The world is no longer the same

Since Trump put Zelenskiy to shame

Now Europe insists

They’re balling their fists

And this time it isn’t a game

But markets just don’t seem to care

That, anymore, war’s in the air

Instead, what’s decisive

Is that the new price of

All cryptos has answered their prayer

Last Friday’s remarkable live TV meeting between Presidents Trump and Zelenskiy in the Oval Office has rocked the entire world, or certainly the entire Western World. The unwillingness of Zelenskiy to consider a ceasefire and Trump’s dismissal of him from the White House, even before lunch, has clearly changed a lot of views of how things are going to evolve from here.

The most noteworthy result is the sudden realization by the EU and NATO that the US is committed to ending the war and is not interested in spending much, if any, more money on the subject. The response by the EU, an emergency meeting in London yesterday where every nation committed to a strong defense of Ukraine, including boots on the ground, is remarkable. My fear is that if they proceed along these lines, and French or British soldiers are attacked/shot during the conflict, NATO will seek to invoke Article 5 and drag the US into the conflict. Certainly, that appears to be Zelenskiy’s goal, to get the US to fight Russia on their behalf. (Although, there are those who might say the Biden administration was using Ukraine to fight Russia on their behalf, so this is justified not surprising.). In the end, I believe this path is terrifying as that would result in two nuclear powers meeting on the battlefield, perhaps a cogent definition of WWIII.

However, there is little evidence that market participants are terribly concerned about this situation. Perhaps they are confident that this is all bluster and ultimately President Trump’s plan of increasing US economic interests in Ukraine will be enacted and a sufficient deterrent to prevent that outcome. Or perhaps this is a YOLO moment, where the belief is, if nuclear war destroys the world, I can’t stop it, so I better make as much money as possible now. I recognize geopolitical risk is tough to price, but I would have expected a lot more flight to safety than so far seen.

In fact, in markets, the true story of the weekend was the announcement of a cryptocurrency reserve to be created by the US although no specific size was revealed. While I don’t typically write on the topic, that is because the crypto space has not yet, in my view, become enough of an influence on the macro world to matter. However, this could change that.

Source: tradingeconomics.com

One cannot be surprised that crypto currency prices have rallied dramatically on the back of the announcement, which almost seemed timed to arrest what had been a very sharp decline in those prices recently. It is too early to really determine if this will draw cryptocurrencies closer to mainstream economic and financial discussion, but I would argue it is closer now than it has ever been before.

In Europe, the scoop on inflation

Does not seem ripe for celebration

While CPI slipped

Most forecasts, it pipped

So, slower but not near cessation

Eurozone CPI data was released this morning and the response to the outcome is quite interesting. The data showed that headline fell from 2.5% to 2.4%, while core fell from 2.7% to 2.6%. Obviously, that is a step in the right direction. Alas, analysts’ forecasts were looking for a 0.2% decline in both readings, so while the data was good, it was worse than expectations. In a perfect encapsulation of how narrative writing is so critical, both the WSJ and Bloomberg wrote articles explaining how the declines had set the table for the ECB to cut rates at their meeting this Thursday with neither one discussing market forecasts.

Now, a look at the market response shows that European sovereign yields have all risen between 6bps and 9bps, hardly the response one would expect in a lower inflation world. As well, with Treasury yields higher only by 5bps this morning, as they bounce from their recent declines, the euro (+0.7%) has rallied sharply on the day.

Much has been made of the European’s new commitments to increase defense spending, especially in the wake of yesterday’s meeting discussed above, and the requisite increases in defense spending that would accompany this new stance. However, increased European defense spending has been a story for the past many weeks as President Trump has been railing against European members of NATO for not holding up their end of the bargain. I guess the meeting added a greater sense of urgency, but remember, not an additional dime has been spent yet, nor even legislated. Talk is cheap!

