The markets are trading like peace

Has come, hence the stock price increase

While crude prices fall

And risk, overall

Is favored like summer in Greece

But can we trust this time it’s true?

Or will, once again, this fall through?

I guess time will tell

If this will compel

The doomers to change their world view

It is certainly a hopeful morning today as risk rallies around the world while oil prices tumble. At $84.72/bbl, down -3.4% on the session, oil is trading at its lowest level since April 17.

Source: tradingeconomics.com

While President Trump had once again threatened to destroy Iran’s oil infrastructure, shortly thereafter he reversed that call with news that Iran was back at the table with both sides closing in on a peace deal. Frankly, despite the absolute certitude that so many pundits seem to have, the reality is nobody really knows if this time is the charm or not. In fact, I would argue that the Iranians themselves, as well as President Trump, are not certain, as though I’m confident both sides would like to stop this, there are many political calculations that go into the process, and the punditry is simply not party to those conversations. We shall see.

Of course, markets trade the rumor, not the news, or at least they initiate positioning on the rumor, so with that story making the rounds, it is also no surprise that equity markets have shaken off their early week blues and rallied strongly pretty much everywhere around the world. The below chart of futures markets shows just how widespread the gains are with only Russia’s MOEX under pressure (is that really even a market still?) and although Toronto, Mexico and Brazil have not yet opened, all rallied yesterday alongside the US.

Source: tradingeconomics.com

Of course, there is another equity story and that is SpaceX, which IPO’d last night at a price of $135/share, and which, like so many things these days, has a seen a huge disparity between the pros and the cons. Many analyses have been performed showing that the company is not “worth” anywhere near the $1.8 trillion market cap at which it is starting. But those same folks have consistently explained that Tesla is not worth the $1.5 trillion, and yet there Tesla sits. There was a huge amount of interest with more than $75 billion of retail orders to buy the IPO. My observation is that Elon Musk is somebody who gets things done, and usually better than anyone else. But markets are, as I always say, perverse, so this will be an interesting ride.

Other than the end of the war and the SpaceX IPO, the two stories that made a brief appearance were yesterday’s PPI data, which depending on the analyst were either hot or cold, and the fact that Madame Lagarde and the ECB raised their base rate by 25bps yesterday, right as energy prices started falling dramatically. This is not the first time the ECB has made a mistake of this nature, one need only look back to the beginning of the GFC when then-president Jean Claude Trichet controversially raised interest rates in July 2008 and reversed course 3 months later after Lehman Brothers failed.

And that’s what the setting is as we head into the last trading session of the week. So, let’s see how other markets are behaving.

It should be no surprise that bond yields are falling. While Treasury yields are unchanged this morning, they fell about -7bps across the board yesterday. But the Iran news was after the European close so sovereign yields are lower by between -4bps and -7bps this morning. I presume some investors are happy that the ECB is fighting inflation, but I think most are responding to the idea that the end of the war means lower oil prices and therefore a significant reduction in inflation pressures. Last night in Asia, we also saw yields fall sharply across the board with JGBs down -6bps and every other market (Australia, Singapore, Korea) slide by a similar or even greater amount.

In the metals markets, while gold (-0.1%) is little changed this morning, it did manage to rally more than $100/oz yesterday, or more than 2%. Silver (-0.5%) is also slipping a bit today but that is after a 6% rally yesterday. My take is these are short term profit taking trades.

Finally, the dollar is, overall, little changed this morning. it was very modestly weaker during yesterday’s session with the DXY slipping back below 100 (currently 99.75), but USDJPY remains above 160, still in a danger zone although there has been precious little discussion on the topic for the past several sessions. You will not be surprised that NOK (-0.5%) is under pressure as it is probably the currency that tracks most closely to oil prices. But other than that, not much to say in this market either.

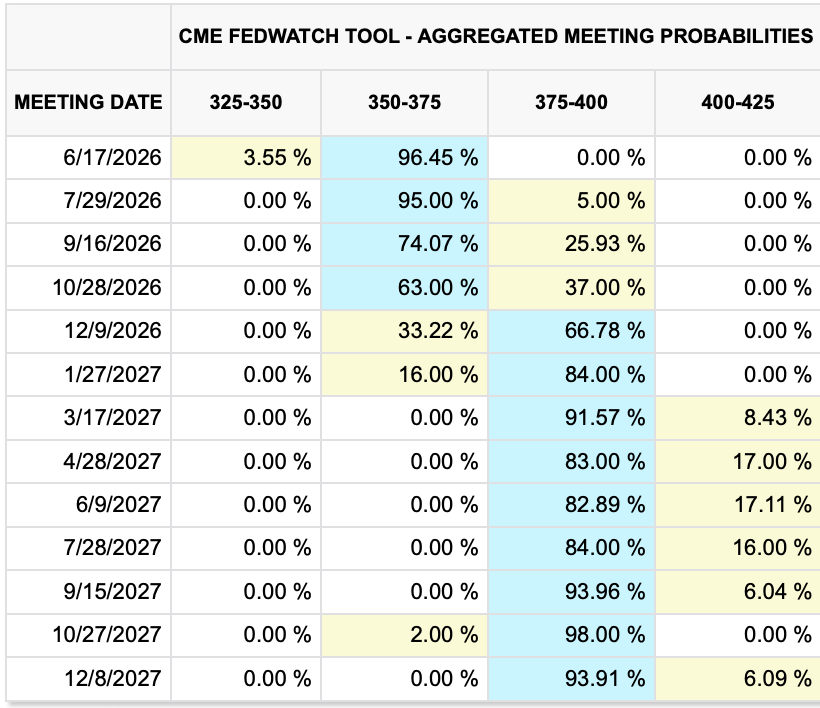

On the data front, this morning brings only Michigan Sentiment (exp 46.0), which continues to hug the lows of the series as a contradiction to the highs in equity markets. But now, with CPI/PPI out of the way, all eyes will turn to next week’s FOMC meeting. If we look at the Fed funds futures curve, it is still forecasting a rate hike by the end of this year.

Source: cmegroup.com

But I have to wonder, if the fighting stops and a deal is reached such that the Strait is reopened and the blockade is lifted, the one certainty is that oil prices will fall much lower, probably below the levels seen prior to the war began. Given all the talk about secondary effects of high oil prices, I would expect that talk to disappear. History has shown that every shortage of a commodity is followed by a glut. Will economists be explaining why persistently low energy prices in the future are going to undermine inflationary expectations?

Markets are still beholden to the headlines so if this deal falls apart, you need to expect all these moves to reverse course with oil higher alongside yields and the dollar while stocks and precious metals fall. But if this is the end of the Iranian engagement, I suspect that risk is going to be in vogue for quite a while, investment will be flowing into the US and the dollar will hold its own, even as yields decline. (Going back to my flows as a key driver, not just interest rates.)

Good luck and good weekend

Adf