If CPI data today

Is hot, then get out of the way

Amid the death knell

Investors will sell

Stocks for which they did overpay

But if, instead, CPI’s cool

The thing to expect, as a rule

Is risk asset rallies

And FinTwitter tallies

Of profits o’er which some will drool

There are some who believe that today’s CPI data will not lead to much price action at all. The thesis seems to be that everybody is too focused on the outcome, and that any hot print will be immediately talked away by folks like Nick Timiraos in the WSJ and every other administration official (Yellen, Brainard) or folks like Larry Summers or Paul Krugman (although I don’t think anybody listens to him anymore). The idea is that the government will not allow things to get out of control ahead of the election and so inflation will be denied and the path to a June rate cut will not be denied. It is easy to ascertain that the FOMC is anxious to cut rates, and I’m sure there is intense pressure on them to do so behind the scenes from the administration. After all, why would they all explain that inflation remains hotter than they expected, but think they are going to cut anyway? The one thing I am willing to wager is that if we see a hot number, there will be an article in the WSJ before lunchtime explaining that it doesn’t change anything.

On the other hand, if the data comes in cooler than expected, one would have to believe that we are going to see risk assets once again take the bit in their proverbial mouth and run higher again. Animal spirits remain quite robust and the modest down days from Friday and yesterday are nothing compared to what we have seen. Very likely, some risk has been lightened up, but I would argue there is very little change of heart at this point.

One thing, though, that is very important is if the market behavior does not follow the data release. For instance, if a hot print results in a short-term dip and then a reassertion of the bull trend, that is hugely positive for risk assets for the next several weeks I would think. Or certainly up until the FOMC meeting. Similarly, if a cool number results in a short-term pop in futures but a continued sell-off over the session, that would be a signal that a correction has begun. A market that cannot rally on good news is one that is exhausted.

