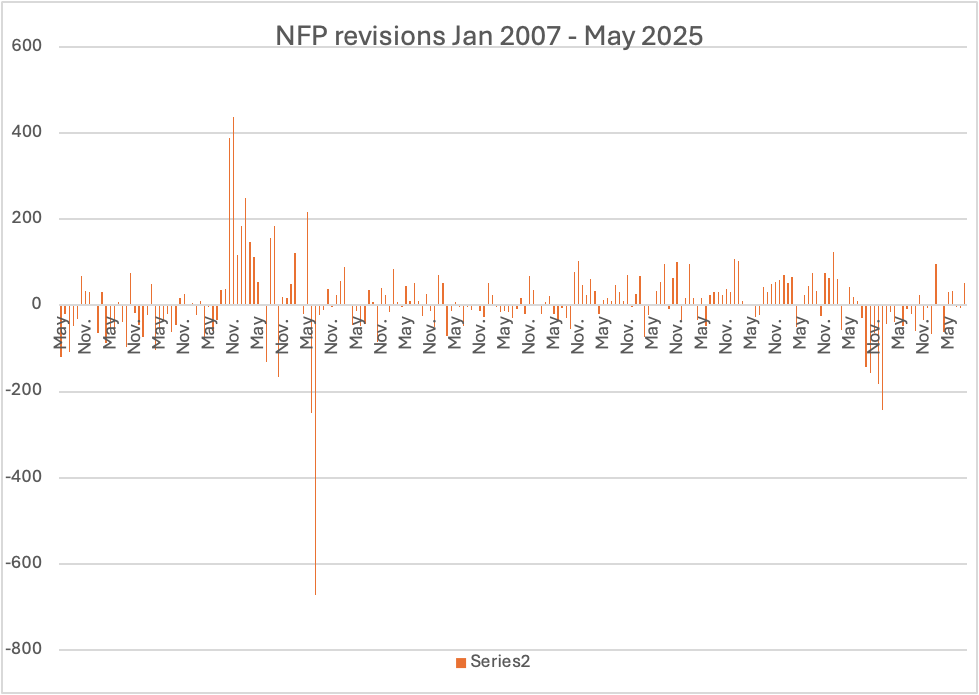

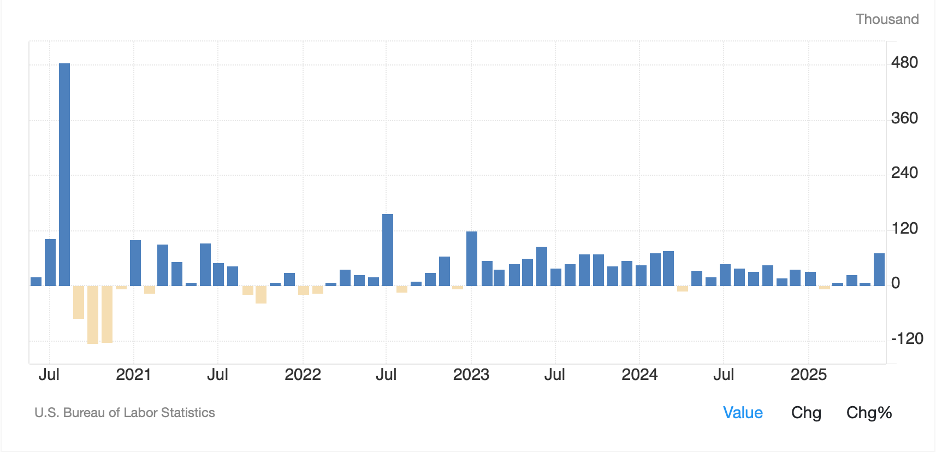

However, it is a fair question to ask if she was incompetent or politically motivated in her daily activities. After all, it is abundantly clear there are many government workers who are ostensibly non-partisan who are, in fact, highly partisan. As such, I took a look at the seasonally adjusted NFP data (the non-seasonally adjusted data is wildly volatile) to see if we could discern a pattern. I created the chart below from BLS data on revisions with May 2025, the latest month with the normal two revisions, on the left and January 2007, prior to the GFC, all the way on the right.

If you look on the left side of the chart, you can see a great many negative revisions. In fact, 21 of the last 29 months were revised lower from the original print. If we assume that the BLS models are unbiased, then one would expect a roughly equal distribution of both positive and negative revisions over time. It turns out, under the unbiased assumption, the probability of 21 out of 29 negative revisions is a very tiny 0.80%.

What conclusions can we draw from this? My first thought is that the BLS models are not very effective at modeling reality. I have raised this point many times in the past, the idea that the models that worked in the past, certainly pre-Covid, have been having trouble. This begs the question as to why an economist of Ms McEntarfer’s long experience didn’t seek to develop a more accurate model. As it is, there is no evidence that she did so. I imagine as a government employee, the idea that one should change something that exists within the government framework is quite alien. Thus, her competence could certainly be called into question, I think.

If we consider the alternative, that her actions were politically motivated, that will be more difficult to discern. However, given the predominance of Democrat voting members of the federal government and given the fact she was appointed to this position by President Biden, it is fair to assume she is not in favor of the current administration, at the very least. Now, during Mr Biden’s term, the initial NFP data was consistently better than expected, thus giving the impression that the economy was stronger than it may have otherwise been. After all, stories about revised data are usually on page 12 of the paper, not headline news. It is, therefore, possible that she was putting her proverbial thumb on the scale to flatter Biden’s economic performance. As to her likely distaste of Mr Trump, I expect that to the extent she had the ability to do so, weaker headlines and large negative revisions would be exactly her contribution.

However, the political issue is largely speculation on my part, although I would argue it is plausible. On the other hand, there is nothing in her background to suggest she is an especially thoughtful or creative economist and there is no indication that she examined the models she oversaw for flaws. In the end, I come down on incompetence driving a political motive. But I doubt we will ever know.

Now, it is not a very good look for a leader to proverbially kill the messenger, which is essentially what Trump did. Not surprisingly, much hair is on fire in the press and punditry, not because they though McEntarfer was particularly good at her job (I’m sure nobody had ever heard of her before) but because, as we have observed time and again, President Trump doesn’t follow their rules, and they don’t know what to do about it.

