The British inflation release Showed prices did not quite increase As much as expected Though still they’re projected To stay at a level, obese But truly, all eyes have now turned To Jay, when past two, we’ll have learned If hawks rule the roost Or if doves seduced The Chairman with more rate hikes spurned

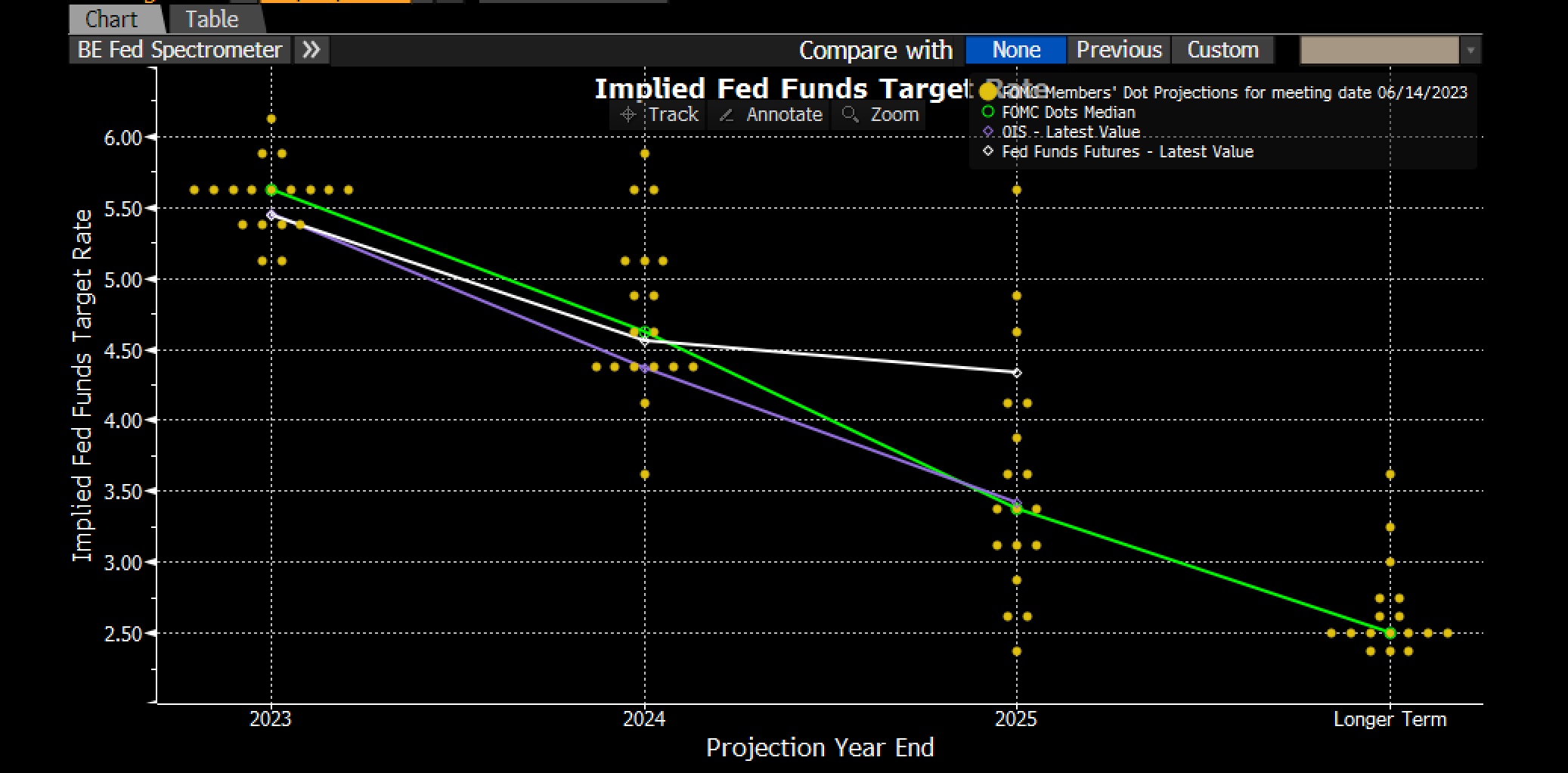

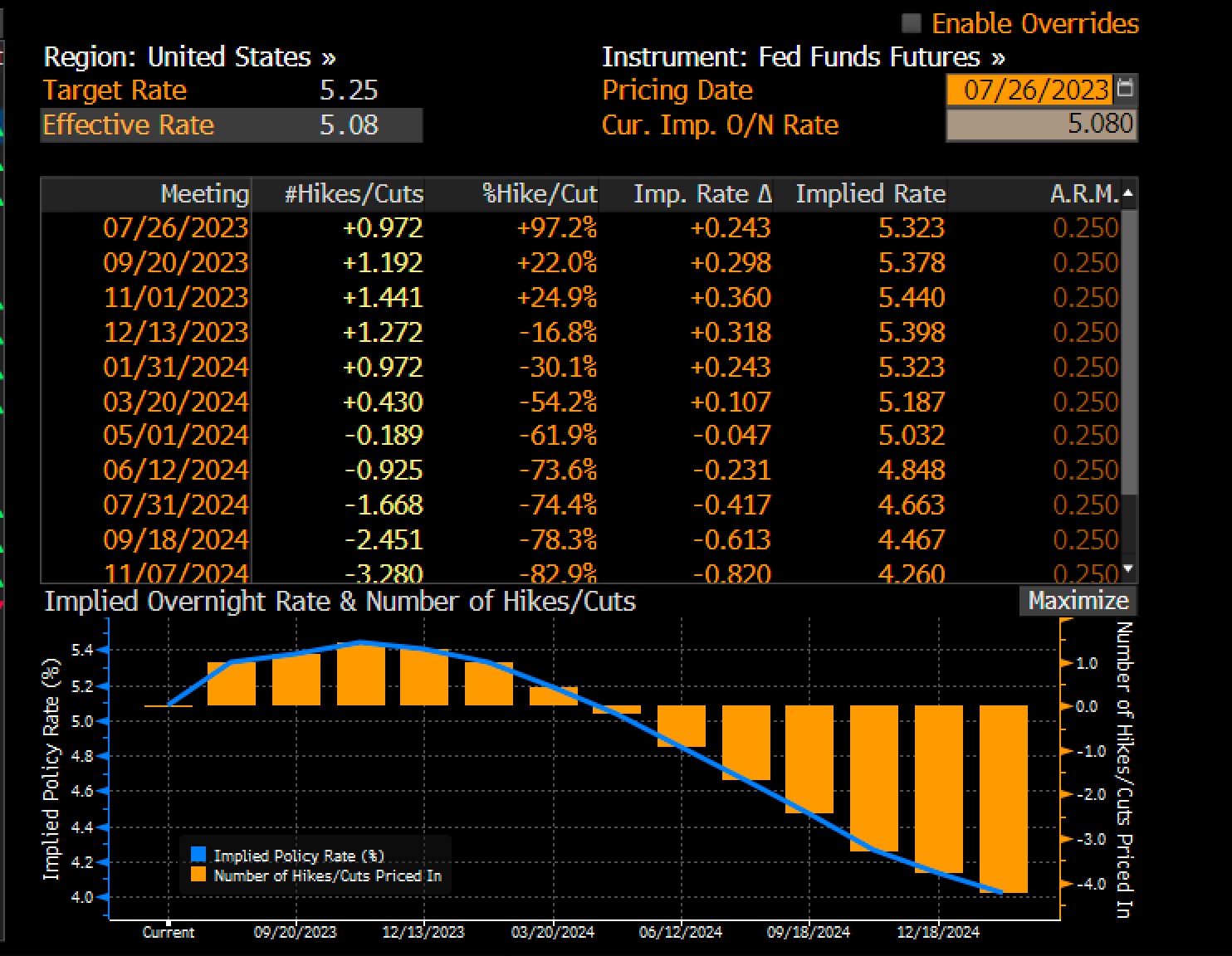

As New York walks into the office this morning, all thoughts are on how the FOMC meeting will play out. The current expectation is for no rate movement today and still about a 50% chance of one more hike either in November or December. More remarkably, as I wrote yesterday, is the belief that there will be 100 basis points of cuts next year despite the growing belief of either a soft landing or no landing. Again, I ask, why would the Fed cut rates if the economy continues to grow with the current monetary policy? However, at this point, all we can do is wait.

