In April, it starts with the Fools

But two days thereafter the rules

For importing cars

To where Stars and Bars

Fly will change with tariffs as tools

For Europe, the pain will be keen

At least that’s what most have foreseen

And poor crypto bros

Will find their Lambos

May soon cost a price quite obscene

While the political set continues to harp on the “Signal” story, markets really don’t care about political infighting between the parties. Rather, their focus is keenly attuned to President Trump’s confirmation that starting on April 3rd, there will be a 25% tariff imposed on all imported autos from everywhere in the world. This is particularly difficult for European auto manufacturers as they produce a far smaller proportion (VW 21%, BMW 36%, Mercedes 41%) of their vehicles in the US than do the Japanese (Honda 73%, Toyota 50%, Nissan 52%), although the Koreans will be impacted as well (Hyundai/Kia 33%). Ironically, according to Grok, where I got all this information, GM only produces about 54% of their vehicles sold in the US, in the US, with the rest coming from Canada and Mexico. As an aside, Tesla produces all their vehicles in the US.

Particularly hard hit are the specialty manufacturers like Porsche, Ferrari and Lamborghini, which produce none of their vehicles in the US. Of course, given the price points of these vehicles, my sense is it may not really hurt their sales as if you are spending $250k on a car, you can likely afford to spend $312.5k as well. In fact, in a funny way, these tariffs may enhance the Veblen effect where people will brag about paying the higher price as it puts it out of reach of more people.

Nonetheless, the action merely confirms that President Trump is very serious with respect to changing the world’s trading model. I saw something interesting this morning in that Paul Krugman, who made his name, and won his Nobel Prize, based on work regarding international trade and was the prototypical free trader, has adjusted his views after recognizing that nations need to maintain some manufacturing capabilities for security reasons. I assure you, if Krugman, who has been a vocal liberal critic of every Republican idea for the past twenty years, agrees with this policy, it will be very difficult for anyone to reject it.

In a perfect world (globo economicus?) free trade accrues benefits to all. But we don’t live in that world and national priorities often supersede these issues. The pandemic highlighted the weaknesses that the US had developed in its ability to manufacture key items necessary for its continued economic and defense survival. And remember this, for the world at large, their idea of free trade is they should be able to sell whatever they grow/manufacture into the US with no barriers, but US manufacturers need to be subject to barriers in order to protect other nations’ favored industries and companies. That world is now history with new rules being written every day and most of them by Donald Trump.

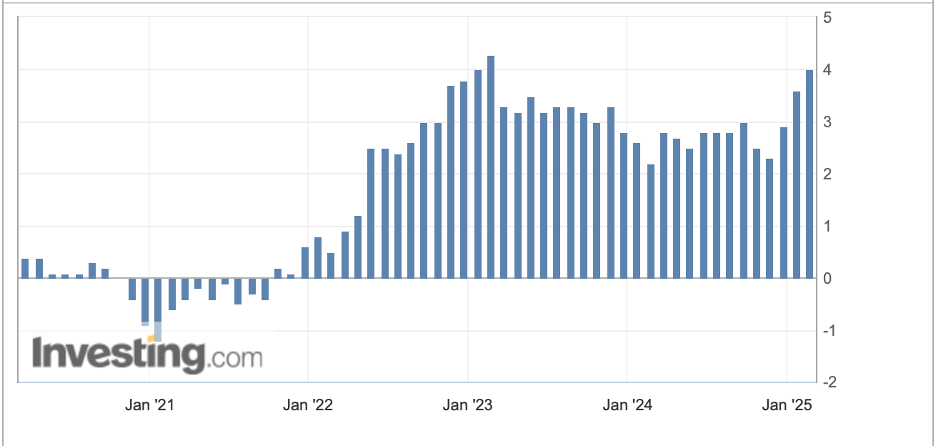

So how have markets responded to this tariff confirmation? Not terribly well. Yesterday’s US equity selloff was pretty significant led by the NASDAQ’s -2.0% decline. In Asia, the Nikkei (-0.6%) also sold off as did Korea (-1.4%), Taiwan (-1.4%) and Australia (-0.4%). On the other hand, both China (+0.3%) and Hong Kong (+0.4%) managed a better session, seemingly as a rebound against declines in the previous session with the only news showing that Chinese industrial profits fell by -0.3% compared to a Y/Y decline of -3.3% in December. However, a quick look at a chart of this data for the past five years tells me they need to seasonally adjust it in order to get something meaningful, so I don’t think it really impacted markets.