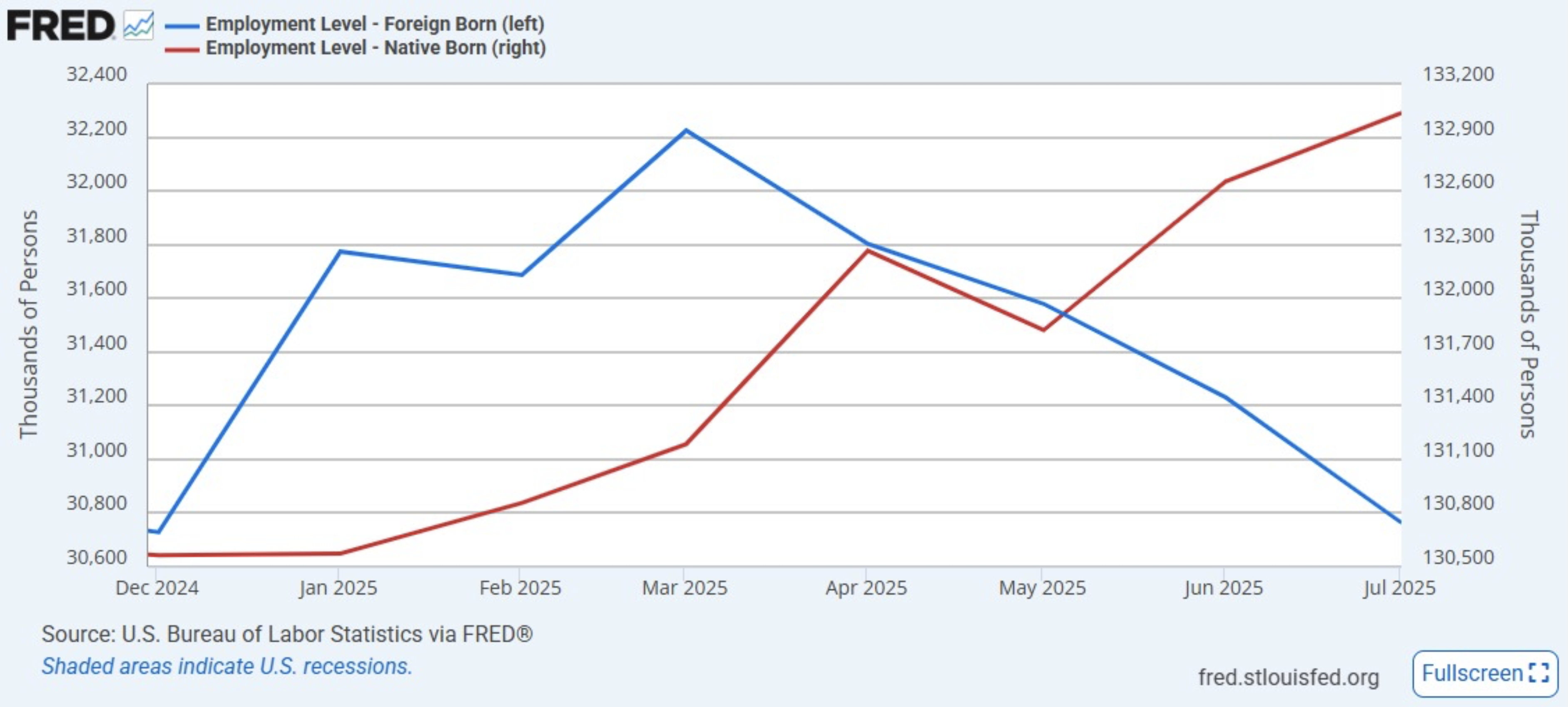

Will this matter in the end? This is merely the latest tempest in a teapot in my opinion and will do nothing to change the economy. However, there is one interesting feature of the employment situation that can be directly attributed to the immigration situation. As you can see in the FRED chart below, since March, the number of foreign-born workers has declined by 1.46 million while the number of US born workers has increased by more than 1.8 million. I would say that as long as American citizens are finding jobs, President Trump is likely to remain quite popular across the nation despite all the negative press.

The weak NFP report altered the narrative on Friday, with bond yields, equity markets and the dollar all tumbling and the probability of a September rate cut jumping to 80%. Perhaps President Trump is correct, and it is time to cut rates.

While NFP’s top of the list For traders this morning, the gist Of recent releases Show more price increases A trend that cannot be dismissed

As well, Tariff Man, once again Imposed more by stroke of a pen While stocks are declining The dollar’s inclining To rise vs. the euro and yen

Let’s get the upcoming data out of the way first as the Employment report is due to be released at 8:30. Current median expectations are as follows:

Nonfarm Payrolls

110K

Private Payrolls

100K

Manufacturing Payrolls

-3K

Unemployment Rate

4.2%

Average Hourly Earnings

0.3% (3.8% Y/Y)

Average Weekly Hours

34.2

Participation Rate

62.3%

ISM Manufacturing

49.5

ISM Prices Paid

70.0

Michigan Sentiment

62.0

Source: tradingeconomics.com

This report is obviously of great importance as the Fed continues to rely on a solid labor market as its key justification for not cutting rates. At least that’s its public stance. Recall, too, that last month’s result of 147K was significantly higher than forecast and really backed them up. In fact, I would contend that one of the reasons that Chairman Powell was willing to sound mildly hawkish on Wednesday is because of the labor market’s ongoing performance.

It is interesting to juxtapose this strength with the increasing number of stories about how the increase in investment and usage of AI, especially at tech firms, is driving a significant amount of personnel reductions. And yet, the broad data continue to point to a solid labor economy.

However, I think it is worth taking a closer look at recent inflation focused data as that, too, is going to be a key driving force in the central bank debate worldwide. Yesterday’s PCE data was largely as expected but resulted in a faster pace of inflation on both the headline and core bases. If we consider the trend over the past three years, as per the Core PCE chart below, it appears that the nadir was reached back in June of last year, and while not every print has been higher, I will contend the trend is starting to point upwards.

Source: tradingeconomics.com

Meanwhile, if we turn our attention to European inflation data, while this morning’s Eurozone flash print was unchanged from last month, it was higher than expected. We saw the same trend in individual Eurozone nations yesterday with Germany, Italy and France all showing the recent disinflationary trend stopping, at least for the past month. With these recent releases, the analyst community is of the mind that the ECB is likely to hold rates steady again in September, extending the pause on their previous rate cutting cycle. The strong belief is that US tariffs are going to dampen economic activity and, with that, inflation pressures.

As to the US, with President Trump having announced another wave of tariffs yesterday, as the 90-day window closed, once again the analyst community is calling for inflation to rise here. Ironically, these analysts may be correct that US inflation is going to be slowly heading higher, but whether that is due to tariffs, or perhaps the fact that more than ample liquidity remains in the economy and services prices continue to rise has yet to be determined.

At this point, I think it might be useful to break out an updated version of a chart that has made the rounds before showing price changes since 2000 broken down by categories. Virtually every sector that has seen significant price rises is on the service side of the ledger while most goods saw either deflation or very modest (~1% per annum) inflation.

Housing, which is both a good and a service, and textbooks, which are directly linked to tuition, are the two outliers. Now, many will complain that something like New Cars having risen only 24.7% since 2000 is crazy given their much higher sticker prices, and that is clearly hedonic adjustments doing its job. But if you consider the key expenses in your life, housing, food and health care are generally top of the requirements. It is abundantly clear from this chart that the American angst on prices is well founded. With that in mind, tariffs are exclusively imposed on goods, not services, so given services represent 77.6% of the US economy as of 2022 (as per Grok), the inflationary impact of tariffs seems like it might not be quite as high as the hysteria indicates.

(This is a perfect time to remind you of a great way to manage your inflation risk if you participate in the cryptocurrency markets by buying USDi, the only fully backed inflation tracking coin available. Learn more at www.usdi.com. It is essentially inflation-linked cash.)

Coming back around to the market, I think it is a good time to review one of the other major narrative themes, that the dollar is collapsing as foreigners flee because of the massive debt load, and that the dollar will soon lose its reserve status. You know I have dismissed this idea from the beginning as nothing more than doom porn and an effort by some analysts to get clicks.

There is no doubt that there had been a downtrend in the dollar for the first six months of 2025, and as has been written repeatedly, the decline was the largest during the first half of the year since the 1980’s. As well, my concern over the dollar has been based on the idea that the Fed would indeed be cutting rates despite no need to do so, and that would undermine its yield advantage. But a funny thing happened on the way to the death of the dollar, it stopped falling. While I have been using the DXY chart as my proxy, pretty much every chart looks the same as per the below of both the euro and yen, where the nadir was at the beginning of July and the dollar has risen vs. both somewhere between 3% and 5%.

Source: tradingeconomics.com

In fact, as I look down my board, the dollar has risen against every major currency over the past month, with even tightly controlled CNY declining -0.8%, and the yen falling furthest, down nearly -5.0%. Combine this with the news that Treasury auctions have been well attended with significant foreign interest, and it is hard to conclude the end is nigh for the US economy.

Ok, a really quick turn to markets here as this has gone on longer than I expected. Equities are red everywhere this morning after yesterday’s US declines. Japan (-0.7%), China (-0.5%) after weak PMI data, Hong Kong (-1.1%) and Australia (-0.9%) set the tone for Asia. In Europe, it is even worse with the CAC (-2.2%) and DAX (-1.9%) both under more pressure as a combination of increased worries over trade (although given they ostensibly have a deal, I’m not sure what the issue is) and companies there reporting weaker than forecast results have been the problem. US futures at this hour (7:30) are all pointing lower by about -0.85%.

Despite the fear in stocks, bonds are not seen as the answer this morning with Treasury yields edging higher by 1bp and European sovereign yields all higher by between 3bps and 5bps. I guess the inflation reading has a few traders nervous. Interestingly, if you look at the ECB’s own website showing rate change probabilities, there is a 14% probability of a rate HIKE priced in for the September meeting! JGB yields have also edged higher by 1bp as the BOJ, in their policy briefing yesterday, raised their inflation forecasts for 2026, ostensibly as a precursor to the next rate hike there. I’ll believe it when I see it!

As to commodities, oil (-1.1%) after touching $70/bbl yesterday has rejected the level. While secondary sanctions on Russian oil exports continue to be discussed, they have not yet been implemented. I continue to believe the price ought to be lower, but clearly there is a risk premium for now. In the metals markets, gold (+0.4%) continues to find support despite weakness in other markets (Ag -0.6%, Cu -0.9%) as its millennia-long status as the only true safe haven is reasserting itself. After all, Bitcoin (-0.6%) has not been able to match the relic’s performance of late despite its modern twist.

And that’s really all there is (I guess that’s enough) as we head into the weekend. The market tone will be set by the NFP data, where my take is a strong report will see the dollar rally, bonds suffer, and stocks suffer as well as hopes for a rate cut fade further. Conversely, a weak report should see the opposite impacts.

