The BOJ did Absolutely nothing new Can we be surprised? The last of the key central bank meetings finished last night with the BOJ not only leaving policy on hold, as expected, but not even hinting that changes were in the offing. Much had been made earlier this month about a comment from Ueda-san that they may soon have enough information to consider policy changes. This was understood to mean that YCC might be ending soon. Oops! If that is going to be the case, it was not evident last night. Rather, the status quo seems the long-term view in Tokyo right now. Not surprisingly, the yen suffered accordingly, selling off another -0.5% overnight and is now back at its weakest point (highest dollar) since October 2022 when the BOJ intervened actively. Also, not surprisingly, after the yen weakened further, we started to hear from the MOF trying to scare the market. FinMin Shunichi Suzuki once again explained that he would not rule out any actions with respect to the currency market if volatility (read depreciation) increased too much. But as of yet, there have been no BOJ sightings and I suspect they will not enter the market until 150.00 is breached once again. Maybe next week. With central bank meetings now past The markets’ response has been fast It seems there’s a pox On both bonds and stocks And owners of both are aghast While further rate hikes may be rare Investors feel some small despair No rate cuts are planned Throughout any land And bond yields are now on a tear Turning to the rest of the G10, what was made clear over the past two weeks is that policy rates are not anticipated to fall anytime soon. While some central banks seemed to finish for sure (ECB, SNB, BOE) others seem like there may be another in the pipeline (Fed, Riksbank, Norgesbank, BOC, RBA), but in no case is there a discussion that inflation has reached a place of comfort for any central bank. Rather, even those banks on hold seem comfortable that policy rates need to remain at current levels in order to continue to battle the scourge of inflation. If anything, the hawks from most central banks continue to push for further tightening, although I suspect that will be a difficult hill to climb given the inherent dovishness of most central bank chiefs. So, what are we to expect if this is the new home for interest rates rather than the ZIRP/NIRP to which we had become accustomed for the past 15 years? The first thing to consider is that despite the higher rate structure, the financial position of the private sector, at least in the US, remains strong. Corporates termed out debt and tend toward being cash rich, so for now, they are benefitting from high interest rates as they locked in low financing and are earning the carry. Many households are in the same position, having refinanced home mortgages at extremely low rates so are not feeling the pain of the recent rise in mortgage rates. Of course, this has reduced the amount of activity in the housing market and is a problem for first-time buyers, but that is not the majority, so net, the pain is not so great. However, the US is unique in this situation as most of the rest of the world are beholden to short-term rates in their financing. This is true in the commercial sector, where bank lending is a far more important part of the capital structure than public debt. Those loans are floating, which is also true in the household sector where most mortgages elsewhere have 5-year fixed terms and so are already repricing higher and impacting homeowners. In fact, if you want one reason as to why the US is likely to outperform the rest of the world, this would be a good place to start. Despite much higher interest rates, the pain is not being felt across much of the US economy while it is being felt acutely throughout Europe and the UK. The upshot of this process is that inflation is likely to remain with us for quite a while going forward. This means that central banks are going to have a great deal of difficulty reversing course absent a major crash in economic activity. Given the US tends to lead the world’s capital markets, it also means that the combination of continuing gargantuan issuance by the Treasury to finance the never-ending budget deficits along with the stickiness of inflation implies that interest rates need to be higher. We saw this price action yesterday with 10yr Treasury yields jumping to 4.5%, another new high for the move, and importantly, a larger move than the 2yr yield. This is the ‘bear steepening’ that I have been writing about, with longer end yields rising faster than shorter yields. Ultimately, this will be quite a negative for risk assets, especially paper ones, although hard assets ought to benefit. The world that we knew has changed, so we all need to adjust accordingly. Turning to the overnight session, yesterday’s US weakness was followed by Japan (-0.5%) but Chinese shares bucked the trend, rising strongly on hopes that the recent data shows the worst is past for the mainland. That seems odd given the lack of additional stimulus forthcoming from the government, but that is the story. European shares are mostly a bit lower this morning after flash PMI data was released showing growth in the Eurozone remains elusive. Germany is still in dire straits with its Manufacturing PMI <40, but the whole of Europe is sub 50 for the past four months at least. Finally, US futures are bouncing slightly this morning, but that seems like a trading reaction to two consecutive days of sharp losses rather than new optimism. Other than YK Gilts, which traded at much higher levels back in August, European sovereigns are following Treasury yields to their highest level in more than a decade. And despite the weak economic story, the fact remains that sticky inflation is the clear driver for now. Consider that the ECB has essentially explained they have finished raising rates with their policy rate at 4.0% while CPI is running at 5.2% headline and 5.3% core. Those numbers do not inspire confidence that the ECB has done its job. I continue to look for higher long-term yields going forward. Part of the reason for this is that oil (+0.9%) continues to find support. While it had a couple of days of a modest pullback, we are back above $90/bbl and the news remains bullish the outcome. The latest is the Russia is halting deliveries of diesel fuel, a particular sore spot as there are already tight supplies around the world, especially here in the US. I see no reason for oil to decline structurally, and that is going to continue to pressure inflation higher. Perhaps of more interest is the fact that the metals complex is rallying today, despite the rise in interest rates. Gold (+0.3%), silver (+1.3%), copper (+0.8%) and aluminum (+1.1%) are all in the green. Again, I would say that owning hard assets is going to be a better outcome than paper ones. Finally, the dollar is mixed this morning, showing gains against the euro, pound and yen, but softer vs. the commodity bloc with AUD, NZD, CAD and NOK all firmer this morning. As well, EMG currencies are having a better session, rising a bit vs. the greenback, but recall, the dollar has had quite a good run lately. My take is there is a lot of profit-taking as we head into the weekend given the lack of fundamental stories that would undermine the buck. Nothing has changed my view it has further to rise. On the data front, the only releases are the flash PMIs here (exp 48.0 Manufacturing, 50.6 Services) and we get our first Fed speaker, Governor Lisa Cook, a confirmed dove. We have already had a lot of activity this week so I suspect that heading into the weekend, it is going to be a quiet session as traders and investors start to plan for next week’s excitement. Good luck and good weekend Adf