FWIW, which may not be much, I continue to see the outcome as follows; no movement today, 25bps in November and then a reassessment in December based on how the data continues to flow. Nothing Powell has said indicates that he is comfortable that the Fed has vanquished inflation, and similar to the idea that every politician only cares about one thing, his reelection, I believe Powell is completely focused on just one thing, killing inflation. He has made it abundantly clear in the past that he expected some economic pain would be necessary in order to achieve that outcome, and he is not going to be deterred at this stage. It would not surprise me if Fed funds remained at the year-end 2023 rate, whether that is 5.50% of 5.75%, for all of 2024. In fact, absent a very significant recession, that is what I believe will occur. One man’s view.

Anyway, turning to the only other data of note today, UK CPI surprisingly fell to 6.7%, down from last month’s 6.8% reading and forecasts for a 7.0% outcome today based on rising energy and food prices. Even better for Governor Bailey, the core rate fell to 6.2%, well below last month’s level of 6.9% and forecasts of 6.8%. The pound dipped on the news, but only by -0.2%, as the entire FX complex remains in thrall to the FOMC outcome later this afternoon. However, this inflation result has pundits asking whether Governor Bailey will be able to skip tomorrow’s rate hike, just like the Fed, and wait until November if they deem it still necessary. My view here is that will not be the case. Given the overall weakness in the UK economy, Bailey is clearly running out of room to hike rates, and tomorrow is likely to be his last chance to raise rates before the evidence of sustained weakness becomes clear. Just like the rest of Europe, I expect the BOE will hike tomorrow and be done.

Once again, I will point out that the basis of my dollar views remains that the US is going to be the most hawkish of all the major economies, maintaining tighter monetary policy far longer than other nations, and that the dollar will naturally see investment flows continue. After all, the combination of higher yields and potentially better growth prospects will be far too much for international investors to ignore.

For now, though, we wait for 2:00pm and the FOMC statement along with their new Summary of Economic Projections, and then for Chairman Powell’s presser at 2:30. As such, until then I expect a pretty dull day.

Overnight, Asian equity markets were under pressure with losses in both Japanese and Chinese shares, as well as generally throughout the region. The only noteworthy news was that the PBOC left rates on hold, which was widely expected, although there were those who thought they might cut again to support the weakening Chinese economy. European bourses, though, are having a much better day, with all markets higher by at least 0.5% and several southern European nations seeing gains greater than 1%. Meanwhile, at this hour (7:30), US futures are edging higher by 0.2% or so after modest declines yesterday.

In the bond market, yesterday’s closing level for 10yr Treasuries was the highest, at 4.36%, since October 2007, and although the yield is lower today by about 2bps, this trend remains intact. The big mover today, though, is UK Gilts which have seen yields drop 8bps after that CPI report. This has helped drag European sovereign yields lower by about 2bps as traders want to believe that the rate hikes are over everywhere in Europe, and cuts are the next step. While that’s not my view, it is gaining traction.

In the commodity markets, oil (-1.0%) has finally had a pullback of substance after a rumor yesterday that the Biden administration was going to completely empty the SPR. There has been no source for that story and no corroboration but given the move that oil has seen over the past 3 months, up more than 35%, a pullback is no surprise. While there is likely to be a further short-term retreat here, the long-term prospects for oil remain significantly positive in my view. As to the metals markets, industrials are a bit firmer this morning, perhaps on the idea that the rate hiking cycle in Europe is ending, while gold is unchanged.

Finally, the dollar is a bit softer this morning, but not very much. The euro remains either side of 1.07 while USDJPY is pushing the 148 level, very close to the key 150 point where many participants believe the BOJ will step back into the market. As to CNY, its home has been the 7.30 level despite all the effort that the PBOC has expended to strengthen the yuan. The biggest winners today have been the Antipodeans, with both AUD and NZD firmer by 0.5% after the Minutes of the RBA meeting indicated that they were considering another rate hike at the last meeting although decided to hold off. The implication is another hike could be in the cards.

On the data front, really the FOMC meeting is today’s only activity of note, although we will see the EIA oil inventories as well. Until the meeting ends, I expect very little to occur. Once the announcement is out, and even more importantly, once Powell starts to speak, be prepared for more volatility.

Good luck

Adf