Last week Japan finally agreed To tariffs as they did concede Now Europe has folded Their cards as Trump molded A deal despite pundits’ long screed

So, now this week there’s lots of news That ought to give markets more cues Four central banks speak And late in the week Inflation and jobs we’ll peruse

All the talk this morning revolves around the announcement yesterday of a US-EU trade deal where the basics are a 15% tariff on all EU exports to the US and an EU promise to buy US energy and defense products totaling some $550 billion. Many have said that the agreement means nothing because for it to become law, it requires both the European parliament and each nation to vote to agree on the deal. As well, we are hearing from various nations how it is a terrible deal (French farmers are furious, German pharmaceutical manufacturers are furious and unions all over the continent are unhappy) and certain politicians (notably Marine Le Pen) are also extremely unhappy.

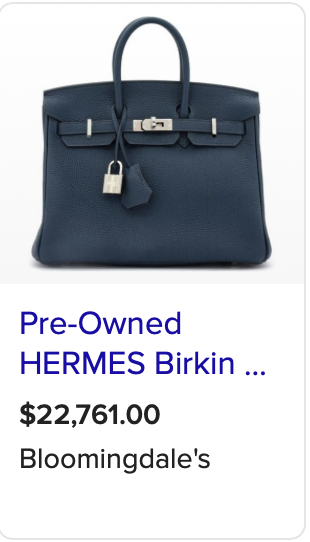

It is far too early to understand if the deal will be implemented in full, but the precedent has been set that European exports to the US are going to be subject to higher tariffs than any time since prior to WWI and that is true whether the deal is ratified or not. As analyst/trader Andreas Steno Larsen explained well this morning, “The EU vs. US trade deal highlights that the EU primarily exports ‘nice-to-have’ products rather than essential ‘need-to-have’ ones. And if you think about it, arguably the best-known EU companies are luxury goods makers, whether in fashion or autos. So, while there are women who swear they ‘need’ that Birkin bag, the reality is far different.

Expect to hear a lot more about this deal going forward, but the market response has been quite positive with European equity markets (IBEX +1.0%, FTSE MIB +0.9%, CAC +0.6%, DAX +0.4%) all higher along with US futures (+0.3%). Interestingly, Asian markets were mixed overnight as Japanese (-1.1%) and Indian (-0.7%) equities suffered, perhaps on the idea that their deals were no longer that special. China (+0.2%) and Hong Kong (+0.7%), though, did well amid news that another meeting was scheduled between the US and China, this time in Stockholm, to continue the trade dialog.

Away from the trade discussion, market focus this week is going to be on a significant amount of news and data to be released as follows:

Tuesday

Trade Balance

-$98.4B

Case Shiller Home Prices

3.0%

JOLTS Job Openings

7.55M

Consumer Confidence

95.8

Wednesday

ADP Employment

78K

Q2 GDP

2.4%

Treasury QRA

BOC Interest Rate Decision

2.75% (unchanged)

FOMC Interest Rate Decision

4.50% (unchanged)

Brazil Interest Rate Decision

15.0% (unchanged)

Thursday

BOJ Interest Rate Decision

0.50% (unchanged)

Initial Claims

224K

Continuing Claims

19660K

Personal Income

0.2%

Personal Spending

0.4%

PCE

0.3% (2.5% Y/Y)

Core PCE

0.3% (2.7% Y/Y)

Chicago PMI

42.0

Friday

Nonfarm Payrolls

102K

Private Payrolls

86K

Manufacturing Payrolls

0K

Unemployment Rate

4.2%

Average Hourly Earnings

0.3% (3.6% Y/Y)

Average Weekly Hours

34.2

Participation Rate

62.3%

ISM Manufacturing

49.6

ISM Prices Paid

66.5

Michigan Sentiment

61.8

Source: tradingeconomics.com

In addition to all of this, there are Eurozone GDP and inflation data, Japanese inflation data and PMI data from all around the world. Happily, there is virtually no central bank speaking beyond the post meeting press conferences as I presume all of them will be seeking an escape.

There is far too much data to discuss in any depth this morning, but my take is that President Trump has managed to move the Overton Window significantly over the course of his first 6 months in office. If you recall, it was on “Liberation Day” back in April, when he announced his reciprocal tariffs on the rest of the world, that the global economic community had a collective meltdown and proclaimed the end of the economy as we know it. Equity markets around the world plummeted and the future seemed bleak, at least according to every economist and pundit who could get their views heard. Now, here we are a bit more than three months later and tariffs of 15% on the entire EU as well as Japan, 10% on the UK and higher on other nations is seen as a solid outcome, sidestepping the worst cases promulgated, and the world is moving on.

It appears, at least for the moment, that Mr Trump understood that most nations need to export to the US more than the US needs to export to them. I would contend that is why these deals, which in many eyes seem unfavorable to the US counterparts, are being agreed. It is far too early to ascertain if things will work out as Trump expects, as the naysayers expect or somewhere in between (or entirely different) but thus far, you have to admit that the president has largely gotten his way.

So, as we open the week, we have already seen equity markets are generally in a positive mood. Bond markets are also behaving well, with Treasury yields edging higher by 1bp, still glued to that 4.40% level, while European sovereign yields have mostly slipped -2bps or so on the session. And last night, JGB yields fell -4bps. It appears that bond investors are not as concerned about the trade deals as some would have you believe.

In fact, the market with the biggest reaction overnight has been FX, where the dollar is showing strength against virtually all its counterparts in both G10 and EMG spaces. EUR (-0.8%) is the G10 laggard, although CHF (-0.8%) is right there with the single currency as clearly, Switzerland will be impacted by the EU tariff deal. But AUD (-0.6%), JPY (-0.5%) and SEK (-0.65%) are all under pressure as well as the DXY (+0.6%) continues its bounce.

Source: tradingeconomics.com

I continue to read about all the reasons why the dollar is losing its luster in the global community, because of tariffs, because of the Treasury’s actions freezing Russian assets after the invasion of Ukraine, because China and the BRICS are seeking other payment means to eliminate the dollar from their economies, because American exceptionalism is dead, and yet, while I am no market technician, I cannot help but look at the chart of the DXY above and see a broken downward trendline, indicating a move higher, and a bottoming in the moving average, also indicating further potential gains. I am confident that if the FOMC cuts rates (which full disclosure I don’t believe makes sense given the current amount of available liquidity and global equity market performance) that the dollar will decline further. But all those traders who are short dollars (and it is a very crowded position) are paying away between 25bps (long GBP) and 450bps (long CHF) on an annual basis so need to see the dollar’s previous downtrend resume pretty quickly. (see current overnight rates across major economies below from tradingeconomics.com)

The market is pricing just a 2% probability of a rate cut on Wednesday, and about 60% of a September cut. Unless this week’s data screams recession, I am having a hard time seeing the case for the dollar to fall much further, at least in the short and medium term. And this includes the fact that it is pretty clear President Trump would like to see a lower dollar to help US export competitiveness.

Finally, a look at commodities shows that while oil (+1.3%) is having a solid session, it remains in the middle of its trading range for the past several weeks. Meanwhile, metals prices (Au -0.1%, Ag -0.2%, Cu -0.4%) are feeling a little strain from the dollar’s strength but generally holding up well overall. Too, while there has historically been a strong negative correlation between the dollar and metals, given the large short dollar positions that are outstanding, it would not be hard to see both cohorts rally in sync for a while going forward.

And that’s really all for today. The data doesn’t really start until tomorrow, and as its summer, trading desks are already lightly staffed. Look for a quiet session today and the potential for choppiness this week if the data is away from expectations.

Though many conclude that recession Is coming, this poet’s impression Cannot overcome A key rule of thumb More jobs mean recession repression

As well, on the fourth of July The naysayers all went awry The BBB’s law As Trump oversaw Parades and a massive fly-by

I will be brief this morning. First, Thursday’s NFP report was much stronger than expected, with 147K new jobs and the Unemployment Rate falling to 4.1%. This is clearly not pointing in a recessionary direction, although as would be expected by all those who have made that call, there was much analysis about the underlying makeup of the jobs report, with more government hires and less private sector ones. And I agree, I would much rather see private sector hiring, but I don’t recall as much angst in the previous administration when they hired into the government extremely rapidly. It is difficult for me to look at the below chart of government hiring over the past five years and conclude that this administration is being anywhere nearly as profligate.

Source: tradingeconomics.com

Second, despite all the naysaying by the punditry, President Trump got his Big, Beautiful Bill through Congress and he was able to sign it on his schedule, July 4th. Whether you love Trump or hate him, you must admit that he is a remarkable political force, greater than any other president I can remember, although Mr Reagan was certainly able to accomplish many things with a very different style. And perhaps, that is the issue, Trump’s style is unique in our lifetimes as a president, although I understand that throughout our history, there have been some presidents with a similarly brash manner, I guess Andrew Jackson is the best known. And it is that style, I would say that leads to the Trump Derangement Syndrome, although his attack on the Washington elite is also a key driver there.