Tag Archives: #BOJ

Concerns Are Severe

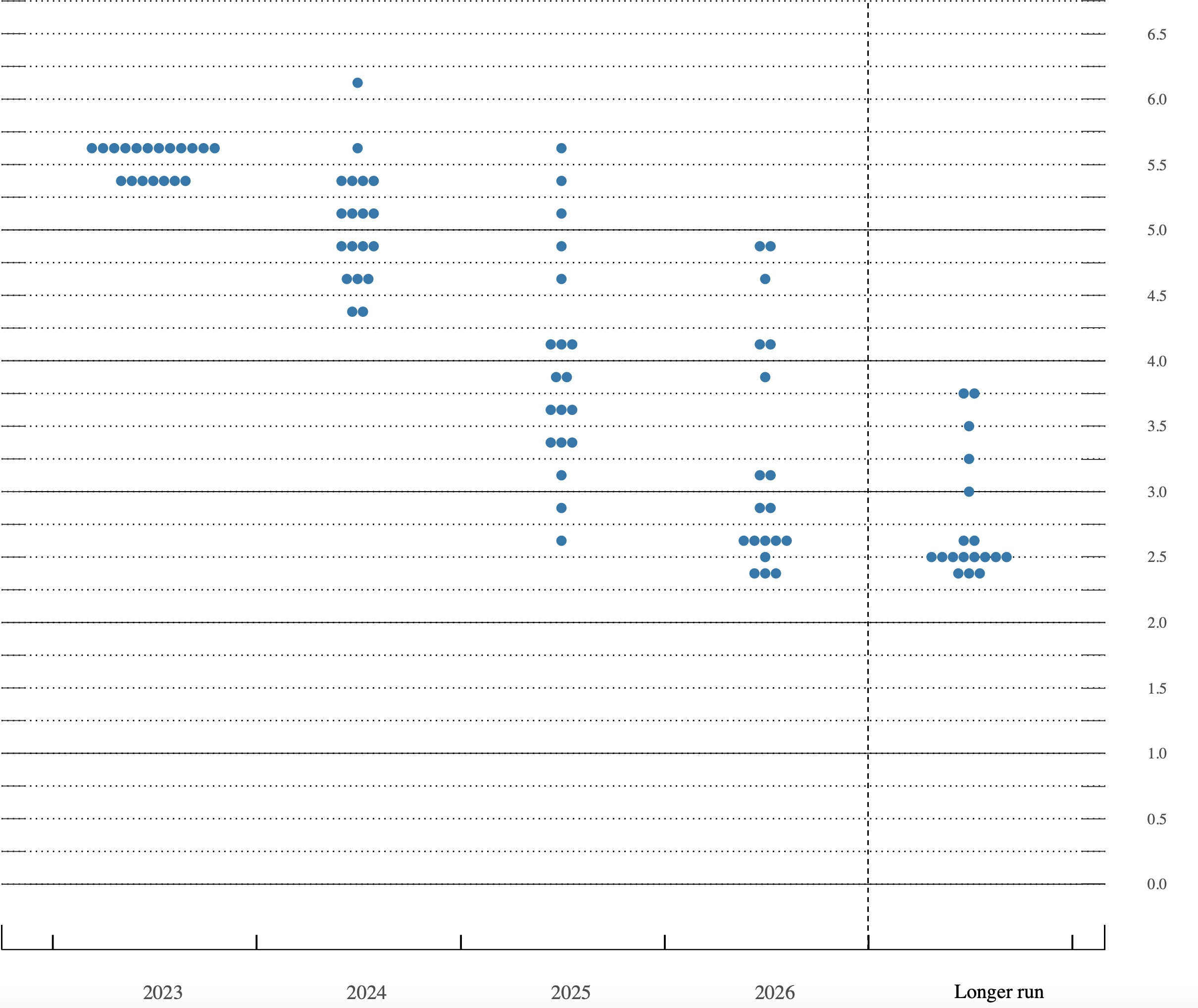

One look at the dot plot makes clear Inflation concerns are severe So, higher for longer Is growing still stronger And Jay implied few cuts next year

First, let’s recap the FOMC meeting. The term hawkish pause had been used prior to the meeting as an expectation, and I guess that was a pretty apt description. While they left policy on hold, as expected, the change in the dot plots, as seen below, indicate that even the doves on the Fed see fewer rate cuts next year, with just two now priced in from four priced in June.

Source: Fedreserve.gov

A quick reading shows that a majority of members expect one more hike this year, and now the median expectation for the end of 2024 has moved up to 5.125%, so 50bps lower than the median expectation for the end of 2023 and 50bps higher than the June plot. To me, what is truly fascinating is the dispersion of expectations in 2025 and 2026, where there are clearly many opinions. And finally, the longer run expectation has risen to 2.5% with many more members thinking it should be even higher than that. The so-called neutral rate estimations seem to be creeping higher. If you think about it, that makes some sense. After all, given the ongoing forecasts for continued labor market tightness due to demographic concerns, and add in the massive budget deficits leading to significantly higher Treasury debt issuance, there is going to be pressure on rates to find a higher level.

The market response was quite negative, albeit not immediately, only after Powell started speaking. But in the end, equity markets fell across the board in the US, with the NASDAQ taking the news the hardest, down -1.5%, as its similarity to long duration bonds was made evident. Asian markets all fell overnight as well, with most tumbling more than -1.0% and European bourses are all under similar pressure, down -1.0% or so as well. The one exception in Europe is Switzerland, where the SNB surprised the market and left rates on hold resulting in a weaker CHF and a very modest gain in their equity market.

However, the bigger market response was arguably in bonds, where yields rose to new highs for the move with the 2yr at 5.15% and the 10yr at 4.43%. Once again, I point to the significant increase in debt that will be forthcoming from the US Treasury as they need to fund those budget deficits. I have been making the case that a bear steepener would be the more likely outcome for the US yield curve. That is where long-term rates rise more quickly than short-term rates due to the US fiscal policy and shrinking demand for US debt by key players, notably the Fed, but also China and Japan. Nothing has changed that view.

Then early this morning, up north Both Sweden and Norway brought forth A quarter point hike To act as a dike Preventing price rises henceforth

After the Fed’s hawkish pause, we turn our attention to Europe, where the early movers, Sweden and Norway, both hiked twenty-five basis points, as expected, while both hinted that further hikes are not out of the question. Inflation remains higher than target in both nations and in both cases, the currency has been relatively weak overall. Switzerland left rates on hold, pointing to the fact that for the past three months, inflation has been within their target range, and they are beginning to see downward pressure on economic activity which they believe will keep that trend intact.

And lastly, from London we’ve learned Another rate hike has been spurned Though voting was tight They said they’re alright With waiting to see if things turned

As to the bigger story, the UK, expectations were split on a hike after yesterday’s tamer than expected CPI report while the pound fell ahead of the news. And the change in expectations was appropriate as in a 5-4 vote, the BOE opted to remain on hold for the first time in two years. They see that inflation may be easing more rapidly than previously expected, and they are concerned about overtightening. While I have a hard time understanding how a 5.15% Base rate is tight compared to CPI running at 6.7% and core at 6.2%, I am clearly not a central banker. At any rate, the pound fell further on the news and is now at its lowest level since March, while the FTSE 100 rallied back and is close to flat on the day from down nearly -1.0% before the announcement. Gilt yields, however, are moving higher as the bond market there doesn’t seem to believe that the BOE is serious about fighting inflation.

And really, those are today’s key stories. Late yesterday, Banco Central do Brazil cut the SELIC rate by 0.50%, as expected, and at the same time the BOE announced, the Central Bank of Turkey raised their refinancing rate by 5 full percentage points, to 30.0%, exactly as expected. And to think, we get concerned over rates at 5%!

As to the rest of the day, there is a bunch of US data as follows: Philly Fed (exp -0.7), Initial claims (225K), Continuing Claims (1695K), Existing Home Sales (4.1M) and Leading Indicators (-0.5%). As is typical, there are no Fed speakers scheduled the day after the FOMC meeting, but we will start to hear from them again tomorrow.

Putting it all together tells me that the Fed is not nearly ready to back off their current stance and will need to see substantial weakness in economic activity before changing their mind. Meanwhile, last week’s ECB meeting and this morning’s BOE meeting tell me that the pain of higher interest rates in Europe is becoming palpable and the central banks are leaning more toward inflation as an outcome despite their mandates. This continues to bode well for the dollar as the US remains the place with the highest available returns in the G10.

Tonight, we hear from the BOJ, where no change is expected. I would contend, though, that the risk is there is some level of hawkishness that comes from that meeting as being more dovish seems an impossibility. As such, there is a risk that the yen could see some short-term strength. Keep that in mind as you look for your hedging levels.

Good luck

Adf

Some Dismay

While everyone’s certain that Jay Will leave rates alone come Wednesday The curve’s longer end Is starting to trend Toward rates that might cause some dismay The problem remains his frustration That he can do naught ‘bout inflation As oil keeps rising It’s demoralizing For Jay and his rate formulation

The overnight session was quite dull overall with virtually no new data or information on the macroeconomic front and a limited amount of commentary from the central banking and financial poohbahs of the world. Friday’s desultory US equity market performance was followed by a mixed session in Asia while European bourses are all in the red after the Bundesbank indicated that Germany would have negative growth in Q3. As well, after last week’s ECB rate hike, we did hear from one of the more hawkish members that further hikes are possible, although listening to Madame Lagarde’s comments, that seems quite a high bar at this time.

So, given the limited amount of new information, it seems that it is time for central bank prognostications. The first thing to note is that while the Fed is certainly the main act this week, there are no less than a dozen other major interest rate decisions due this week including the BOE, BOJ, PBOC, Swedish Riksbank, Norgesbank, SNB and Banco Central do Brazil.

While much has been written about the FOMC on Wednesday, with the current market pricing just less than a 1% probability of a hike, the European banks that are meeting are all expected to follow the ECB and hike by 25bps. Meanwhile, the PBOC remains caught between a rock (slowing economic growth) and a hard place (a weakening currency) and seems highly likely to follow the Fed’s lead and leave rates on hold.

