Two things have been talk of the town

First, silver ne’er seems to go down

But also, of late

The Dow’s in a state

Where it wears the daily stock crown

But if we dig deeper, we find

Industrials, as they’re defined

Don’t build many things

Instead, they pull strings

As finance and tech are combined

Before I start, this will be the last poetry of 2025. I want to thank all my readers for continuing to read and I certainly hope I both amused you and highlighted one view of what is driving the zeitgeist in markets these days. FX poetry will return on January 5th with my annual long-form poetic prognostications. Merry Christmas, Happy Chanukkah and Happy New Year to you all.

So, I was reading my friend JJ’s evening wrap up from yesterday and he highlighted the fact that the DJIA (+1.3%) made a new all-time high in trading and it was led by…Goldman Sachs.

Source: tradingeconomics.com

Now, I have nothing against Goldman Sachs, per se, but it struck me as odd that Goldman Sachs, an investment bank, was a member of the Dow Jones Industrial Average. It’s not that I wasn’t aware of the fact, but for some reason, this mention stuck out. So, I thought I might look at the current membership of the Dow and see just how industrial it is.

While you will likely not be surprised that it has several non-industrial, service-based companies in the index, you might be surprised by just how many. For instance, aside from Goldman, JPMorgan, American Express and Visa are in there as well as United Health and Travelers from the insurance space. There are major retailers like Walmart, Home Depot, Amazon and McDonalds, along with tech and telecom/media names like Microsoft, Salesforce, Disney and Verizon.

This is not to say that these are misplaced with respect to their relative importance in the US economy, clearly all are major corporations with long histories of profitability. But it seems odd to list them as industrial. I would contend that nothing explains the financialization of the US economy better than the fact that 14 out of the 30 members of the DJIA are service companies rather than producers of stuff. Maybe they should rename it the Dow Jones Major Corporate Index.

To conclude the equity portion of our discussion, yesterday saw the NASDAQ (-0.25%) decline in the face of a broad overall equity rally as there appears to be a rotation of investors from AI into other things like financials (as hopes of another Fed rate cut spring eternal) and power producers as the power needs of AI keep getting estimated ever higher. This rally was followed pretty much everywhere around the world as regardless of one’s religion, it appears investors are all counting on Santa to deliver higher prices. In Asia, Tokyo (+1.4%). HK (+1.75%), China (+0.6%), Australia (+1.2%), Korea (+1.4%) and virtually every other market rallied. The only data of note here was Japanese IP which came in a tick higher than its preliminary forecast, but to counter that, Nikkei reported that the BOJ, when they meet next week, are definitely going to raise the base rate by 25bps to 0.75%, the highest level since 1994. That doesn’t seem that bullish, but then, I’m not Japanese.

In Europe, the gains are also universal, albeit less impressive with Spain (+0.5%) and France (+0.5%) leading the way and Germany and the UK both only marginally higher. The most interesting news here is about the EU’s efforts to confiscatethe Russian assets that have been frozen since they invaded Ukraine, but which are being blocked by Belgium where they reside under SWIFT. And as I type (7:45) US futures are mixed with the Dow (+0.2%) still in favor while NASDAQ (-0.5%) continues to lag.

