The Chinese have not finished yet

Their efforts to counter the threat

Of weaker stock prices

Which seems like a crisis

So new triple R rates were set

But one thing I don’t understand

Is while CCP’s in command

Just why do they care

‘Bout stocks anywhere

Perhaps communism ain’t grand

Yesterday, the Chinese government announced that there would be up to CNY 2 trillion of support for Chinese equity markets in their latest effort to stanch the 3-year bear market. But apparently, that was not enough as last night Pan Gongsheng, the PBOC governor, announced they were reducing the Reserve Requirement Ratio (RRR or triple R) in order to free up additional loan capacity for the banks. The move, a 0.50% cut in the ratio will ostensibly release another CNY 1 trillion into the economy.

There are two issues I’d like to address here. First, given the property market in China remains under significant pressure as activity still seems to be lethargic, at best, and the economy overall is not really expanding at a significant pace, why do they think that allowing more loans will encourage people to take more loans. After all, last week, they left the Loan Prime Rates unchanged, so were not trying to encourage more activity, and it is not clear that loan capacity has been a constraint in any manner during the past several years. As global growth remains slow overall, it is entirely possible, if not likely, that there is just reduced demand for Chinese manufactures around the world right now.

The second issue is a bigger picture question, why does the Chinese Communist Party care at all about the stock market? After all, a reading of Das Kapital would explain that there is no place for private ownership at all in a communist system and by extension, no place for shareholders. The state is supposed to own everything. My conclusion is that Xi, and the entire CCP, are full of s*it regarding their belief in communism. In fact, I would contend that is true for every communist regime on the planet. Rather, those in charge in communist regimes merely see it as the most effective way to command all the power and wealth personally and could care less about the concepts Marx espoused. In the end, I would argue that the human condition is one where acquiring as much power and wealth as possible is the driving goal for most people. While many people have much smaller ambitions, the sociopaths who rise to leadership roles in politics know no bounds as to what they believe is their due. Just sayin!

Regardless of the underlying rationale, though, the PBOC had the desired impact as both the Hang Seng (+3.6%) and the CSI 300 (+1.4%) rallied sharply on the news. As well, the Nikkei (-0.8%) slid a bit further as it seems there had been a growing position by CTAs and hedge funds in the long Japan/short China trade which I illustrated yesterday. If China is rebounding, I expect that Japanese shares will have further to slide in the near-term. As well, after another day with some record high closings in the US yesterday, European bourses are all in the green nicely this morning with the DAX (+1.3%) leading the way although the other main indices are also higher by about 1%. The laggard here is the UK (+0.4%) and I attribute this movement to the Flash PMI data which was released this morning showing that continental growth continues to slide, hence increasing the chance of a rate cut sooner, while UK data was a bit better than expected, and well above 50 across the board, implying the BOE will lag any rate cuts going forward. And happily, as I type at 8:00, US futures are all nicely in the green as well.

In the bond market, Treasury yields are a touch softer this morning, down 2bps, but still hanging right around the 4.10% level which has been a pivot for the past week. European sovereigns have seen yields decline about 3bps across the board after that soft PMI data, while UK Gilts have moved the other direction on the stronger data there. Of more interest, I think, is that JGB yields have jumped 5bps overnight and are now back above 0.70%. It seems that there is an evolution in thinking regarding Ueda-san’s comments after the BOJ meeting Monday night, and the belief that they will be exiting NIRP in April is growing stronger. We shall see.

Commodity prices are higher across the board this morning with oil (+0.3%) continuing to find support, arguably from the troubles in the Middle East, although some short-term issues like the shuttering of a Russian export terminal after a Ukrainian attack have also had an impact. But metals markets are universally higher this morning as well, with gold (+0.25%) far less impressive than copper (+2.0%) or aluminum (+0.9%) as positivity from the Chinese RRR cut and the potential for stronger growth on the mainland feed through the markets.

Finally, the dollar is under pressure this morning across the board. This is true in the G10 bloc with the euro and pound both firmer by 0.5%, while the yen (+0.8%) and CHF (+0.8%) are having even better days. Similarly, the EMG bloc has seen gains across the board with the leader ZAR (+1.1%) on the back of those metals gains, but strength in PLN (+0.8%), CZK (+0.7%) and HUF (+0.65%) showing their high beta with respect to the euro, and gains in APAC currencies (KRW +0.4%, SGD +0.3%, CNY +0.3%) and LATAM currencies (MXN +0.6%, BRL +0.8%) as it is unanimous regarding the dollar’s weakness.

