We have now a President Joe

Whose allies had asked him to go

Reject them, he did

For there was no quid

To pay him if he gave the quo

But Sunday, the news was revealed

That his campaign, he would now yield

It’s, therefore, not clear

Who’s running this year

‘Gainst Trump, it’s a wide-open field

Of course, you are all aware by now that President Biden has decided to abandon his re-election campaign and “to focus solely on fulfilling my duties as president for the remainder of my term.” While he has endorsed Vice-president Kamala Harris, and since the announcment, there have been more endorsements for the VP, nothing is clear yet. If nothing else, there has been no clarity whatsoever regrading who VP Harris would select as her running mate should she be the presidential nominee.

In the end, this adds uncertainty to the political situation and is likely to add some volatility to financial markets as well. However, remember that political impact on financial markets tends to be relatively rare and if it is going to be significant, must be a genuine surprise. Given the drumbeat from an increasing number of Democrat politicians and donors, this cannot be considered a real surprise. I suspect that recent volatility will continue, but it is unlikely to increase substantially because of this. However, if, say, the Fed were to cut rates next week, that would be a genuine surprise with a major market reaction. (That is a hypothetical, I am not forecasting that.) All told, the circus that is the US presidential campaign seems likely to simply continue for the next four months.

In China, the Plenum has ended

And rate cuts last night were extended

But is that enough

To help Xi rebuff

The weakness with which he’s contended

In the meantime, while all eyes around the world remain on the US as both allies and enemies try to determine what is happening, and likely to happen going forward, in the US regarding its presidential politics, China’s Third Plenum has ended, and the decisions have been made public. Reuters has given an excellent, and succinct, description of what this meeting represents and why it is seen as so important. The link above is a worthwhile, and quick read, but the money lines are [emphasis added]: “China’s ruling Communist Party commenced its so-called third plenum on Monday, a major meeting held roughly once every five years to map out the general direction of the country’s long-term social and economic policies,” and “This week’s third plenum, described by Chinese state media as “epoch-making”, is expected to deliver major initiatives to address the risks and obstacles related to China’s long-term social and economic progress.”

So, in essence, this is the annual meeting where Xi and his fellow senior policymakers focus on the economy for the next decade. This is quite timely given the economy in China has been consistently disappointing over the past several years with the most recent data releases showing that GDP growth declined to 4.7%, far below expectations as well as Xi’s target, in the second quarter. Now, the law of large numbers would indicate it will be increasingly difficult for China, a $17 trillion economy, to continue to grow at previous rates, especially since its population is shrinking. But that will not stop Xi from trying, or at least from having the government publish numbers that indicate he is succeeding.

Ultimately, the problem in China remains that domestic consumer demand remains lackluster, largely because of the sharp decline in the Chinese property market. In China, property had been a key store of personal wealth as there were limited vehicles in which citizens could invest. But with that bubble having burst, and continuing to deflate, ordinary people do not feel the confidence to continue previous consumption patterns. This is the underlying reason why China continues to focus on industry, and the genesis of the international angst over China’s manufacturing exports. It is also the genesis of why tariffs are so prominent in discussions around Western policy circles. The perception that China is dumping product offshore at a loss, undermining Western companies, and therefore Western job markets, is a powerful political motive to find some way to restrict said exports. Tariffs are the most obvious first solution.

But China knows there are problems internally and that led to last night’s surprise cuts in the Loan Prime Rates for both 1-year and 5-year, with each being cut by 10 basis points. I would look for further rate cuts shortly after the Fed starts to cut rates here (assuming they do so) whether that is next week or in September. Ultimately, I continue to believe that the PBOC will need to allow the renminbi to weaken, but it will be a long, drawn-out process as Xi remains steadfast in his view that the currency must be seen as a stable store of value. Ironically, I believe we are entering a timeline when pretty much every nation will seek to weaken their currency to gain a trading advantage, but of course, if that is the case, then the only thing that will change is inflation will rise. Oh well, policymakers around the world all have the same blind spots.