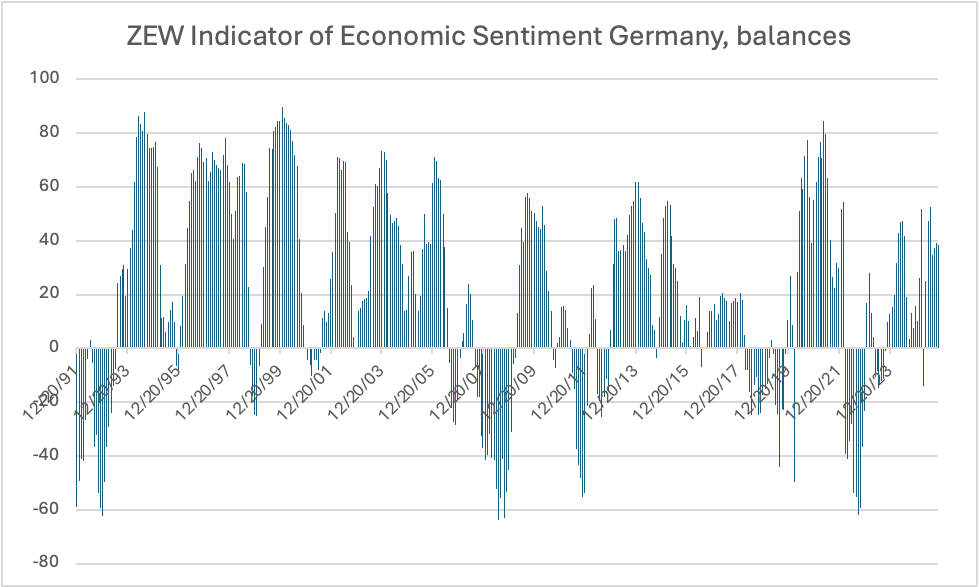

But the other story that is getting press, and arguably more press, is precious metals. Silver (+0.9% today, +10% this week, +122% this year) is the leader and is now trading above $64/oz. This is the very definition of a parabolic move, which is obvious when you look at the silver chart for the past 5 years.

Source: tradingeconomics.com

Referring back to JJ’s note, it is important to understand he is a commodity trader of long standing (remarkably even longer than my time in FX) and he discussed silver from an insider’s perspective. The essence of the issue here is that there are quite a few paper short positions that have existed for a long time. The rumor has long been that JPMorgan has been preventing silver from rising by playing in futures markets. But now, real demand, between industrial users (solar panels and electronics) and Asian retail demand from both India and China is far higher than new supply or recovery from scrap, to the tune of 120 million oz/year, and those shorts cannot find the metal to deliver. The last time there was a squeeze, when the Hunt’s tried to corner the market in 1980, people lined up at stores to sell their silver tea services, bringing metal to the market. But those are all gone. I’m not sure what will change this in the short run, but it cannot go up forever. With that in mind, though, I think precious metals have much further to run as the ongoing debasement of fiat currencies simply adds further to demand.

Silver managed to drag gold (+1.1% today, +3.0% this week, +65% this year) and platinum (+3.6% today, +7.2% this week, +98% this year) along for the ride and I expect this will continue across the board. Meanwhile oil (0.0%) is unchanged this morning but has fallen -4.0% this week. The news that the US boarded a Venezuelan oil tanker and took control in an effort to pressure Maduro didn’t seem to concern anyone in the market. This trend remains clear.

