Mnuchin and Powell explained

That Congress ought not be restrained

In spending more cash

Or else, in a flash

The rebound might not be maintained

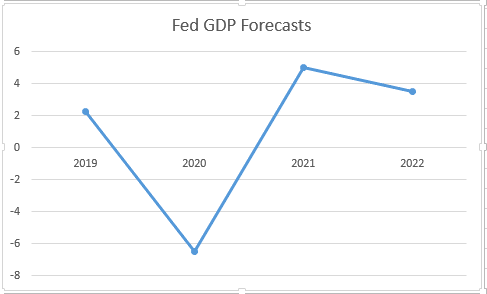

Meanwhile, as the quarter expired

The data show growth is still mired

Within a great slump

And hopes for a jump

Are high, but a vaccine’s required

I continue to read commentary after commentary that explains the future will be brighter once a Covid-19 vaccine has been created. This seems to be based on the idea that so many people are terrified of contracting the disease they they will only consider venturing out of their homes once they believe the population at large is not contagious. While this subgroup will clearly get vaccinated, that is not likely to be majority behavior. If we consider the flu and its vaccine as a model, only 43% of the population gets the flu shot each year. Surveys regarding a Covid vaccine show a similar response rate.

Consider, there is a large minority of the population who are adamantly against any types of vaccines, not just influenza. As well, for many people, the calculation seems to be that the risk of contracting the flu is small enough that the effort to go and get the shot is not worth their time. Ask yourself if those people, who are generally healthy, are going to change their behavior for what appears to be a new form of the flu. My observation is that human nature is pretty consistent in this regard, so Covid is no scarier than the flu for many folks. The point is that the idea that the creation of a vaccine will solve the economy’s problems seems a bit far-fetched. Hundreds of thousands of small businesses have already closed permanently because of the economic disruption, and we are all well acquainted with the extraordinary job loss numbers. No vaccine is going to reopen those businesses nor bring millions back to work.

And yet, the vaccine is a key part of the narrative that continues to drive risk asset prices higher. While we cannot ignore central bank activities as a key driver of equity and bond market rallies, the V-shaped recovery is highly dependent on the idea that things will be back to normal soon. But if a vaccine is created and approved for use, will it really have the impact the market is currently anticipating? Unless we start to see something akin to a health passport in this country, a document that certifies the holder has obtained a Covid-19 shot, why would anyone believe a stranger is not contagious and alter their newly learned covid-based behaviors. History shows that the American people are not fond of being told what to do when it comes to restricting their rights of movement. Will this time really be different?

However, challenging the narrative remains a difficult proposition these days as we continue to see the equity bulls in charge of all market behavior. As we enter Q3, a quick recap of last quarter shows the S&P’s 20% rally as its best quarterly performance since Q4 1998. Will we see a repeat in Q3? Seems unlikely and the risk of a reversal seems substantial, especially if the recent increase in Covid cases forces more closures in more states. In any event, uncertainty appears especially high which implies price volatility is likely to continue to rise across all markets.

But turning to today’s session, equity markets had a mixed session in Asia (Nikkei -0.75%, Hang Seng +0.5%) despite the imposition of the new, more draconian law in Hong Kong with regard to China’s ability to control dissent there. Meanwhile, small early European bourse gains have turned into growing losses with the DAX now lower by 1.5%, the CAC down by 1.4% and the FTSE 100 down by 1.0%. While PMI data released showed that things were continuing on a slow trajectory higher, we have just had word from German Chancellor Merkel that “EU members [are] still far apart on recovery fund [and the] budget.” If you recall, there is a great deal of credence put into the idea that the EU is going to jointly support the nations most severely afflicted by the pandemic’s impacts. However, despite both German and French support, the Frugal Four seem to be standing their ground. It should be no surprise that the euro has turned lower on the news as well, as early modest gains have now turned into a 0.3% decline. One of the underlying supports for the single currency, of late, has been the idea that the joint financing of a significant budget at the EU level will be the beginning of a coherent fiscal policy to be coordinated with the ECB’s monetary policy. If they cannot agree these terms, then the euro’s existence can once again be called into question.

Perhaps what is more interesting is that as European equity markets turn lower, and US futures with them, the bond market is under modest pressure as well this morning. 10-year Treasury yields are higher by more than 2bps and in Europe we are seeing yields rise by between 3bps and 4bps. This is hardly risk-off behavior and once again begs the question which market is leading which. In the long run, bond investors seem to have a better handle on things, but on a day to day basis, it is anyone’s guess.

Finally, turning to the dollar shows that early weakness here has turned into broad dollar strength with only two currencies in the G10 higher at this point, the haven JPY (+0.4%) and NOK (+0.2%), which has benefitted from oil’s rally this morning with WTI up by about 1% and back above $40/bbl. In the emerging markets, only ZAR has managed any gains of note, rising 0.4%, after its PMI data printed at a surprisingly higher 53.9. On the flip side, PLN (-0.6%) is the laggard, although almost all EMG currencies are softer, as PMI data there continue to disappoint (47.2) and concerns over a change in political leadership seep into investor thoughts.

On the data front, we start to see some much more important data here today with ADP Employment (exp 2.9M), ISM Manufacturing (49.7) and Prices Paid (44.6) and finally, FOMC Minutes to be released at 2:00. Yesterday we saw some thought provoking numbers as Chicago PMI disappointed at 36.6, much lower than expected, while Case Shiller House Prices rose to 3.98%, certainly not indicating a deflationary surge.

Yesterday we also heard the second part of Chairman Powell’s testimony to Congress, where alongside Treasury Secretary Mnuchin, he said that the Fed remained committed to doing all that is necessary, that rates will remain low for as long as is deemed necessary, and that it would be a mistake if Congress did not continue to support the economy with further fiscal fuel. None of that was surprising and, quite frankly, it had no impact on markets anywhere.

At this point, today looks set to see a little reversal to last quarter’s extremely bullish sentiment so beware further dollar strength.

Good luck and stay safe

Adf