Though troubles worldwide haven’t ceased

Investors continue to feast

On assets with risk

As if they’re crab bisque

And appetites all have increased

Perhaps they believe peace is near

Or maybe they’re just cavalier

‘Cause Bitcoin has rallied

And profits they’ve tallied

Convinced them they’ll have a great year

This poet is a bit confused this morning as I watch ongoing record high equity markets in the US and elsewhere indicate a bright future, but I continue to read about the problems around the world, specifically in Ukraine and Gaza, but also throughout Africa, as well as the apparent end of democracy in the US. Though it is showing my age, I recall during the Reagan presidency, equity markets performed well amid a sense that the world was going in the right direction. The Cold War ended and Fed Chair Volcker had shown he had what it took to fight inflation effectively. This combination was very effective at brightening one’s outlook on the future.

Then, leading up to the dotcom bubble, attitudes were also remarkably positive as the future held so many possibilities while peace had largely broken out around the world. Again, the rally albeit overdone, at least had a basis that combined financial hopes with a positive geopolitical background. Of course, the events of 9/11 put the kibosh on that for quite a while.

Leading up to the GFC, though, I would contend that the zeitgeist was a bit different, and while housing markets were on fire, the geopolitical picture was far less rosy with Russia reasserting itself and taking its first piece of Ukraine, the Middle East situation much dicier with the ongoing military action in Iraq and Afghanistan, and China beginning to flex its muscles in the South China Sea.

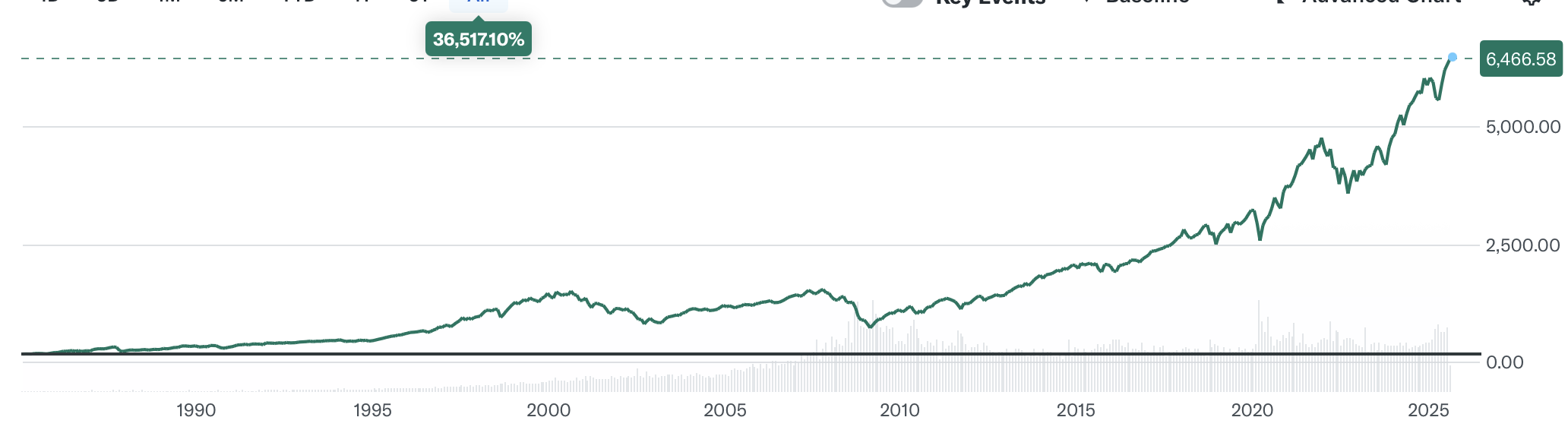

Of course, the similarity to these times is they all ended with significant equity market declines and resets of attitudes, at least for a while as per the below chart of the S&P 500. Of course, given the exponential move over time, the early dips don’t seem so large today, although I assure you, on October 19, 1987, when the DJIA fell 22.6%, it seemed pretty consequential on the trading desk.