Thus far, the articles I have read about the legislation all focus on how many people are going to die because Medicaid is requiring able-bodied adults to work, volunteer or go to school 20 hours/week in order to remain eligible. It would be helpful if these ‘news’ sources could keep a running tally so we can all see the results. Given the law simply sets priorities, and not actual appropriations yet, my take is all this death and destruction may take a few months yet to materialize.

But after those two stories, there is a growing focus on the upcoming Tariff deadline this Wednesday, with a mix of views. There is both a growing concern that the original level of tariffs is going to be put back in place, and that will disrupt global commerce, and there is a story gaining traction that the deadline will be delayed again. The administration hinted there would be some notable deal signings this week, so we shall see.

As that’s all there is, let’s look at markets overnight. Thursday’s US rally in the wake of the NFP data is ancient history. Overnight in Asia, the major markets (Japan -0.6%, Hang Seng -0.1%, CSI 300 -0.4%) were under pressure but the rest of the region was mixed with some gainers (Korea, Indonesia, Singapore) and some laggards (Taiwan, Malaysia, Australia) although none of the movement was very large, 0.5% or less in either direction. In Europe this morning, the DAX (+0.65%) is far and away the leader after a stronger than expected IP reading of +1.2%. However, the rest of the continent and the UK are all tantamount to unchanged in the session. US futures at this hour (7:00) are pointing slightly lower, about -0.025%.

In the bond market, Treasury yields which rallied 5bps on Thursday after the data are higher by one more basis point this morning. European sovereign yields are all higher this morning as well, between 2bps and 3bps, as concerns over the timing of tariffs has investors cautious. The rumors are solid progress has been made in these negotiations.

In the commodity space, oil (+0.7%) is higher this morning which is a bit of a surprise given that OPEC+ raised their production quotas by a more than expected 548K barrels/day at their meeting this weekend. At this point, they are well on their way to eliminating those production cuts completely. I guess demand must be real despite the recession calls. Metals markets, though, are all lower this morning (Au -1.0%, Ag -2.0%, Cu -0.6%) as hopes for trade deals has reduced some haven demand. Of course, copper’s decline doesn’t jibe with oil’s rally on a demand note, but the movements have not been that large, so it is probably just random fluctuations.

Finally, the dollar is stronger this morning, which is also weighing on the metals markets. ZAR (-1.1%) is the biggest loser overnight although NZD (-0.9%) and AUD (-0.7%) are doing their best to catch up. But the euro (-0.35%) and pound (-0.3%) are both under pressure as is the yen (-0.7%) and CAD (-0.5%) and MXN (-0.5%). In other words, the dollar’s strength is quite broad-based. On this note, I couldn’t help but chuckle at this article in Bloomberg, Misfiring Models Leave Wall Street Currency Traders Flying Blind, which describes how all the old models no longer work in the current world. This is a theme I have harped on for a while, mostly with the Fed, but also with the punditry in general. The world today is a different place, and I might ascribe the biggest difference to the fact that for 20+ years, inflation had fallen to 2% or lower in most of the western world and markets behaved accordingly. But now, inflation is higher, and those relationships no longer hold.

On the data front, this may be the least active week I have ever seen.

Tuesday

NFIB Small Biz Optimism

98.7

Consumer Credit

$10.5B

Wednesday

FOMC Minutes

Thursday

Initial Claims

235K

Continuing Claims

1980K

Source: tradingeconomics.com

There are only 3 Fed speakers as well so pretty much, Washington is on vacation this week. It is very hard to get excited about much right now. We will all need to see the outcomes of the trade negotiations and which countries will see tariffs applied or not. I have no forecasts for any of that. In the meantime, I think the fact that implied volatilities are relatively low across most asset classes offers the opportunity for hedgers to protect themselves at reasonable prices.

According to those in the know The BBB’s ready to go The vote is this morning So, this is your warning That President Trump will soon crow

As well, ere the Fourth of July The NFP may quantify If rate cuts are coming (A subject, mind-numbing) Or whether Fed funds will stay high

Perhaps this will be the last day we hear about the Big Beautiful Bill, or at least the last day it leads the news, as it appears that by the time you read this, the House will have voted on the changes and by all accounts it is set to pass. If so, the President will sign it tomorrow amidst great fanfare and then it will just be a secondary story when somebody complains about something that was in the bill. However, the drama over passage will have finally ended.

(I guess what has really led the news was that Diddy was found not guilty of the RICO charges and Kohburger in Idaho got a plea deal avoiding the death penalty, but neither of those are market related.)

At any rate, the question now to be asked is will the BBB perform as advertised by either side of the aisle? Experience tells us that while the economy will not take off rapidly while inflation collpases, neither will there be people dropping in the streets because of the changes in Medicare, although if you listened to the pundits on both sides of the aisle, that is what you might expect. While this is not quite as bad as Nancy Pelosi’s immortal words, “we have to pass the bill to find out what’s inside it”, the fact that it approaches 1000 pages in length implies there is a lot inside it.

From what I have read, and it has not been extensive, it appears that there is some stimulus in the bill in the form of tax relief on tips and overtime as well as reductions for seniors, and spending on defense and the border. It also appears there have been several previous subsidies, notably for wind and solar, that are being removed. The fact that the CBO is claiming it will increase the budget deficit by $1.5 trillion, and given the fact that Jim Cramer is the only one with a worse track record than the CBO, tells me it will have limited impact on the nation’s fiscal stance initially, although if growth does pick up, that will clearly help things.

Which takes us to the other story this morning, the payroll report. Here are the current median forecasts by economists for the results, as well as the rest of the data to be released:

Nonfarm Payrolls

110K

Private Payrolls

105K

Manufacturing Payrolls

-5K

Unemployment Rate

4.3%

Average Hourly Earnings

0.3% (3.9% Y/Y)

Average Weekly Hours

34.3

Participation Rate

62.3%

Initial Claims

240K

Continuing Claims

1960K

ISM Services

50.5

Factory Orders

8.2%

-ex Transport

0.9%

Source: tradingeconomics.com

Some will point to yesterday’s ADP Employment report which showed a decline of -33K, the first decline in more than 2 years, as a harbinger of a bad number, but as you can see from the chart below, there has been a pretty big difference between ADP (grey bars) and NFP (blue bars) for a while now.

Source: tradingeconomics.com

Perhaps of more concern is the Unemployment Rate, which is forecast to rise a tick to 4.3%, which would be its highest print since October 2021 and if I look at the chart below, it is not hard to see a very gradual trend rising higher here. While markets really focus on NFP, I learned a long time ago from a very smart economist, Larry Kantor, that the Unemployment Rate was the best single indicator of economic activity in the US, and that when it is rising, that bodes ill for the future.

Source: tradingeconomics.com

You may recall there was a great deal of discussion about a year ago regarding the Sahm Rule, which hypothesized that when the Unemployment Rate rose more than 0.5% above its cycle average within 12 months, the US was already in a recession. The discussion centered on whether it had been triggered although the final claim was it hadn’t when extending the readings out to the second decimal place. Now, for the past year, the Unemployment Rate has hovered between 3.9% and 4.2%, so there doesn’t seem to be any chance of a trigger here, although if it does rise, you can be sure you will hear about it.

And that’s what is on tap ahead of the long holiday weekend. With that in mind, let’s look at the market action overnight. Excitement is clearly lacking in the equity markets these days as the summer doldrums are universal. Yesterday’s new closing highs in the S&P 500 seem like they should be exciting but were anything but amid low volume. As to Asia, Japan was flat, China (+0.6%) and Hong Kong (-0.6%) offset each other and in the rest of the region, other than Korea (+1.3%) which is starting to see a steady stream of foreign investment on the premise that the country is set to improve the regulatory structure for equities there, things were +/- a bit.

Meanwhile, in Europe, there is little net movement on the continent but the UK (+0.4%) is bouncing off recent lows after PM Starmer reiterated his support for Chancellor Reeves. A story I missed yesterday was that when she was trying to make a case in parliament for spending cuts, the back bench liberals revolted, literally bringing her to tears. The market response was that the UK would blow up its fiscal situation which saw Gilts tumble and yields rise 15bps yesterday at one point, while stocks fell. But that problem has been addressed for now. However, looking at the statement Starmer made, it reminded me of a baseball GM’s comments supporting his manager right before he fires him.

In the bond market, yields are declining, led by Gilts (-9bps) which are retracing yesterday’s gains on the above story. But Treasury yields are down (-2bps) and European sovereigns are all seeing yields lower by between -4bps and -5bps. In Japan, JGB yields are unchanged as PM Ishiba grapples with a trade deal where the US is keen to be able to export rice to the nation and Japan has a rice shortage with prices rising sharply but doesn’t want to accept imports. Go figure.

In the commodity markets, oil (-0.2%) is slipping slightly after a solid rally over the past seven sessions where it rose over $3.50/bbl. Gold (-0.3%) continues to trade around its pivot level of $3350/oz while silver (+1.0%) continues its longer run rally.