And those are really the only stories of note, although naturally, the first one is massive and will be the talk of the world for at least the next month until the Democratic convention produces a presidential ticket. So, with all that in mind, let’s look at the market responses overnight.

Friday’s continued weakness in the US equity markets was mostly followed in Asia with the Nikkei (-1.2%) continuing its recent retracement from the highs made a week and a half ago. And that red ink was seen throughout the region with one exception, the Hang Seng (+1.25%) as it responded to the PBOC’s rate cuts. Interestingly, the onshore markets (CSI 300 -0.7%) did not. However, in Europe, this morning, equities are having a great day with strong gains across the board. While part of this is certainly simply a rebound from last week’s declines, it seems that there is a thesis brewing regarding Europeans now gaining confidence that Mr Trump will not be re-elected and so attracting some bullish views. I don’t necessarily agree with that, but that seems to be the take. As to US futures, they are firmer this morning as well, although given the sharp declines at the end of last week, this seems a reflexive bounce

In the bond markets, Treasury yields, which backed up despite the equity market declines on Friday, are softening a bit this morning, down 2bps, while European sovereign yields are mostly little changed from Friday’s levels, down about 1bp in most nations. Right now, there is very little excitement in this space.

In the commodity space, oil prices are continuing their decline from last week with WTI back below $80/bbl as this market seems to believe that Mr Trump will win in November and that he is very serious about ‘drill baby, drill’. Certainly, I would anticipate a Trump administration will be quite focused on increasing energy output and that should undermine prices. As to the metals markets, gold (+0.5%) continues to find buyers although it did sell off sharply on Friday, but the rest of the space is under pressure, notably copper (-1.25%) as that Third Plenum did not encourage anyone that China would be subsidizing further economic activity and driving up demand for the red metal.

Finally, in the FX markets, the dollar is under modest pressure overall, although not universally so. JPY (+0.4%) is the leading gainer in the G10 space as hopes for a Fed cut continue to impact views on the carry trade here. However, the euro (+0.1%) and pound (+0.25%) are also edging higher, albeit on much less information. Perhaps, the idea that Trump has been vocally calling for a weaker dollar is part of this movement, but that seems awfully early in the process. On the flip side, AUD (-0.3%) is being weighed down by the decline in commodity prices. In the EMG bloc, MXN (+0.35%) is the biggest gainer on the day although the CE4 currencies are all demonstrating their high beta with the euro as they have gained about 0.25% across the board. Lacking new information, it appears that the peso is acting as a broad EMG proxy for traders wanting to short the dollar.

On the data front, the important stuff all comes at the end of the week with GDP on Thursday and PCE on Friday.

