While data at home is robust In Europe and China the thrust Is weakness abounds Which seems to be grounds For traders, their risk, to adjust So, equities are on the schneid While bond yields have been amplified The dollar’s on fire Continuing higher And oil’s climb won’t be denied

Another day, another wave of bad economic news from elsewhere in the world. However, the US continues to surprise with better than expected results. Yesterday’s ISM Services data was far better than forecast with a headline print of 54.5, 2 points above both last month and expectations for this month, while the sub-indices all showed significant strength, including the Prices Paid index. The latter is clearly a concern for Chairman Powell and his crew as it is an indication that inflationary tendencies have not yet been snuffed out. Ultimately, the market response was to sell stocks and bonds while increasing the probability of a November Fed funds rate hike a few points. Interestingly, the market pricing for a September hike has fallen to just a 7% probability despite the hotter than expected data. My sense is that the big market adjustment is going to come as traders come to understand that higher for longer means no cuts until 2025 on the current basis, especially if we continue to see data like the ISM print yesterday.

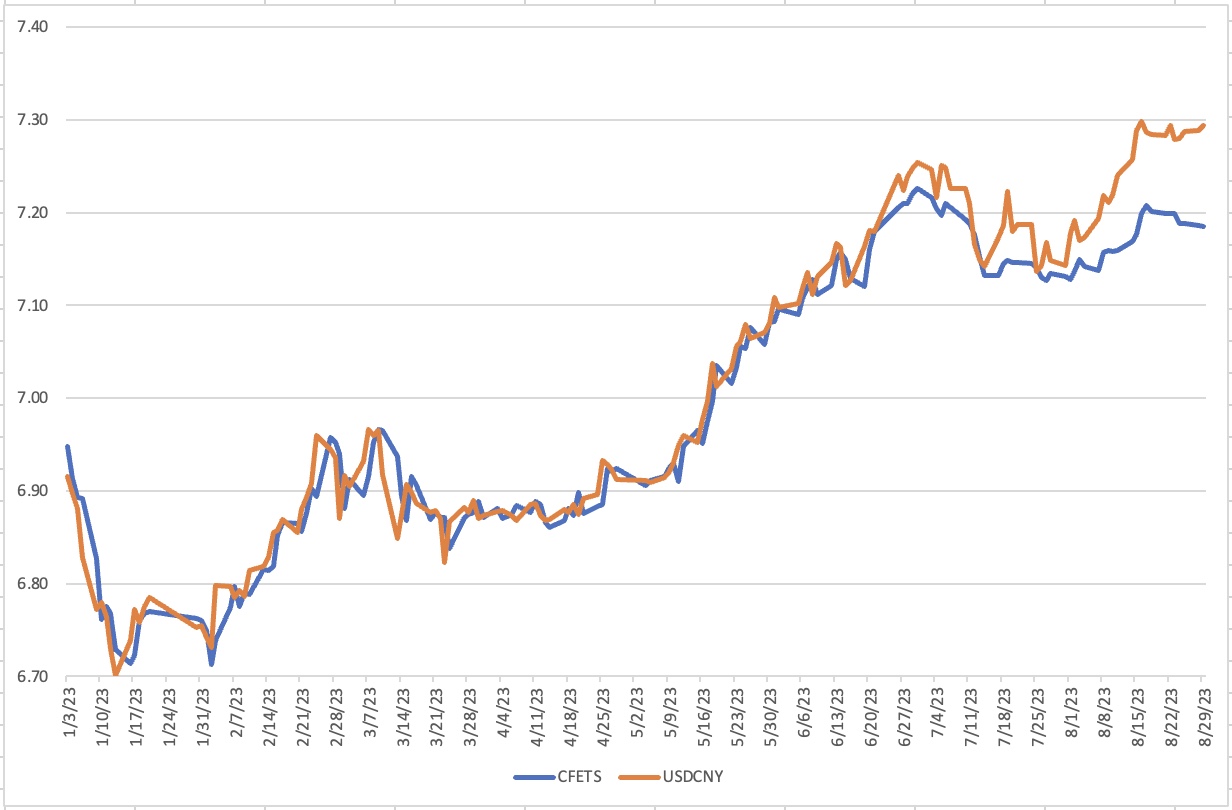

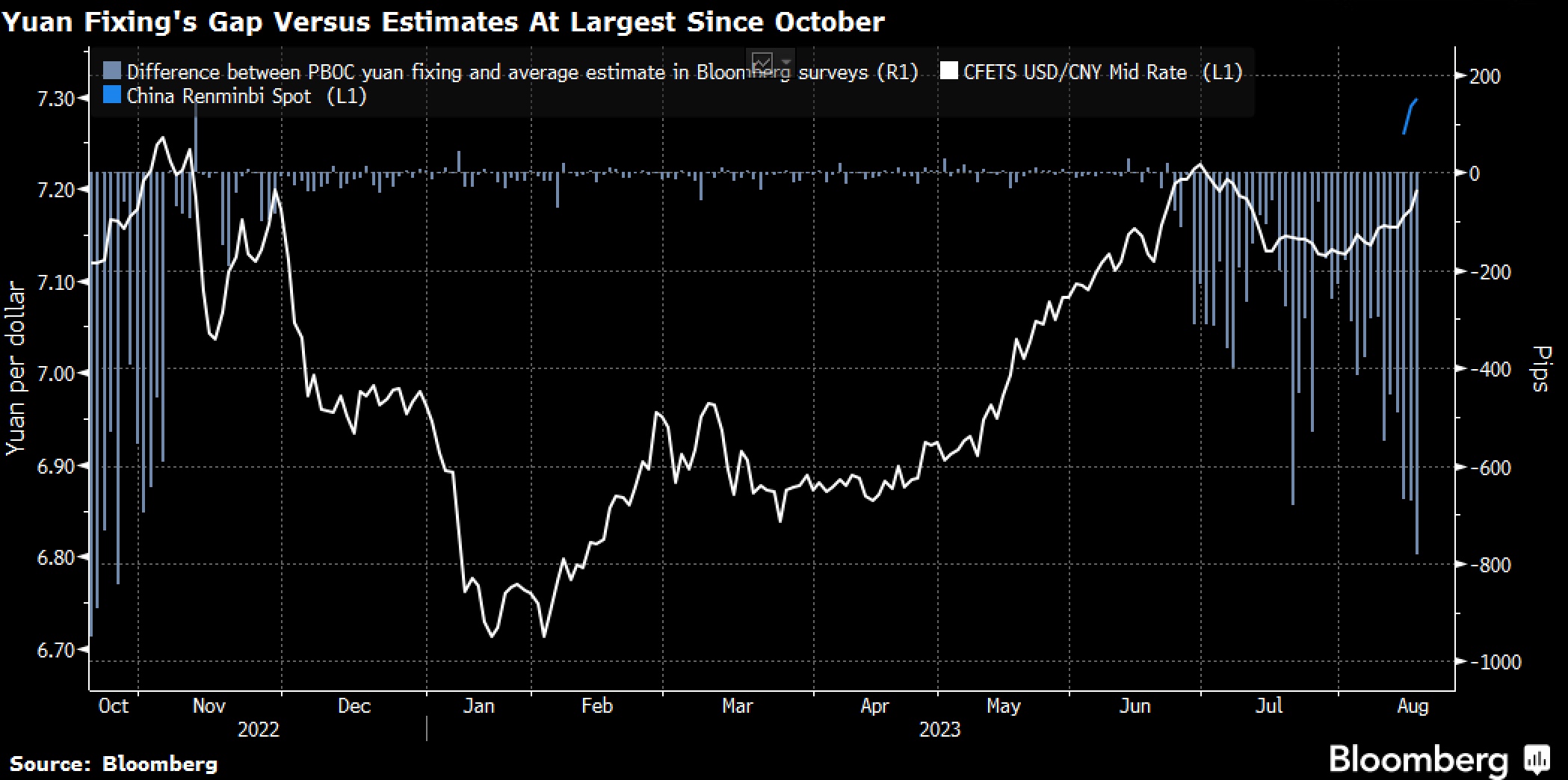

But the US storyline is clearly not the same as the storyline elsewhere in the world. Last night, for example, Chinese trade data was released and both imports (-7.3%) and exports (-8.8%) fell sharply again, with the Trade Surplus falling to $68.3B. Granted, the declines were not as bad as last month, nor quite as bad as expectations, but there is no way to spin the data as indicating a positive economic impulse in China right now. While Chinese equity markets fell sharply (Hang Seng and CSI 300 both -1.4%) we also saw further weakness in the renminbi.