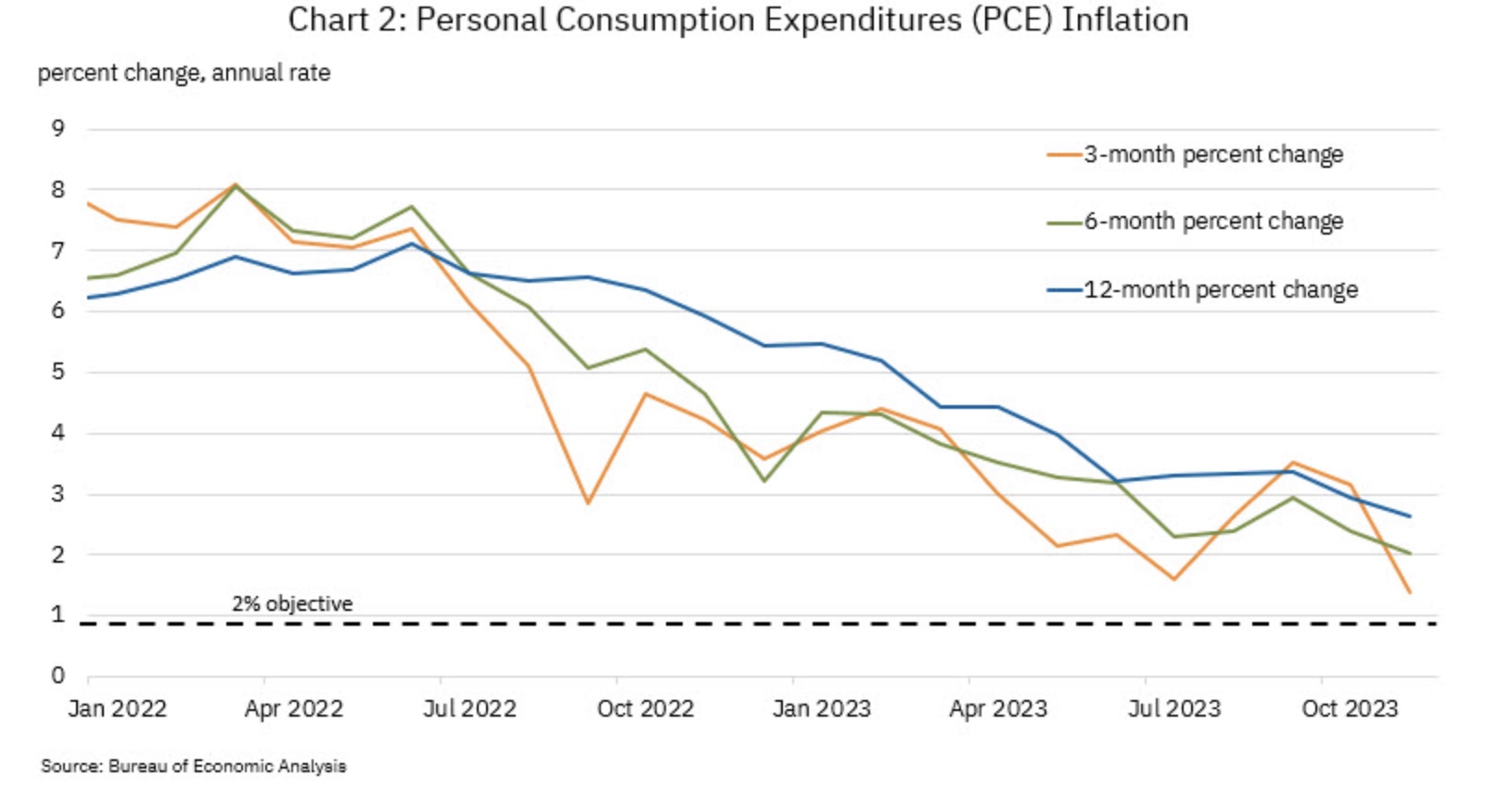

On the data front, today brings only the Flash PMI data (exp 47.9 manufacturing, 51.0 services) and the EIA oil inventories. There are no Fed speakers due to the quiet period, so I foresee market activity focused on equity earnings releases although none of the big names are due today. Right now, the dollar is under pressure amid ongoing belief that the Fed is going to cut ahead of other central banks. Until that story changes, I expect that we could see a bit more dollar weakness. But in the end, tomorrow’s GDP and Friday’s PCE data are going to really drive views. Look for a quiet one today.

Good luck

Adf