The story of note for today

Is how will the BLS play

Employment revisions

And then what decisions

Will Powell be likely to weigh?

For now, markets still seem assured

That rate cuts will soon be secured

The doves still want fifty

But most are more thrifty

With twenty-five likely endured

But what if Chair Powell decides

Inflation, just like ocean tides

Both waxes and wanes

And though they’ve made gains

No rate cuts, to Fed funds, provides

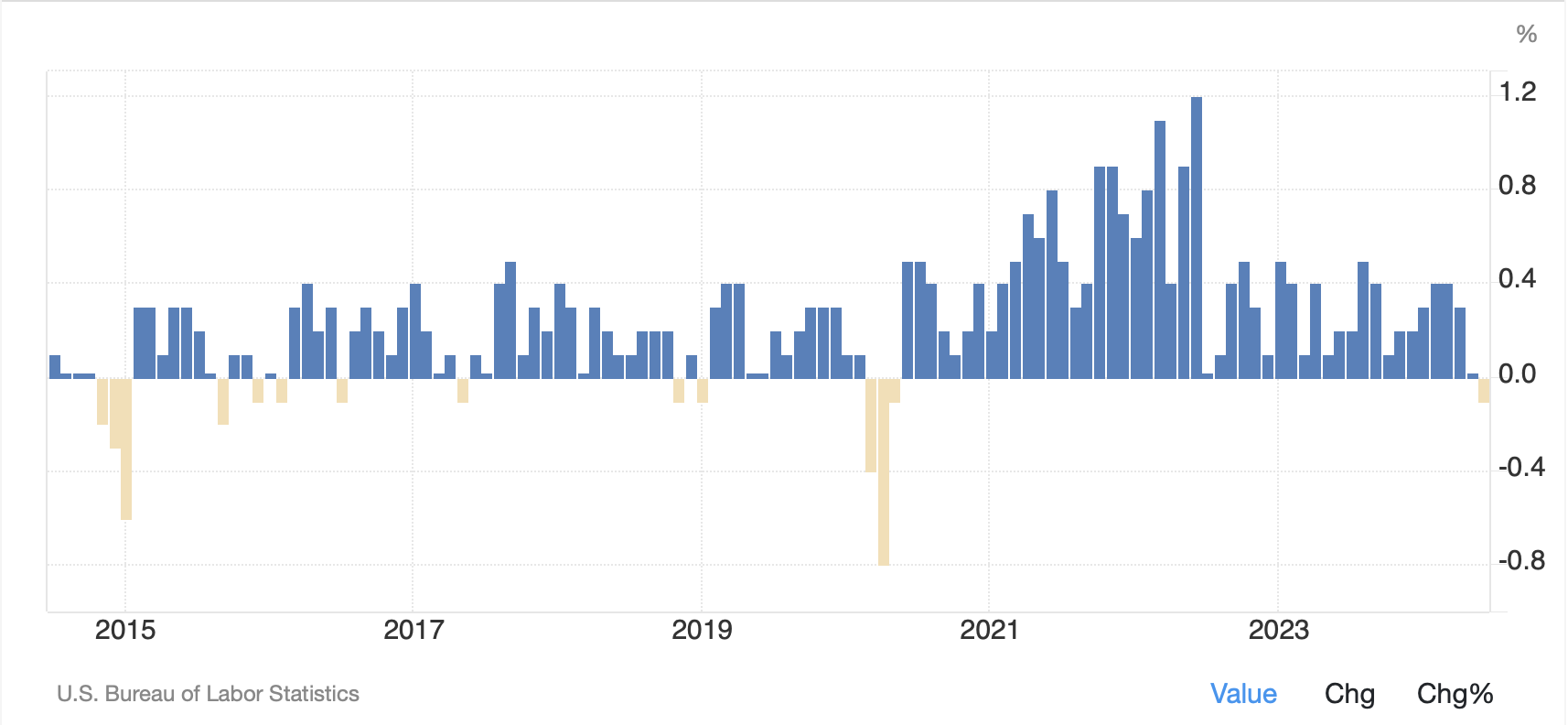

So, the big story today, which I briefly discussed on Monday, is that the BLS is going to make benchmark revisions to their NFP data for the year through March 2024. These revisions come from a closer analysis of the Quarterly Census on Employment and Wages (QCEW) data, which is the most comprehensive data set on jobs available. Remember, for their monthly reports, the BLS uses a model that incorporates samples of data from respondent companies, and then includes their own adjustments based on the birth-death model of new businesses and how many jobs they create. But the QCEW data doesn’t model things, it counts all the data from states regarding unemployment insurance and reports required to be filed by companies regarding quarterly contributions. It is the gold standard.

Naturally, when the QCEW is released (the most recent was released in June), the analyst community goes through everything and makes their own estimates as to the changes that will occur. Prior to any revision, the BLS data show that the economy added 2.9 million jobs in the 12 months from April 2023 through March 2024. But analyst estimates range from a reduction in that number ranging from 300K to as much as 1 million fewer jobs.

