While last week a great deal was learned

‘Bout how much the Fed is concerned

That prices won’t fall

Chair Powell’s clear call

Was higher for longer’s returned

And next week, we’ll see CPI

A critical piece of the pie

Is ‘flation still hot?

And if it is not

Will traders, more equities, buy?

But this week is dull as can be

With virtually nothing to see

No data of note

And no anecdote

About which the masses agree

There is precious little to discuss this morning. The market is still generally in a good mood for risk assets on the back of the combination of the perceived Powell dovishness and the softer than expected NFP data which adds to the opinion that monetary policy going forward will loosen further. And this week offers virtually no data at all, just the weekly Claims data and then Michigan Confidence on Friday.

Granted, we will hear from several Fed speakers, a process which got started yesterday when Richmond Fed president Barkin explained that, while hopeful inflation declines, he continues to believe that the current policy stance is “sufficiently restrictive.” Meanwhile, NY Fed president Williams assured us that, eventually there will be rate cuts, that GDP would remain solid and that the Fed is looking at the “totality” of the economic data. Given how frequently Chairman Powell used that word, totality, I have the feeling that at the end of the FOMC meeting last Wednesday, Powell reminded every speaker to use that phrase in their speeches. I only say that because I would contend it is not a word used regularly by the population, even when it might be appropriate.

But did we actually learn anything new from these two? I would argue we have not, nor is it likely that any of the other speakers lined up this week, starting with Kashkari today and followed by Governors Jefferson and Cook tomorrow, SF President Daly on Thursday and Governors Bowman and Barr along with Chicago president Goolsbee on Friday, will tell us anything new at all.

So, where does that leave us? With no new data and a low probability of new Fed opinions to be revealed, this week has all the earmarks of a complete nothingburger. Granted we hear from both the Swedish Riskbank (no change expected) and the BOE (no change expected) but given the lack of likely policy adjustment, markets will be trying to discern the subtleties of their comments. And the one thing we all know extremely well is that markets know absolutely nothing about subtlety. With this in mind, my expectations are that the current driving force, the underlying bullish thesis based on slowly easing monetary policies around the world, will continue to be the main driver of markets this week. This is not to say that things are on autopilot, but until we see a new piece of information, range trading with a bias toward higher risk asset prices seems to be the most likely outcome.

This was generally what we saw overnight with most Asian markets performing well led by the Nikkei (+1.6%), catching up after the Golden Week holidays, but other than Hong Kong (-0.5%), the rest of the region was green. Europe, too, is having a good session, with gains ranging from the CAC (+0.3%) to the FTSE 100 (+1.0%). However, at this hour (7:20), US futures are essentially flat.

