Three score and a year have now passed

Since flags in the States flew half-mast

In honor of Jack

Who wouldn’t backtrack

On his goal of world peace at last

It has been sixty-one years since President John F Kennedy was assassinated in Dallas. This was one of the most dramatic and impactful events in the history of the US with many still of the belief that it was an inside job. One needn’t wear a tin-foil hat all the time to recognize that the government has done nothing but grow dramatically since then, with the defense complex the leader of the pack. Perhaps in his second term, President Trump will release the case files in an effort to shine a light on the underbelly of the government. This poet has no idea what occurred that day (although I did recently visit the 6th floor museum in Dallas, a quite interesting place) and I would guess that all these years later, there are very few, if any, people who may have been involved that are still alive. Of course, the risk is that powerful organizations like the CIA and FBI could be forever tarred with this if they were involved, and that would have dramatic implications going forward, hence their desire to maintain secrecy. I highlight this simply as another potential flashpoint in the upcoming Trump presidency.

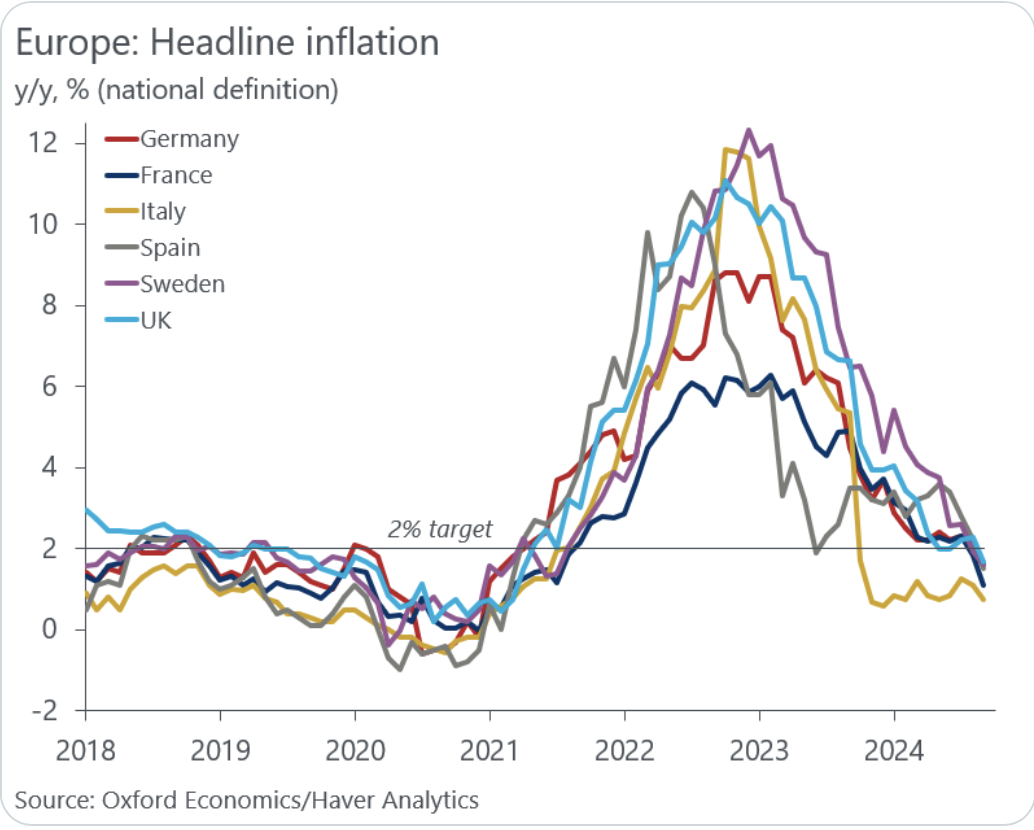

The data from Europe revealed

That if there is growth, it’s concealed

The PMI’s sank

And German growth stank

Thus Christine, her razor, will wield

Let us now discuss the Eurozone. Not only do they have an increasingly hot war on their border and not only are they being inundated by a major blizzard interrupting power and transportation throughout France, Germany and Scandinavia, but their economies appear to be slowing down far more rapidly than previously anticipated. But that inflation was slowing as quickly!

