Before we all hear from Chair Jay This morning we’ll see QRA The question is will The bond market kill The vibe all things are okay While no one expects a rate hike Of late, there’s been news not to like Both housing and wages Have moved up in stages Though as yet, there’s not been a spike

We are definitely in a period where there is a huge amount of new information to digest on a daily basis, whether it is data or policy actions by central banks and finance ministries. During times like this, we have historically seen slightly less liquidity in markets as the big market-makers reduce their activity to prevent major blowups. Of course, the result is that we have periods that are quite punctuated by sharp moves on the back of the latest soundbite.

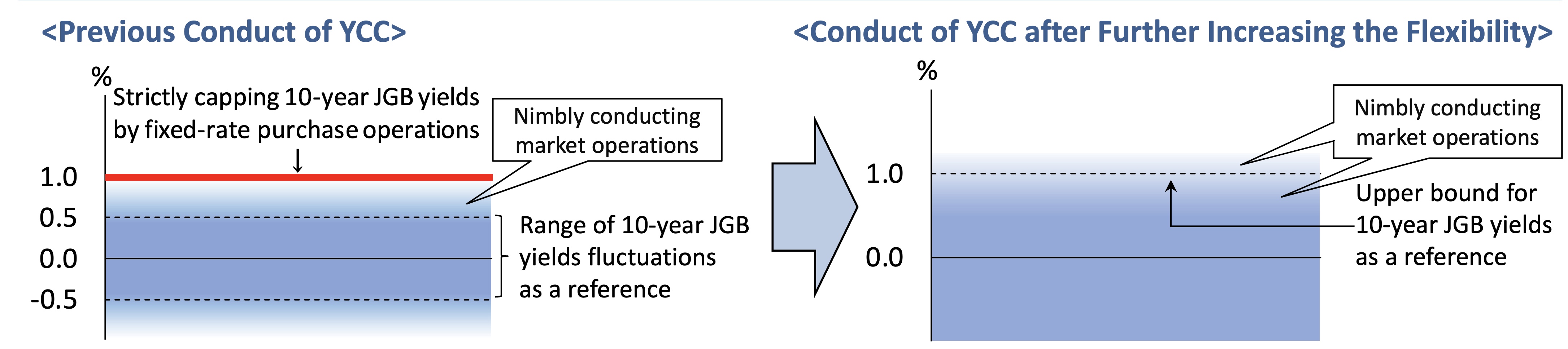

So, with that in mind, let’s look at today’s stories. Starting last night, we saw JGB yields rise to yet another new high for the move, touching 0.98%, before the BOJ executed an unscheduled bond-buying exercise to push back a bit. Ultimately, the 10-year JGB closed back at 0.94%, but despite the brave words from Ueda-san yesterday, it is clear there will be no collapse in the JGB market. They simply will not allow anything like that to happen. At the same time, USDJPY retraced about 0.3% of its recent decline, but continues to hold above 151 for now. We did hear from Kanda-san, the new Mr Yen, that they were watching carefully, but given the rise in JGB yields has been matched by the rise in Treasury yields, it is hard to get too bullish, yet, on the yen.

This is the first big assumption that has not played out as anticipated. Prior to the BOJ meeting, the working assumption was that when they adjusted YCC the yen would start to rally sharply. My view has always been that the yen won’t rally sharply until the Fed changes their tune, and that is not yet in the cards. If the BOJ intervenes, it is probably a good opportunity to sell at those firmer yen levels as until policies change, a weaker yen remains the most likely outcome.

Turning to the US, at 8:30 this morning the Treasury is due to announce the makeup of the $776 billion of debt they will be borrowing this quarter. The key issue is how much will be short-dated T-bills and how much will be pushed out the curve. The higher the percentage of long-dated issuance, the more pressure we will see on the bond market going forward. The 10-year yield is already back to 4.90% this morning, rising another 3bps, and we are seeing pressure throughout Europe as well with yields there up between 1bp and 3bps except for Italian BTPs which have seen yields rise 9bps this morning. That has taken the Bund-BTP spread back to 200bps, the place where the ECB starts to get concerned.

But back to the US, where a second key narrative assumption has been that housing prices would be falling, thus reducing pressure on the inflation metrics over time. Alas, that assumption, too, has been called into question after yesterday’s Case Shiller home price data showed a rise in home prices across the country, back toward the peak seen in June 2022. While the number of transactions continues to decline, given the reduction in both supply and demand it seems that it is still a sellers’ market. If housing prices don’t decline, then it seems even more unlikely that rents will decline and that means that inflation is going to remain much stickier than the Fed would like to see. This does not accord well with the thesis that a slowing economy is going to help bring down housing demand followed by slowing inflation.

As well, there was another data point yesterday, the Employment Cost Index, which rose a more than expected 1.1% Q/Q, and looking at the chart of its recent movement, shows little inclination that it is heading lower. This is a key data point for the Fed as rising wages is something of which they are greatly afraid given the belief in its impact on prices. While the White House may have celebrated the UAW’s ability to extract significant gains from the big three automakers, I’m guessing the Fed was a bit more circumspect on the effects those wage gains will have on overall wages in the economy and inflation accordingly.

Adding all this up tells me that the ongoing belief that inflation is going to be declining steadily going forward, thus allowing the Fed to reduce the Fed funds rate and achieve the highly sought soft-landing is in for a rude awakening. Rather, I remain quite concerned that monetary policy is going to remain much tighter for much longer than the market bulls believe. And that means that I remain quite concerned equity multiples will derate lower along with equity markets overall.

Turning to the overnight price action, after a late rebound in the US taking all three major indices higher on the day, though just by 0.3% or so, we saw a big boost in Tokyo, with the Nikkei jumping 2.4%, as it seems there is joy in the idea that the BOJ may allow yields to rise further. Either that or they were happy to see the BOJ buy bonds, I can’t tell which! Europe, though, is a touch softer this morning with very marginal declines and US futures markets are looking to reverse yesterday’s gains, all -0.35% or so, at this hour (8:00).

Oil prices are higher this morning, up 1.8% as concerns about escalation in the Middle East seem to be growing after some comments about a wider war and further attacks by both Iranian and Hamas leaders. Gold is little changed today but did suffer in yesterday’s month end activity although copper is firmer this morning in something of a surprise given the continuing weak PMI data we have been seeing.

Finally, the dollar continues to flex its muscles as the DXY is back just below 107 with both the euro and pound lower this morning by about -0.25%, and virtually all EEMEA currencies under pressure as well. Other than the yen’s modest rebound, the dollar is higher vs. just about everything.

On the data front, in addition to the QRA and the FOMC later this afternoon, we see ISM Manufacturing (exp 49.0), Construction Spending (0.5%) and JOLTS Job Openings (9.25M). Overnight we saw weaker PMI data from Japan (48.7) and China (Caixin 49.5), although for some reason, European PMI data is not released until tomorrow.

At this point, it is very much a wait and see session but as far as I can tell, the big picture has not yet changed. Inflation remains stickier than the Fed wants, and the market seems to believe which leads me to believe we are going to see yields remain higher for quite a while yet. I would estimate we will see 5.5% 10-year yields before we see 4.5% yields and if that is the direction of travel, equity markets are going to have a tough time while the dollar maintains its bid.

Good luck

Adf