Two narratives are now competing Recession, the first, is retreating No-landing is rising As those analyzing The data claim weakness is fleeting But what of the curse of inflation Which for two years has gripped the nation Is it really past Or are we too fast To follow that interpretation? Friday’s employment data was, for a second consecutive month, a bit lower than the median forecast of economists. However, it was still reasonable at 187K new jobs. One of the positive aspects was the decline in the Unemployment Rate to 3.5% although from an inflation perspective, Average Hourly Earnings (AHE) rose more than forecast. In a way, there was something for everyone in the report with the recessionistas highlighting the decline in average weekly hours and the fact that last month’s data was revised down for the 6th consecutive month, typically a very negative signal. However, the no-landing crowd points to the AHE data as well as the Unemployment Rate and claim all is well.

Of course, ultimately, the opinion that matters the most is that of Chairman Powell and his acolytes at the Fed. Are they glass half full or glass half empty folks? I have been highlighting the importance of the NFP data as I believe it remains the fig leaf necessary for the Fed to continue to raise interest rates if they want to in their ongoing efforts to rein inflation back to their target level. My sense is that Friday’s data will not dissuade them from hiking rates in September if they decide it is still appropriate, but it could also be argued as a reason for another pause. Certainly, there is nothing about the data that would indicate a rate cut is on the table anytime soon. And remember, we will see the August report shortly after Labor Day, which comes before the next FOMC meeting, so still plenty of information yet to come.

Which brings us to this week’s numbers on Thursday and Friday when CPI and PPI are set to be released respectively. While we all understand that the Fed’s models use core PCE as their key inflation input, we also know that CPI, especially core -ex housing, has been a recent focus for Powell and that is the number that gets the press. You may recall that last month, the headline CPI number printed at 3.0%, it’s lowest since early 2021, and was widely touted as proof positive that the Fed was close to achieving their objective. Alas, energy prices have done nothing but rise in the ensuing month and given the ongoing reductions in production by OPEC+, it seems unlikely that we are done with this move. In fact, ironically for the no-landing crowd, if there is no landing and supply continues to shrink, energy prices, both oil and gasoline, will likely continue to rise as well, putting significant upward pressure on headline CPI. If CPI is rising it will be extremely difficult for Powell to consider anything but more rate hikes.