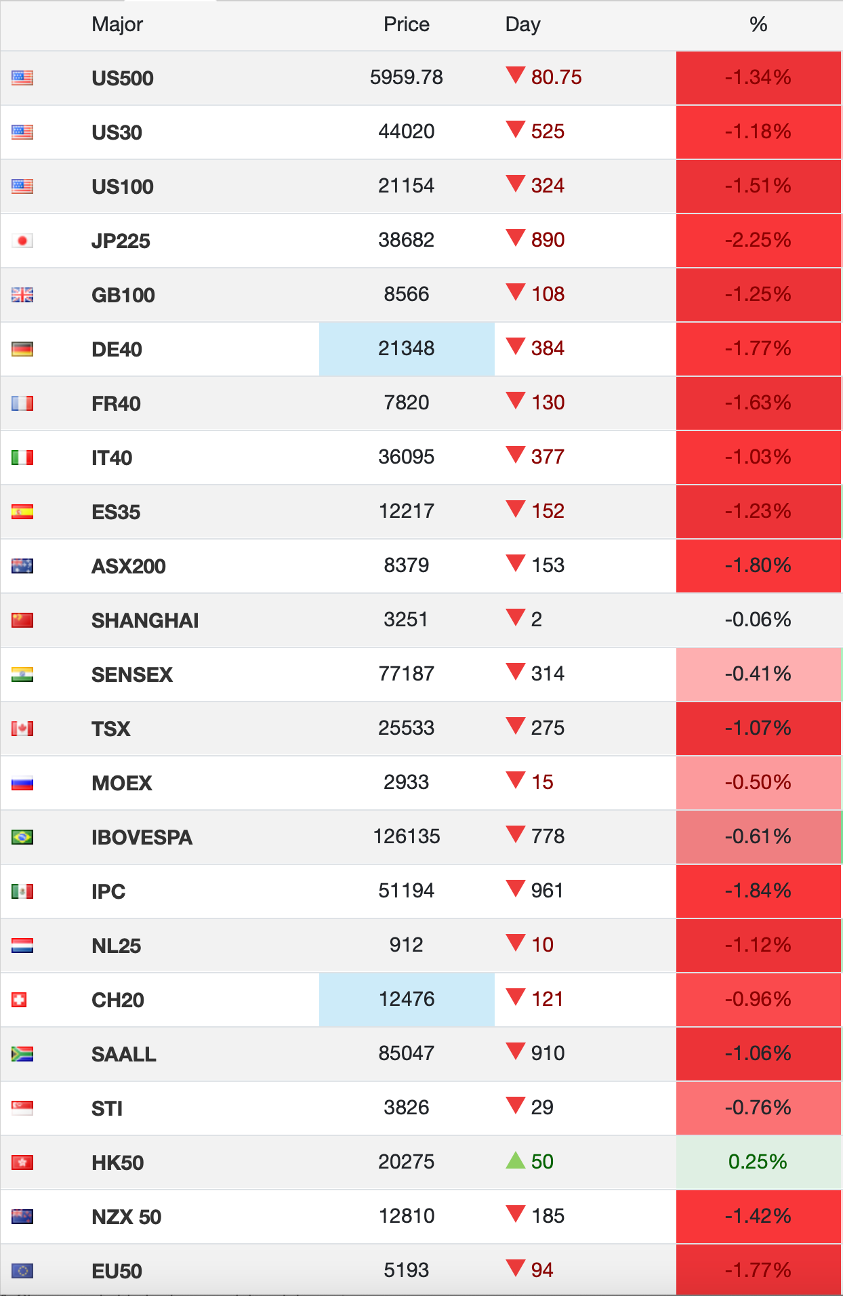

But there you have it. Despite what appears to be a giant step closer to a major global conflagration, the market response has been a more classic risk-on result, with bond yields rising, the dollar falling and most equity indices doing fine. Some days, things don’t make much sense.

Time for a quick recap of overnight markets then. Friday’s strong US equity rally was followed by strength in Tokyo (+1.7%) and Australia (+0.9%) although both Hong Kong and China were little changed in the session. It appears Chinese traders are awaiting the news from Wednesday’s NPC meeting where the government will define their economic growth targets for the current year and how they might achieve them. In Europe, Spain (-0.1%) is the laggard with the rest of the continent doing well, led by Germany (+1.1%). It seems there are more defense companies there to benefit from all this mooted spending than elsewhere, hence the rally. Lastly, US futures are higher by 0.35% or so at this hour (7:00).