Source: finance.yahoo.com

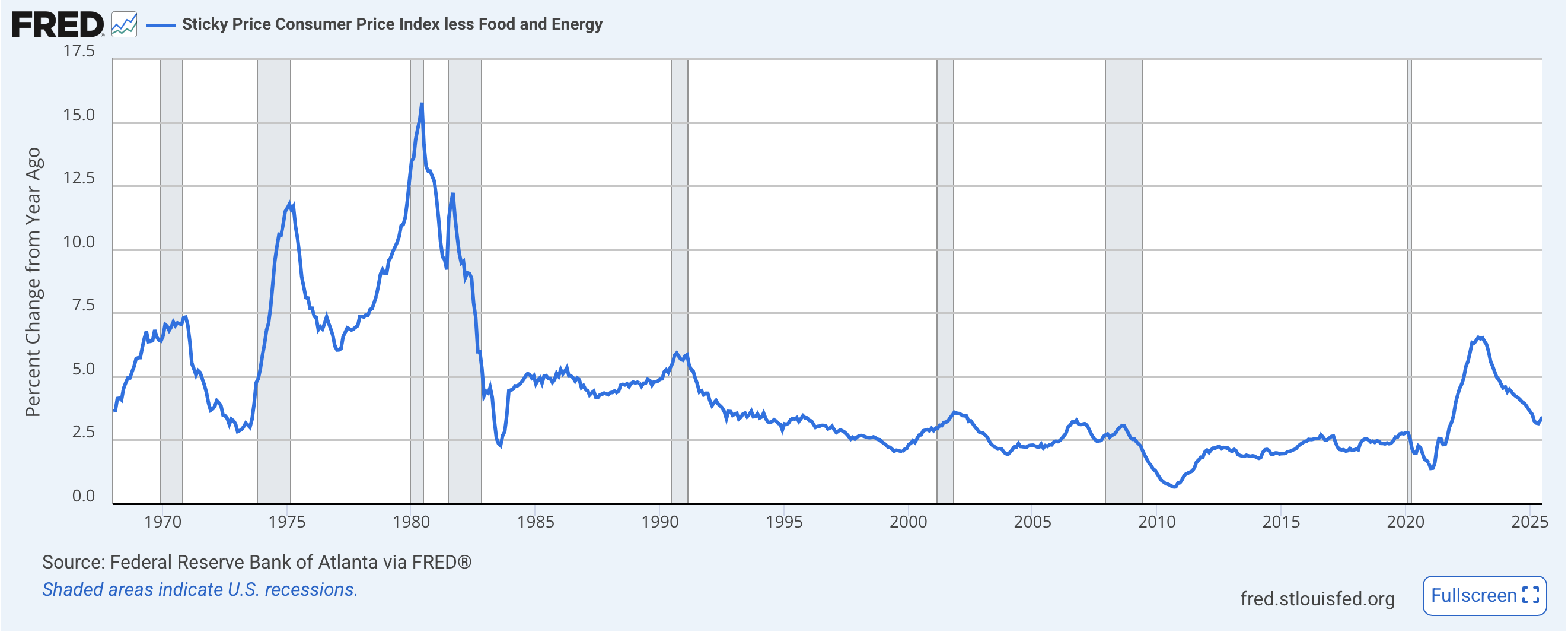

But today, I find the disconnect between market behavior and global happenings far harder to understand. Yes, there is a prospect that Presidents Trump and Putin will agree a ceasefire tomorrow when they meet in Alaska, although I’m not holding my breath for that. At the same time, President Trump is doing his best to reorder the global economic framework, and doing a pretty good job of it, but causing significant dislocations around the world with respect to trade and finance. Too, through all the other bubbles, consumer price inflation was not a concern of note, with CPI remaining quiescent throughout until the Covid response as per the below and, as Tuesday’s core CPI reminded us, inflation remains a specter behind all our activities.