The PBOC is still desperately trying to prevent the renminbi from weakening too quickly, but they are having a hard time at this stage. The difference between the CFETS fixing and the onshore spot market is now 1.8%, dangerously close to the 2.0% boundary. At the same time, the offshore renminbi, CNH, is pushing back to its highs from last October, now trading above 7.3400, which is 1.97% above the fixing. This is a losing battle for the PBOC unless they change their monetary policy, but given the Chinese economy’s weakness, tighter money seems an unlikely step. 7.50 is still on the cards here.

China, though, is not the only problem. European data this morning was uniformly lousy with German IP (-0.8%) and Eurozone GDP (Q2 revised lower to 0.1% Q/Q, 0.5% Y/Y) highlighting the problems facing the old world. Alas, price pressures have not yet abated there, and stagflation is the new watchword on the continent.

When the US was faced with stagflation in the 1970’s, Paul Volcker opted to fight inflation first, sending the country into a double dip recession in 1980 and 1981-82, before things turned around. But that was a different time…and Christine Lagarde is no Paul Volcker! Is it even possible for an “independent” central bank to knowingly create a recession to slay inflation these days? I suspect inflation would need to be far higher, stable in double digits, before politicians would accept that it is a bigger problem than a recession, at least electorally. The upshot of this scenario is that the ECB, despite ongoing higher than targeted inflation, is very likely at the end of its hiking cycle. This, combined with the overall weak economy there, is going to continue to undermine support for the euro. While the movement will be gradual, I expect that the single currency will slide below 1.05 and possibly get to parity by the end of the year.

And I would be remiss if I didn’t touch quickly on Japan, where they released their Leading Indicators at a weaker than expected 107.6, continuing the two-year downtrend. Slowing growth in Japan and still extraordinarily loose monetary policy is going to continue to weigh on the yen. While it has bounced slightly this morning, 0.2%, it continues to weaken steadily closer to the psychological 150.00 level.

So, with all that happy news, let’s tour the overnight session to see the results. The rest of the APAC equity markets also were under pressure overnight with Japan, Australia and South Korea all in the red as well. In Europe this morning, the picture is more mixed with some gainers and some losers but no large movements overall, mostly +/- 0.2%. US futures, after a lousy session yesterday, are all pointing lower at this hour (7:30) as well.

In the bond market, Treasury yields are essentially unchanged on the day, holding onto their gains for the past week and just below the 4.30% level. European sovereigns, though, are seeing a bit of support as the weak economic data has engendered hope that inflation will stop rising and the ECB will be okay to pause. The latter remains to be seen. I cannot get over the idea that the uninversion of the yield curve is going to come because long rates are going to rise, not because short rates are going to be cut, and I’m pretty sure nobody is ready for that outcome.

Oil (-0.5%) is consolidating its recent gains with WTI north of $87/bbl and showing no signs of backing off. If OPEC+ keeps a lid on production, you have to believe that prices will continue to rise. In the metals markets, both copper and aluminum are soft today, responding to the weak Chinese and German data, while gold, after a selloff this week, is bouncing slightly.

Finally, the dollar remains king of the hill, stronger against virtually all its counterparts in both the G10 and EMG blocs. I’m old enough to remember when the prevailing narrative was the dollar was dead and would be replaced by the euro, or the yuan, or a BRICS currency and yet, it continues to be subject to more demand than virtually every other currency around. The broad story is the US economy continues to lead the global economy and the prospects for Fed rate cuts are diminished relative to other nations. Tight monetary and loose fiscal policy combinations have historically been very supportive of a currency and clearly that is the current US state.

Two quick stories in the EMG bloc are from Poland (-0.7%), where yesterday’s surprising 75bp rate cut has undermined the zloty amid concerns that inflation is going to remain unhindered there, and MXN (+0.75%) where traders are unwinding some positions after a sharp decline over the past week. The peso has been one of the few currencies that has outperformed the dollar this year as Banxico has been ahead of the curve on inflation and tight monetary policy. However, with an election upcoming it appears there may be a change in attitude there. If that is the case, then look for the dollar to regain some lost ground.

On the data front, Initial (exp 234K) and Continuing (1719K) Claims are released along with Nonfarm Productivity (3.4%) and Unit Labor Costs (1.9%). As traders and investors bide their time ahead of next week’s CPI and the following week’s FOMC meeting, it is not clear that today’s numbers will have much impact. As such, I see no reason for the dollar to cede its recent gains, especially if equities remain under pressure.

Good luck

Adf