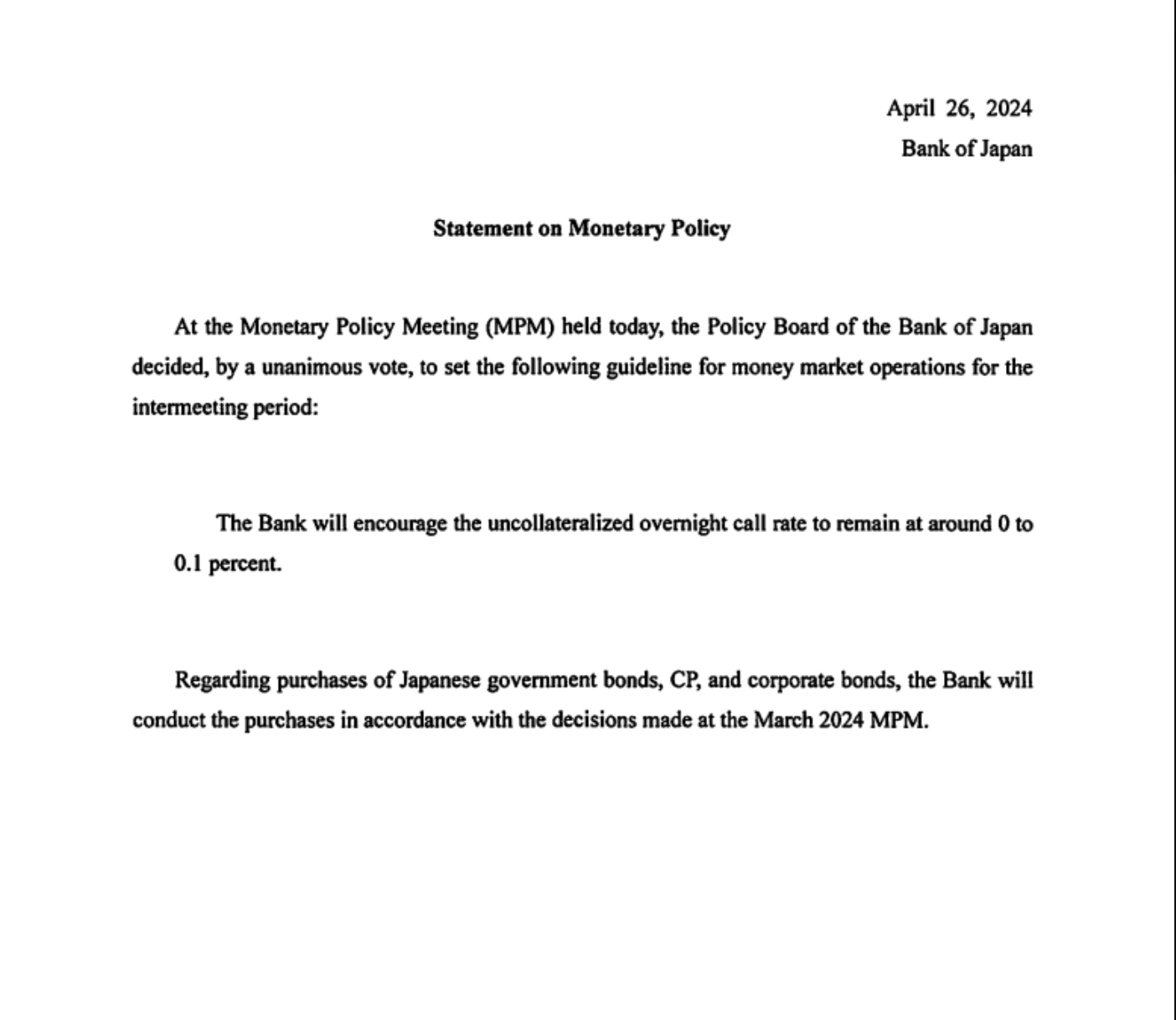

Bond markets are still feeling good about the Fed and weaker employment data with yields continuing to drift lower. This morning, Treasuries have seen yields decline 3bps, while in Europe, continental sovereigns are seeing similar yield declines. The big exception is the UK, where gilt yields are down 9bps this morning despite any news of note or commentary by BOE policymakers. I think there is a growing anticipation that the BOE is going to pivot more dovish on Thursday which is driving this story. Finally, with Japan back in session, JGB yields also declined 3bps as the yen’s recent strength (albeit not today where it has drifted lower by -0.2%) has allayed some market fears that the BOJ will need to be more aggressive in their policy tightening.

Commodities, which have had a terrific run are under pressure this morning, although given the absence of new information, this has all the hallmarks of a trading correction. But oil (-0.4%) cannot gain any traction despite the fact that Israel is in the process of their long-awaited incursion into Rafah while ceasefire talks have faltered. Metals, too, are under pressure across the board, but on the order of -0.4% for all of them. Given the recent movement, this cannot be surprising (nothing goes up in a straight line) and I expect that we will see directionless price activity for the next several sessions.

Finally, the dollar is ever so slightly firmer this morning, with DXY having bounced off the 105 level and USDJPY starting to rise again with no sign that the MOF is keen to do anything else. But as I look across the board, the largest movement of any currency, G10 or EMG, has been just 0.3% (both KRW and NOK having fallen that amount) which is really indicative of the doldrums into which this market has fallen. I will say that there is growing talk that the next big trade is to be long yen (short dollars) with more and more people indicating they see higher Japanese rates coming while the Fed drifts toward eventual rate cuts. The hard part about this trade is it is extremely expensive to carry for any length of time. Until the Fed preps the market for cuts, rather than its current higher for even longer stance, I would be wary of the trade. However, as I explained yesterday, for hedgers, this is exactly when options make the most sense.

And that’s really all there is. Consumer Credit (exp $15.0B) is released this afternoon at 3:00 and Mr Kashkari speaks at 11:30. It beggars’ belief that he will say something new and exciting so I anticipate a very dull session across the board today.

Good luck

Adf