The word for today is inflation

With many convinced its cessation

Is just round the bend

So, growth will ascend

Alongside Chair Jay’s coronation

But what if inflation don’t slow?

And rather, continues to grow

Can bonds stand the pain?

Will stocks feel the strain?

Or will we go on with the show?

The first thing to mention is the Bitcoin ETF was approved by the SEC last evening and the price…is basically unchanged. As I mentioned yesterday, it seems quite ironic that Bitcoin, a shining symbol of freedom from the government and regulation is now tightly ensconced in government and regulation. Do not be surprised if it becomes a much less interesting asset having lost one of the key things that makes it different. Just a thought.

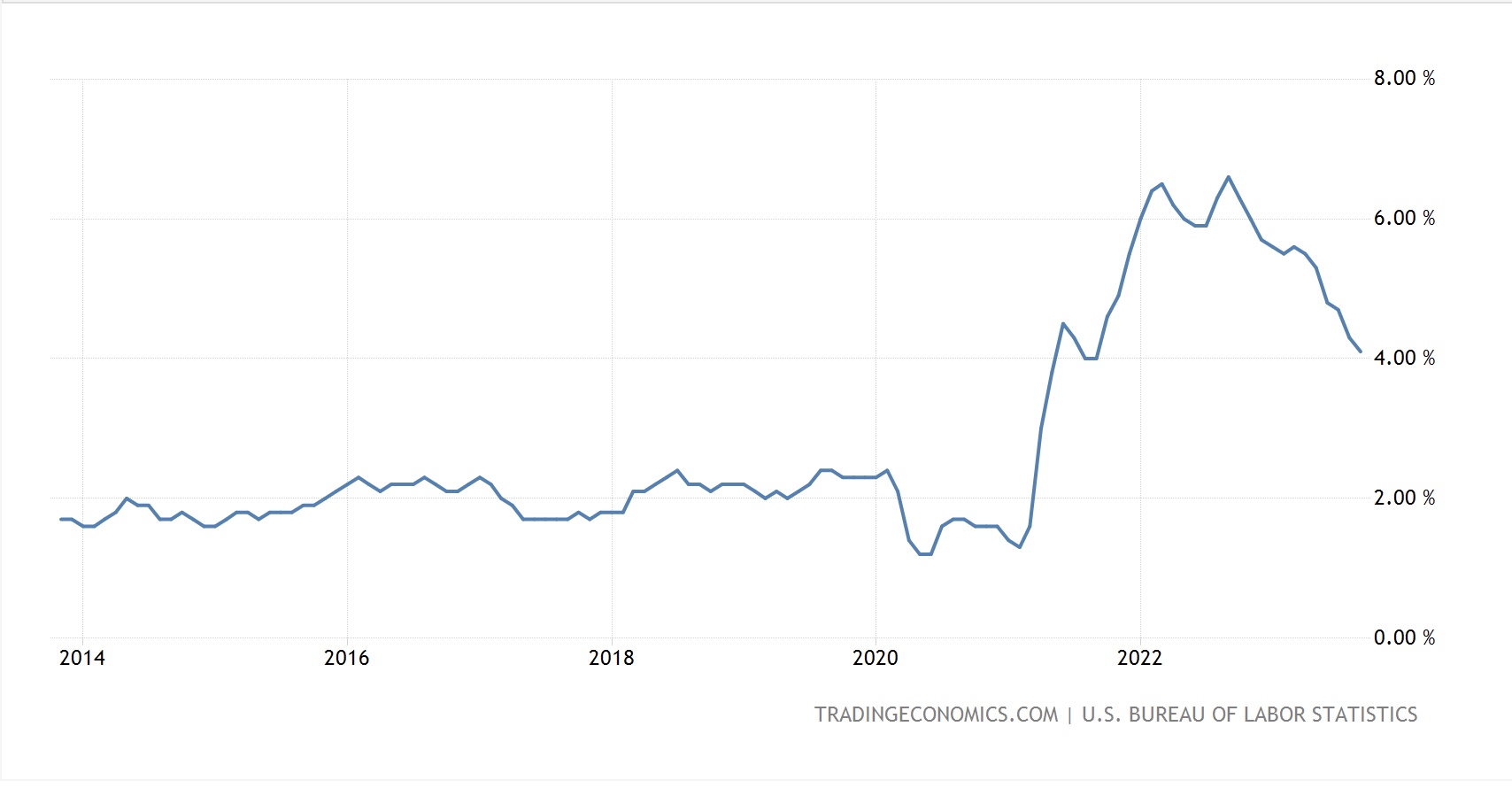

Ok, on to the more important stuff, the economy and today’s CPI report. Current consensus forecasts are as follows: CPI 0.2% M/M (3.2% Y/Y) and -ex food & energy 0.3% M/M (3.8

% Y/Y). If realized, these represent a 0.1% rise in the headline and 0.2% decline in the core readings from last month on an annual basis. Now, in the broad scheme of things, and more importantly, in our day-to-day lives, that 0.1% or 0.2% has absolutely no meaning or impact. However, the importance allotted to that 0.1% is remarkable. Entire narratives will be spun about how the Fed has been amazing in their ability to achieve a soft landing, or the Fed is a group of 17 incompetent fools based on an estimated data point that is often revised and does not clearly measure what the words in its name describe. As such, let’s simply focus on the market reaction function rather than the meaning of the data.

