Come Wednesday through Friday this week

It’s payrolls and Powell to speak

Let’s take time today

To hear people say

What’s driving the year-to-date streak

The first key is so many think

That Powell and friends need to blink

And cut rates quite soon

Else markets will swoon

And ‘flation will not rise, but sink

The other idea that’s around

Is AI and Bitcoin are bound

To fly to the moon

An idea, jejune,

For OG’s, though elsewhere profound

Once again, lackluster was an apt description of the market activity yesterday, although given the plethora of information that is on the horizon, we cannot be surprised by this result. As such, I thought it might be worthwhile to review the themes that seem to be driving markets these days, as well as how expectations are built into pricing.

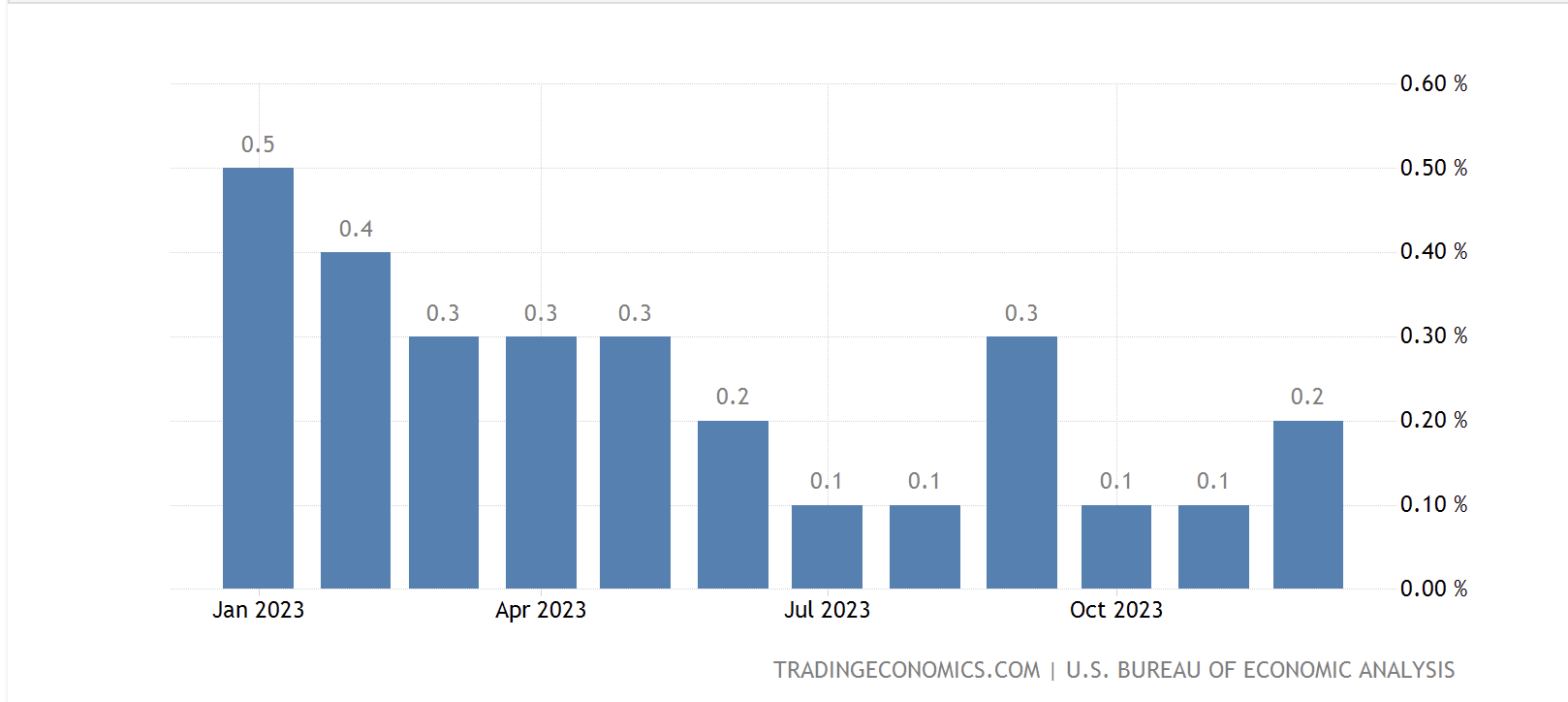

Clearly, the biggest story remains the Fed and its potential timeline for the mooted rate cuts necessary to achieve the much-vaunted soft landing. As of this morning, the probability of a May cut remains near 24% with June the odds-on favorite for the first action. While there has been some back and forth with respect to the actual probabilities, there has been no major change in that view for several weeks. My question continues to be, why are so many people of the opinion that the Fed must cut rates?

So far, at least based on both the GDP and payroll data, the economy is chugging along quite well with the current monetary policy settings while inflation remains well above the Fed’s target. Arguably, a great deal of that is due to the fiscal impulse that has been ongoing, but there is no sign that is going to end anytime soon. In fact, it strikes me that easing monetary policy amid a period of fiscal excess may juice the inflation data substantially. Literally every Fed speaker has made this exact point, that things are going well, inflation seems to be trending lower, but there is more certainty needed before a cut would be appropriate.

