In Joburg a gath’ring of nations Is trying to firm up foundations For alternate ways That each of them pays The other with no complications Meanwhile, we are starting to hear A story that we should all fear The calls have come forth Inflation that’s north Of two percent’s where Jay should steer

The BRICS nations are meeting in Johannesburg starting today with, ostensibly, a mission to exit the dollar financial system. While Russia has already done so involuntarily, the biggest proponent of the move is China, although the other nations are certainly willing to listen. In addition to this goal, they will hear from many other developing nations as to whether these other nations merit inclusion in the BRICS club.

Ultimately, the problem that this disparate group of nations has is that none of them really trust any of the others. Certainly, the historical conflict between China and India is well-known and long-lasting. It was not that long ago that their soldiers were shooting at each other in the Himalayas. At the same time, both Brazil and South Africa are extremely remote from the other nations and have completely different economic and political systems. In other words, the common ground of wanting to do something about the US and its dollar, while certainly a goal, is unlikely to be enough for any of them to risk potential negative consequences of a failed concept.

Much will be made of this meeting in the press, but we have already heard from South Africa’s FinMin, Enoch Godongwana, that it is premature for South Africa to stop using the USD and SWIFT system. Ultimately, my strong belief is this is much ado about nothing, at least for the foreseeable future. Perhaps in 25 years, after the 4th Turning is complete, the global currency system will be different, but not anytime soon.

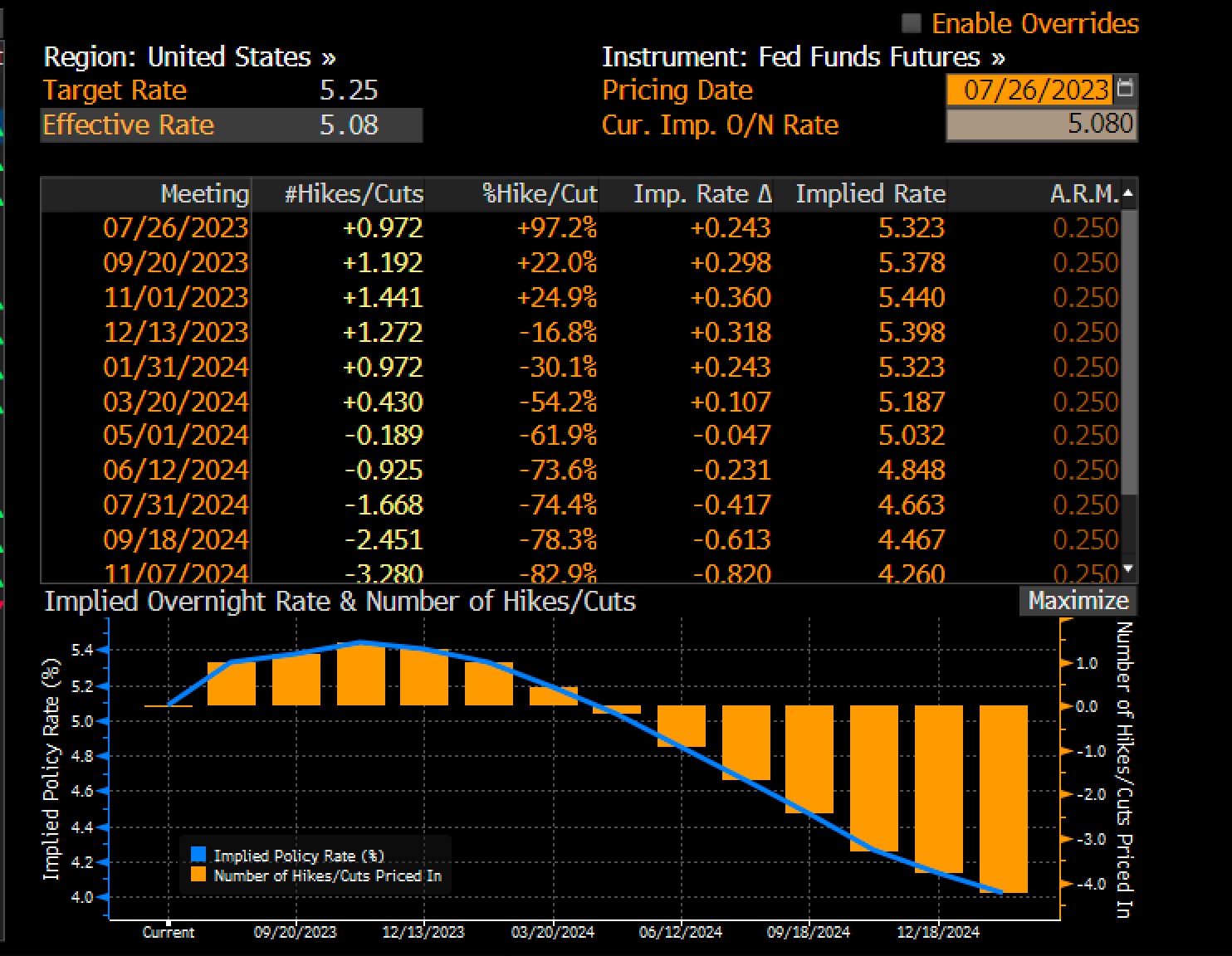

Which brings us to the other story which has me far more concerned about the dollar and the US economy, the substantial increase in calls by mainstream economists to raise the Fed’s inflation target. Understand that I have never been a fan of the target to begin with, recognizing its arbitrary nature. However, the world in which we live has been predicated on the idea that the Fed is focused on that target and its policies are designed to maintain a relatively low rate of inflation. Raising that target, with 3% the new favored call, is just as arbitrary as the initial level, but it changes the dynamic in the economy as well as markets.

