tuesday on a panel with other central bankers at a conference in Portugal. After serious shortages two years ago that sent wages up sharply, the labor market has “seen a pretty substantial move toward better balance,” he said.

The Fed leader’s remarks underscored a sense of cautious optimism that had faded after disappointing inflation readings in April. He alternately said the economy had made “significant progress,” “real progress” and “quite a bit of progress” toward cooler inflation with stable growth.

Apparently, progress toward their stated goals has been substantial. And while that is fantastic, he also mentioned, later in his speech, that they were now also looking far more carefully at the labor market, which is starting to slow down. “You can see the labor market is cooling off, appropriately so, and we’re watching it very carefully.” You may recall that SF Fed president Daly also focused on the labor market late last week and I am confident that it is on every FOMC members’ radar.

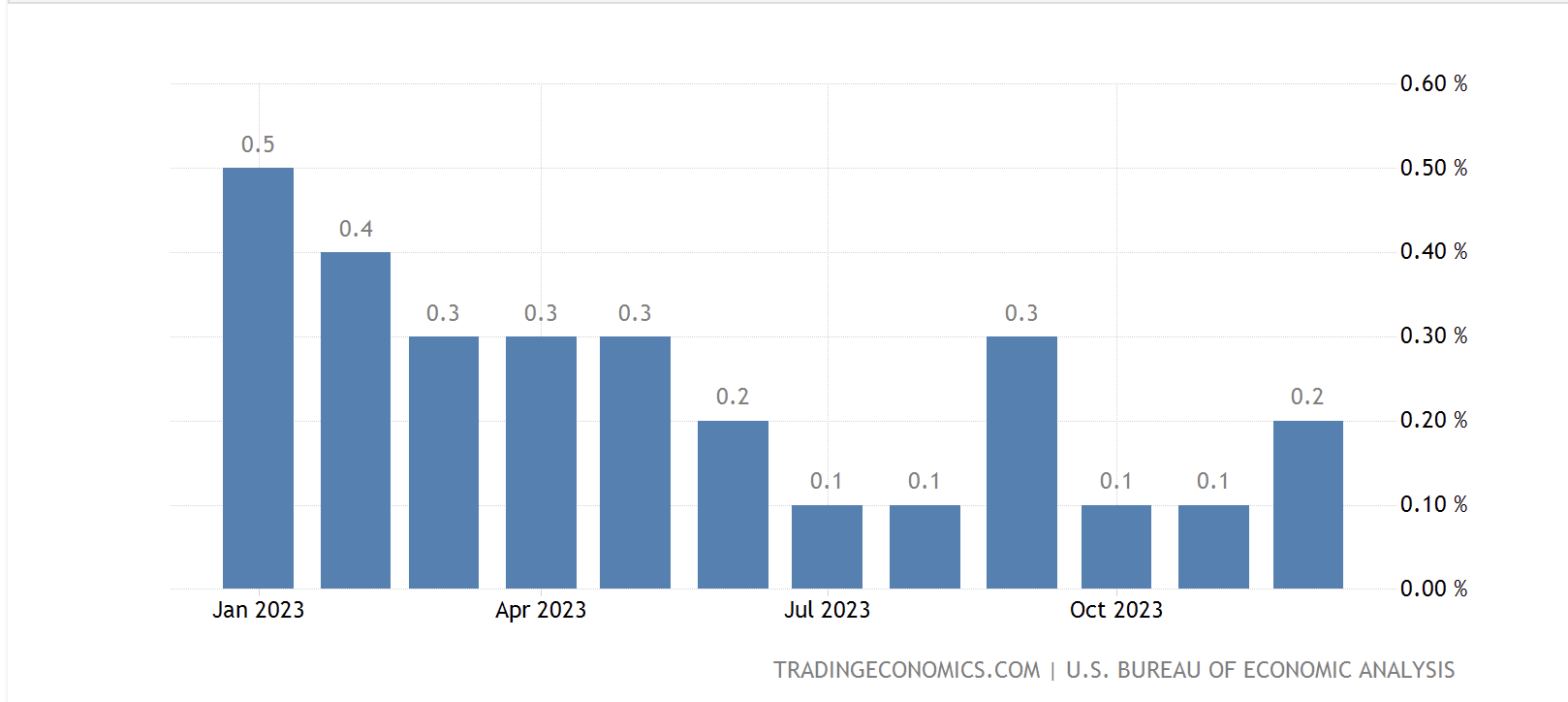

Of course, that’s why Friday’s Payrolls report is going to be so important. Arguably, while the NFP data gets all the press, the Unemployment Rate is really going to matter this time as it ticked up to 4.0% last month. A rise from here will start to call into question just how strong the labor situation remains. For instance, while yesterday’s JOLTS data showed a modest rise to just over 8M job openings, that is after the previous month’s data was revised down substantially, by nearly 240K jobs. One of the things about the Unemployment Rate is that once it starts to move in one direction or the other, it tends to really build momentum for a while. As you can see from the long-term chart below, once it starts to rise, it tends to go a lot higher.

Source: tradingeconomics.com

I have maintained that the payrolls have been a key all along as it is quite easy for the Fed to parry complaints from Congress about ‘too high’ interest rates if the job market is tight. But if it starts to loosen too quickly, Congress will be howling every day and night and make the Fed’s life quite miserable. As such, my eye is on the Unemployment Rate rather than NFP come Friday.