Finally, the dollar, which fell during yesterday’s session after I wrote, is effectively unchanged net this morning ahead of the data with very modest moves of +/-0.2% or less almost universal. KRW (+0.4%) is the outlier here and based on equity inflows discussed above, that makes sense.

So, that’s where we stand heading into the payroll report and the long weekend. If pressed on the NFP outcome, I expect a weak outcome, 50K or so, as the birth/death model continues to be revised. But remember, the error bars on this number are huge. However, if it is weak, look for the probability of a July rate cut (currently 25.3%) to rise and the equity market to follow that higher. As to the dollar, I think for now, lower is still the trend.

The Senate completed their vote And so, BBB, though there’s bloat Will soon become law As Dems say pshaw While lacking a doctrine, keynote

So, eyes now turn to NFP The key for the FOMC The JOLTs showed that gobs Of ‘vailable jobs Exist, though savants disagree

Market activity continues to demonstrate lower volumes and despite several competing political narratives, price action remains muted overall. The biggest news of late is the Senate passed their version of President Trump’s BBB last night and now it goes to committee for reconciliation before getting to the president for signing. Of course, given the mainstream media’s complete antagonism toward the president, the headlines this morning refer to the problems the Republicans will have agreeing terms between the two houses, and I’m sure it will be difficult. However, based on everything that President Trump has done to date, I expect it will get completed. While perhaps not by Friday, probably by next week.

This matters to markets because it will help set the tone for government spending and the potential companies that will benefit, as well as those that will be negatively impacted, based on the change in focus from that of the Biden administration.

At this point, it is impossible to forecast with any certainty how things will evolve, especially with respect to issues like the budget deficit and debt issuance. While yesterday, Treasury Secretary Bessent did explain that they were going to continue to focus on short-term issuance, if (and it’s a big if) the bill does goose economic activity in the US, it is quite possible that faster GDP growth increases tax collections and reduces net government spending and the deficit. I would estimate that view is not discounted at all in markets at this time given the constant messaging from media and the punditry that not only are people going to starve to death and lose their medical care because of this bill, but that it is unaffordable and will bankrupt the country. Something tells me the results will be slow acting, although if the government does continue its deportations and stops subsidizing too-expensive green energy projects, we could see less government spending. We shall see.

But markets need a focus and tomorrow’s NFP is as good as it gets. Chairman Powell has been attending the ECB’s summer symposium and, in his speech, yesterday he essentially reiterated his views that the Fed will continue to watch and wait on rates as there is still concern that tariffs may drive inflation higher. As to jobs, they are watching the situation closely, but thus far, the labor market has held up. Proof of that idea was evident in yesterday’s JOLTs Job Openings data which showed a surprising jump of more than 300K new job listings available. I haven’t seen a rationale yet, but perhaps it is related to the self-deportations by illegal immigrants who have left businesses with numerous vacancies. The weekly claims data, while above its lowest levels lately, continues to run at very modest numbers on a long-term perspective as can be seen in the chart below with data from the Department of Labor. If the job market holds up, I don’t see the Fed cutting rates despite President Trump’s ire.

Also, at Sintra was BOJ Governor Ueda who explained that Japanese policy rates were substantially lower than neutral and that inflation would likely continue creeping higher over time. I guess we cannot be surprised that the yen (-0.5%) has slipped in the wake of those comments. The final noteworthy comments from Sintra were from BOE governor Bailey who explained that despite sticky inflation, more rate cuts were on the way, helping to undermine the pound (-0.4%) this morning.

But there is one final thing to discuss regarding the Sintra meeting, and that is how many central bankers were suddenly concerned that their currencies were getting “too strong”! We have been hearing about the dollar’s decline in the first half of the year as though it was a signal the US was in permanent decline. Of course, given the nature of FX trading, a weaker dollar can also be seen as strength in other currencies. (To be clear, all fiat currencies continue to weaken vs. stuff as evidenced by the fact that inflation continues to be positive everywhere in the world, except perhaps Switzerland and China right now.) However, I could not help but laugh at the ECB comments from several board members, that if the euro were to rise any further it could become a problem for the Eurozone economies. All their models show that if a major export destination raises tariffs, their own currencies should decline to offset those tariffs. Alas, once again, their models are not giving them answers that reflect the reality in markets. And given Europe has built their economies on export reliance, a strong currency is a problem.

We must distinguish between a stronger exchange rate and a strong case to own a currency, especially as a reserve asset, but the two have historically been highly correlated. As I have repeatedly explained, the dollar’s decline this year is neither anomalous nor particularly large in the broad scheme of things. As well, it is exactly what the administration is seeking as it helps the competitiveness of US companies on the world stage. However, my take is that at some point soon, the dollar will find a bottom. I indicated a move to 90 on the DXY would be possible, and I think that is probably still true, although given the growing net short positions in USD vs. other currencies, the short squeeze will be spectacular when it arrives!

Ok, let’s see if we can get through the overnight activity without falling asleep. Yesterday’s mixed US session was followed by a mixed session in Asia (Nikkei -0.6%, Hang Seng +0.6%, CSI 300 0.0%) with a mixture of modest gains and losses across the rest of the region, all on low volumes. In Europe this morning, bourses are firmer led by the CAC (+1.1%) and Spain’s IBEX (+0.75%) as hopes for further rate cuts from the ECB dominate discussions. As to US futures, they are modestly higher at this hour (7:30), about 0.15%.

In the bond market, after stronger than expected JOLTs data and ISM data, yields are backing up with Treasuries (+4bps) leading the way although both Germany (+5bps) and the UK (+6bps) are seeing selling pressure as well. However, the rest of European sovereigns have only seen yields edge 1bp higher. The only noteworthy comments I saw were from the Italian FinMin who explained Italy would be maintaining its fiscal prudence. Not surprisingly, given Ueda-san’s comments, JGB yields rose 4bps overnight as well.

In the commodity space, oil (+1.25%) continues to drift higher as it tries to fill the gap seen last week.

Source: tradingeconomics.com

Apparently, the fact that supply seems to be rising rapidly has not dissuaded traders from the view that the ‘proper’ price range is $65-$75 rather than my belief of $50-$60. But right now, they are looking smart. In the metals markets, we continue to see support as the entire decline in the gold price at the end of June has been recouped and we are modestly higher this morning across all the metals (Au +0.1%, Ag +0.6%, Cu +0.4%, Pt +2.2%) with platinum merely showing its volatility due to lack of liquidity.

Finally, the dollar is firmer this morning against every one of its G10 and major EMG counterparts with the euro and pound (both -0.4% now) setting the tone. Perhaps the best performer this morning is INR (-0.1%) which seems to be benefitting from the news that a trade deal is almost complete there. As to trade with the Eurozone, that deal seems a bit further away, although I did see something about a European recognition that US tariffs would be, at a minimum, 10%. At least for today, I haven’t read anything about the dollar’s ultimate demise!

On the data front, today brings ADP Employment (exp 95K) and then the EIA oil inventory data. There are no Fed speakers either, so quite frankly, absent something newsworthy from DC, I suspect this will be a quiet session ahead of tomorrow’s NFP. I guess the dollar is not dead yet.

While jobs data Friday was fine The weekend has seen a decline In positive news As riots infuse LA with a new storyline

The protestors don’t like that ICE Is doing their job in a trice So, Trump played a card, The National Guard As markets search for the right price

Despite all the anxiety regarding the state of the economy, with, once again, survey data like ISM showing things are looking bad, the most important piece of hard data, the Unemployment report, continues to show that the job market is in solid shape. Friday’s NFP outcome of 139K was a few thousand more than forecast, but a lot more than the ADP result last Wednesday and much better than the ISM indices would have indicated. Earnings rose, and government jobs shrunk for the first time in far too long with the only real negative the fact that manufacturing payrolls fell -8K. But net, it is difficult to spin the data as anything other than better than expected. Not surprisingly, the result was a strong US equity performance and a massive decline in the bond market with 10-year yields jumping 10bps in minutes (see below).

Source: tradingeconomics.com

But that is not the story that people are discussing. Rather, the devolution of the situation in LA is the only story of note as ICE agents apparently carried out a series of court-warranted raids and those people affected took umbrage. The face-off escalated as calls for violence against ICE officers rose while the LAPD was apparently told to stand down by the mayor. President Trump called out the National Guard to protect the ICE agents and now we are at a point of both sides claiming the other side is acting illegally. Certainly, the photos of the situation seem like it is out of hand, reminding me of Minneapolis in the wake of George Floyd, but I am not on site and can make no claims in either direction.

