Opinions are already set The Fed is no longer a threat Today’s NFP Will help all to see That buying stocks is the best bet At least that’s the narrative tale The talking heads want to prevail The question’s, will Jay Have something to say If finance conditions, up, scale

To conclude what has already been a tumultuous week, this morning brings the monthly payroll report, a key piece of evidence for the Fed to determine the health of the economy. Expectations for the readings are as follows:

| Nonfarm Payrolls | 180K |

| Private Payrolls | 158K |

| Manufacturing Payrolls | -10K |

| Unemployment Rate | 3.8% |

| Average Hourly Earnings | 0.3% (4.0% Y/Y) |

| Average Weekly Hours | 34.4 |

| ISM Services | 53.0 |

Source: tradingeconomics.com

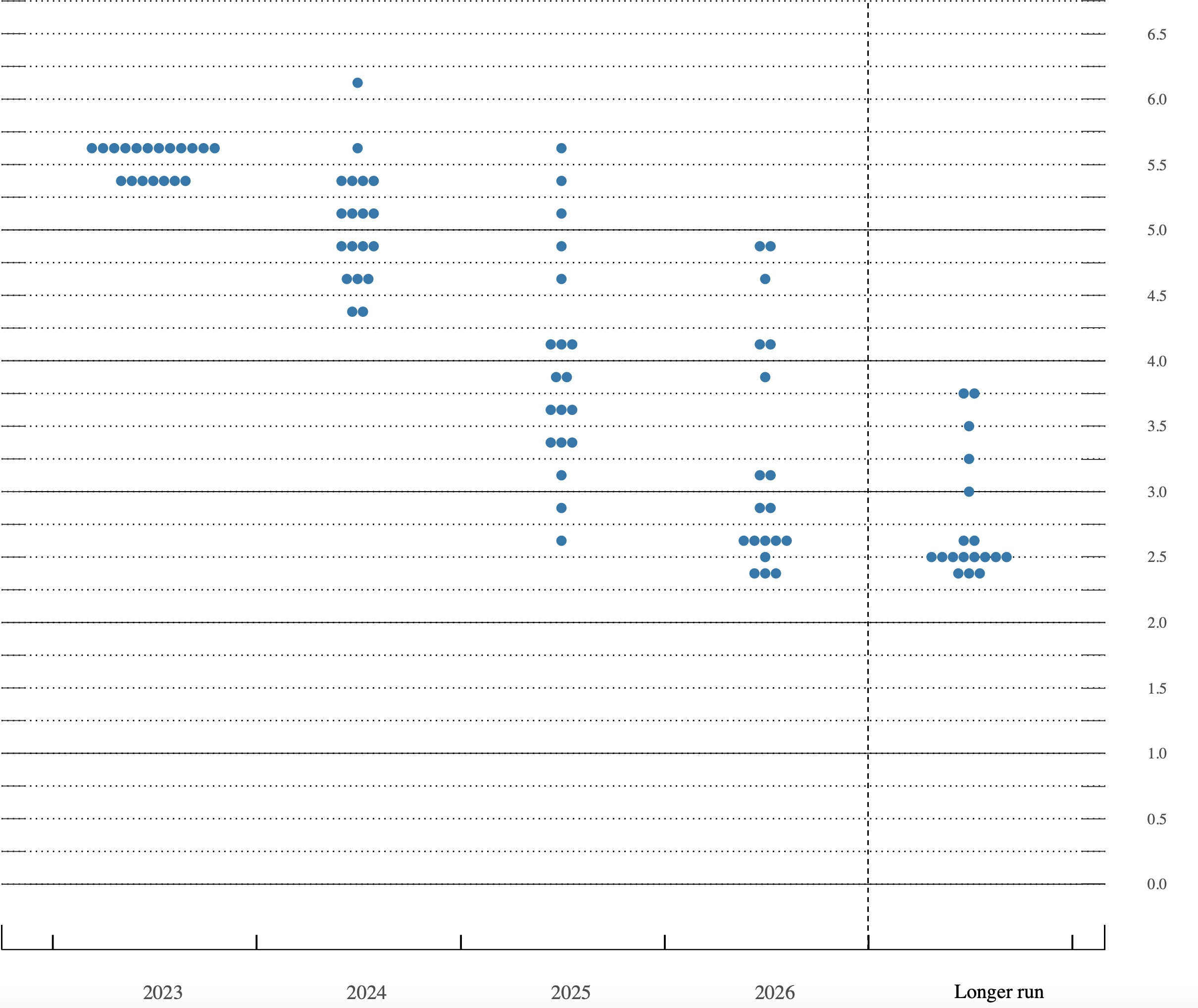

Apparently, the whisper number is a bit above 200K, but we also must pay close attention to the revisions. Recall last month had a blowout 336K result, which was much larger than expected. If that number retains its strength, it would certainly be indicative of a still healthy labor market. This matters a great deal as after Powell’s press conference on Wednesday and the surprising QRA that shortened the duration of upcoming Treasury bond issuance, the market is all in on the goldilocks story, solid growth with low inflation. The corollary to this is that the market is looking for the Fed to back off the current rate policy and begin to reduce the Fed funds rate, thus helping all the DCF models pump up the value of equities.