Now, this is not the only story around, but from a market perspective, I believe it is the most important by far. However, let’s touch on some others before highlighting the ongoing risk rally. While most of the oxygen in US newsrooms is consumed by the debate on whether President Biden is fit to, and will, be the Democratic nominee, there are several other key elections coming this week.

Tomorrow, the UK heads to the polls (was the July 4th date chosen to commemorate the last big English loss?) where the current Tory government, led by PM Rishi Sunak, is forecast to be decimated by the voters. Apparently, the good folks of the UK are fed up with the same inflation and immigration issues that are apparent elsewhere in the Western world and are looking for a change. Interestingly, a look at UK markets doesn’t really indicate that investors are greatly concerned over the change as Gilt yields, the FTSE 100 and the British pound have all been range trading for the past month. Certainly, there is no indication a Labour government is going to be fiscally responsible, but they have promised to raise taxes to try to fund their spending. In the end, I don’t see the change in government having an immediate impact on financial markets in the UK. Rather, I expect that the US story on rates and economic activity is still going to be the main driver of things.

Come Sunday, the French head back to the polls for the second round of their parliamentary election and virtually every story you can read about it describes the lengths to which the coalition of left-wing parties and the current Macronist parties are going to try to prevent Marine Le Pen’s RN party from gaining a working majority. I find it instructive that rather than considering why so many people were drawn to the RN message of restricting immigration and enhancing public safety, the other parties simply demonize the RN as a reincarnation of the Nazis. (sounds familiar, no?). The current market narrative seems to be that the RN will not be able to capture an absolute majority by themselves with the result that a caretaker government will be appointed with limited powers. This has been seen as a great leap forward from the fear of an RN led government, and so we have seen French equity markets rebound from their worst levels last week, while French OAT yields have compressed vs. their German counterparts by about 15bps from the widest levels seen just before last Sunday’s first round votes.

In a related note, this morning I have seen several articles describing the recent rise in US yields as a response to the presidential debate last week, where suddenly there is concern that Mr Trump may win and spend trillions of dollars, rather than a Biden win where the government would spend trillions of dollars. Frankly, there is no indication that either party is going to rein in spending, it is far more a question of their spending priorities. But that is the story that is all over the press this morning.

Ok, a quick look at the overnight session shows that yesterday’s US equity rally was largely followed by shares in Asia (Nikkei +1.25%, Hang Seng +1.2%) although Chinese shares remain lackluster. In Europe, as well, shares are higher across the board with the CAC (+1.55%) in Paris leading the way on this renewed narrative of a caretaker government. I suppose if the RN does win a majority that come Monday, French shares, and most of Europe as well, will see sharp declines. As to US futures, at this hour (7:30), they are edging very slightly higher, just 0.1%, ahead of this morning’s data dump.

In the bond market, Treasury yields are unchanged this morning, but Europe has seen virtually all sovereigns rally slightly vs. Bunds as the French narrative seems to have longer tails than one might imagine. So, spreads are narrowing a bit. The one consistency in bond markets, though, has been Japan which saw yields edge higher by another basis point overnight and are now 18bps higher in the past two weeks. Remarkably, despite the rise in Japanese yields, the yen continues to get punished daily.

In the commodity markets, oil is little changed on the day, but has rallied more than 2% in the past week on rumors of a significant inventory drawdown to be reported later this morning, as well as the pending shut in of production in the Gulf of Mexico. However, metals markets are rallying this morning with both precious (Ag +0.6%, Ag +1.8%) and base (Cu +1.6%, Al +0.7%) finding support amid the equity/risk rally and the dollar’s softer tone today.

Speaking of the dollar, other than the yen (-0.25%) which is now pushing to 162.00, the rest of the G10 bloc is modestly firmer, between 0.1% and 0.25%. Meanwhile, in the EMG bloc, ZAR (+0.65%) is again the biggest mover, rallying on metals strength along with broad dollar weakness. One must be impressed with the ongoing volatility in the rand, which seems to be the leading mover in one direction or the other every day. However, away from that, while most EMG currencies are a bit firmer, the movement has been much less dramatic.

On the data front, it is a busy day as tomorrow’s holiday has forced much info onto today’s calendar. As well, since there will be no poetry on Friday morning, I will include the current estimates of the payroll data as well

| Today | ADP Employment | 160K |

| Trade Balance | -$76.2B | |

| Initial Claims | 235K | |

| Continuing Claims | 1840K | |

| ISM Services | 52.5 | |

| Factory Orders | 0.2% | |

| -ex Transport | 0.3% | |

| FOMC Minutes | ||

| Friday | Nonfarm Payrolls | 190K |

| Private Payrolls | 160K | |

| Manufacturing Payrolls | 5K | |

| Unemployment Rate | 4.0% | |

| Average Hourly Earnings | 0.3% (3.9% Y/Y) | |

| Average Weekly Hours | 34.3 | |

| Participation Rate | 62.7% |

In addition to all this, we hear from NY Fed president Williams this morning, but given that Powell continued to highlight the lack of confidence that inflation was quickly going to reach their target, I doubt Williams will say anything different. My concern is that we are going to see the Unemployment Rate rise to 4.1% or 4.2% and that will change the narrative greatly. Suddenly, there will be a lot more pressure to allow inflation to stay at current levels or even go higher to address the employment side of the mandate. As I have written in the past, any rate cuts before inflation is well and truly vanquished will likely result in a much weaker dollar and much higher commodity prices. Be on the watch for Friday’s data to be the first step in that direction.

Good luck and have a good holiday weekend

Adf