The BOJ is also very likely to leave their rate structure on hold, but questions keep arising regarding any other potential tweaks to the YCC framework. However, given the relatively strong denials of anything like that from Ueda-san at the end of last week, I am inclined to believe they are comfortable where they are.

Finally, a look down south shows that Brazil is forecast to cut the SELIC rate (their Fed funds equivalent) by 50bps to 12.75% with a handful of analysts calling for a 75bp cut. Of course, inflation in Brazil has fallen from effectively 12% last summer to 4.65% now, so real rates are still remarkably high there which is the key reason the real has been such a great performer over the past twelve months, having risen ~8%.

The only market that is really showing much movement is oil, which is higher yet again this morning, by another 0.5% and now above $91/bbl. It is becoming very clear that the OPEC+ production cuts are having the impact that MBS desired, with tightening supply meeting ongoing demand growth, despite slowing economic activity. The one thing that should remain abundantly clear to all is that no amount of effort by Western governments to reduce demand for fossil fuels is going to have the desired impact as developing nations will not be denied their opportunities to improve their own economic situation and that generally takes access to energy. To date, fossil fuels continue to prove to be the most cost-effective and efficient sources, so that demand will just not abate. Oil prices are going to continue to head higher, mark my words.

And truthfully, on this rainy Monday morning in NY, that is pretty much all the excitement that we have ongoing. The data this week is focused on Housing and expectations are as follows:

| Tuesday | Housing Starts | 1437K |

| Building Permits | 1440K | |

| Wednesday | FOMC Rate Decision | 5.50% (current 5.50%) |

| Thursday | Initial Claims | 225K |

| Continuing Claims | 1695K | |

| Philly Fed | -1.0 | |

| Existing Home Sales | 4.10M | |

| Leading Indicators | -0.5% | |

| Friday | Flash PMI Manufacturing | 48.2 |

| Flash PMI Services | 50.6 |

Source: Bloomberg

A side note regarding the data is that the Leading Indicators Index is forecast to decline again, which will be the 17th consecutive decline, a very strong indication that future economic activity seems likely to suffer. Of course, this is just one of the numerous signals of an impending recession (inverted yield curve, ISM/PMI sub 50.0, etc.) that have yet to play out as they have done historically. Perhaps the UAW strikes will be enough to tip things over, especially if they widen in scope, but that seems premature.

In addition, we are beginning to hear more about a potential government shutdown as the House has not yet completed its funding bills but my take here is that while the rhetoric may heat up, the reality is that a continuing resolution will be passed and that this is just another tempest in a teapot in Washington, SOP really.

When looking a little further ahead, I continue to see a far better chance that the Fed remains the most hawkish of the major central banks, and that higher for longer really means just that. Economic activity elsewhere, notably in Europe and China, is suffering far more acutely than in the US, at least statistically, and that implies that this week’s rate hikes across the UK and the continent are very likely the end of the cycle. I am not convinced that the Fed is done. That combination leads me to continue to look for relative dollar strength over time. For asset/receivables hedgers, keep that in mind.

Good luck

Adf

Goldilocks Dream

It seems many thought the word ‘could’ Was feeble when posed against ‘would’ The fact Chairman Jay Had phrased things that way Last month, for the bulls, is all good And so, the new narrative theme Is Jay is convincing his team No more hikes are needed And they have succeeded In reaching the Goldilocks dream

The following quote from a weekend WSJ article by Fed whisperer Nick Timiraos is almost laughable in my mind.

This is apparent from how Fed Chair Jerome Powell recently described the risk that firmer-than-expected economic activity would slow recent progress on inflation. Last month, he twice used the word “could” instead of the more muscular “would” to describe whether the Fed would tighten again.Evidence of stronger growth “could put further progress at risk and could warrant further tightening of monetary policy,” he said in Jackson Hole, Wyo.

Talk about parsing language to the nth degree! I bolded the line that I found the most ridiculous, but as we all know, my view does not drive the markets nor policy. However, as I had written last week, we have definitely seen a shift amongst some of the FOMC members with respect to the idea of another rate hike this year. Timiraos is widely believed to have the inside track to Chairman Powell, and now that the FOMC is in their quiet period ahead of the September 20th meeting, this will be the mode of communication.

I guess the big risk of going all in on the Fed is done is we are still awaiting CPI Wednesday morning and with energy prices continuing to climb, I fear the opportunity for a high surprise is very real. Literally every story that is written in the mainstream media these days tries to talk up the prospects of the economy and, correspondingly, for further equity market gains. To me, there is a lot of whistling past the graveyard here, but so far, equities have held in despite some weaker data. The one thing I would highlight is the market feels quite complacent with implied volatility across numerous markets, stocks, bonds, commodities and FX, all quite low. Hedge protection is cheap here, if you need to hedge something, don’t wait for the move.

Ueda explained We may soon understand if Inflation is back

“If we judge that Japan can achieve its inflation target even after ending negative rates, we’ll do so,” said Ueda. This was the key sentence in a weekend interview published last night. The market response was immediate with the yen jumping more than 1% in the early hours of Asian trading before ceding a large portion of those gains when Europe walked in the door. However, regardless of today’s price action, there is a longer-term signal here that is important to understand. It has become clear that the BOJ is becoming somewhat uncomfortable with the speed of the yen’s decline. Prior to last night’s session, the yen had fallen 7.75% from July’s levels, which is a pretty big move for less than 2 months. There is no secret to why the yen continues to decline, the vast policy differences between the US and Japan are sufficient reason. While Ueda-san made no promises, this was very clearly a signal that a change is coming soon. In the near-term, hedgers need to be very careful and those who are hedging JPY assets or revenues should really consider buying JPY puts outright or via collars as there is every reason to believe that further yen strength is coming by the end of the year.

Meanwhile, on the western edge of the Yellow Sea, the PBOC was quite vocal last night as well. On the back of Chinese monetary data that showed a larger rebound than forecast in New Loan data as well as Aggregate Financing data, the PBOC issued the following statement, “Participants of the foreign exchange market should voluntarily maintain a stable market. They should resolutely avoid behaviors that disturb market orders such as conducting speculative trades.” That is very clear language that the PBOC is unhappy with the recent CNY performance. In addition, the PBOC issued new regulations regarding large purchases of dollars telling banks that any corporate client that wants to purchase more than $50 million will need to get approval to do so, and that approval will take quite some time to be forthcoming.

It should be no surprise that the renminbi is stronger this morning, having rallied 0.65% and thus closing the gap with the CFETS fix for the first time in months. Of course, given the double whammy of Japanese and Chinese policy implications, it should be no surprise that the dollar is softer overall. Especially when considering the WSJ article explaining that the Fed may be finished hiking rates. So, we have seen the dollar fall against all its counterparts in the G10 and most in the EMG blocs. Aside from the yen (+0.65%), we have seen the most strength in AUD (+0.8%) which has benefitted from the overall Chinese story, both the currency issues and the better data, as well as the rise in commodity prices. Kiwi (+0.55%) and SEK (+0.45%) are next on the list as there is broad-based dollar weakness today after an eight-week run higher.

In the emerging markets, ZAR (+1.1%) is actually the best performer on the commodity story as well as the general dollar weakness, but after that and CNY, HUF (+0.6%) is the only other currency in the bloc with substantial gains. The story here is what appears to be a shift from zloty to forint as the market continues to punish PLN (-0.35%) after the surprisingly large rate cut last week by the central bank there. Net, however, the dollar is clearly under pressure this morning.

If we turn to other markets, though, things don’t seem to make as much sense. For instance, oil prices (-0.4%) are a bit softer while metals prices (AU +0.4%, CU +1.7%, AL +1.0%) are all firmer. Now, the metals seem to be behaving well on the back of the dollar’s weakness, but oil’s decline is not consistent with that view.

In the equity markets, last night saw a mixed picture in Asia with the Nikkei (-0.4%) and Hang Seng (-0.6%) both under pressure while the CSI 300 (+0.75%) and ASX 200 (+0.5%) both responded well to the news. For the Nikkei, the combination of prospects of higher rates and a stronger yen are both negative for Japanese stocks, while much of the rest of APAC benefitted from the Chinese story. In Europe, the bourses are all green, averaging about +0.5% as investors continue to believe the ECB is done hiking rates with the market now pricing less than a 40% probability of a hike this week and not even one full hike priced into the curve over time. US futures are also green as investors embrace the WSJ article’s hints that the Fed is done.