And yet, all-time highs are the norm in markets these days, whether US equities, Japanese equities, European equities, Bitcoin or gold, prices for financial assets remain in the uppermost percentiles of their historic ranges. Perhaps this is the YOLO view of life, or perhaps markets are telling us the technology futurists are correct, and AI will bring so much benefit to mankind that everything will be better. Or…maybe this is simply the latest bubble in financial markets, and that permanently high plateau for asset values, as Irving Fisher explained in October 1929, is once more a mirage. Is the value of Nvidia, at $4.466 trillion, really greater than the economic output of every nation on earth other than the US, China and Germany? It is a comparison of this nature that has me concerned over the short- and medium-term prospects, I must admit.

However, the valuations are what they are regardless of any logic or financial comparisons. If the Fed cuts 50bps in September, which as of now would be a huge surprise to markets based on pricing, would that really increase the value of these companies by that much? Perhaps, as frequently has been the case, Shakespeare was correct and “something is rotten in the state of Denmark.” Care must be taken with regard to owning risk assets I believe, as a correction of some magnitude seems a viable outcome by the end of the year. At least to my eyes. Just not today.

Today, this is what we’ve seen in the wake of yesterday’s ongoing US equity rally. Tokyo (-1.45%) slipped on what certainly looked like profit-taking after reaching new highs. China was little changed but Hong Kong (-0.4%) fell ahead of concerns over Chinese data due this evening and the idea it may not be as strong as forecast. As to the rest of the region, the larger exchanges, Korea and India, were little changed and the smaller ones were mixed, all +/- 0.5%. In Europe, gains are the order of the day, at least on the continent (DAX +0.5%, CAC +0.35%, IBEX +0.8%) although the FTSE 100 (0.0%) is struggling after mixed data showing stronger than expected GDP but much weaker than expected Business Investment boding ill for the future. As to US futures, they are little changed at this hour (7:30).

In the bond markets, Treasury yields (-3bps) continue to grind lower as comments from Treasury Secretary Bessent have encouraged investors that interest rates will be declining across the curve. Teffifyingly, there is a story that President Trump is considering Janet Yellen as the next Fed Chair, something I sincerely hope is a hoax. European sovereign yields are lower by -1bp across the board but JGB yields (+3bps) are rising after Bessent basically said in an interview that the Japanese needed to raise rates to support the yen!

In commodities, oil (+0.4%) is stabilizing after several days of modest declines, but the trend of late remains lower. If peace breaks out in Ukraine, I suspect the price will have further to fall as the next step will be the reduction or ending of sanctions on Russian oil. Meanwhile, the metals markets are little changed to slightly softer this morning after a modest rally yesterday as a stronger dollar and a general lack of interest are evident.

As to that dollar, only the yen (+0.4%) is bucking the trend of a stronger dollar today although the pound is unchanged after the data dump there. But the rest of the G10 is weaker by between -0.2% and -0.4% which is also a pretty good description of the EMG bloc, softer by those amounts. It’s funny, once again this morning I read some comments about how the dollar’s decline in the first half of this year, where it has fallen about -10%, is the largest since the 1970’s, as though the timing within the calendar is an important part of the dollar’s value. While I would guess that Bessent is conflicted to some extent, I believe the administration is perfectly happy with a decline in the dollar if it helps US export competitiveness as long as inflation remains under control. Of course, that is the $64 thousand (trillion?) dollar question.

On the data front, this morning brings the weekly Initial (exp 228K) and Continuing (1960K) Claims as well as PPI (Headline 0.2%, 2.5% Y/Y and Core 0.2%, 2.9% Y/Y). I always find that there is less interest in PPI when it is released after CPI, but a surprise, especially a hot surprise, could well impact some views. Once again, we hear from Richmond Fed president Barkin, although so far all he has told us is he is the quintessential two-handed economist, so I’m not expecting anything new here.

Personally, I am getting uncomfortable with equity market valuations and levels based on the rest of the things ongoing and sense a correction in the offing. As to the dollar, I suspect if I am correct, the dollar will benefit alongside bonds. Otherwise, the summer doldrums seem likely to describe the day.

Good luck

Adf