But even though I have been highlighting the importance of the NFP number for the past two years as a key for the FOMC, it is not clear to me that today’s is so important. I only say this because the Fed just met two days ago, and we will see another NFP before they meet again. Arguably, this one will get lost in the fog of memory.

If that is the case, then it is probably a good time to recap what we have seen this week and how it has affected market sentiment. The bulls are on a roll right now as we have seen a significant pullback in Treasury yields with 10yr down to 4.66%, down 36bps from their peak back on October 23rd. While that is certainly a large move in a short period of time, it is in line with the types of movement we have been seeing all year, so hardly unprecedented. But Powell’s comments, which have been read as dovish despite his best efforts to prevent that view, and the bond market movement have many market participants licking their chops for a massive equity rally going forward.

Interestingly, one of the things the talking heads have been using to pump their story has been the tightening in financial conditions that were a result of declining stock and bond prices. The whole issue of tighter financial conditions doing the Fed’s work for them has been a key story for the past several weeks since it was first mentioned by Dallas Fed President Lorrie Logan. However, the big rally in both stocks and bonds, as well as the decline in the dollar, are all critical features in the calculation of those financial conditions, and they are all pointing to easier conditions. The point is, if tighter conditions was a reason for the Fed to have stopped tightening further, the fact that they are now easing implies the Fed may feel the need to raise rates again in December, although that is clearly not the consensus view.

At any rate, right now, momentum is on the bulls’ side, and it is tough to overcome. Certainly, the economic data continues to point to a resilient economy which implies, to me at least, that the Fed will not feel any urgency to cut rates soon. There has also been a great deal of discussion regarding the fact that the average time the Fed has held rates at a peak before cutting is just 7 months. We are now three months into the most recent hold, and, by definition, since the next meeting is not until December, we will be at 5 months then. My observation about Chairman Powell, though, is at this point he is unconcerned with statistics of that nature and is far more focused on achieving their objective of 2% inflation.

One last thing about inflation before we touch on markets. There has been a growing chorus that deflation is on its way because M2 money supply growth is currently declining. However, for the economics majors out there, recall that the key monetary equation is M*V = P*Q. P = prices, and Q = quantity of goods, or, combined economic output. M = Money supply and V = Velocity of money. It is the last piece that is often ignored but remains quite important. My good friend @inflation_guy, has just published a piece which is well worth reading. The essence is that while M2 may be declining, V is rising rapidly, offsetting that impact and creating conditions for much stickier inflation than many believe. I have a feeling the Fed is going to stay on hold, if not tighten further, for a much longer time than currently anticipated. While this week’s news has clearly been seen as bullish, the long-term trends have not yet changed in my view.

Ok, so a quick look at markets shows that after another gangbusters day in the US, where all three major indices were higher by 1.7% or more, Asian markets followed suit, with virtually every index there higher by at least 1.0%. Europe, however, has been more circumspect with markets essentially unchanged this morning, just +/- 0.1% on the day. US futures are ever so slightly softer at this hour (7:30) down about -0.15% on average, as investors and traders await this morning’s data.

At this point, bonds seem to be taking a rest after a huge price rally / yield decline over the past several sessions and we are seeing very little movement on the day with Treasuries and European sovereigns all within 1 basis point of yesterday’s closing. Even JGB yields slid a bit yesterday but remain above 0.90% as of now. As to the shape of the yield curve, that inversion is starting to show its head again, with the current 2yr-10yr spread back to -32bps. Remember, two days ago that was at -18bps. Broadly speaking, yield curve inversions are not signs of economic strength.

In the commodity space, oil is creeping back higher, up 0.4% this morning although still lower on the week. Gold is basically unchanged this morning, continuing to hang out just below $2000/oz, which continues to surprise me given the sharp decline in yields, at least nominal yields. As to the rest of the space, base metals are mixed amid small changes this morning and foodstuffs, something I have not mentioned in a while, have actually been declining with the FAO’s world food price index falling to its lowest level in more than 2 years last month. It may not seem that way in the grocery store, but perhaps future price rises will be more muted.

Finally, the dollar is generally biding its time ahead of the data, although leaning lower overall. In the G10, the average gain of a currency is about 0.2% while in the EMG bloc we have seen a few outliers, notably KRW (+1.2%) but a more general rise of 0.4% or so. You already know that my view has changed given the seeming change in the underlying drivers. For now, and likely through the end of the year at least, I think the dollar will be under pressure.

Aside from the data this morning, we get our first Fed speaker, Supervision Vice-Chair Michael Barr, this afternoon, but the topic is the Community Reinvestment Act, which makes it unlikely he will swerve into monetary policy. So, as is often the case, the data will see a flurry of activity at 8:30 and then I suspect the recent trends will reassert themselves in a slower session overall. We will need to see an extraordinarily strong NFP print to help reverse the dollar’s current malaise.

Good luck and good weekend

Adf