Given the increased importance the Fed has placed on the employment side of their mandate lately, and given that one of the reasons, if not the key reason, Powell has been willing to leave rates at current high levels is the employment situation has remained robust, if he and his colleagues were to suddenly find out that there were one million less employed people around, that would likely have a serious impact on their views as to where rates should be.

Based on the stories that I have seen on this topic over the past several days, as well as the positioning that is being revealed by the Commitment of Traders’ reports showing massive long positions in both treasury bond futures and SOFR call options, both of which are real money expressions of expectations of lower interest rates coming soon, it strikes me that the pain trade is the opposite. In other words, what if this revision is much smaller than the largest estimates, maybe 100K or something. Suddenly, the idea that the Fed is going to be pressured into cutting rates despite the fact that inflation, though lower, remains well above their target, is not quite as certain.

The thing is, based on what I keep reading and hearing, it strikes me that the market is set up for a bond sell-off and higher yields today. Either, the number is large, about 1 million jobs removed, and then we will see profit taking on the outstanding positions, or the number is small, and the entire story needs to be rewritten regarding the timing of the first rate cut, which means that positions need to be abandoned. I’m not sure what the goldilocks number needs to be to have traders maintain their positions ahead of Friday’s Powell speech, but given that is a wild card as well, I think that is the least likely outcome, no change in positions.

Elsewhere, the only other noteworthy thing was a story about a BOJ staff paper that discussed the idea that inflation in Japan is still structural and that higher rates are still appropriate, but that is a staff paper, and not necessarily Ueda-san’s view. The BOJ next meets on September 20, two days after the FOMC, so Ueda-san will have lots more new information to decide just how hawkish he wants to be. Recall, the dramatic market collapse in Japan at the beginning of the month, while completely reversed now, forced their hand to back off their hawkishness. Perhaps, the second time, if they remain hawkish, they will be able to withstand that type of movement.

So, as we all await this BLS revision, which comes at 10:00 this morning, here is how things behaved overnight. After the first down day in the US in 9 sessions, Japanese (-0.3%) and Chinese (-0.3%) markets were also soft although the rest of the region was mixed with some gainers (India, Indonesia, Australia) and some laggards (Hong Kong, Taiwan, New Zealand). In Europe, though, equity markets are modestly firmer this morning, somewhere between 0.25 and 0.5%, although there has been a lack of new information seemingly to drive things. As to the US, futures at this hour (7:30) are edging higher by about 0.1%.

In the bond market, Treasury yields have edged up 1bp this morning, although they have been trending down for the past week in anticipation of this BLS employment adjustment. European sovereign yields are essentially unchanged this morning while JGB yields dipped 1bp. The story there remains that 10-year JGBs are yielding well less than 1.00%, the perceived key level at which more Japanese funds flow home. I think we will need to see a much more hawkish BOJ to get that trade going.

In the commodity markets, oil (0.0%) has stopped falling for the time being, but remains under pressure overall, down more than 6.6% in the past month. Yesterday’s API data (the private sector version of the EIA data to be released later this morning) showed a small build of inventory as opposed to the continued draws that we have seen lately and that were expected. However, a look at the oil chart tells me that we are much closer to the bottom of its trading range for the past 3 years, than the top, and seem likely to rebound a bit. Gold (-0.15%) is consolidating its recent gains and remains above that big round $2500/oz level but both silver (+0.5%) and copper (+0.5%) are rallying today. I keep reading stories about how the physical shortages in both those markets, due to increased production of solar panels and batteries, is going to become the key driver going forward. While I have believed that story, it is always hard to ascribe a given day’s movement to something like that absent a major new piece of information, and I haven’t seen that piece of the puzzle.

Finally, the dollar is bouncing slightly this morning, although that is after a pretty straight-line decline for the past two months. Given the hype about Fed rate cuts, especially adding in this new focus on the BLS job data adjustment, it is easy to see why traders are looking for much lower US rates and therefore selling the dollar. But remember, in the big scheme of things, at least based on the Dollar Index, the dollar is pretty much at its long-run average, neither weak nor strong. I will say that if the Fed does enter a serious rate cutting cycle, the dollar is likely to weaken quite a bit more, perhaps with the euro testing 1.15 – 1.20 before it ends. However, remember, if the Fed starts cutting aggressively, so too will the ECB, BOE and BOC, so any weakness will be somewhat limited. As to today’s price action, the dollar’s strength is universal, but pretty modest overall with the biggest mover JPY (-0.5%) although obviously there are other things ongoing there.

Aside from that employment report revision, there is no other data to be released and there are no Fed speakers scheduled today. Today will be driven by that revision. The larger the revision, the more likely we see the dollar decline, although the initial reaction on interest rates may be opposite on profit taking.

Good luck

Adf