It seems these calls are coming from the hyper-Keynesians who lean toward MMT and believe that the risk of any economic growth slowdown should be addressed ahead of all other concerns. (It could be argued that the current administration is quite concerned that a recession next year, heading into the presidential election, would not favor President Biden’s reelection.). Now, nobody is happy when the economy slows down as it makes life difficult for us all, but one of the reasons the nation is in its current situation, with unsustainable levels of debt outstanding, is because the willingness of any politician to allow markets to actually clear (meaning asset prices fall sufficiently to hurt the 1% club) is essentially nil. This has been the underlying driver of constant spending programs and ultimately, the cause of the ballooning budget deficits and Federal debt.

The unspoken piece of this concept is that permanently higher inflation will reduce the real value of the outstanding debt that much more quickly, hence allowing for even more deficit spending going forward. The fact that higher inflation is an effective tax on the bottom 99% of the income brackets, with the pain increasing more rapidly the further down that scale you look, is of no concern it seems.

Thus far, Chairman Powell has been adamant that there is no change to the goal on the table. But I assure you that the longer it takes for inflation to retreat to its former levels, the more we will hear about this idea. When I combine this concept with my belief that inflation is going to remain sticky in the 3%-4% range going forward for quite a while, it does not paint a promising picture. The Fed already has credibility issues; moving the goalposts in the middle of their inflation fight would really destroy any remaining credibility they have, and that would be a real problem for monetary policy activities going forward.

But these problems are far too forward looking for today’s markets. Instead, the future is…Nvidia! At least, that seems to be the case right now. As investors await their Q2 earnings release tomorrow afternoon, the working thesis seems to be that they will beat the currently inflated analyst expectations and drive the next leg of the equity bull market higher. Now, remember, they currently trade at a 228 P/E ratio, which seems pretty high in the scheme of things, regardless of the promise of AI going forward. (You can tell AI didn’t write this as I call into question its value here). There has been much talk of a big ‘beat’ in earnings and that has been the catalyst for today’s equity rally. Well, that and the fact that the Chinese seem to have instructed their ‘plunge protection team’ to get back to buying Chinese stocks as well as the yuan. Regardless of the rationale, though, risk is definitely in favor today.

Asian equity markets were higher across the board, with the big ones all higher by just under 1%. European bourses are similarly situated, all higher by about 1% while US futures, at this hour (7:30) are lagging a bit, only up by about 0.5%, although that was after a pretty solid performance yesterday. Woe betide the equity markets if Nvidia misses its numbers!

At the same time, bond yields are generally lower this morning with 10yr Treasuries down 2bps from yesterday’s new closing high near 4.35%. European sovereign bonds have also seen demand with yields sliding between 4bps (Germany) and 7bps (Italy) as a combination of mildly positive UK Public Sector Finance news and a very large Eurozone Current Account surplus seem to have bond investors quite excited. Asia, however, did not share this excitement with JGB yields rising 2bps and getting to their highest level (0.663%) since the change of policy last month.

On the commodity front, oil (-0.2%) has edged back below $80/bbl, representing a sharp decline yesterday afternoon after signs of increased supply started to show up in the market. The metals markets, however, are in much better shape this morning with gold (+0.4%) back above $1900/oz and the base metals both firmer as well. It seems that mildly lower yields and a weaker dollar are having quite a positive effect.

Speaking of the dollar, it is under broader pressure this morning vs. most of its G10 and EMG counterparts. In the G10, NZD, AUD and SEK have all gained about 0.5% with NOK +0.4% as commodity prices find some support, and the China renewal story helps the overall global growth story this morning. While the euro is little changed on the day, the rest of the bloc has edged higher as well. Meanwhile, in the EMG bloc, ZAR (+1.1%) is the biggest gainer on the day, perhaps getting a little boost from positive BRICS vibes, but more likely from positive commodity vibes. As to the rest of the bloc, APAC currencies have benefitted from the China story and THB (+0.65%) has benefitted from the resolution of the political crisis with a new PM finally being named.

On the data front, we see Existing Home Sales (exp 4.15M) and Richmond Fed Manufacturing (-10) and we hear from several Fed speakers. However, with Powell on the calendar for Friday morning, I don’t think a great deal of attention will be paid to any other Fed speaker until he’s done. There is a strong belief he is going to lay out the policy framework going forward, but I have a suspicion that he is happy with the current ‘guidance’ of higher for longer and may not say much at all.

Right now, risk is to the fore, and as such, the dollar is likely to remain under pressure until that changes. It may be this way all week, or if Nvidia misses its numbers, don’t be surprised to see the dollar reverse course higher after that.

Good luck

Adf