Finally, the big conundrum is the bond market, which is selling off across the board. Or perhaps it is not such a conundrum. If both the Fed and ECB are done hiking despite inflation continuing at a pace far above target, then the attractiveness of holding duration wanes dramatically. Add to that the gargantuan amount of debt yet to be issued and the fact that the biggest buyers of the past decades, China and Japan, seem to be backing away from the market, and it will require much higher yields for these issues to clear. Of course, one could also look at this as a risk-on session with stocks higher and bonds getting sold along with the dollar, so perhaps that is today’s explanation. Just beware the movement here. 10-Year Treasury yields (+3bps) are back to 4.30%, and if the story is no more Fed tightening thus higher inflation, that is unlikely to be a long-term positive for equities. At least that’s what history has shown.

On the data front, the back half of the week brings the interesting stuff.

| Tuesday | NFIB Small Biz Optimism | 91.5 |

| Wednesday | CPI | 0.6% (3.6% Y/Y) |

| -ex food & energy | 0.2% (4.3% Y/Y) | |

| Thursday | ECB Rate Decision | 3.75% (current 3.75%) |

| Initial Claims | 227K | |

| Continuing Claims | 1695K | |

| Retail Sales | 0.1% | |

| -ex autos | 0.4% | |

| PPI | 0.4% (1.3% Y/Y) | |

| -ex food & energy | 0.2% (2.2% Y/Y) | |

| Friday | Empire Manufacturing | -10.0 |

| IP | 0.1% | |

| Capacity Utilization | 79.3% | |

| Michigan Sentiment | 69.2 |

Source: Bloomberg

As we are in the Fed quiet period, there will be no Fedspeak, so it is all about the data this week. Beware a hot CPI print as that will pressure the narrative of the soft landing. This poet’s view is no soft landing is coming, rather a much harder one is in our future, but at this point, probably not until early next year. Until then, and despite today’s news cycle, I still think the dollar is best placed to rally not fall.

Good luck

Adf

Quickly Slowing

We will take action Threatened Vice FinMin Kanda If you speculate

“If these moves continue, the government will deal with them appropriately without ruling out any options.” So said Vice FinMin Masato Kanda, the current Mr Yen. Based on these comments, one might conclude that ‘evil’ speculators were taking over the FX market and distorting the true value of the yen. One would be wrong. The below chart shows the yields for 10yr JGBs vs 10yr Treasuries. You may be able to see that the most recent readings show a widening in that yield spread in the Treasury’s favor. It cannot be a surprise that investors continue to seek the highest return and the yen most certainly does not offer that opportunity.

While I don’t doubt there is a place where the BOJ/MOF will intervene, they know full well that the yen’s weakness is a policy choice, not a speculative outcome. They simply don’t want to admit it. The upshot is that the yen edged a bit higher overnight, just 0.2%, as market realities are simply too much for words to overcome. The yen has further to fall unless/until the BOJ changes its monetary policy and ends YCC while allowing yields in Japan to rise. Until then, nothing they can say will prevent this move.

While ECB hawks keep on screeching More rate hikes are not overreaching The data keeps showing That growth’s quickly slowing So, comments from Knot are just preaching

“I continue to think that hitting our inflation target of 2% at the end of 2025 is the bare minimum we have to deliver. I would clearly be uncomfortable with any development that would shift that deadline even further out. And I wouldn’t mind so much if it shifted forward a little bit.” These are the words of Dutch central bank chief and ECB Governing Council member Klaas Knot. As well, he intimated that the market might be underestimating the chance of a rate hike next week, which at the current time is showing a 33% probability. Another hawk, Slovak central bank chief Peter Kazimir also called for “one more step” next week on rates.

The thing about these comments is they came in the wake of a German Factory Orders number that was the second worst of all time, -11.7%, which was only superseded by the Covid period in March 2020. Otherwise, back to 1989, Factory Orders have never fallen so quickly in a month. This is hardly indicative of an economy that is going to grow anytime soon. Rather, it is indicative of an economy that has inflicted extraordinary harm to itself through terrible energy policies which have forced producers to leave the country.

The key unknown is whether the slowing economic growth will also slow price growth. Given oil’s continued recent strength, with no reason to think that process is going to change given the supply restrictions we have seen from the Saudis and Russia, I fear that Germany is setting up for a very long, cold winter in both meteorological and economic terms. With the largest economy in the Eurozone set to decline further, it is very difficult to be excited at the prospect of a stronger euro at any point in time. It feels to me like the late summer downtrend in the single currency has much further to go.

This is especially true if the US economy is actually as resilient in Q3 as some economists are starting to say. Yesterday, I mentioned the Atlanta Fed GDPNow number at 5.6%, but we are seeing mainstream economists start to raise their Q3 forecasts substantially at this point given the strength that was seen in July and August. Not only will this weigh on the single currency, and support the dollar overall, but it may also put a crimp in the view that the Fed is done hiking rates. Consider, if GDP in Q3 is 3.5% even, it will not encourage the Fed that inflation is going to slow naturally. And while they may pause again this month, it seems highly likely they would hike again in November with that type of data.

Which takes us to the markets’ collective response to all this news. Risk is definitely under some pressure as the combination of stickier inflation and slowing growth around the world is weighing on investors’ minds. The only market to manage a gain overnight was the Nikkei (+0.6%) which continues to benefit from the weaker yen, ironically. But China, which is also growing increasingly concerned over the renminbi’s slide, remains under pressure as do all the European bourses and US futures. Good news is hard to find right now.

Meanwhile, bond investors are in a tough spot. High inflation continues to weigh on prices, but softening growth, everywhere but in the US it seems, implies that yields should be softening with bond buyers more evident. This morning, 10yr Treasury yields are lower by 2bp, but that is after rallying 16bps in the past 3 sessions, so it looks like a trading pullback, not a fundamental discussion. But in Europe, sovereign yields are edging higher as concern grows the ECB will not be able to rein in inflation successfully. As to JGB yields, they seem to have found a new home around 0.65%, certainly not high enough to encourage yen buying.

Oil prices (-0.1%) while consolidating this morning, continue to rally on the supply reduction story and WTI is back to its highest level since last November. Truthfully, there is nothing that indicates oil prices are going to decline anytime soon, so keep that in mind for all needs. At the same time, metals prices are mixed this morning with copper a bit softer and aluminum a bit firmer while gold is unchanged. It seems like the base metals are torn between weak global economic activity and excess demand from the EV mandates that are proliferating around the world. Lastly a word on uranium, which continues to trend higher as more and more countries recognize that if zero carbon emissions is the goal, nuclear power is the best, if not only, long term solution. The price remains below the marginal cost of most production but is quickly climbing to a point where we may see new mining projects announced. For now, though, it seems this price is going to continue to rise.

Finally, the dollar is mixed this morning, having fallen slightly vs. most G10 currencies, but rallied slightly vs. most EMG currencies. This morning we will hear from the Bank of Canada, with expectations for another pause in their hiking cycle, but promises to hike again if needed. Meanwhile, the outlier in the EMG bloc is MXN (-0.7%) which seems to be a victim of the overall risk situation as well as the belief that its remarkable strength over the past year might be a bit overdone. In truth, this movement, five consecutive down days, looks corrective at this stage.

On the data front, we see the Trade Balance (exp -$68.0B) and ISM Services (52.5) ahead of the Beige Book this afternoon. We also hear from two FOMC members, Boston’s Susan Collins and Dallas’s Lorrie Logan. Yesterday, Fed Governor Waller indicated that while right now, the data doesn’t point to a compelling need to hike, he is also unwilling to say they have finished their task. However, that is a far cry from the Harker comments about cutting in 2024 seems appropriate. I suspect Harker is the outlier for now, at least until the data truly turns down.

Net, the big picture remains that the US economy is outperforming the rest of the world and the Fed is likely to retain the tightest monetary policy around, hence, the dollar still has legs in my view.