Source: tradingeconomics.com

As to European shares, it should be no surprise that the tariff announcements have negatively impacted shares there with declines of between -0.2% (Spain) and -0.7% (Germany). US futures though, at this hour (7:00) are little changed on the session.

In the bond market, Treasury yields continue to creep higher, up another 3bps this morning and back to levels last seen a month ago. This cannot be helping Secretary Bessent’s blood pressure, although he very clearly has a plan in mind. There is much stagflation discussion in the markets by the punditry as they assume tariffs will slow growth and raise prices and bonds are not the favored investment in that scenario. Meanwhile, European sovereign yields are all sliding this morning, largely down -2bps, amid growth concerns on the back of the tariff announcements. The one exception here is UK Gilts (+7bps) as the UK Budget announcement indicated slightly more gilt issuance would be necessary to fund the government’s spending plans. However, there is a growing concern over the financial management of the Starmer government overall.

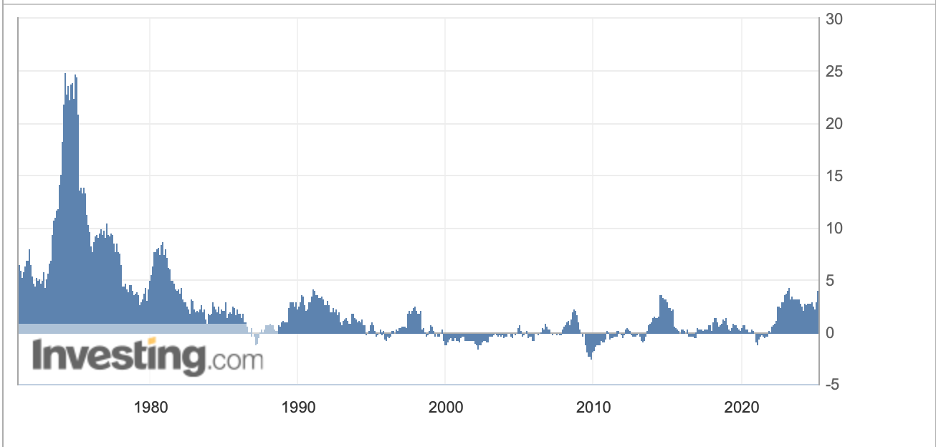

In the commodity markets, oil (-0.35%) is slipping from yesterday’s closing levels and continues to flirt with the $70/bbl level but has not been able to breech it since late February. Apparently, there are questions as to whether the auto tariffs will reduce demand. Personally, I would think it is the opposite as more older, less fuel efficient cars will remain on the road here. As to gold (+1.0%) after a several day pause, it appears that it is resuming its very strong trend higher. You know what we haven’t heard about lately? Ft Knox auditing. I wonder if that is getting arranged or is now so old a story nobody cares. Silver (+1.0%) is along for the ride although copper (-0.4%) is taking a breather after a breathtaking run to new all-time highs this year. Look at the slope of the copper chart and you can see why it is pausing, at the very least.

Source: tradingeconomics.com’

Finally, the dollar is broadly softer this morning, with the euro, pound and Aussie all gaining on the order of 0.3%. As well, NOK (+0.3%) is firmer after the Norgesbank surprised some and left rates on hold with a relatively hawkish message about the future. But there is weakness vs. the greenback around with JPY (-0.3%), MXN (-0.3%) and INR (-0.2%) all leaning the other way. Another tariff related story is that India is planning to cut its tariffs in half for the US, a very clear victory for President Trump.

On the data front, this morning brings the weekly Initial (exp 225K) and Continuing (1890K) Claims data as well as the third and final look at Q4 GDP (2.3%). Part of the GDP data is Real Final Sales (4.2%) which is a key indicator for what happens here given consumption represents ~70% of the economy. We do hear from Richmond Fed president Barkin this afternoon, but right now, Fed speakers are speaking into the void.

International statecraft continues to be the underlying thesis of global relations and President Trump’s goals of reshoring significant amounts of manufacturing and jobs along with it is still the primary driver. There has been far less talk of the Mar-a-Lago Accord as that seems to be losing its luster. If countries adjust their trade policies, Trump will continue in this direction. While that may include short-term economic weakness and some pain, for both the economy and the stock markets, there is no indication, yet, he is anywhere near blinking. One thing to keep in mind is that an overvalued stock market can correct by prices falling sharply, but also by prices stagnating for a long time while earnings catch up and multiples compress. We may very well be looking at the latter scenario, so no large gains nor losses, just choppy markets going forward. As to the dollar, lower still seems the direction of travel overall from current levels, but probably in a very gradual manner.

Good luck

Adf