This morning the Flash PMI data was released for Germany, France and the Eurozone as a whole, as well as the UK. It did not make for happy reading if you are a politician or policymaker in any of these nations.

| Indicator | Current | Previous |

| Germany | ||

| Manufacturing PMI | 43.2 | 43.0 |

| Services PMI | 49.4 | 51.6 |

| Composite PMI | 47.3 | 48.6 |

| France | ||

| Manufacturing PMI | 43.2 | 44.5 |

| Services PMI | 45.7 | 49.2 |

| Composite PMI | 44.8 | 48.1 |

| Eurozone | ||

| Manufacturing PMI | 45.2 | 46.0 |

| Services PMI | 49.2 | 51.6 |

| Composite PMI | 48.1 | 50.0 |

| UK | ||

| Manufacturing PMI | 48.6 | 49.9 |

| Services PMI | 50.0 | 52.0 |

| Composite PMI | 49.9 | 51.6 |

Source: tradingeconomics.com

One needn’t look too hard to see that the economic situation in Europe is ebbing toward a recession or at least toward much slower growth (German GDP was also released at a slower than expected 0.1% Q/Q, -0.3% Y/Y). While the ECB is very aware of this situation, the problem is that like most other central banks, their strong belief that inflation is going to reach their 2.0% goal has not yet been realized let alone shown an ability to stay at that level over time. However, the ongoing comments from ECB members is that more rate cuts are coming with only the timing and size in question. There is still a strong belief that interest rates in Europe (and the UK) are well above ‘neutral’.

Of course, it will not surprise you to see the chart of the EURUSD exchange rate given this information as the single currency collapses continues its sharp decline.

Source: tradingeconomics.com

Since the end of September, the single currency has declined ~7.0% in a quite steady fashion. All the technical levels that had been in play have been broken with the next noteworthy level to consider being parity. I have been clear for a while that I expected the dollar to continue to perform well and nothing has changed that view. The combination of an increase in fear amid the escalation of tensions in Ukraine and Russia’s intimation that the US and NATO have entered the war already and the very divergent paths of the US and Eurozone economies can only lead to the conclusion that the euro is going to continue to decline for a while. And remember, this price action has very little to do with potential Trump tariff or other policies as they remain highly uncertain. The euro is simply a victim of its own leaders’ ineptitude on both the economic and diplomatic/military fronts. Any Trump tariffs that are imposed on Europe will simply add to the pain.

Before we head to other asset classes, let’s take a quick look beyond the euro in the FX markets. It should be no surprise that the dollar is broadly higher, although not universally so. Versus the rest of the G10, even the yen has not been able to find enough haven demand to hold up as the greenback rallies against them all with the euro (-0.6%) and pound (-0.6%) sharing honors as the laggards. However, in the EMG bloc, the picture is more mixed with CE4 currencies all sliding but ZAR (+0.4%) rallying amid the ongoing rebound in the price of gold (+1.2%) which is also benefitting from increased fear and risk disposition. As to Asian currencies, most were somewhat weaker but other than KRW (-0.4%) the moves were unimpressive.

On the commodity front, oil (-0.6%) is slipping a bit heading into the weekend but it has had an excellent week, rallying more than 4%. There are many cross tensions in this market as on one side we have fears that the Russia/Ukraine situation will impact supply, or that Iran will react to Israel’s ongoing campaign in Lebanon and do something about the Strait of Hormuz. These are obviously bullish for crude. But the flip side is that Trump has made very clear his desire to open up far more land for drilling and is seeking to increase supply substantially, a negative price signal.

Turning to bond markets, there is demand everywhere as the combination of risk aversion and weaker Eurozone growth have brought the buyers out of the woodwork. Treasury yields have slipped -4bps and in Europe, the entire continent is seeing yields decline between -7bps and. -8bps. After the PMI data this morning, the Euribor futures market upped pricing for a December ECB rate cut from a 15% to a 50% probability. Add to that comments from ECB members Stournaras and Guindos and it seems quite likely that rates in Europe are going to decline.

Finally, equity markets have shown very little consistency. Yesterday’s strong US rally was followed by strength in Japan (+0.7%) but massive weakness in China (CSI 300 -3.1%, Hang Seng -1.9%) as concerns over those Trump tariffs continue to weigh on investors there. However, it was only China that suffered as pretty much every other market in the region saw gains, with some (India +2.55, Taiwan +1.6%, New Zealand +2.1%) quite substantial. European shares, however, are more mixed with most continental bourses showing modest declines although the UK (+0.8%) has managed to buck that trend despite the weak PMI data and weak Retail Sales data as investors seem to be prepping for a BOE rate cut next month. As to US futures, at this hour (7:30) they are little changed.

Yesterday’s data showed Initial Claims sliding but Continuing Claims rising to their highest level, above 1.9M, in three years. It appears that while layoffs aren’t increasing, finding a job once you are unemployed is much tougher. Philly Fed was also softer than forecast and that seemed to help the Fed funds futures market push up the probability of a December cut to 59% this morning, up from 55% yesterday. This morning, we see the Flash PMI data here (exp Mfg 48.5, Services 55.0) and then Michigan Sentiment (73.7). There are no Fed speakers on the schedule so I expect that this morning’s trends may run for a little longer, but as it is Friday, I would not be surprised to see a little reversal amid week ending profit taking. However, the dollar has further to go, mark my words.

Good luck and good weekend

Adf