Good luck

Adf

Just Kidding

Remember Friday When one percent was declared The top? Just kidding

Much has been written about the BOJ’s surprising change in policy at their meeting last Friday, when they ostensibly widened the cap on their Yield Curve Control to 1.00% while explaining that flexibility in operations was the watchword. They did not touch their overnight rate, which remains at -0.10% and there is no apparent belief that they are going to adjust that anytime soon.

Neither market pricing in the OIS market nor any commentary from any BOJ official has hinted at such a move. So, the question is, did they really change their policy?

This matters a great deal for those amongst us who care about USDJPY and its potential future direction. The prevailing narrative has been that once the BOJ altered policy and allowed Japanese interest rates to rise to a more normal setting, investment would flow into JGBs, and the yen would strengthen rapidly. Remember, a big part of this process is that since the yen is the last remaining currency with negative interest rates in the front end of the curve, it remains the financing currency of choice amongst the speculative and hedge fund set. Adding to this discussion was the fact that back in December of last year, when Kuroda-san truly surprised the market by raising the YCC cap from 0.25% to 0.50%, it took less than one day for the 10-year JGB yield to test the new cap. Expectations recently had been that a similar move was likely to be seen this time around as well.

Alas, it is Monday, so some thirty-six market hours into the new policy and already the BOJ has stepped into the market to prevent a further rise in the 10-year yield once it touched 0.60%. Last night they stepped in with a ¥300 billion program of additional QE. One cannot be surprised that USDJPY (+0.9%) is higher on this news as it undermines the entire thesis about imminent JPY strength once they changed policy. And if they didn’t really change policy, as evidenced by the fact that they have already stepped into the market, then THE key pillar of the stronger yen thesis has just been removed. The other problem for the yen bulls is that the US data last week, especially the GDP and IP data, indicate that the Fed will be under no duress if they continue to tighten policy beyond current levels. Despite all the arguments about the Fed making another policy error, and there are sound arguments there, in Jay Powell’s eyes, until NFP starts to fall sharply, or Unemployment starts to rise sharply, or both, there are no impediments to a continuation of the current tightening policy.

It is with this in mind that I foresee continued strength in USDJPY, and while it seems likely that a very rapid move higher will see further intervention by the BOJ/MOF like we saw last autumn, another test of 150 is in the cards. A quick look at the chart below (from tradingeconomics.com) shows that the trend higher in the dollar remains intact with the decline in the first part of July already mostly undone. For those of you who were looking for a reversion to the 120 or 130 level, I fear that is just not in the cards for a long time to come.

Last Thursday the ECB said That policy, looking ahead Need not be so tight And so, they just might Stop raising rates, pausing instead Though their only mandate is prices They’ve come to a bit of a crisis Seems growth’s really weak And so, they will seek A policy, sans sacrifices

The good news in Europe is that Q2 GDP was positive, which followed a negative Q4 and a flat Q1. Hooray! The bad news about the data, which showed a 0.3% rise, is that fully half that number comes from Ireland! Now, Ireland’s weight in the Eurozone economy is tiny, about 4%, so the fact that growth there represented half the entire EZ’s growth is remarkable. However, if you consider that this growth is more illusion than economic activity, it is easier to understand. The growth is a result of the large profitability of US tech companies that generate their profits, from an accounting perspective, in Ireland to take advantage of the extremely low Irish corporate tax rate of 12.5%. So, US tech companies had a good quarter driving Irish GDP higher, and by extension Eurozone GDP higher. But they didn’t really produce that much stuff.

At the same time, Core CPI in the Eurozone printed at 5.5% this morning in July’s preliminary reading, hardly indicative of a collapse and calling into question Lagarde’s seeming dovishness last week. In the end, the dichotomy between the US economy, where the latest data continues to show a robust outcome, and Europe, where the only thing rising is prices with economic activity lackluster at best, remains the key reason why the dollar’s demise is still a theory and not reality.

To summarize the information that we have received from around the world in the past several days, Japan is unwilling to allow interest rates to rise very far, European growth is staggering, US growth is accelerating, the ECB is inclined to stop hiking rates and the Fed continues with ‘higher for longer’. All of this points to the dollar maintaining its value and likely rising further. I have yet to see anything persuasive in the dollar bear case to address all these issues.

Now, those are the big picture views, but let’s take a quick tour of the overnight session. Equities rallied in Asia following the US performance on Friday, but Europe has been a bit more circumspect with a couple of markets showing gains, notably France and Italy, but the rest doing nothing at all. At the same time, US futures are little changed at this hour (7:30).

Arguably, though, it is the bond market where things are really interesting as yields continue to rebound. US Treasuries are higher by 1.5bps and pushing back to that all important 4.00% level this morning. There is a growing belief that if 10-year yields push above 4.10%, that may signal a new framework, a breakout in technical terms, and we could see much higher yields from there. The Fed is likely to welcome such an event as it will help tighten financial conditions, something that they have been unable to achieve thus far. However, I do not believe the equity markets would take kindly to that type of movement, so beware. As to European sovereigns, they are mostly higher by about 1bp-2bps this morning and of course, JGBs saw yields finish higher by 6bps, just below 0.60%.

Oil prices (+1.0%) continue to rise on an organic basis. By this I mean there have been no announcements, no disruptions and no news of any sort that might indicate a change in the current situation. In other words, there is just a lot of buying going on. WTI is well above $81/bbl and we have seen a gain of more than 16% in the past month. Headline inflation will not be sinking on this news. We are also seeing a little strength in the metals space this morning with gold, copper and aluminum all firmer as the week begins. The base metals are responding to continued indications that China is going to support their economy, although direct fiscal payments don’t yet seem likely. Just wait a few months.

Finally, the dollar is net, little changed, although we have a wide array of gainers and losers today. In the G10, AUD (+0.9%) and NZD (+0.75%) are the leaders, rallying alongside the commodity rally, while JPY (-0.8% now), is the laggard based on the discussion above. As to the rest of the bloc, there are more gainers than losers, but the movement has been far less impactful. In the EMG space, MYR (+1.1%) has been the leading gainer on significant (for Malaysia) equity market inflows of ~$40mm -$50mm last night. After that, though, the gainers have mostly been EEMEA currencies, and they have not moved that much. On the downside, ZAR (-0.7%) is the laggard on limited news, implying more of a trading action rather than a fundamental shift. But on this side of the ledger as well, things haven’t moved that far and net, the space is little changed.

It is an important week for data in the US culminating in the payroll report on Friday.

| Today | Chicago PMI | 43.4 |

| Dallas Fed Mfg | -22.5 | |

| Tuesday | JOLTS Job Openings | 9600K |

| ISM Manufacturing | 46.9 | |

| Wednesday | ADP Employment | 183K |

| Thursday | Initial Claims | 227K |

| Continuing Claims | 1723K | |

| Unit Labor Costs | 2.5% | |

| Nonfarm Productivity | 2.2% | |

| Factory Orders | 2.1% | |

| ISM Services | 53.0 | |

| Friday | Nonfarm Payrolls | 200K |

| Private Payrolls | 175K | |

| Manufacturing Payrolls | 5K | |

| Unemployment Rate | 3.6% | |

| Average Hourly Earnings | 0.3% (4.2% Y/Y) | |

| Average Weekly Hours | 34.4 | |

| Participation Rate | 62.6% |

In addition to this, we get the first post-FOMC Fedspeak with just two speakers, Goolsbee and Barkin, on the calendar this week although the pace picks up next week. As long as the data remains strong, I see no reason for the Fed to change its tune nor any reason for the dollar to back off its recent net strength.