| Today | Chicago Fed National Activity | 0.3 |

| Tuesday | Existing Home Sales | 3.99M |

| Wednesday | Goods Trade Balance | -$98.0B |

| Flash Mfg PMI | 51.7 | |

| Flash Services PMI | 54.4 | |

| New Home Sales | 640K | |

| Thursday | Initial Claims | 239K |

| Continuing Claims | 1869K | |

| GDP Q2 | 1.9% | |

| Durable Goods | 0.4% | |

| -ex Transport | 0.2% | |

| Friday | Personal Income | 0.4% |

| Personal Spending | 0.3% | |

| PCE | 0.1% (2.4% Y/Y) | |

| Core PCE | 0.1% (2.5% y/Y) | |

| Michigan Sentiment | 66.5 |

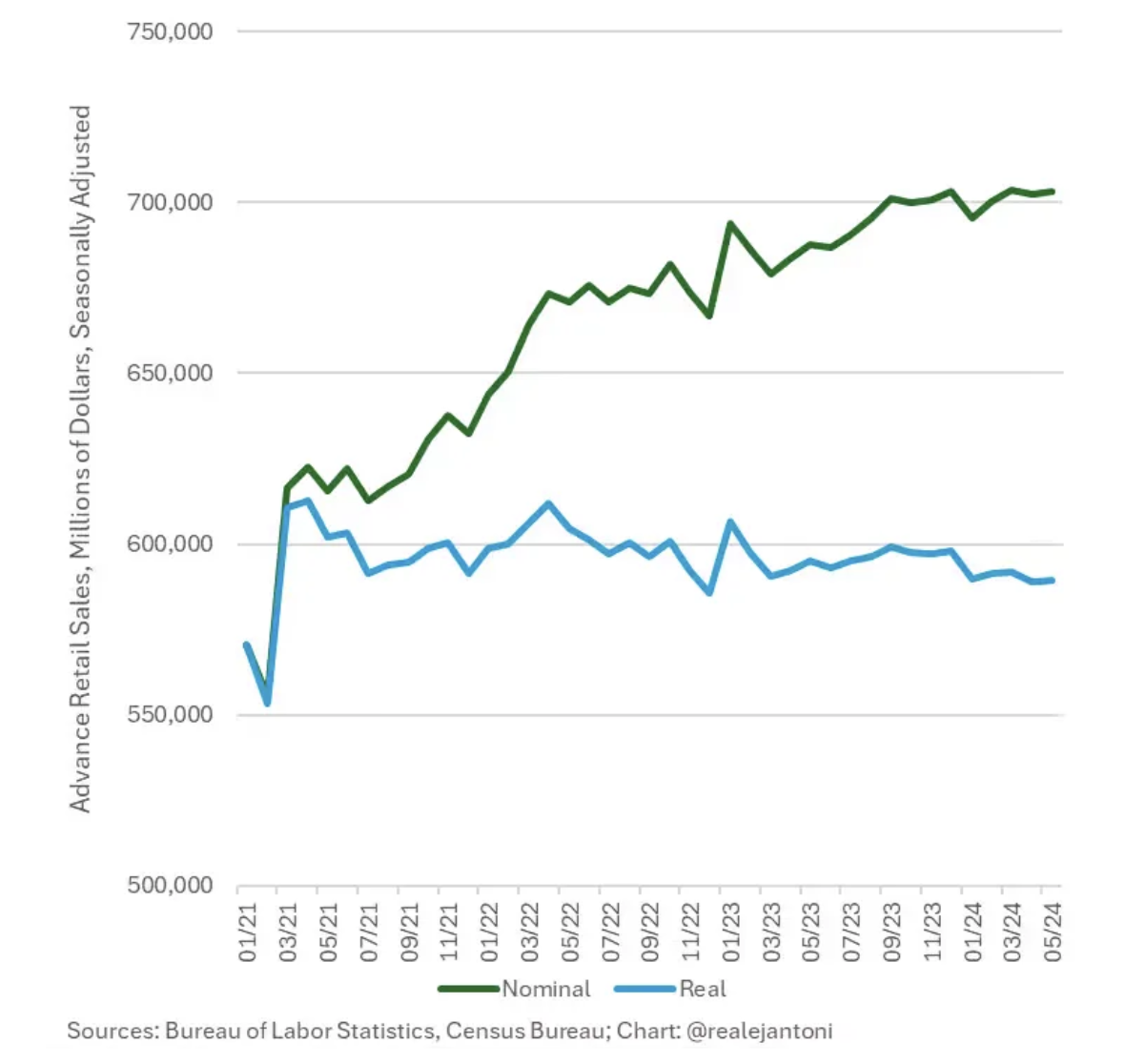

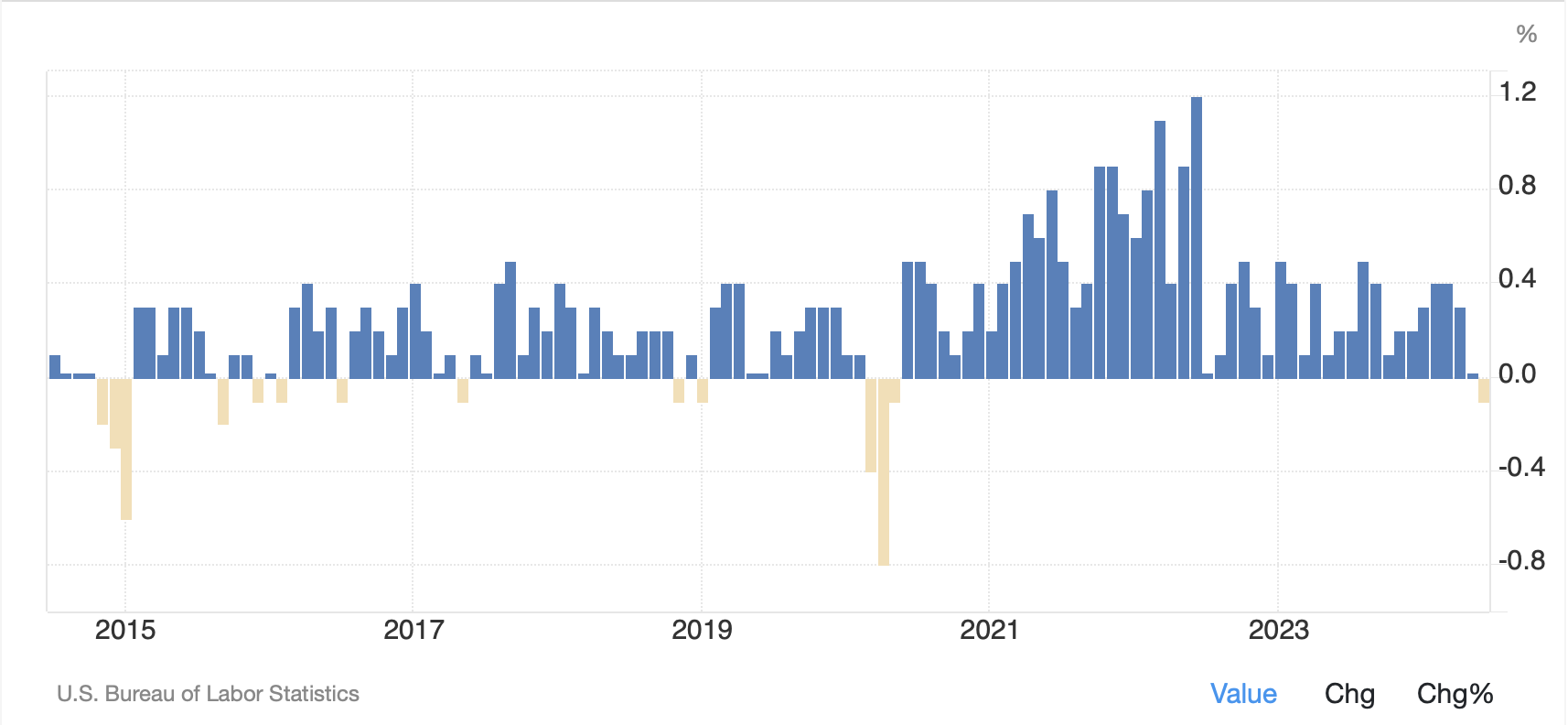

Mercifully, there will be no Fedspeak at all this week as they remain in the quiet period. The expected declines in PCE inflation will continue to support the September rate cut expectation which remains at a virtual 100% probability according to the CME Fed funds futures pricing. That would be in concert with everything we heard from Fed speakers in the past several weeks, although the stronger than expected Retail Sales data has some claiming the Fed will remain on hold. My read is there are fewer people discussing an impending recession, although that may be more about the cacophony of political discussion drowning things out, than a real change in sentiment. Alas, I find myself far more concerned about an economic slowdown, although not necessarily with a corresponding decline in inflation. Meanwhile, the dollar, while under some modest pressure, remains pretty solid and I wouldn’t look for a significant change, at least not until Friday’s data.

Good luck

Adf