The GDP number was smokin’

As animal spirits have woken

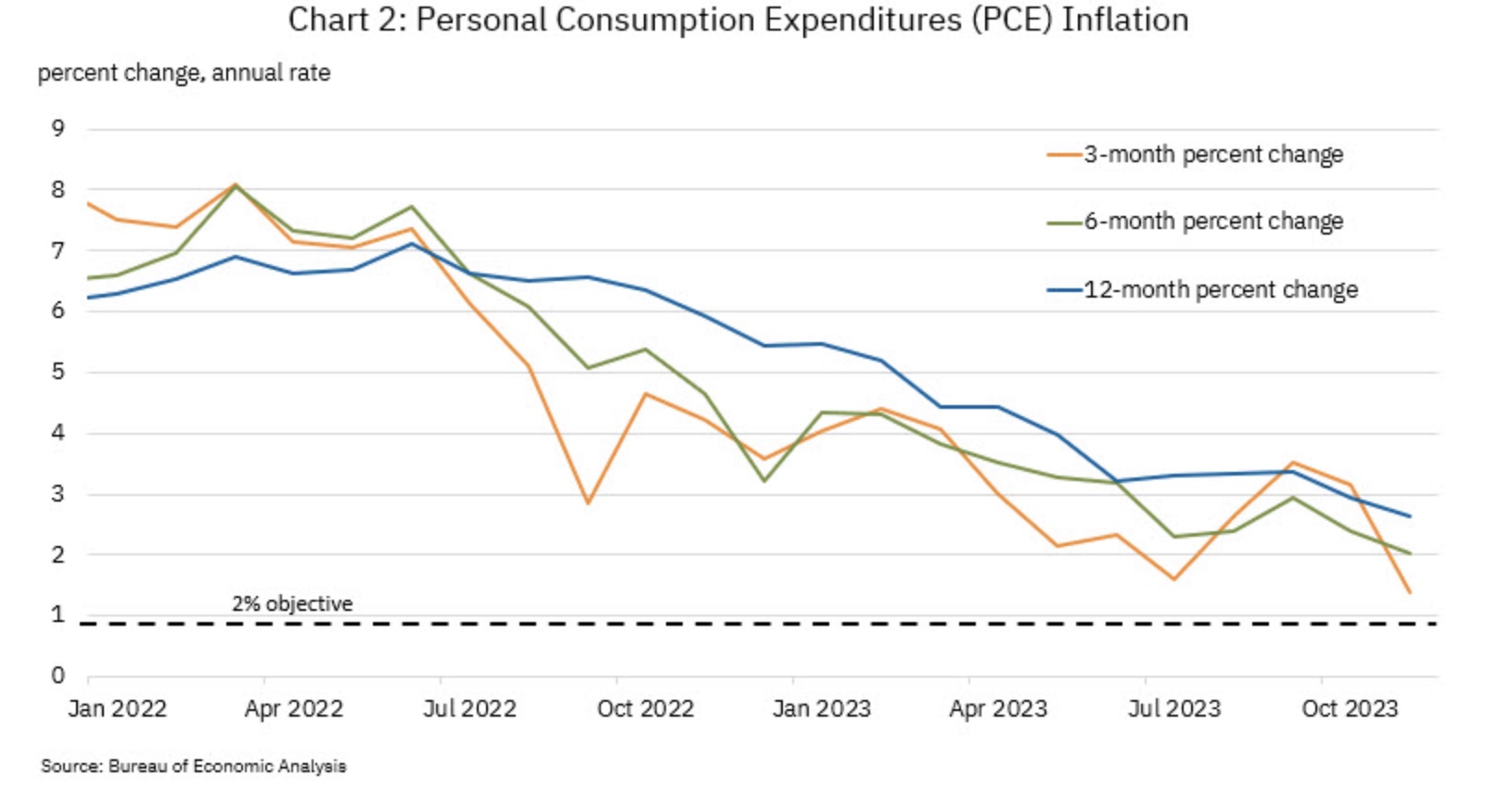

The Core PCE

If higher than three

Could slay rate-cut talk that’s been spoken

Thus, if the Fed’s data dependent

The ‘conomy’s truly resplendent

So, please do explain

Why rate cuts are sane

Seems rates ought, instead, be ascendent

By now you are all aware that Q4 GDP was a significantly better than expected 3.3% SAAR, far above the 2.0% analyst forecasts and far above the Atlanta Fed’s GDPNow readings. For everyone who is looking for that recession, thus far it still appears to be somewhere further down the road. At some point, it is certain, there will be a recession but the when is the big question.

Now, a different question would be what is driving the economic activity that we have seen? That answer is far easier to determine as in the equation that defines economic growth: Y=C+I+G+NX (exports-imports), the variable that is growing most consistently is the G, government spending. Simply look at the size of the budget deficit. This is not to say that government spending is not growth as measured, just that it is not organic growth that feeds on itself. It is the organic kind that is the sign of a healthy economy. Government spending can be analogized as gaining weight but not growing stronger, i.e. getting fat.

Regardless, though, of the reasons for the growth, it is real in the sense that more activity is taking place. This implies that demand continues to be robust. Since this is the case, I would ask all those who are expecting the Fed to cut rates by May at the latest, but begging for a March rate cut, why do you think that is appropriate?