Good luck

Adf

A Suggestion

Nought point five percent Is not a rigid limit It’s a suggestion At least that is the word we got last night from Kazuo Ueda, BOJ Governor when he announced some surprising policy changes. No longer would 10-yr JGBs be targeted to yield 0.0% +/- 0.50%, which in practice had meant a 0.50% cap. Going forward, the BOJ would buy an unlimited amount of JGBs at 1.0%, if necessary, as its new framework. Perhaps the most humorous part of the concept was the suggestion that they always saw the 0.50% cap “as references, not as rigid limits, in its market operations.” That’s right, after 7 years of a seemingly explicit cap on JGB yields, with the BOJ willing to buy unlimited amounts in order to prevent yields from climbing, now they mention it was merely a suggestion, a guideline rather than a hard limit. It is commentary of this nature that tends to undermine investor trust in central bankers. Given the surprising nature of the policy changes, although they left their O/N financing rate at -0.10%, it should be no surprise that the market had some large, short-term responses. JGB yields jumped 10bps on the news, trading to a new 9-year high at 0.575% before slipping back a few bps to close the week. The Nikkei, meanwhile, fell nearly 2.5% in the immediate aftermath of the decision, but rallied back all afternoon there to close lower by just -0.4%. It turns out the financial sector benefitted greatly as higher rates really helps them. As to the yen, it saw substantial short-term volatility, as ahead of the meeting it weakened nearly 1.75%, trading above 141.00, but very quickly reversed course and rallied > 2% as the dollar briefly fell to 138.00. In the end, though, the yen is just a hair stronger on the day now, back near 139.50 where things started. The lesson, I think, is that policy shifts tend to have very immediate consequences, but the longer term impacts, especially in the currency market where we have a lot of moving pieces between the Fed, ECB and BOJ, will take longer to play out.

In Europe, inflation remains The issue that’s caused the most pains But growth there is stalling So, Christine is calling For slowing the rate hike campaigns

“We have an open mind as to what decisions will be in September and subsequent meetings…We might hike, and we might hold. And what is decided in September is not definitive, it may vary from one meeting to another,” Lagarde said.It was with these words that Madame Lagarde informed us the rate hiking cycle in the Eurozone may have ended. Despite the fact that core CPI remains above 5.0% while their deposit rate is now at 3.75%, seemingly not high enough to effectively combat the inflation situation, it is becoming ever clearer that the European growth story is starting to slide. This is in direct contrast to the US growth story, which based on yesterday’s extremely robust data, shows no signs of fading.

But as I have written numerous times in the past, once the Fed is perceived to have stopped raising interest rates, it was clear the ECB would be right behind them. The entire basis of my stronger dollar thesis has been that other central banks will find it very difficult to tighten policy aggressively to fight inflation if the Fed has stopped doing so.

In the end, no country really wants a strong currency as the mercantilist tendencies of every country, seeking to increase exports at the expense of their domestic inflation situation, remains quite strong. Faster growth with higher inflation is a much preferred economic outcome for essentially every government than slower growth with low inflation. Inflation can always be blamed on someone else (greedy companies, Ukraine War, OPEC+, supply chain disruptions) while faster growth can be ‘owned’ by the government.

So, between the ECB and BOJ, we did see further policy tightening in line with the Fed’s actions on Wednesday. Arguably, the difference is that the US economic data continues to be quite strong, at least on the surface. Yesterday’s first look at Q2 GDP printed at 2.4%, much higher than expected and showing no signs of the ‘most widely anticipated recession in history.’ The strength was seen in Government spending (IRA and CHIPS Act), Private Domestic Investment (which is directly related to that as companies build out new plant infrastructure) and Services, i.e. travel and restaurants. Once again, I will say that as long as the US economy continues to show growth of this nature, and especially as long as the Unemployment Rate doesn’t rise sharply, the Fed will have free rein to continue to raise rates going forward if inflation does not settle back to their 2% target.

One thing to consider regarding the central bank comments and guidance is that virtually every one of them has ended the strict forward guidance we had seen in the past. Rather, data dependence is the new watchword as none of them want to be caught out doing the wrong thing. Alas, the result is that, by definition, if they are looking at trailing data, they will always be doing the wrong thing. I expect that one of the key features of the past 40 years, ever reducing volatility in markets, is going to be a victim of the current framework. It is with this in mind that I suggest hedging financial exposures, whether FX, rates, or commodities, will be far more important to company balance sheets and bottom lines than they have been in the past.

Ok, let’s see how investors are behaving today as we head into the weekend. We’ve already discussed the Japanese market, but Chinese shares, both onshore and in HK, had a very strong day as there was more talk of official policy support for the property market there. Ultimately, it is very clear they are going to need to spend a lot more money to prevent an even larger calamity. European shares, though, are generally little changed this morning with investors preparing to take the month of August off, as usual there. Finally, US futures are higher this morning after what turned out to be a surprising fall in all three major indices yesterday. The overall positive data plus indication that the Fed may be done seemed to be the right conditions for further gains. But markets are perverse, that much we know. We shall see if US markets can hold onto these premarket gains. I would say that a lower close on the day would be quite a negative for the technicians.

In the bond market, yesterday saw US 10-year yields jump 15bps, its largest rise this year, although it is giving back about 4bps of that this morning. European sovereigns, though, are little changed this morning and have not been subject to the same volatility as the Treasury market given the far less exciting economic picture there. If the ECB is truly finished, my take is yields there could slide a little over time.

In the commodity markets, oil (-0.35%) is a touch lower this morning, but the uptrend continues. This certainly seems to be more about reduced supply than increased demand, although with the US data, the demand picture looks better. Interestingly, both gold (+0.6%) and copper (+1.0%) are higher this morning despite the dollar holding its own. Yesterday saw a sharp decline in both and I think there is a realization that was overdone.

Speaking of the dollar, it is modestly softer today after a strong gain yesterday. In the G10, GBP (+0.6%) is the leader followed by NOK (+0.5%) although AUD (-0.6%) and NZD (-0.3%) are taking the opposite tack. The pound seems to be benefitting from anticipation of next weeks’ BOE meeting where 25bps is a given, but the probability of a 50bp hike seems to be creeping up. Meanwhile, NOK is just following oil’s broad trend with WTI just below $80/bbl now. Meanwhile, Aussie seems to be suffering some malaise from the BOJ actions, at least that’s what people are saying although I’m not sure I understand the connection. Perhaps it is the idea that higher JPY yields will result in unwinding the large AUDJPY carry trades that are outstanding.

However, the emerging markets have seen a much wider dispersion of performance with much of the APAC bloc under pressure last night on the back of the strong dollar performance yesterday, while we are seeing strength in LATAM and EEMEA currencies this morning, which really looks an awful lot like simple trading activity with positions getting reduced after yesterday’s dollar performance.

In addition to the GDP data yesterday, we saw a lower-than-expected Initial Claims print at 221K while Durable Goods orders blew out on the high side at 4.7%! Again, lots to like about the US data right now. Today we see Personal Income (exp 0.5%) and Spending (0.4%) along with the Core PCE Deflator (0.2% M/M, 4.2% Y/Y) and finally Michigan Sentiment (72.6). based on yesterday’s results, I would expect the Income and Spending data to be strong along although PCE is probably finding a bottom here.

In the end, even if the Fed has stopped hiking, although with the economy still showing strength that is not a guaranty, I find it hard to believe that the ECB will go any further, and the tendency around the world will be to slow or stop tightening as well. I still like the dollar in the medium term.