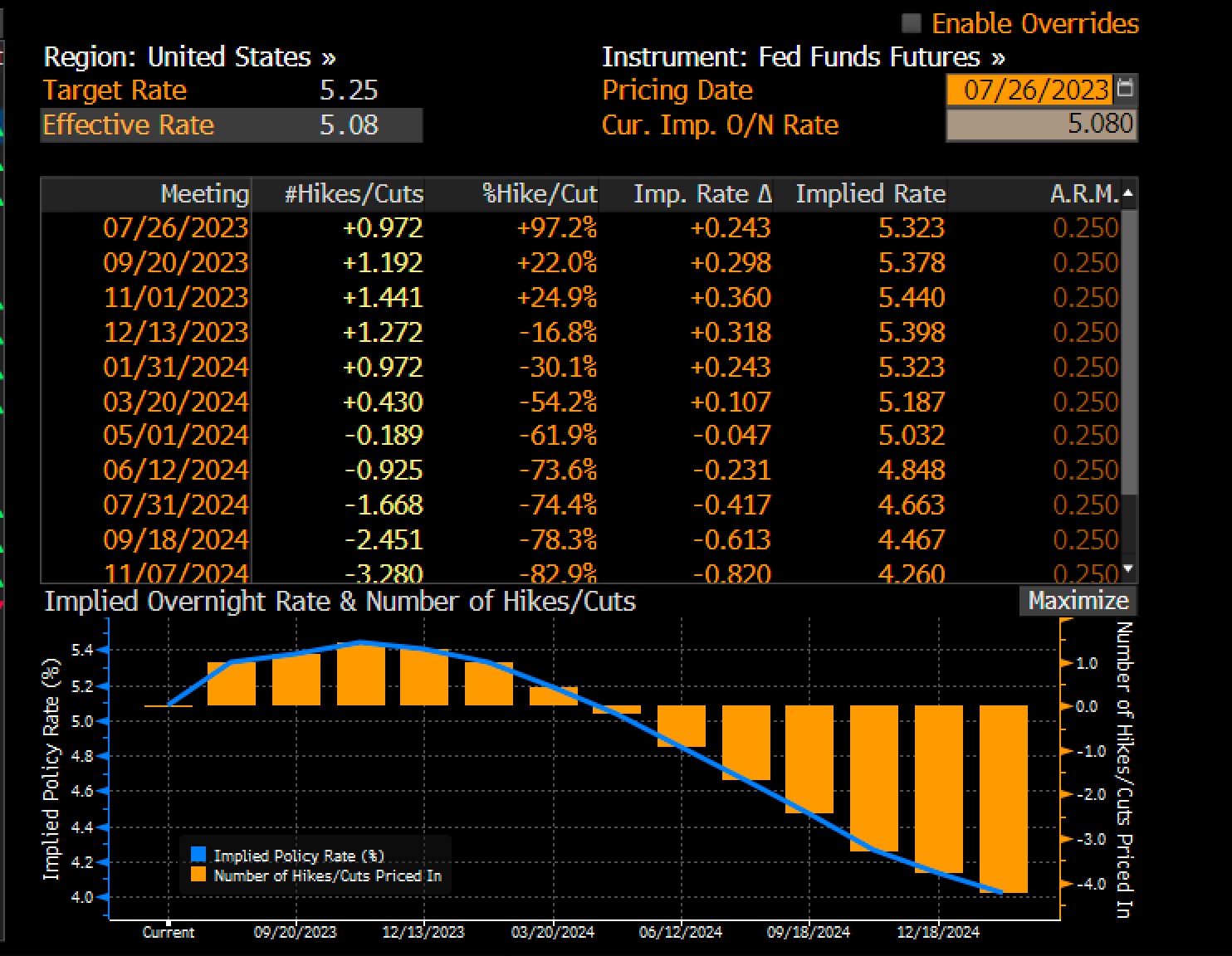

Currently, the market is pricing a very low probability of a September rate hike by the Fed, just 16%, so there is ample room for repricing if the data comes in hot. Surprisingly, the market is pricing in a higher probability of an ECB hike, 38% in September, despite the fact that Madame Lagarde essentially told us at the last meeting they were done. My suspicion is that there is room for a more negative outcome in the interest rate space going forward. One other tidbit this morning is the Cleveland Fed has an CPI Nowcast, similar to the Atlanta Fed’s GDPNow but for inflation, and that number is currently 0.41% for July, well above the market median forecast of 0.2%. The point is there is room for a negative inflation surprise and the knock-on effects of such a result would likely be risk negative. Just sayin’.

Meanwhile, Friday’s equity market reversal in the US has mostly been followed around the world with red the dominant color on screens in the major markets. In Asia, while the Nikkei managed to eke out a small gain, China and South Korea both saw renewed selling. As to Europe, all markets are lower on the order of -0.25% to -0.5% at this hour (7:30). However, US futures are currently edging higher on what seems to be a reflexive bounce rather than a fundamental opinion.

Bond markets, though, are reversing much of Friday’s rally with 10-yr Treasury yields higher by 7bps this morning and most European sovereign yields up a similar amount. Friday saw a sharp rally on the headline NFP number which served to force the hand of many short sellers in the Treasury market. Recall, heading into the release, there was a growing consensus, especially after a particularly strong ADP Employment number, that the no-landing scenario was the most likely and that would mean higher yields for longer. In addition, the market was informed of the extra $1.9 trillion in Treasury issuance that was coming the rest of the year, with the bulk of that coming out the curve, rather than in the T-bills that have been the focus to date. It feels like the short-selling crowd is getting back on board and the weight on prices of excessive issuance and the Fed’s ongoing QT program means higher yields should be expected.

As to oil prices, while they are lower this morning by -0.7%, they remain well above $80//bbl and appear to be consolidating ahead of the next attempt to break above key technical resistance at $85/bbl. Absent a very severe recession, which has not yet shown up, it is hard to make the case for a large decline in this sector of the market. Metals markets are far more benign this morning with tiny gains and losses as traders continue to try to figure out if there is a recession coming.

Lastly, the dollar’s demise, which is touted on a weekly basis by pundits everywhere, will have to wait at least one more day as the greenback is stronger vs. essentially every one of its major counterparts. There is still a strong relationship between US Treasury yields and the dollar, and with higher yields, it is no surprise the dollar is higher. Consider, too, the fact that the market is pricing such a small probability of a Fed funds hike next month. If (when?) that pricing changes, I expect the dollar to benefit greatly.

On the data front, there is a bit more than CPI and PPI, but not much:

| Today | Consumer Credit | $13.55B |

| Tuesday | NFIB Small Biz Optimism | 90.5 |

| Trade Balance | -$65.0B | |

| Thursday | Initial Claims | 230K |

| Continuing Claims | 1710K | |

| CPI | 0.2% (3.3% Y/Y) | |

| -ex food & energy | 0.2% (4.8% Y/Y) | |

| Friday | PPI | 0.2% (0.7% Y/Y) |

| -ex food & energy | 0.2% (2.3% Y/Y) | |

| Michigan Sentiment | 71.5 |

Source: Bloomberg

In addition to the data, we have three Fed speakers, Bostic, Bowman and Harker, each speaking twice this week. Ultimately, my take is that Friday’s NFP data did nothing to change the current Fed calculus and higher for longer remains the operative thought process. As to the dollar, if we continue to see Treasury yields rise, which I think is the most likely scenario, then I suspect the dollar will find buyers. For those of you awaiting a sharp dollar pullback to establish hedges, you may be waiting quite a while.

Good luck

Adf