It strikes me that for our purposes here, the question is how will this impact markets going forward. A case could be made that the unrest is symptomatic of the chaos that appears to be growing around several cities in the US and could be blamed for investors seeking to move their capital elsewhere, thus selling US assets and the dollar. Equally, a case could be made that haven assets remain in demand and while US equities do not fit that bill, Treasuries should. In that case, precious metals and bonds are going to be in demand. The one thing about which we can be sure is there will be lawsuits filed by Democratic governors against the federal government for overstepping their authority, but no injunctions have been issued yet.

However, let’s step back a few feet and see if we can appraise the broader situation. The US fiscal situation remains cloudy as the Senate wrangles over the Big Beautiful Bill (BBB), although I expect it will be passed in some form by the end of the month. The debt situation is not going to get any better in the near-term, although if the fiscal package can encourage faster nominal growth, it is possible to flatten the trajectory of that debt growth. Meanwhile, the tariff situation is also unclear as to its results, with no nations other than the UK having announced a deal yet, although the administration continues to promise a number are coming soon.

If I look at these issues, it is easy to grow concerned over the future. While it is not clear to me where in the world things are that much better, capital flows into the US could easily slow. Yet, domestically, one need only look at the consumer, which continues to buy a lot of stuff, and borrow to do it (Consumer Credit rose by $17.9B in April) and recognize that the slowdown, if it comes, will take time to arrive. Remember, too, that every government, everywhere, will always err on the side of reflating an economy to prevent economic weakness, and that means that the first cracks in the employment side could well lead to Fed cuts, and by extension more inflation. (This note by StoneX macro guru Vincent Deluard discussing the Cancellation of Recessions is a must read). I have spoken ad nauseum about the extraordinary amount of debt outstanding in the world, and how it will never be repaid. Thus, it will be refinanced and devalued by EVERY nation. The question is the relative pace of that adjustment. In fact, I would argue, that is both the great unknown, and the most important question.

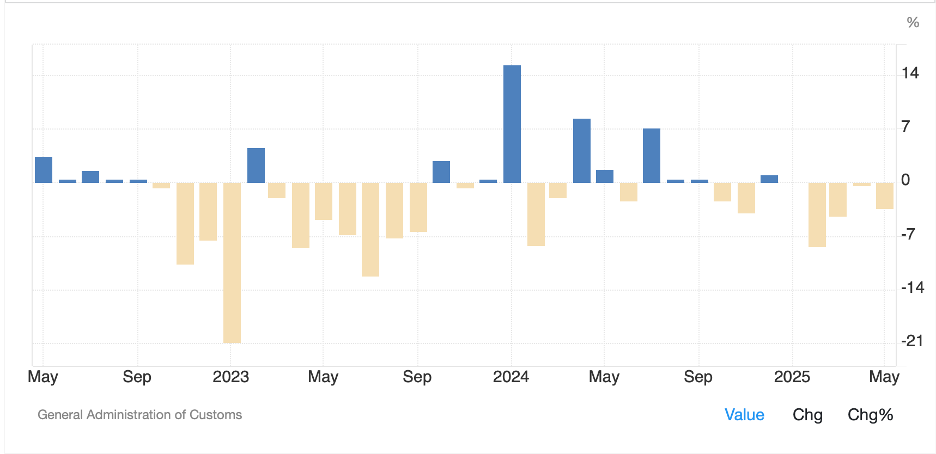

While answering this is impossible, a few observations from recent data are worth remembering. US economic activity, at least per the Atlanta Fed’s GDPNow continues to rebound dramatically from Q1 with a current reading of 3.8%. Meanwhile, Chinese trade data showed a dramatic decline in exports to the US (-35%) but an increased Trade Surplus of $103.2B as they shifted exports to other markets and more interestingly, imports declined-3.4%. in fact, it is difficult to look at this chart of Chinese imports over the past 3 years and walk away thinking that their economy is doing that well. Demand is clearly slowing to some extent, and while their Q1 GDP was robust, that appears to have been a response to the anticipated trade war. Do not be surprised to see Chinese GDP slowing more substantially in Q2 and beyond.

Source: tradingeconomics.com

Europe has been having a moment as investors listen to the promises of €1 trillion or more to build up their defense industries and flock to European defense companies that had been relatively cheap compared to their US counterparts. But as the continent continues to insist on energy suicide, the long-term prospects are suspect. Canada just promised to raise its defense spending to 2% of GDP, finally, a sign of yet more fiscal stimulus entering the market and the UK, while also on energy suicide watch, has seen its service sector hold up well.

The common thread, which will be exacerbated by the BBB, is that more fiscal spending, and therefore increased debt are the future. Which nation is best placed to handle that increase? Despite everything that you might believe is going wrong in the US, ultimately the economic dynamism that exists in the US surpasses that of every other major nation/bloc. I still fear that the Fed is going to cut rates, drive inflation higher and undermine the dollar before the year is over, but in the medium term, no other nation appears to have the combination of skills and political will to do anything other than what they have been doing already. And that is why the long-term picture in the US remains the most enticing. This is not to say that US asset prices will improve in a straight line higher, just that the broad direction remains clear, at least to me.

Ok, I went on way too long, sorry. As there is no US data until Wednesday’s CPI, we will ignore that for now. A market recap is as follows: Asia had a broadly stronger session with Japan, China, HK, Korea and India all following in the US footsteps from Friday and showing solid gains. Europe, though, is mostly in the red with only Spain’s 0.25% gain the outlier amongst major markets. As to US futures, they are essentially unchanged at this hour (7:00).

Treasury yields have backed off -2bps from Friday’s sharp climb and European sovereign yields are softer by between -3bps and -4bps as although there has been no European data released; the discussion continues as to how much the ECB is going to cut rates going forward. JGB yields were unchanged overnight.

In the commodity space, while oil (+0.3%), gold (+0.1%) and even silver (+0.8%) are edging higher, platinum has become the new darling of speculators with a 2.8% climb overnight that has taken it up more than 13.5% in the past week and 35% YTD. Remarkably, it is still priced about one-third of gold, although there are those who believe that is set to change dramatically. A quick look at the chart below does offer the possibility of a break above current levels opening the door to a virtual doubling of the price. And in this environment, a run at the February 2008 all-time highs seems possible.

Finally, the dollar is softer across the board this morning, against virtually all its G10 and EMG counterparts. AUD (+0.55%) and NZD (+0.7%) are leading the way, but the yen (+0.5%) is having a solid session as are the euro and pound, both higher by 0.25%. In the emerging markets, PLN (+0.7%) is the leader with the bulk of the rest of the space higher by between +0.2% and +0.4%. BRL (-0.3%) is the outlier this morning, but that looks much more like a modest retracement of recent gains than a new story.

Absent both data and any Fedspeak (the quiet period started on Friday), we are left to our own devices. My take is there are still an equal number of analysts who are confident a recession is around the corner as those who believe one will be avoided. After reading the Deluard piece above, I am coming down on the side of no recession, at least not in a classical sense, as no politician anywhere can withstand the pain, at least not in the G10 and China. That tells me that while Europe may be the equity flavor of the moment, commodities remain the best bet as they are undervalued overall, and all that debt and new money will continue to devalue fiat currencies.

The feud between Elon and Trump Show’s Musk has become a mugwump But though there’s much drama It’s not clear there’s trauma As markets continue to pump

So, turning our eyes toward today’s Report about jobs, let’s appraise The call for recession That’s been an obsession Of some for six months of Sundays

Clearly the big headlines are all about the escalating war of words between President Trump and Elon Musk. I guess it was inevitable that two men with immense wealth and power would ultimately have to demonstrate that one of them was king. But other than the initial impact on Tesla’s stock price, it is not clear to me what the market impacts are going to be here. After all, President Trump has attacked others aggressively in the past when they didn’t toe his line, and it is not a general market problem, only potentially the company with which that person is associated. As such, I don’t think this is the place to hash out the issue.

However, I think it is worth addressing one point that Musk raised regarding the Big Beautiful Bill. The thing about reconciliation is it only addresses non-discretionary spending, meaning Social Security, Medicare, Medicaid and the interest on the debt. All the other stuff that DOGE made headlines for, USAID etc., could never be part of this bill. That requires recission packages where Congress specifically passes laws rescinding the previously enacted payments. So, if this was a part of the blowup, it was senseless. I will say, though, that the Trump administration did not communicate this fact effectively as I read all over how people are upset that Congress is not addressing these other things. At any rate, this is not a political commentary, but I thought it was worth understanding because I only learned of this in the past weeks and I don’t believe it is widely understood.