Adjacent stories here are related to the election in the US, with many assuming the Fed will cut rates to help support the Biden administration (I think this is extremely unlikely). The other key story has to do with the other G7 central banks, and their ability/willingness to change policy prior to the Fed. Considering that Japan, Canada, the UK and Europe are all basically in recession, or right on the cusp, there is a far greater need to ease monetary policy in those places. However, they have a serious concern that if they cut before the Fed, the dollar will rally sharply and negatively impact both economic activity and market activity, as well as undermine their currencies. In the end, everybody is waiting for Godot Powell, and it is not clear he is going to come through.

The second key story is the remarkable performance of both Bitcoin and the tech sector. There have been many stories comparing the current move in the NASDAQ to various times in the late 1990’s and the runup to the Tech bubble then. We all know that eventually, despite the internet having an amazingly profound impact on all our lives, the tech sector corrected more than 80% from its early 2000 peak and it took 15 years to regain those levels. I don’t think anybody is willing to say that the current tech leaders are bad companies with problems, but the price one pays for a company’s shares is THE key to long-term investment performance. AI can be transformative in many ways and that doesn’t mean these shares will not decline and decline sharply.

Speaking of AI’s impact, my good friend the @inflation_guy, Mike Ashton, wrote a terrific piece about the potential impact on the economy overall, comparing it to the internet, the last significantly transformative technological revolution. This is a must read! Ultimately, while the impact of the internet was significant, it was not nearly as productivity enhancing as many had forecast at the initial stages of the mania. Just keep that in mind with respect to AI as well.

As to Bitcoin, it is pushing to new all-time highs as flows into the spot ETF’s are quite substantial and driving the move. However, it strikes me that the rationale for buying Bitcoin is very different than the rationale for buying NVIDIA. Bitcoin believers are concerned over the integrity of the entire concept of money and its future. They look at the dramatic increase in Treasury issuance and ask, is that debt really risk-free? They are seeking to own alternative assets, outside the current monetary framework. Meanwhile, buying the AI craze is as mainstream as you can get, counting on the equity values to rise substantially from here and protect your wealth, even if it is denominated in a currency that is subject to inflation and devaluation. But for now, the two are linked at the proverbial hip.

I would not look to short either process at this point, but having seen numerous bull markets in my time, the one thing I know is that trees don’t grow to the sky. At some point, there will be a significant correction in both these asset classes, and we are sure to hear a great deal of screaming about how the Fed needs to come in and stop it.

In China, last night Premier Li

Revealed what their growth ought to be

Though clearly well-meant

To reach five percent

Is certainly no guarantee

One other key story overnight was Premier Li Qiang’s speech in which he declared the GDP growth target for China this year is “around 5%” with inflation to run at 3% and a budget deficit also at 3%. While this all sounds great, there is reason for some skepticism. Perhaps the biggest issue is that domestic demand for products is not growing and is unlikely to start doing so until the property crisis is behind them. However, given President Xi’s unwillingness to face that music, the drawn-out process to address the situation will likely weigh on overall economic activity for a few more years yet.

There is a potential knock-on effect of this, though, and something that I have not really considered in the past but need to investigate further. We all know that there is a concerted effort by G10 nations to reshore and friendshore manufacturing capacity, and that has been a key driver of US economic activity. Recall, that was the entire goal of the Inflation Reduction Act. It has also been clear that there is currently a boom in factory construction in the US, something else supporting GDP data. Now, if the US, and much of the G10, is adding to manufacturing capacity while China maintains its own manufacturing capacity, that is a LOT of capacity to build stuff. It is not unreasonable to expect that the prices of manufactured goods will decline given what could well be significant excess supply.

In the US, regardless of who wins the presidential election, it is very easy to foresee another increase in import tariffs on Chinese goods (Trump has proposed a 60% tariff on all Chinese imports). We have heard similar rumblings from Europe as well. The point is that absent a substantial change in trade policy, goods inflation is likely to be well-contained. Services inflation is a different issue, and given services represents a much larger proportion of the US economy, seems likely to keep price pressures pushing higher. But rampant price rises are far less likely if we wind up with duplicate production sources for various goods. Of course, tariffs will feed directly into inflation data, and the Fed cannot address that at all.

My point is that the economy is a highly interconnected and complex system and tracking all the potential outcomes is extremely difficult, if not impossible. This is just one that I hadn’t considered in the past but may have some legs. To be continued…

Ok, I have gone on too long so here’s the recap for overnight. The Hang Seng sold off (-2.6%) but otherwise in Asia and Europe shares are little changed. Yields are broadly lower (Treasuries -3bps, Europe -5bps on average) while oil prices have slipped a bit. Gold (+0.5% and new all-time highs) is the commodity outlier. Finally, the dollar remains little changed and is likely to stay that way until we see the next monetary policy adjustments.

ISM Services (exp 53.0) is the only data release today and only Michael Barr is speaking. I see no reason for things to move very far until tomorrow, when both ADP Employment is released, and Chairman Powell testifies. Equity futures are pointing a bit lower this morning after a soft session yesterday. That drift feels like it can continue as we await the rest of the week’s news.

Good luck

Adf