Said Jay, we are not very far

From when we can all wave au revoir

To higher for longer

With confidence, stronger,

Inflation will reach our lodestar

“We’re waiting to become more confident that inflation is moving sustainably at 2%. When we do get that confidence — and we’re not far from it — it’ll be appropriate to begin to dial back the level of restriction.” So said Chairman Powell yesterday in front of the Senate Banking Committee in response to some of the questions he received. Nuff said! Regardless of the fact that there has been limited indication of slowing economic activity (although this morning’s payroll report will be critical), it seems quite clear that Powell is under a great deal of pressure to reduce rates. One must assume this pressure comes from the White House as in last night’s SOTU speech, President Biden even mentioned that mortgage rates were too high, and he was going to push them down. Clearly, the only tool that Biden has is to lean on Powell to cut rates.

But despite what had appeared to be a concerted effort by every Fed speaker to push back against the proximity of the first interest rate cut for this cycle, it appears that Powell is blinking. Interestingly, while the Fed funds futures markets didn’t really adjust very much, we did see the 2yr Treasury yield fall back 5bps and this morning it sits slightly below 4.50%, its first time back to this level since the surprising CPI print last month. Of course, equity markets love the message, and we continue to see new highs on a daily basis. But we are also continuing to see new highs in the anti-fiat monies, gold and bitcoin. The world is not without risk.

An angry old fella named Joe

Last night tried explaining our woe

Was not his, to blame

Though he wouldn’t name

The culprit, throughout the whole show

While I try to leave politics out of this missive, the status of the SOTU is such that I don’t believe it can be completely ignored. My takeaway from last night’s speech was that President Biden, in an attempt to show vigor, came across as the angry old man shaking his fist and yelling at the clouds. He had a laundry list of things he claims to want to accomplish, all of which will cost trillions of dollars, and none of which are likely to be enacted before the election. Many pundits pointed out this seemed more like a campaign speech than a SOTU and I think there is merit in that view. In the end, while we understand where the pressure on Powell is coming from, I don’t believe this is going to change anything, certainly not from a market perspective.