Onward to the major market news today, the payroll report. As of this morning, according to tradingeconomics.com, here are the forecast outcomes:

Nonfarm Payrolls

130K

Private Payrolls

120K

Manufacturing Payrolls

-1K

Unemployment Rate

4.2%

Average Hourly Earnings

0.3% (3.7% Y/Y)

Average Weekly Hours

34.3

Participation Rate

62.6%

Of course, Wednesday’s ADP Employment number was MUCH lower than expected, so the whispers appear to be for a smaller outcome. As well, the key wildcard in this data is the BLS Birth-Death model which is how the BLS estimates the number of jobs that have been created by small businesses which aren’t surveyed directly. As with every model, especially post-Covid, what used to be is not necessarily what currently is. The most accurate, after the fact, representation of employment is the Quarterly Census of Employment and Wages (QCEW) but that isn’t released until 6 months after the quarter it is addressing, so it is not much of a timing tool. It is also the genesis of all the revisions.

Here’s the thing, a look at the chart below shows that the BLS Birth-Death model appears to still be substantially overstating the payroll situation. Given the datedness of its model, that cannot be a real surprise, but I assure you, if there is a major revision lower in that number, and NFP prints negative, it WILL be a surprise to markets. I am not forecasting such an occurrence, merely highlighting the risk.

If that were to be the case, I imagine the market reaction would be quite negative for stocks and the dollar, positive for bonds (lower yields) and likely continue to push precious metals higher, although oil would likely suffer. I guess we will all have to wait and see at 8:30 how things go.

In the meantime, ahead of the weekend, let’s see how markets behaved overnight. Yesterday’s modest sell-off in the US was followed by a mixed session in Asia (Nikkei +0.5%, Hang Seng -0.5%, CSI 300 -0.1%) but strength in Korea (+1.5%) and India (+0.9%). Trade discussions still hang over the market and there are increasing bets that both India and Korea are going to be amongst the first to come to the table. As well, the RBI cut rates by 50bps last night with the market only expecting 25bps, so that clearly supported the SENSEX. In Europe, no major index has moved even 0.2% in either direction as positive European GDP data was unable to get people excited and there is now talk that the ECB will not cut rates again until September. As to US futures, at this hour (6:50) they are pointing higher by about 0.3% across the board. It appears that the Tesla fears are abating.

In the bond market, yields continue to slide with Treasuries falling -1bp and European sovereign yields down between -3bps and -5bps despite the stronger than expected Eurozone data which also included Retail Sales (+2.3%) growing more rapidly than expected. But this is a global trend as recession discussions increase while we also saw JGB yields slip -2bps overnight. It feels like the bond markets around the world are anticipating much slower economic activity.

In the commodity space, oil (0.0%) is unchanged this morning and continuing to hang around at its recent highs, but unable to break above that $63+ level. It strikes me that if slower economic activity is on the horizon, that should push oil prices lower as there appears to be ample supply. But I read that Spain has stopped importing Venezuelan crude as US secondary sanctions are about to come into effect there. As to the metals markets, silver (+1.5%) and platinum (+2.6%) have been the leaders for the past few sessions although gold (+0.2%) continues to grind higher. The loser here has been copper (-0.8%) which if the economic forecasts of slowing growth are correct, makes some sense. Of course, there is a strong underlying narrative about insufficient copper supplies for the electrification of everything, but right now, payroll concerns are the story.

Finally, the dollar is a bit firmer this morning, but only just, with G10 currencies slipping between -0.2% and -0.3% while EMG currencies have shown even less movement. INR (+0.25%) stands out for being the only currency strengthening vs. the dollar after the rate cut and positive growth story, but otherwise, this is a market waiting for its next cue.

In addition to the payroll report, we get Consumer Credit (exp $10.85B) a number which gets little attention but may grow in importance if economic activity does start to decline. As well, I cannot ignore yesterday’s Trade data which saw the deficit fall much more than expected, to -$61.6B, its smallest outturn since September 2023. While I didn’t see any White House comments on the subject, I expect that President Trump is happy about that number.

Are we headed into a recession or not? Will today’s data give us a stronger sense of that? These are the questions that we hope to answer later this morning. FWIW, which is probably not that much, my take is while economic activity has likely slowed a bit, I do not believe a recession is upon us, and as I do believe the reconciliation bill will be passed which extends the tax cuts, as well as adds a few like no tax on tips or Social Security, I expect that will turn any weakness around quickly. What does that mean for the dollar? Right now, it is piling up haters so a further decline is possible, but I cannot rule out a reversal if/when the tax legislation is finalized.

The calendar’s not e’en turned twice Since Trump, with JD as his Vice Have taken the reins And beat up on Keynes While weeding out waste in a trice

For markets, the problem, it seems Is rallies are now merely dreams So, equity buyers Are putting out fires While thinking up pump and dump schemes

For bondholders, it’s not so clear If salvation truly is near But one thing seems sure The buck will endure Much weakness throughout this whole year

We have not even reached 50 days of a Trump presidency as of this morning and nobody would fault you if you estimated we had three years of policies enacted to date. The pace of changes has been blistering and clearly most politicians, let alone investors, have not been prepared for all that has occurred.

One of the things that I read regularly is that Trump is destroying the Rules Based Order (RBO) which was underpinned by the Pax Americana of the US essentially being the world’s policeman. This is cast as a distinct negative under the premise that things were going great and now, he is upsetting the applecart for his own personal reasons. Of course, market participants had grown quite accustomed to this framework, had built all sorts of models to profit from it and with the Fed’s help of monetization of debt, were able to gain significantly at the expense of those without market linked assets. Hence, the K-shaped recovery.

But while that is a lovely narrative, is it really an accurate representation of the way of the world? If the US was truly the world’s policeman, and we certainly spend enough on defense to earn that title, perhaps it was time for the US to be fired from that role anyway. After all, there is currently raging military conflict in Ukraine, Lebanon, Syria, Congo, Sudan and the ongoing tensions in Gaza. That’s a pretty long list of wars to claim that things were going great.

Secondly, the question of financing all this conflagration, as well as other economic goals, notably the alleged transition to net zero carbon energy production, appears to be reaching the end of the line. While the US can still borrow as needed, (assuming the debt ceiling is raised), the reality is that the US gross national debt outstanding is greater than $36,000,000,000,000 relative to GDP that is a touch under $28,000,000,000,000. On a global basis, total (not just government) debt is in excess of $300,000,000,000,000 while global GDP clocks in somewhere just north of $100,000,000,000,000. Arguably, on a credit metric basis, the world is BB- or B+, a clear indication that all that debt is unlikely to be repaid.

If we consider things considering this information, perhaps the RBO had outlived its usefulness. Arguably, the loudest complaints are coming from those who benefitted most greatly and are quite unhappy to see things change against them. But as evidenced by the polls taken after President Trump’s speech last Tuesday evening, the bulk of the American public is still strongly supporting this agenda. The idea that the president and his Treasury secretary are seeking to engineer a short-term recession early, blame it on fixing Biden’s mess, and having things revert to stronger growth in time for the 2026 mid-term elections is not crazy. In fact, there have been several comments from both men that short-term pain would be necessary to achieve a stabler, long-term gain.

So, what does this mean for the markets? You have no doubt already recognized that volatility is the main event in every market, and I don’t see that changing anytime soon. But some of the themes that follow this agenda would be for US equities to suffer relative to other markets, as the last decade plus of American exceptionalism, led by massive deficit spending and borrowing, would reverse under this new thesis. Add to this the sudden realization that other nations are going to be investing significantly more in their own defense, and money will be flowing out of the US into Europe, Japan and emerging markets around the world.

Bonds are a tougher call as a weaker economy would ordinarily mean lower yields, but the question of tariff impacts on prices, as well as reshoring, which, by definition, will raise prices, could mean we see the yield curve steepen with the Fed cutting rates more aggressively than currently priced, but 10-year and 30-year yields staying right where they are now.

I believe this will be a strong period for commodities as all that foreign capex will be a driver, as will the fact that, as I will discuss shortly, the dollar is likely to underperform significantly. Gold will retain its haven characteristics as well as remain in demand for foreign central banks, while industrial metals should hold their own. As to oil, my take is lower initially, as OPEC returns its production and slowing GDP weighs on demand, at least for a while, although eventually, I suspect it will rebound along with economic activity.

Finally, the dollar will remain under significant pressure across the board. Clearly, Trump is seeking a weaker dollar to help the export industries, as well as discourage imports. Add to this the potential for lower yields, lower short-term rates, and an exit of equity investors as US stocks underperform, and you have the making of at least another 15% decline in the greenback this year.

With this as backdrop, we need to touch on three key stories this morning. First, Friday’s NFP report was pretty much in line with expectations at the headline level but seemed a bit weaker in some of the underlying bits, specifically in the Household Survey where a total of 588K jobs were lost and there was a large increase in the number of part-time workers doing so for economic reasons. Basically, that means they wanted full-time work but couldn’t find a job. Markets gyrated after the release, with yields initially sliding but then rebounding to close higher on the day. Equities, too, closed higher on the day although that had the earmarks of a relief rally after a lousy week overall. The thing about this report is that it did not include any of the government changes that have been in the press, so next month may offer more information regarding the impact of DOGE and their cuts.