We have already discussed bonds, where yields are higher everywhere, including Japan (+4bps) as all the war talk has investors convinced there will be a lot more government borrowing everywhere in the world going forward.

In the commodity markets, oil (+0.25%) has been trading either side of unchanged in the overnight session but seems to be consolidating after last week’s declines. I continue to believe that if the Ukraine war does end (and I believe that will be the outcome regardless of Europe’s hawkish turn), oil prices are likely to slide further as one of the likely outcomes will be the end of sanctions against Russian oil and Russian oil transports. Meanwhile, gold (+0.6%) which had a rough week last week, is bouncing and dragging the entire metals complex higher with it. If war is truly in the air, gold and silver seem likely to rally further.

Finally, the dollar is under great pressure this morning across the board. Not only is the euro higher, but only JPY (-0.4%) is weaker vs. the dollar in the G10 as this seems a very risk-on initiative. SEK (+1.3%) is the leader, perhaps because it is on the front lines of the potential war? Seriously, I have no explanation there. But EMG currencies are also rallying with HUF (+2.1%) the big winner, although the entire CE4 is stronger. Again, this makes little sense to me if the politics is pushing toward war as all those nations are on the front lines. Meanwhile, MXN (+0.4%) is managing to rally despite the ongoing threat of tariffs to be imposed tonight at midnight. I continue to read numerous stories on the potential impacts of tariffs with dramatically different takes. In the end, it appears that at least some things will go up in price, although fears of widespread massive price rises seem a bit overdone.

On the data front, along with Thursday’s ECB meeting, Friday brings the payroll report and there is plenty of stuff between now and then.

| Today | ISM Manufacturing | 50.5 |

| ISM Prices Paid | 56.2 | |

| Wednesday | ADP Employment | 140K |

| ISM Services | 52.9 | |

| Factory Orders | 1.6% | |

| -ex Transport | 0.3% | |

| Fed’s Beige Book | ||

| Thursday | ECB Rate Decision | 2.75% (current 3.00%) |

| Trade Balance | -$93.1B | |

| Initial Claims | 340K | |

| Continuing Claims | 1870K | |

| Nonfarm Productivity | 1.2% | |

| Unit Labor Costs | 3.0% | |

| Friday | Nonfarm Payrolls | 153K |

| Private Payrolls | 138K | |

| Manufacturing Payrolls | 5K | |

| Unemployment Rate | 4.0% | |

| Average Hourly Earnings | 0.3% (4.1% Y/Y) | |

| Average Weekly Hours | 34.2 | |

| Participation Rate | 62.6% | |

| Consumer Credit | $15.5B |

Source: tradingeconomics.com

In addition to this, we hear from 7 more Fed speakers at 9 venues including Chairman Powell Friday afternoon at 12:30. Now, I have made a big deal about the fact that the Fed has lost much of its sway in the market to President Trump. I believe that Powell’s speech will tell us much about whether they are unhappy about this, or whether they will be quite comfortable sinking into the background. Given Powell’s previous antagonistic relationship with President Trump, I would think it would be the latter. But every central banker seems drawn to the limelight like moths to a flame, so I would not be surprised to see something more dramatic.

As things currently stand, I see the ongoing efforts to cut government spending as a critical piece of the US fiscal puzzle. The more success that DOGE and the administration has in this process, the better the potential outcomes for the US, tariffs or not. This could increase private sector activity and reduce the deficit, thus slowing the debt issuance, and perhaps, weighing on inflation. However, this is a longer-term process, not something that will happen in weeks, but over quarters. In the meantime, I cannot get past the Ukraine situation as the biggest potential risk factors around, and if escalation is in the cards, I would expect Treasury yields to decline amid growing demand while the dollar rallies along with the yen as a haven. Hopefully not but be prepared.

Good luck

Adf