Heading into the release, my take is that given the recent run of softer than forecast inflation readings around the world, whatever the economists and analysts have forecast, the market is leaning toward a soft print. The fact that oil prices fell about -6% during the month of December, although gasoline prices were nearly unchanged, has tongues wagging. As well, discussions about slowing growth in China and their negative PPI as a driver of deflation is another key element of the narrative.

Counter to this is the fact that the Fed refuses to take their victory lap. Yesterday, John Williams explained, “My base case is that the current restrictive stance of monetary policy will continue to restore balance and bring inflation back to our 2% longer-run goal. As inflation comes down over time, my expectation is interest rates will also come down over time.” In other words, things are going well, but we have not reached the finish line. This certainly didn’t sound like someone who was ready to cut interest rates in two months’ time although the market continues to price a better than 2/3 probability that the Fed will do just that. Now, if we take him at his word and inflation fell another 0.6% or more by March, maybe that would be enough to get them into a cutting mood. But I just don’t see that.

One of the things that is often either overlooked or not well understood is the fact that things move REALLY slowly in the economy, especially when it comes to measured moves of economic data points. Of course, the exception that proves this rule was the Covid recession, but in order to get data to move at the same speed as markets required virtually every government in the world to shut their economies down at the point of a gun! My take is that will not happen again in our lifetimes, regardless of the threat. As such, we need to recognize that, to use a well-worn metaphor, the economy is an aircraft carrier and turning it takes time.

When applying this concept to inflation, and prices more generally, especially wages, they don’t move that quickly. In fact, they move quite slowly. People get annual raises, not weekly or monthly ones. While gasoline prices move up and down on a daily basis, the same is not true for menu prices, items in the supermarket or rent. Real-time price adjustments are a flaw feature of financial markets, not of real life. While many will point to the fact that the shelter portion of CPI (and PCE) is a smoothed average of the past twelve months and so not indicative of today’s situation, I would counter that most of the people who pay rent haven’t moved in the past twelve months and their rent remains the same. It is certainly not declining, and I am still looking for that first story of the landlord who saw the CPI data slipping and cut his tenants rent to keep in line!

The point is that expectations of a sharp move in a slow-moving data series are misplaced. Much has been made of the fact that if you annualized the last 3 months or 6 months of CPI monthly data, CPI is already below the Fed’s target of 2.0% and so they should be cutting. Personally, I find that ridiculous. But more importantly, the Fed, as evidenced by Williams’ comments above, has no truck with that idea. Add to this the fact that growth seems to be holding in at trend or better, despite interest rates being “too high” according to the cutting advocates, and it becomes that much harder to believe the Fed is ready to go.

Net, regardless of today’s number, the Fed is not going to change its mind soon. Markets, however, are a different story. If the readings are soft, look for a big rally in both stocks and bonds, for the dollar to fall, and for commodity prices to rally nicely. At least initially. And the converse should be true as well, a hot number will see red numbers in the stock market, higher yields, a stronger dollar and commodities come under pressure.

Leading up to the number, here’s what we see. After a nice day in the US yesterday, Asian markets were all in the green led by the Nikkei continuing its rip higher, but this time dragging Chinese shares along for the ride. In Europe, it appears things are more circumspect as they await the CPI data with most markets +/- 0.2% or less on the day while US futures are currently (7:30) modestly in the green.

Bond yields are definitely in the low inflation reading camp as Treasury yields have fallen 4bps this morning and we are seeing similar movement all across Europe. The one exception to this story is Japan, where JGB yields edged higher by 2bps despite a couple of soft Leading Economic Index numbers. However, since the peak, just below 1% in early November, this trend remains clearly lower for yields.

Apparently, the hijacking of an oil tanker in the Persian Gulf has been seen as an escalation of the situation there and oil prices are higher by nearly 2% this morning, although that simply takes the weekly change back to flat. Gold prices are rallying, 0.5%, and not surprisingly in this environment, so are base metals prices with both copper and aluminum higher by 0.6% this morning.

Finally, on the dollar front, it is lower after a small decline yesterday. This is of a piece with the inflation expectation story and the idea that the Fed is preparing to cut rates, boost stocks and undermine the dollar. Even the yen has rallied a bit today, so no currencies are really bucking the trend of a weak dollar, whether G10 or EMG.

Aside from the CPI data, as it’s Thursday we also see Initial (exp 210K) and Continuing (1871K) claims and then early this afternoon we hear from Tom Barkin again. At this stage, the Fed seems to be of a mind that things are going well, and they are not about to rock the boat in either direction. Absent a huge surprise in the data this morning, I think this slow grind toward risk on continues.

Good luck

Adf