The second story comes from north of the border where Mark Carney, former BOC and BOE head, was elected to lead the Labour Party in Canada and replace Justin Trudeau. As is always the case, when there is new leadership, there is excitement and he said he will call for a general election in the next several weeks, ostensibly to take advantage of this new momentum. It seems that President Trump’s derision of not only Trudeau, but Canada as well in many Canadian’s eyes, will play a large role with the two lead candidates, Carney and Poilievre, fighting to explain that they are each better placed to go toe-to-toe with Trump on critical issues.

Here’s the thing, though. Despite much angst about the US-Canada relationship on the Canadian side of the border, the market viewpoint is nothing has really changed. a look at the chart below shows that after a bout of weakness for the Loonie in the wake of the US election and leading up to Trump’s tariff announcements, USDCAD is basically unchanged since mid-December, with one day showing a spike and reversal in early February. My point is that the market has not, at least not yet, determined that the Canadian PM matters very much.

Source: tradingecoomics.com

The last story to discuss is Chinese inflation data which was released Saturday evening in the US and showed deflation in February (-0.7% Y/Y) for CPI and continuing deflation in PPI (-2.2%). In fact, as you can see from the below chart, PPI in China has been in deflation for several years now. Recently there have been several articles explaining this offers President Xi a great opportunity for significant stimulus because no matter how much the government spends and how much debt they monetize, inflation won’t be a problem for a long time to come. I would counter that given deflation has been the norm for several years, they have had this opportunity for quite a while and done nothing with it. Why will this time be different? Ultimately, the default result in China is when things are not looking like they will achieve the targeted growth of “about 5%”, you can be sure there will be more investment to build things up adding still more downward pressure on prices as production facilities increase.

Source: tradingeconomics.com

The renminbi’s response to this news has been modest, at best, with a tiny decline overnight of -0.25%. And a look at the chart there shows it is remarkably similar to the CAD, with steady weakness through December and then no real movement since then. Given the dollar’s recent weakness overall, this seems unusual. Although, we also know that China prefers a weaker currency to help support their export industries, so perhaps this in not unusual at all.

Source: tradingeconomics.com

Ok, this note is already overly long, so will end it here. We do have important data later this week with both CPI and Retail Sales coming. As well, the consensus from the Fedspeak is that they are pretty happy right here and not planning to do anything for a while.

The big picture is best summarized, I believe, by the idea that we are at the beginnings of a regime change in markets as discussed above. Volatility continues to be the driving force, so hedging remains crucial for those with natural exposures.

Investors have been inundated By news that has been unabated There’s tariffs and war Plus rate cuts and more With stocks and bonds depreciated

Now looking ahead to today The payroll report’s on its way As well, later on With nothing foregone We’ll hear from our own Chairman Jay

It has certainly been an interesting week in both markets and the world writ large. So much has happened and yet so much is still unclear as to how things may evolve going forward. Through it all, volatility is the only constant. To me, what has become abundantly clear is the post WWII order is being dismantled, and every nation is trying to determine its place in the future. This is a grave threat to those who benefitted from flowery words and limited action, which covers a wide swath of government leaders around the world. I’m not sure if this is the 4th Turning, or if this is merely the prelude, with the impacts of all these changes what brings the 4thTurning about. Regardless, history is clearly in the making.

I do not have the bandwidth to continuously follow the tariff story, although yesterday’s news was there will be more delays for both Canada and Mexico. China received no such relief and at their National People’s Congress they seemed resolute in their pushback and highlighted their own achievements. The data from China, though, tells me that their goals for more domestic consumption remain far in the distance. Last night they reported their Trade Balance for the January/February period (they always combine because of the Lunar New year disruptions) and it jumped to $170.5B, far greater than anticipated. While exports underperformed slightly, growing only 2.3% compared to a 5% estimate, it was the imports that really tells the story. Imports fell -8.4%, a significant shortfall from both last year and consensus estimates, and an indication that the Chinese consumer is not yet the type of force that President Xi would like to see.

In fact, a look at the chart below showing imports for the past 10 years demonstrates that very little has changed on this front. As I wrote yesterday, converting a mercantilist economy into a consumer-focused one is a huge lift, and one that the CCP has not yet figured out. It is not clear that they ever will. Meanwhile, the obvious explanation for the huge jump in the trade balance was companies pre-ordering things to get ahead of the tariffs.

Source: tradingeconomics.com

Moving on to the Ukraine situation, while yesterday’s news was of the “whatever it takes” moment for defending Europe, this morning it seems there are some caveats attached. Of course, the first caveat is the changing of the German constitution to allow them to spend all that money. The second seems to be that not every European nation is on board for the massive spending increase and continuation of the war. There are many political and financial hurdles to overcome in this story in Europe, and this morning’s European equity markets are indicative of the idea that this is not a straight-line higher. In fact, every equity market in Europe is lower this morning, led by the DAX (-1.5%) although with solid declines elsewhere as well (CAC -1.0%, FTSE 100 -0.5%). This, too, is a story with no clear end in sight. One unconfirmed story I saw was that the group convened by the UK last weekend has not been able to agree terms for additional support.

Meanwhile, yesterday the ECB cut their short-term rates by 25bps, as widely expected, with the Deposit Rate now down to 2.50%. The funny thing is nobody really noticed. This is of a piece with my observation that central bankers just don’t have that much sway on market activity these days, it is all about politics and statecraft, not monetary policy. This morning, Eurozone GDP for Q4 was released at 0.2%, a tick higher than forecast but still lower than Q3’s 0.4%. There is no doubt the financial mandarins of Europe are keen to get this defense spending going, because otherwise they will continue to preside over a stagnant economy.

But here’s an interesting thing to consider. Germany has made a big deal about this new willingness to spend €500 billion outside the bounds of their budget framework on defense. However, they continue with their Energiewende policy which has been the Achilles Heel of the German economy and will prevent them from actually producing armaments if they seek to continuously reduce fossil fuel powered energy for renewables. It is almost as if this is theater, rather than policy, but that may just be my cynicism speaking.

Moving on to the US, this morning brings the Payroll Report with the following current median estimates:

Nonfarm Payrolls

160K

Private Payrolls

111K

Manufacturing Payrolls

5K

Unemployment Rate

4.0%

Average Hourly Earnings

0.3% (4.1% Y/Y)

Average Weekly Hours

34.2

Participation Rate

62.6%

Source: tradingeconomics.com

As well, we hear from Chairman Powell at 12:30pm, along with Bowman, Williams and Kugler in the hours leading up to that. But again, I ask, do they matter to the markets right now? Certainly, there is much discussion that the US economic data is starting to show more weakness, and there are many who are saying that long-anticipated recession is going to become evident. If that is the case, we could certainly see the Fed cut rates, but again, my take is markets are far more attuned to 10-year yields than Fed funds. And remember, while 10-year yields are clearly quite inflation sensitive, what we also know that questions over budget deficits and supply are critical to their pricing as well. This was made evident yesterday in Germany.

I have glossed over market activity overnight so will give a really short update here. Yesterday’s weakness in the US was followed by broad weakness throughout Asia, with most markets there lower on the day, notably Japan (-2.2%), but declines almost everywhere. We have already discussed European bourses and at this hour (7:30) US futures are basically unchanged ahead of the data.

In the bond market, Treasury yields are slipping back -3bps this morning and we are seeing similar price action across most of Europe although Spain (+1bp) is bucking the trend on some domestic issues. It is easy to believe that the Germany story was a bit overblown, and remember, if they cannot change the constitution, I expect a rally in Bunds (lower yields) along with a selloff in the DAX and the euro.

Speaking of the euro, it is continuing its sharp ascent, up another 0.6% this morning. however, something to keep in mind regarding all the huffing and puffing about the euro is that with this sharp move higher in the past week, it is merely back to the middle of its 3-year trading range. So, is this as big a deal as some are saying?

Source: tradingeconomics.com

But the overall currency picture is more mixed with both AUD (-0.6%) and NZD (-0.5%) lower along with CAD (-0.2%). There are other gainers (GBP +0.2%, SEK +0.7%) and other laggards (ZAR -0.2%) although I would say the broad direction is still for dollar weakness.

Finally, oil (+1.5%) is bouncing this morning, although this could well be a trading bounce as I have seen no new news on the subject. I guess the delay on Canadian tariffs probably played a role as well. Gold (+0.4%) is also firmer although both silver (-0.4%) and copper (-1.2%) are lagging. In fairness, the latter two have had significant up weeks so are likely seeing some profit taking.

Once again, I will remark that for those who have real flows and exposures, the current market situation is why hedging is critical to maintain financial performance. Nobody really knows where anything is going to go, but right now, it feels like the one thing we know is prices will not remain where they currently are for very long.