And finally, it’s time to turn

To data for which we all yearn

The Payroll report

Which, if it falls short

Will likely give hawks great heartburn

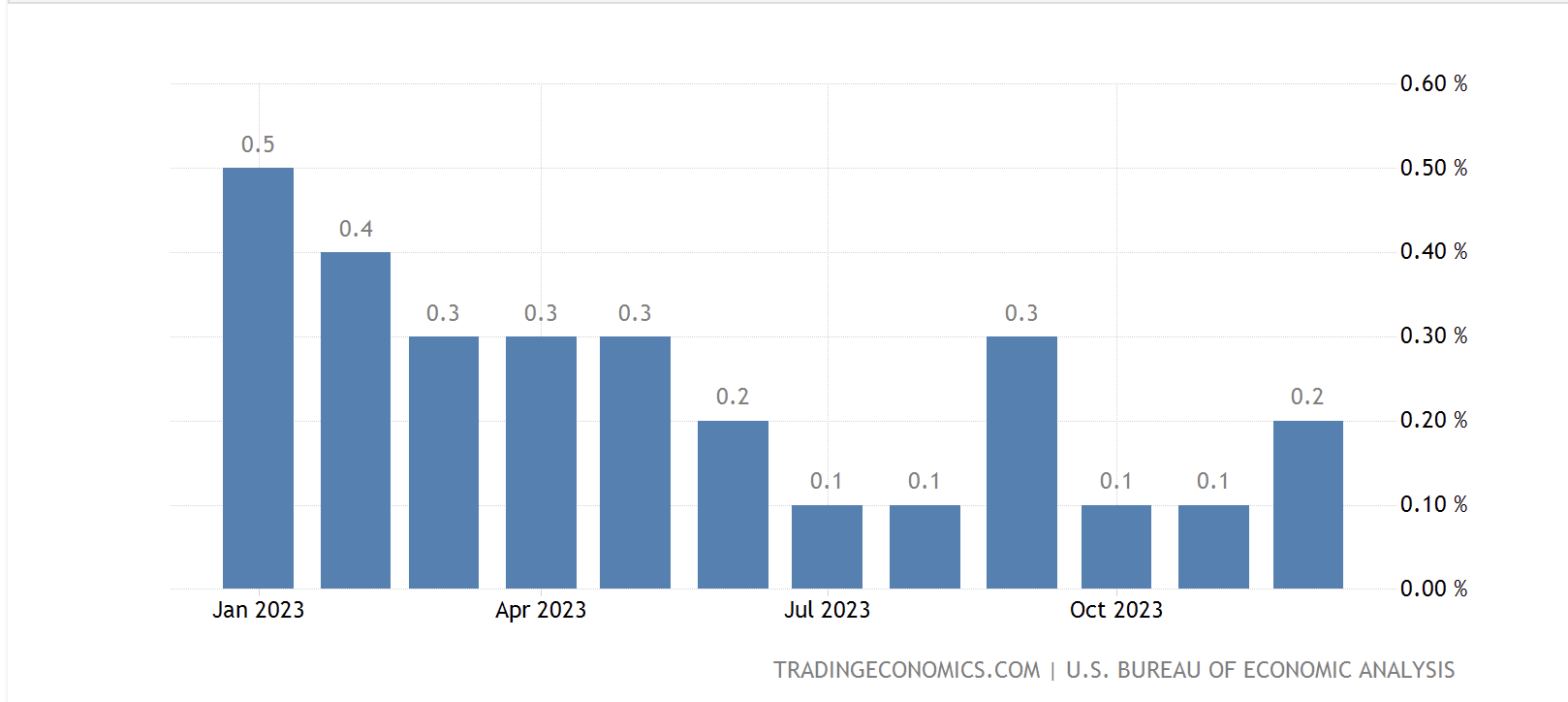

Looking ahead, this morning brings the monthly payroll report. Current median expectations are as follows:

| Nonfarm Payrolls | 200K |

| Private Payrolls | 160K |

| Manufacturing Payrolls | 10K |

| Unemployment Rate | 3.7% |

| Average Hourly Earnings | 0.3% (4.4% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 62.6% |

Source: tradingeconomics.com

Recall, last month’s number was massively higher than anticipated at 353K and had higher revisions as well. The revisions were almost more surprising than the headline number as the trend for the entire previous year had been for revisions to be to softer data. There will certainly be revisions to the January data as well, so there is a great deal of uncertainty. My sense is, though, that the market really wants to see a softer number with downward revisions as that will work toward cementing the case for the Fed to cut rates even sooner. Sub 150K and look for a bond and stock rally. Above 250K and bonds will sell off, although stocks have a life of their own. At least that’s one man’s view.

Ok, let’s look at how things played out overnight ahead of this key data. Asian markets followed the US rally with green across the screen. The Hang Seng, which is seen as the tech proxy in Asia, rallied most, 0.75%. Europe, on the other hand, is having a tougher day with most markets slightly softer although the FTSE 100 is down -0.5%, the clear laggard this morning. Apparently, Madame Lagarde’s comments did nothing to support the hopes that rate cuts were coming soon as ostensibly, rate cuts were not even discussed in the meeting and all signs point to June as the first time by which they will have confidence in the inflation story, if it is to come. Meanwhile, US futures are pointing a bit lower, -0.3%, at this hour (8:00).

In the bond markets, Treasuries have edged lower another 1bp this morning and we are seeing yields across the board in Europe decline by between 2bps and 4bps. I can’t tell if that is confidence in the ECB (doubtful) or belief that the ongoing decline in economic activity (Eurozone GDP in Q4 was confirmed at 0.0% Q/Q and 0.1% Y/Y) has simply encouraged investors that rates are going to fall with no chance of a backup. Meanwhile, JGB yields were unchanged overnight despite the ongoing excitement(?) that the BOJ may raise rates a week from Monday.

Oil prices have retreated a bit (-0.6%) but are essentially range trading and have been for the past month. However, the star of the commodity space continues to be the barbarous relic, with gold rallying another 0.3% this morning to yet another new all-time high. As to the base metals, copper is unchanged this morning, but has been on a roll lately while aluminum is higher by 0.65%. Metals investors are gaining confidence that not only is there going to be no landing in the US, but that China is going to stimulate more.

Finally, the dollar remains under pressure overall as yields continue to decline. While the euro is a touch softer this morning, virtually every other G10 currency is firmer with JPY (+0.55%) leading the way. Remember, too, that with FY end approaching for Japan, we will begin to see Japanese corporates repatriating funds which typically sees further yen strength. Combine that seasonal activity with the relatively new BOJ hawkishness/Fed dovishness combination and the yen could rally a lot more. After all, it has fallen a lot in the past two years! But, while the G10 currencies are generally having a good day, the picture in the EMG bloc is far more mixed with BRL (-0.6%) the laggard after total credit in Brazil was shown to have fallen in January for the first time since the pandemic. On the flipside, CLP (+1.0%) is rallying after a higher-than-expected CPI report (4.5%) has traders looking for tighter monetary policy than previously anticipated.

Aside from the payroll report, there is no other data to be released and there are no Fed speakers on the calendar. Yesterday we did hear Cleveland Fed president Mester sound more hawkish, becoming the third FOMC member to discuss only 2 cuts this year, and I maintain that when the dot plot comes out, that could be the median view. But for now, markets and investors remain euphoric about the apparent Powell dovishness, so that will be the driver absent a huge NFP this morning. For the dollar, that will be bad news.

Good luck and good weekend

Adf