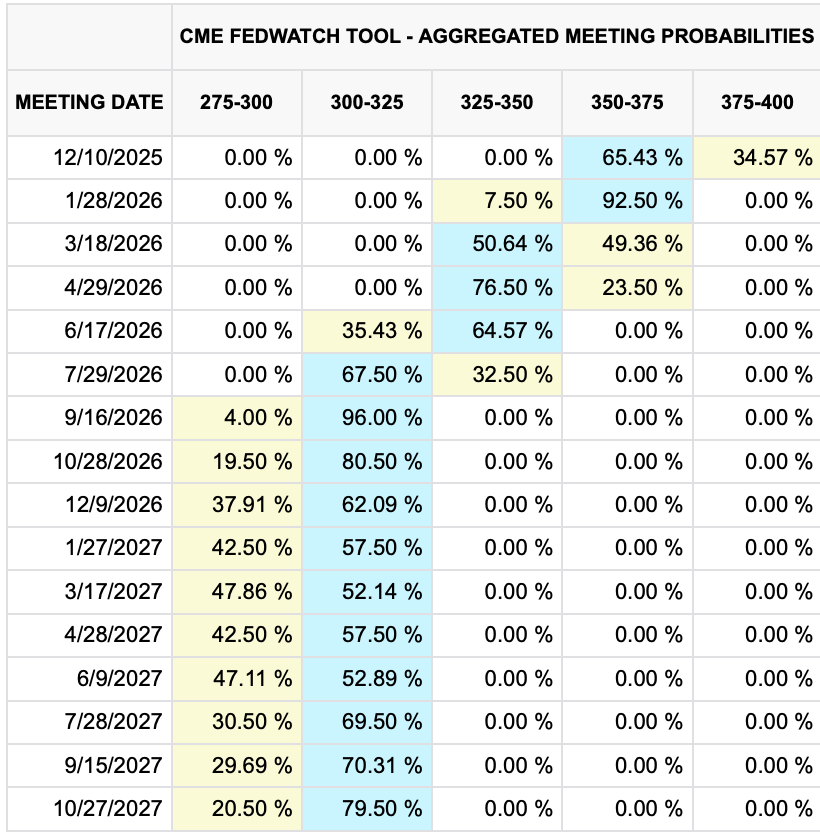

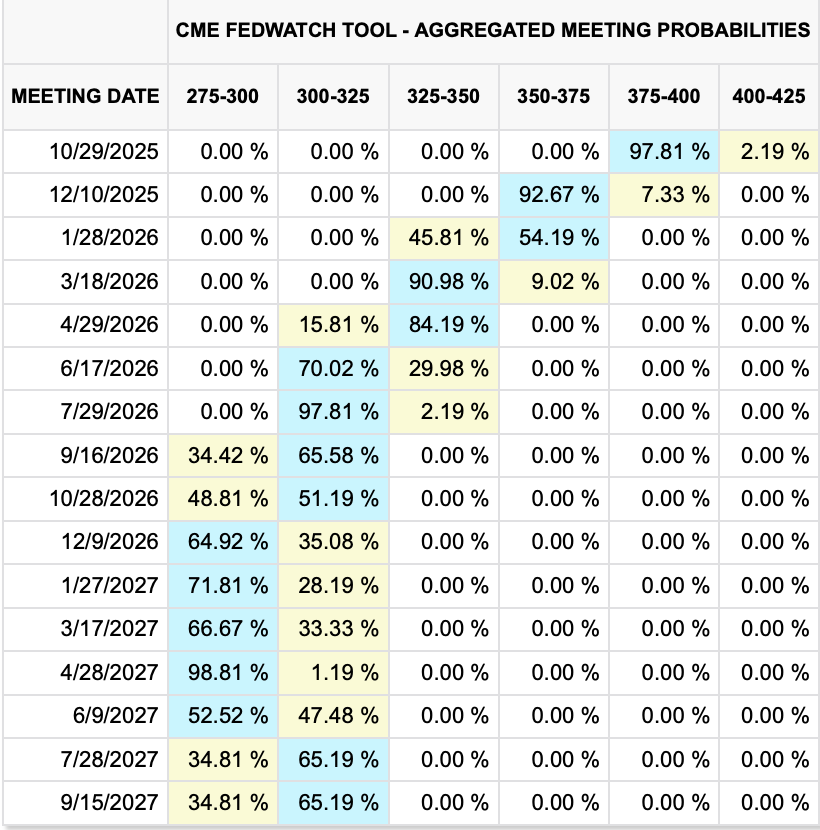

As to the bond market, this morning yields are higher by 2bps, pretty much across the board of Treasuries and all European sovereigns. But with that in mind, the 10-year Treasury is still yielding 4.18%, below its worst level immediately following the FOMC meeting, and as I mentioned above, there appears to be a growing belief that Powell’s concern about the labor market will result in more cuts sooner rather than later. While that is not really playing out in the futures market yet, as you can see below with the next cut priced for April with a 76% probability, that is the narrative that is being promulgated in FinX.

Source: cmegroup.com

Next week we will get the November NFP report (exp 35K) and all the data we missed in October. I can assure you if that comes in weak, the idea of a rate cut will explode onto the scene once again. Too, on Wednesday evening, the WSJpublished an article indicating that Chairman Powell is concerned the employment data is overstating things because of the flaws in the birth/death model. The point is he may be far more inclined to cut if next Tuesday’s report is weak.

Finally, the dollar is…still here. It sold off after the Fed, and as I showed yesterday, has fallen back to the middle of its trading range of the past 6 months. I keep reading how the dollar is the key, but quite frankly, I’m not certain what that key will unlock. We need out of consensus activities to change the current situation. After all, the underlying demand for dollars because of the trillions of dollars of debt outstanding outside of the US makes it difficult to get too bearish without a major reason. If the Fed cut 50bps intermeeting, that would do it, but I’m not holding my breath.

And that’s really it my friends. There is no data today although we do hear from three Fed speakers. Given the dissent on the FOMC, I expect that we are going to be need to keep score as to views for a while when these folks speak.

In the meantime, as I said above, have a wonderful holiday all

Adf