Good luck and good weekend

Adf

A Bad Dream

The narrative’s gaining more steam With landings, so soft, the new theme In England today They’re trying to say Inflation was just a bad dream The problem is that on the ground, In Scotland and Wales and around, Is incomes keep lagging With purchases sagging Which pressures the Great British pound The biggest story of the morning has clearly been the UK inflation data which saw CPI fall back below 8.0% Y/Y for the first time in more than a year. Granted, 7.9% is not that far below 8% and certainly still miles above the BOE target, but the decline was substantially more than had been expected by the analyst community as well as the market. For instance, 10-year Gilt yields have tumbled -17.5bps and are now lower by 50bps since the peak two weeks’ ago and back to their lowest level since early June. 2-year Gilt yields have fallen even further, -25bps, so the market is really quite positive on this outcome. It should be no surprise that UK equity markets have rallied as well, with the FTSE 100 the leading gainer in Europe, up 1.5%, nor should it be a surprise that the pound has fallen sharply, -1.0%, as traders re-evaluate the idea about just how much the BOE is going to raise rates going forward. Prior to this release, the OIS market had been pricing in a terminal interest rate at 6.1%, implying at least 4 more rate hikes by the BOE. But this morning, traders have removed one of those hikes from the curve and the excitement over further potential declines is palpable. Now, the inflation news in Europe is not all rosy as the final release on the continent showed that core CPI turned out to be a tick higher at 5.5% in June, clearly an unwelcome result. And remember, it was just yesterday that we heard from Klaas Knot implying that while a hike next week is a given, nothing is certain past that. So, the question, currently, is will the ECB look through a revision to continue their more dovish stance? I guess we’ll find out next week. But here’s an interesting tidbit regarding Europe, and something you need to consider when it comes to both investments and market outcomes there, electricity demand is falling there amid deindustrialization on the continent. The IEA just issued their latest Electricity Market Report and the reading was not pleasant for Europe. Consider that in the US, the combination of reshoring and the impact of the (ironically named) Inflation Reduction Act, as well as the CHIPS Act, has driven a marked increase in industrialization in the US. Meanwhile, in Europe, the loss of their cheap energy from Russia combined with their climate goals has resulted in industry fleeing the continent. For everyone who is long-term bearish the dollar, you better be far more bearish the euro given this new reality. Remember, energy consumption is the mark of a growing and healthy economy. When it is declining, absent extraordinary productivity/efficiency gains, it bodes ill. If anything, the increasing reliance on less dense energy sources like wind and solar just reduces energy efficiency. Be wary. But, away from that news, things are a bit more confusing. For instance, virtually all European bourses are higher this morning, albeit not as much as the FTSE 100, but in Asia, while the Nikkei (+1.25%) had a good session, Chinese equities were under pressure. Yes, US markets yesterday continued their rally as earnings data has been able to beat the much-reduced estimates although futures this morning are essentially unchanged. But arguably, we can describe the equity picture as risk-on. The same cannot be said for the bond market though, where yields have fallen everywhere, again, just not as much as in the UK. Treasury yields are down another 2bps, and most European sovereigns are also seeing modest yield declines, not the typical risk-on behavior. In fact, given the Eurozone CPI release, it would not have been surprising to see yields climb a bit. As to the commodity space, oil is essentially unchanged on the day, but WTI is back above $75/bbl with Brent right at $80/bbl after several strong sessions. There has definitely been a renewed focus on the bullish supply story in oil as opposed to the recession discussion of late. At the same time, gold (-0.3%) which has rallied nicely during the past week, up nearly 2%, is holding the bulk of its gains. Alas, the base metals continue to lag, with both copper and aluminum softer on the day. Perhaps they didn’t get the bullish memo! Finally, the dollar is quite robust this morning, which is not what one might expect given the equity and bond moves. In fact, it is firmer vs. the entire G10, with the pound the laggard, as would be expected given the inflation data and falling UK rates. But as well, the yen (-0.8%) is under pressure along with AUD (-0.7%) and the whole lot. Regarding the yen, it has been rallying sharply of late, up more than 5% during July until yesterday. That seems to be on an increasing belief that the BOJ, which meets next Friday, is going to tweak its policy in a tighter fashion, whether that involves YCC or rates or QE. Now, these stories have not disappeared, I just think that we are seeing a bit of a breather for this move. Remember, the yen has been the funding currency of choice for every asset all year as the BOJ remains the only central bank that hasn’t tightened policy at all. This month appeared to be profit-taking ahead of potential BOJ activity, and last night appears to be a simple trading bounce. FWIW, I do not believe the BOJ is ready to adjust its policy yet as the big review has just begun. And as I have written before, it doesn’t appear that the rising inflation pressures in Japan have yet become a major political liability for PM Kishida, so there is only limited pressure to make a change. For now, I would rather be short than long the yen. Turning to the EMG bloc, only THB (+0.5%) is firmer this morning as the political machinations continue there in the wake of the recent election. In a nutshell, the winner of the election to replace the military junta is clearly not favored by the powers-that-be, and is being disqualified on a technicality, but another member of the coalition seems to be getting closer to taking the reins, with optimism building. But aside from that story, the dollar is firmer vs. the entire bloc as we are seeing a solid trading bounce in the greenback after several days/weeks of weakness. On the data front, yesterday’s Retail Sales data was disappointing, and the IP and Capacity Utilization data were awful. Obviously, that didn’t hurt equities which remain disconnected from any macro data at this point. This morning brings the Housing Starts (exp 1480K) and Building Permits (1500K) data, although if Retail Sales didn’t have an impact, it is hard to believe the housing data will. I remain uncomfortable with the equity market’s ongoing rally as I fail to see the underlying strength in the economy or earnings. Certainly, recent dollar weakness has helped goose the stock market a bit, but I would not be surprised to see things start to turn around in the near term, meaning the dollar rebounding after its recent sell-off and the equity market seeing some profit-taking. Good luck Adf

No Longer Clear

Inflation remains Far higher than desired Will Ueda-san blink?

Which one of these is not like the other?

|

Central Bank |

Policy Interest Rate |

Core CPI |

|

Federal Reserve |

5.25% |

5.3% |

|

ECB |

4.00% |

5.3% |

|

BOE |

5.00% |

7.1% |

|

Bank of Canada |

4.75% |

4.2% |

|

RBA |

4.10% |

6.8% (headline) |

|

BOJ |

-0.10% |

3.2% |

Source: Bloomberg

Japanese inflation readings were released overnight, and they showed no signs of declining. In fact, they were actually a tick higher than the median forecasts. However, there has been zero indication that the BOJ is set to respond to the highest inflation in decades. As everything economic is political, by its very nature, the reality seems to be that there is not yet any political price for PM Kishida to pay for rising inflation. Recall, as inflation started to pick up sharply in the wake of the pandemic reopenings, the universal central bank response was, inflation is transitory and it will subside soon. Politically, at that time, governments were keen to keep interest rates near (or below) zero as part of their belief that it would foster economic activity and recession was the big concern.

However, once it became so clear that even central banks understood this bout of inflation was not a transitory phenomenon, policy prescriptions changed rapidly leading to the very rapid rise in interest rates we have seen since early 2022. Politically, inflation was the lead story in every media outlet with governments around the world and their central banks being blamed, so they had to respond. (Whether their response has been effective is an entirely different story). Except in one place, Japan. As is abundantly clear from the table I constructed above, the BOJ has yet to alter their monetary policy stance despite core CPI remaining at extremely elevated levels far above the BOJ’s 2% target. In fact, prior to the recent spike, you have to go back to 1981 to see Japanese core CPI this high.

Apparently, though, inflation is not making headlines in Japan as it has been throughout the rest of the G7 and so the BOJ is perfectly happy to continue on their path of infinite QE and YCC. Remarkably, 10-year JGB yields fell further last night, now around 0.35%, as there is seemingly very little concern that a policy change is in the offing there. Certainly, there has been no indication from any BOJ commentary nor from Kishida’s government. As such, it can be no surprise that the yen continues to fall, declining 1% this week and more than 3% over the past month.

Interestingly, there has definitely been an uptick in the buzz from market talking heads about the need for the BOJ to abandon YCC and that a change is imminent. I have seen a number of analyses that foretell of the inevitable change and how the yen is likely to rise dramatically when it happens. FWIW, which may not be that much, I agree that when the BOJ does change policy, we are likely to see the yen rally sharply. The problem is, I see no indication that is going to happen anytime soon. Show me the headlines in the Asahi Shimbun or the Nikkei Shimbum (major Japanese newspapers) that are focused on inflation and I will change my view. But until it is a political problem, the BOJ is serving its current function of supplying the world’s liquidity with a correspondingly weaker yen as a result.

The messaging’s no longer clear Regarding the rest of the year While some at the Fed See more hikes ahead Some others feel ending is near

Once again yesterday we heard mixed messages from Fed speakers with some (Barkin) talking about evaluating their actions so far and waiting for more proof that further tightening was needed while others (Bowman, Waller) seeming pretty clear that more hikes are in the offing. Powell’s Senate testimony was largely the same as the House testimony on Wednesday with more of the questions focused on bank capital rather than monetary policy. Of course, the big question remains, are they done or not? Fed funds futures are still pricing a 72% chance of a hike in July and a terminal rate of 5.33%, so one more hike from current levels. But the arguments on both sides remain active. It appears to me that as long as the employment situation remains robust, they will continue to hike until inflation falls closer to their target. Yesterday’s Initial Claims data printed just a touch higher, 264K, and the trend certainly seems to be moving higher, but is not nearly at levels consistent with recession. The NFP report in two weeks will be critical but until then, we are likely to be whipsawed by commentary.

