Confusion today is what reigns

As no pundit clearly explains

Why previous claims

Have gone up in flames

And how much more pain still remains

They still blame the Bank of Japan

With spoiling their well thought out plan

And too, yesterday

When bonds went astray

It gave them a new boogeyman

Yesterday started out so well for all those who were convinced that it was the BOJ’s surprising and extreme actions last week that led to an unwarranted selloff in stocks and other risk assets. First off, the BOJ, via one of its members Ichida-san, basically apologized for their actions and said that they would not be making any other changes after all. That led to a rally in equities and a sell-off in bonds as risk assets were suddenly back in favor. Alas, by the end of the day, that was no longer the case.

But let’s look at what the BOJ actually did last week. On the interest rate front, they raised their base rate to 0.25% and regarding their balance sheet, they indicated they had a plan to slow down its growth at a very gradual pace. Remember, they did not say they were going to sell JGBs, they said that by 2026 they would be buying half as many JGBs as they do today.

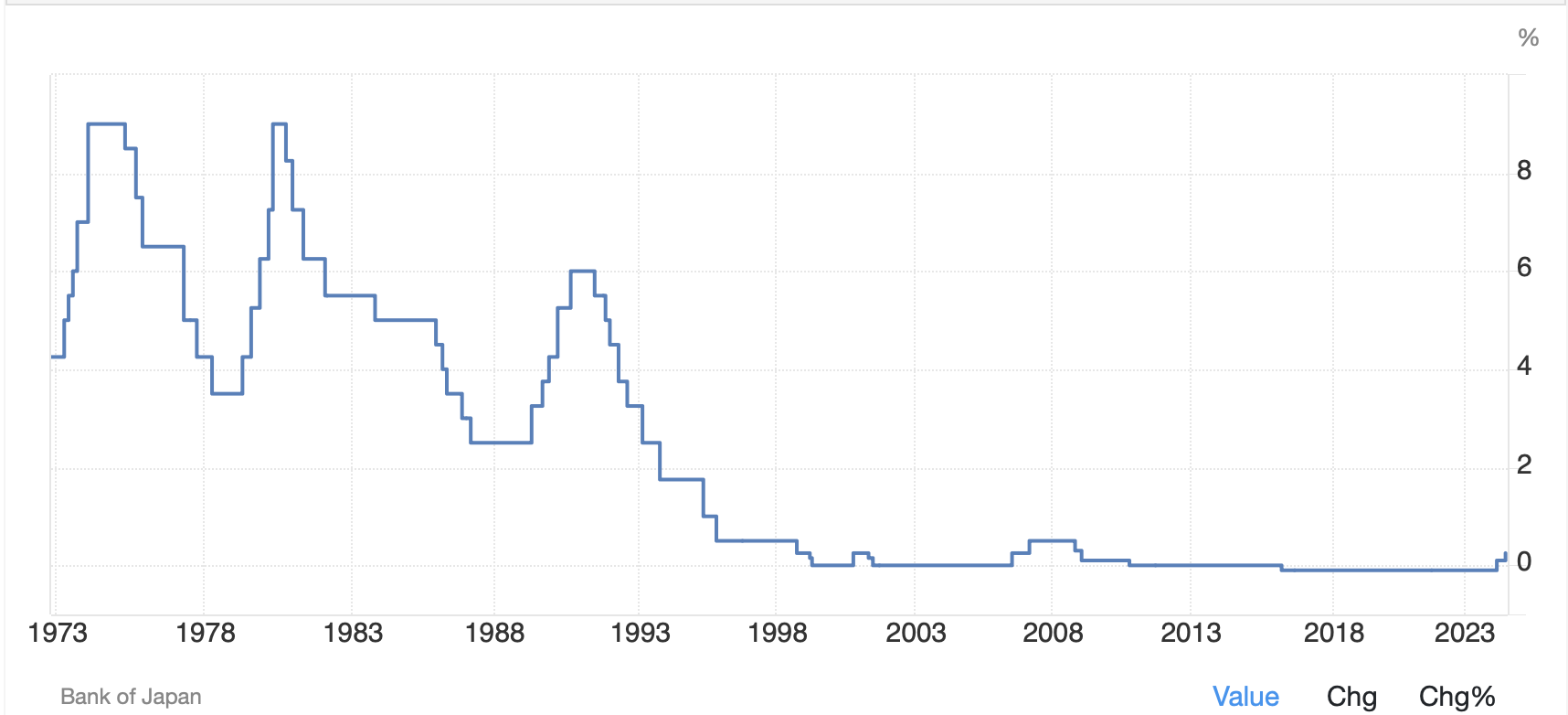

Also, let’s remember that inflation in Japan is currently measured at 2.8%, so the base rate remains deeply negative in real terms. I understand the signaling impact of what they did as any change in the status quo while there is a significantly leveraged market can have major impacts. And that is what we saw during the past week. It is also important to remember that given the length of time that the Japanese have maintained their ZIRP/NIRP monetary policy, the opportunity for very large institutions to build up very large positions was, to be succinct, very large. The chart below shows for just how long Japanese interest rates have been near zero, more than twenty years.