First off, another way to say data dependent is to call the Fed reactive. This means that the Fed is explicitly going to be behind the curve and react to the data they see, they are not going to pre-empt expectations for future economic outcomes. Back in the day, when Alan Greenspan was Fed chair, he would raise rates occasionally to head off what he thought was incipient inflation, but rate cuts were then, and have always been, reactive to problems in the economy. That is why, generally, rate decline much faster than the rise. This cycle was quite the exception but then Chairman Powell was in denial for a very long time before he figured out he had made a mistake. It is this reason that I believe the Fed funds outcome is bimodal, that either there will be only one or two token cuts, or we will see 300bps or more as the economy craters. Based on yesterday’s data, I’m still in the one cut camp this year as per my 2024 forecasts.

It is important to remember that the Fed’s dot plot is not the road map, per se, it is merely a compilation of each member’s individual forecasts. But they are just that, forecasts, and as we saw with yesterday’s GDP number, FORECASTS ARE WRONG ALL THE TIME! There is no reason to believe the Fed or its members, who have an atrocious forecasting record, know where things are going to be later this year, let alone in 2025 or 2026.

Back to my point, to drive it home; the Fed has explained they are going to be reactive to the data when it comes to setting policy rates. So far, the data is pointing to continued solid, above trend, economic growth and the employment situation remains strong (Initial Claims at 200K, Unemployment Rate at 3.7%). As well, inflation remains well above their target. Once again, I will ask, why will they be cutting rates in H1? If they do, it implies that things have gotten a whole lot worse in a hurry, and that, my friends, will not be a positive for risk assets.

Turning to the overnight session, after a solid equity market performance in the US, where all three major indices rallied a bit, Asia took a different path as both Japanese and Chinese shares fell 1.35% or more. Apparently, the luster of the Chinese fiscal and market support has faded a bit, but that hasn’t stopped those who got long Japanese shares in that pairs trade I discussed yesterday, from continuing to sell. Interestingly, the data overnight showed that Tokyo CPI, on every measure, was much softer than forecast implying that the BOJ has far less need to consider tightening policy in the near future. I would have thought that would have helped Japanese shares, but not so much. Europe, though, is having a much better day with the CAC (+2.1%) leading the way on the back of very strong results by LVMH, the luxury goods firm. But all the indices are higher on the continent. Alas, US futures are a bit softer at this hour (7:00), but only just and really it is the NASDAQ which has been lagging a bit.

In the bond market, activity has been muted everywhere as investors and traders around the world await this morning’s PCE data in the US. Treasury yields, which slid a few bps yesterday, are unchanged on the day and European sovereigns are all seeing yields drift lower by between 1bp and 3bps. Perhaps the least surprising move is JGB yields sliding 3bps overnight on the back of that Tokyo CPI data. As an indication of what those numbers are like, Headline and Core both printed at 1.6% Y/Y, significantly below the December readings and the lowest in nearly two years.

While oil prices have backed off a bit this morning, -0.8%, they have had an excellent week, up nearly 5% on the back of the stronger showing in the US economy, the fiscal stimulus stories in China and the fact that Ukraine was able to successfully attack a Russian oil shipping facility, closing it down and reducing supply. In the short-term, it does feel like there are more potential catalysts to drive this price higher, but the long-term question remains open. As to the metals markets, they continue to do very little with marginal gains or losses on a day-to-day basis as we have been trendless in gold and copper for the past several months. We will need to see some fundamental changes in the supply/demand equation to shake out of this lethargy, but that remains true in many markets. Data of late is a Rorschach test as there always seems to be a data point to help someone justify their view, regardless of their view. We need to see things align more clearly for a change in either direction.

Finally, the dollar, which has been grinding ever so slightly higher over the past month or two, is a bit softer overall this morning, roughly 0.3% across the board in both the G10 and EMG blocs. Arguably, the most important data overnight was that Tokyo CPI, but the yen is actually unchanged on the session, lagging the euro and pound, but not responding very much. Interestingly, despite oil’s decline, NOK is slightly firmer, so this is really a modest dollar weakness story for now. Perhaps in anticipation of a soft PCE number?

So, let’s turn to the data today. Everything comes at 8:30 and here are the consensus views right now: Personal Income (0.3%), Personal Spending (0.4%) PCE (0.2% M/M, 2.6% Y/Y), and most importantly, Core PCE (0.2% M/M, 3.0% Y/Y). Much has been made of comments that Governor Waller made a few weeks ago which have been interpreted as ‘knowledge’ that the M/M number would be soft, 0.1%, dragging all the other indicators with it. As well, Treasury Secretary Yellen ostensibly explained that the recession has been avoided and the soft landing achieved so inflation is no longer a problem. And maybe that will be the case. But inflation is a funny thing. It is insidious and extremely difficult to remove from an economy as complex as the United States once it is embedded there. I have no idea where today’s data will print, but I will say that my bias is that inflation is stickier than the rate cut advocates believe.

As to the market reaction, that is also very difficult to anticipate. Yesterday in my assessment of what would occur in response to a hot number, I was right about the dollar and oil, but not about stocks and bonds, both of which rallied. As of now, the Fed funds futures market continues to price a 50:50 chance of a March cut. I feel like we will need to see a very soft number today to keep that stable. And if the M/M number is 0.3%, I would expect that March probability to shrink rapidly. However, for now, those looking for rate cuts remain on top in the game, and they will only give up their views kicking and screaming. Keep your ears peeled.

Good luck and good weekend

Adf