As to the overnight session, risk is very definitely on its heels this morning with equity markets in the red around the world, with all of Asia falling by -1.5% or more although European bourses have not suffered quite as much, -0.3% to -0.8%. US futures are also under pressure, down about -0.5% at this hour (8:00).

Bond markets, on the other hand, are performing their role as safe haven, with yields sharply lower this morning. Treasury yields, which had risen yesterday have given all that back and then some, down 6bps, while in Europe, sovereigns are down 12-13bps virtually across the board. The latter seems to be a response to the Flash PMI data which was released showing slowing activity across the continent, especially in France where both Manufacturing and Services fell below 50 and where German Manufacturing PMI tumbled to 41.0. If the Eurozone economy is truly performing so poorly, it is hard to believe that the ECB will continue on its current path much longer. One other rate story is the short-term GBP rates which are now pricing a terminal rate by the BOE at 6.13%, pricing another 5 rate hikes into the curve by the middle of next year.

However, on this risk off day, it is the dollar that is truly king of the world, rallying vs every one of its counterparts in both the G10 and EMG. NOK (-2.2%) is the G10 laggard on the back of general risk aversion as well as the fact that oil prices are tumbling again, down a further -1.25% this morning on the recession fears. But the weakness is pervasive with AUD (-1.0%) weak and the euro (-0.7%) giving up chunks of its recent gains in short order. Interestingly, the yen (-0.1%) is the best performer in the G10. The picture in the emerging markets is similar, with substantial losses across the board led by TRY (-1.3%) and ZAR (-1.1%). Of course, Turkey’s lira is destined to continue collapsing given the dysfunctional monetary policy there, but ZAR is feeling the pressure of declining metals prices, especially gold, which is down again this morning and now pressing $1900/oz. Meanwhile, China’s renminbi continues to slide, trading to new lows for this move with the dollar marching inexorably higher.

On the data front, today brings Flash PMI data (exp 48.5 Manufacturing, 54.0 Services, 53.5 Composite) and that’s it. Two more Fed speakers, Bullard and Mester, are due to speak and both have been leading hawks so we know what to expect. So, looking at the rest of the session, I suspect that the dollar will maintain most of its gains, but do not be surprised to see a little sell off as we head into the weekend and positions are reduced.

Good luck and good weekend

Adf

The Battle’s Been Won

‘Bout Jay and the FOMC The market has come to agree The battle’s been won And hiking is done So, buy stocks with verve and with glee In Europe, though, Madame Lagarde Is finding that things are still hard Inflation’s not tamed And she will be blamed If prices, she cannot retard Meanwhile on the world’s other side Where growth has begun to backslide The PBOC More cash will set free As Xi tries to hold back the tide

When looking at the market activity yesterday, it is easy to conclude that the market believes the Fed has instituted their last hike. This was evident in the equity market’s performance where all three major indices rallied more than 1% and it was evident in the FX market where the dollar was pummeled, falling by 1% or more against 7 of its G10 counterparts as well as about half the EMG bloc. In addition, Treasury yields fell sharply as the idea that the Fed is going to continue hiking, as implied by Chairman Powell in his comments on Wednesday, seems to have faded from memory.

But that’s not all! While key markets are beginning to discount any further Fed activity, the ECB not only raised their rate structure by 25bps as expected, but Madame Lagarde essentially promised another hike in July and this morning the ECB’s hawks are circling and hinting that a September rate hike is quite possible as well.

Now, we already know that the Fed’s dot plot is calling for 2 more rate hikes this year, but the Fed funds futures market is not in accord with that view. Rather, it is pricing a 70% probability of a July hike as the final move. But, will they hike again? Clearly, between now and the end of July we will all have seen a great deal more data, including both an NFP and CPI report, and that will have a major impact on the Fed. But after yesterday’s US data dump, which showed Retail Sales holding up far better than expected while both the Import and Export Price Indices showed price declines, there has been a significant increase in the chatter of the Fed pulling off a soft landing after all. And, if the landing is soft, do they need to hike more?

Although the manufacturing side of the economy remains lackluster, Services have been killing it. There is one other reason to believe the Fed will remain on hold as well, and that is the employment situation. While we have seen a much hotter than forecast NFP print basically each month for the past year, we are starting to see Initial Claims data tick higher. Yesterday’s 262K was both higher than expected and the highest print since October 2021 when claims were tumbling during the post-pandemic recovery. More ominously, the 4-week and 13-week moving averages (analyzed to seek a trend and remove the weekly choppiness) are both clearly trending higher. If that number continues to rise, the Fed’s confidence in the economic recovery continuing is likely to be impaired. In fact, I think this is the feature that is most likely to cause the Fed to stop hiking.

If we pivot to Asia for a moment, we see a completely different set of concerns in both China and Japan. Starting with China, after cutting their lending rates earlier this week, the PBOC is still struggling to figure out how to support what is a clearly softening economy. Although there has been much lip service paid to the fact that China will no longer prop up the property market and investment and is instead seeking to generate more domestic consumption, the fact that the youth unemployment rate is at a record 20.8% and that the only playbook the Chinese really understand is infrastructure spending and leveraged property speculation, they are falling back into that trap. Rumors abound that the government is going to put forth a CNY1 trillion (~$140B) spending package and that the PBOC is going to ease restrictions on property lending, removing the ban on second home purchases in small cities. Remember, property speculation was a critical part of China’s rapid growth as people there have little confidence in a social safety net and were using those second homes as an investment to secure their nest egg. Alas, with China’s population shrinking, that may no longer be an interesting investment for the middle class. So, while China’s problems are different, they are no less severe than those in the West.

Uncertainty is “Extremely high” over both Wages and prices So, Ueda-san Will keep liquidity flows Like flooding rivers

As to Japan, I’m old enough to remember when there was a growing belief that once Kuroda-san stepped down as BOJ head, his replacement would have free rein to tighten policy. Boy, were we ever wrong about that. After last night, while there was no policy adjustment as expected, Ueda-san’s comments can only be construed as strongly dovish and the market got the message. JGB yields slid a few basis points and are back below 0.40% while the yen is the only currency that is underperforming the dollar. Meanwhile, the Nikkei (+0.65%) continues its recent strong performance as the second best major index after only the NASDAQ.

The one thing that we know is that things do not seem to be evolving as per much of the consensus from earlier this year. While there is still a long way to go before this cycle ends, and I still expect a more significant economic slowdown globally, the possibility that Chairman Powell pulls off a soft landing cannot be dismissed. And as I saw on Twitter yesterday, if he does so, he will be hailed as the greatest Fed chair ever, even more so than Paul Volcker. Alas, I fear things will not work out that way. Remember that monetary policy works with long and variable lags, and I would contend that the economy is likely just beginning to feel the true impacts of tighter policy. Now, this may only happen in the manufacturing sector, where the cost of capital is such a critical input, but history has shown if that sector stumbles, it drags the economy down with it. Remember that so much of the service economy exists to service manufacturing, so the two are quite intertwined.

Remember, too, there are potential exogenous shocks, both positive and negative, that can have a big impact. What if the Ukraine war ended? What if China invaded Taiwan? What if there was an escalation of fighting in the Middle East with a dramatic reduction in oil production? All I am pointing out is that myopically focusing on just the economic data is not sufficient for a risk manager. Sh*t happens and it can matter a lot.

Ok, as to today, we already know that risk is on. The data coming out this morning is Michigan Sentiment (exp 60.0) and of the three Fed speakers, two have already commented with Governor Waller not talking economics or policy, but rather bank regulation and Bullard was more theoretical than policy focused, so really there has been nothing new there either. In a little while, Richmond’s Barkin will discuss inflation, so that could be interesting. But for right now, the market has made up its mind. Everything is right as rain so add risk. That means the dollar is likely to remain under pressure with a test of its lows (EUR 1.11, DXY 102) coming soon to a screen near you.

Heading into a bank holiday weekend, I expect positions to be lightened but the recent dollar weakening trend to remain intact.

Good luck and good weekend

Adf