Source: tradingeconomics.com

My point is that Japanese investors have been seeking alternative opportunities for an entire generation. As well, the concept of the carry trade has been in place for that same amount of time. It will take a long time for these ideas to be changed and the positions along with them. Now, according to a Bloomberg article, JPMorgan’s analysts claimed that three-quarters of the carry trade has already been unwound. And maybe they are right about that. But I assure you that three-quarters of Japanese investors have not adjusted their positions in the fixed income market. We have not come to the end of this road.

So, analysts found another cause for yesterday’s negative outcomes, the 10-year bond auction. It turns out that investors are seeking more yield than the market had anticipated ahead of the auction. This led to a 3 basis point tail, meaning that the auction cleared at a yield, 3.96%, 3 basis points higher than traders were pricing ahead of time (typical 10-year tails are well less than 1bp.) There were less bids than anticipated, and generally this is not a good story for Secretary Yellen and the Treasury. The story that circulated was that the reason stocks fell in the afternoon was the weak auction. Alas, the timing of that does not make sense. Equity markets had already given back their morning gains before the auction results were announced and were lower on the day at 1:00pm. But narrative writers need a story, and that was a good one.

So, what really happened? Who knows? But FWIW this poet has seen enough market action during his career to recognize that while fundamentals matter in the long-run, daily changes are often completely random, or at least seemingly so. Large orders can drive markets, especially when liquidity is lower because of holiday schedules and the time of year. And lately, the combination of algorithmic trading and extreme retail speculation will also move markets in surprising directions.

I believe that we remain in a period of change. Monetary policies around the world are adjusting to the realities of inflation remaining stickier than policymakers want to believe. In addition, the political cycle continues to be difficult to forecast, notably in the US, with market perceptions of very different economic policies to be implemented depending on the next US president. And finally, I believe the best way to describe the global economy is that it is in transition. After a decade or more of easy money policies around the world, as those policies start to change, they impact different segments of the economy at different rates. This means that some parts of an economy can be in recession while other parts can be doing fine. And that gives rise to confusing data with no broad trend. This may explain why manufacturing survey data is so weak while service survey data has held up well.

My best guess is that we are going to continue to see confusion until policy makers are more aligned. In fact, that is why there are so many calls for the Fed to start cutting rates soon, so they can catch up and unify monetary policies around the world.

Ok, let’s see how things looked overnight. After yesterday’s reversal and lower closes in the US, that theme was extended largely around the world. Japanese shares fell (-0.75%) as did shares everywhere else in Asia (Korea, India, Australia, etc.) except in China, where both mainland and Hong Kong shares were essentially flat. The story is no better in Europe where shares are lower by between -0.7% (DAX ) and -1.1% (CAC, FTSE 100) as investors demonstrate they are concerned with the future. As to the US, at this hour (7:15) futures are very slightly lower.

In the bond market, after yesterday’s poor auction, and ahead of today’s 30-year Treasury auction, yields have fallen from their highest points. Treasury yields (-3bps) are pacing the European sovereign market (Bunds -3bps, OATs -3bps, Gilts -1bp, BTPs -2bps) as the fear factor on stocks seems to be encouraging some haven buying. But the most interesting thing was that JGB yields fell -5bps overnight and are now back down to 0.84%. The BOJ Summary of Opinions (effectively their Minutes) was released last night and clarified that they are not interested in a rapid tightening of policy. Given GDP growth was negative last quarter, this can be no surprise.

In the commodity markets, oil is little changed this morning but has recouped most of its losses from the past week and sits back at $75/bbl. This is still a range-bound situation, and we need something really big to change that. Gold (+1.1%) is making a comeback and back over $2400/oz as the fear factor seems to be playing a role here today. However, copper (-0.2%) continues to demonstrate short-term concerns over economic activity around the world.

Finally, the dollar is having a much less volatile session than we have seen recently. AUD (+0.5%) is the biggest mover I can find after hawkish comments from the RBA, claiming they will not hesitate to raise interest rates again if inflation reappears. However, the yen (+0.15%) seems like it has found at least a temporary home, perhaps gaining some support on what appears to be a risk off day. Funnily, though, the major risk proxies in the EMG space, ZAR and MXN are virtually unchanged this morning. I believe that like most markets today, more clues are sought before views are expressed.

Speaking of clues, this morning brings the other US data with Initial (exp 240K) and Continuing (1870K) Claims at 8:30. Richmond Fed president Barkin speaks at 3:00 this afternoon, the same time we will hear from Banxico on their rate decision (no change expected). But once again, there is not much new information expected, so markets are going to respond, in my view, to equity activity. If US stocks can find support, look for other markets to follow along. However, that does not feel like today’s message. As to the dollar, against the majors, I think it has found a temporary range.

Good luck

Adf