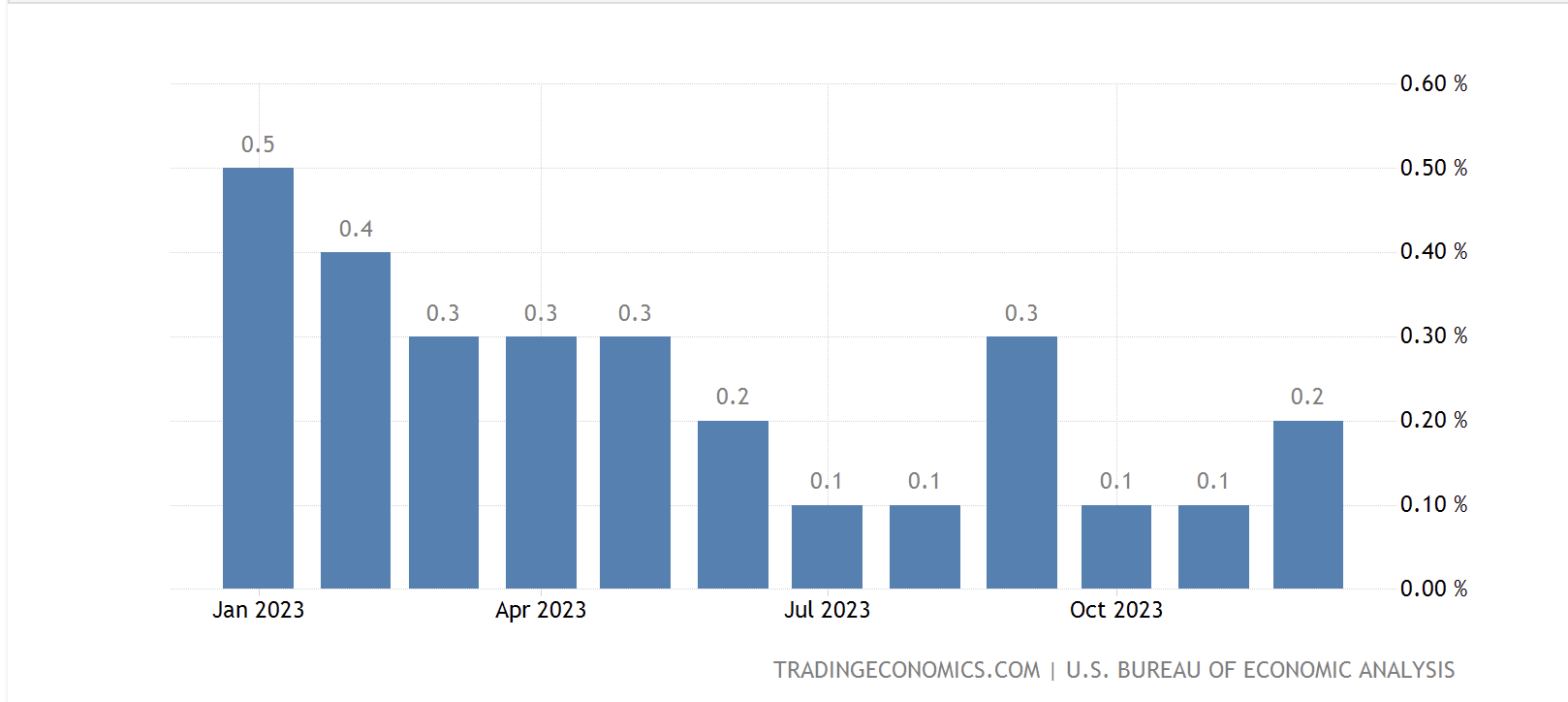

For good order’s sake, let me repeat the current expectations: Headline (0.4%/3.1% Y/Y) and Core (0.3%/3.7% Y/Y). Prior to the CPI data, we have already seen the NFIB Small Business Optimism index which fell to 89.4, a point worse than expected. Interestingly, the largest concern amongst this cohort of business owners is rising inflation, which has replaced ability to find quality employees at the top of the list of issues. This is not the type of data the Fed wants to see, rising inflation expectations alongside a softer labor market. But in the end, it’s the CPI data that is going to matter today.

Aside from that, or perhaps more accurately because everyone is so focused on that, there has been very little else ongoing in markets overnight.

After a very lackluster session in the US yesterday, last night saw Japanese stocks essentially unchanged with the big activity in Hong Kong (+3.0%) despite the largest listed property company, Vanke, getting downgraded to junk by Moody’s. Methinks there could have been some official activity there to help support things. Interestingly, both South Korea and Taiwan saw positive sessions, but most of the rest of the region did very little at all. In Europe this morning, we are seeing gains led by the FTSE 100 (+1.0%) which seems to be responding to a slightly softer than forecast employment report (Unemployment rose to 3.9% and wages slid a bit) with growing expectations that a rate cut will come sooner rather than later. And at this hour (7:30) US futures are a bit firmer, about 0.3% or so.

In the bond market, yields backed up slightly yesterday although the 10-year Treasury remains at 4.10% ahead of both the CPI report and today’s 10-year auction. European yields are a touch softer this morning -1bp, except for UK Gilts (-6bps) which also see the prospects for a rate cut coming sooner than previously thought. Finally, JGB yields edged 1bp higher overnight amid further chatter that the BOJ is going to move next week. The latest rumors from Tokyo are that the Shunto wage talks have seen significant wage hikes agreed which has been a precondition for the BOJ to exit NIRP. It strikes me that whether they move on Monday or next month it doesn’t really change anything as I continue to believe that the totality of the movement will be limited at best, perhaps 30bps overall.

In the commodities markets, oil is little changed this morning, still stuck in the middle of its recent trading range. Gold (-0.4%) is sliding this morning for the first time in 2 weeks, in what appears to be a modest correction. However, both copper and aluminum are a bit firmer this morning along with most of the rest of the commodities space as the dollar seems to be drifting a bit.

Speaking of the dollar, I would argue it is a touch softer overall, although there are both gainers and losers around. ZAR (+0.6%) and SEK (+0.4%) are the best performers across all currencies while we are seeing weakness in JPY (-0.3%) and HUF (-0.4%). The gainers appear to be a product of inflows to their equity markets as both have had good runs today while the laggards have no such excuse with Hungarian stocks rising nicely. As to the yen, that remains beholden to the BOJ story I believe, so is likely to remain somewhat idiosyncratic compared to the rest of the FX complex until next week.

And that’s really all we have today. It’s CPI then bust. I remain in the sticky inflation camp and anticipate a print at least at the current expectations with a decent chance of something a touch higher. I remain convinced that the next dot plot will show only 2 rate cuts as the median forecast for the Fed and today’s data will be a key part of that story. If that is the case, the dollar’s recent weakness is likely to come to an end as it finds some real support.

Good luck

Adf