The data remains rather mixed

But traders are still all transfixed

By tariffs and trade

As JGBs fade

And new ideas get eighty-sixed

Despite signs that peace in Ukraine

Is further away and hopes wane

It seems all that matters

Is whether Huang flatters

Investors, so stock markets gain

Apparently, at least based on yesterday’s equity market performance, concerns over the eventual outcome of the current global fiscal and monetary regimes remains far down everyone’s list of worries. Rising inflation? Bah, doesn’t matter. Increasing tensions between Presidents Trump and Putin as Russia continues, and arguably increases its aggression? No big deal. But you know what has tongues wagging this morning? Nvidia earnings are to be released after the close, and as we all know, if they are strong (everyone is counting on Jensen Huang, the CEO), then every other concern pales in significance. After all, a global conflagration is no match in the imagination compared to your stock portfolio increasing in value!

Once upon a time, investors in the stock market sought companies that had good business models and good management who were able to grow their businesses. These investors were buying a piece of a business in which they believed. Analysts looked at metrics like P/E ratios and book value to determine if the price paid offered future opportunities as an investment, but the underlying company was the focus. Of course, that is simply a quaint relic of times long ago, pre GFC. Today, there is only one metric that matters, ‘NUMBER GO UP’! While this concept was originally ascribed to Bitcoin and the crypto universe, it has spread across virtually all financial markets. Nobody cares what a ticker symbol represents, they only care if the number next to the ticker symbol rises, and how rapidly it does so. Welcome to the future.

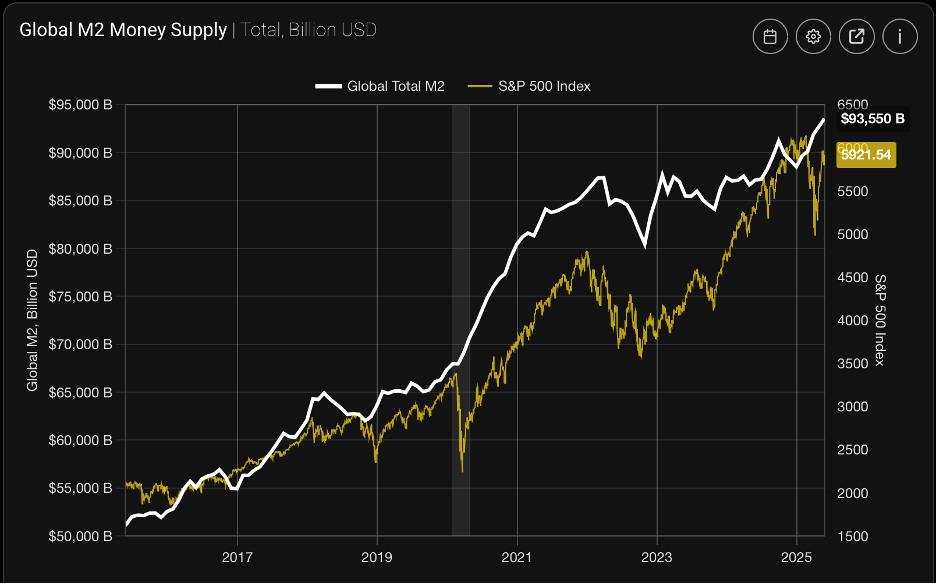

I highlight this because it has become increasingly clear that the macroeconomic landscape is an anachronism for analyzing financial markets. At this point, whether or not a recession is on the horizon, or inflation is rising, or unemployment is rising or falling seems to have only a fleeting impact on market movements. Rather, the true driver appears to be the flow of all that money that has entered the global financial system since the GFC. The below chart from streetstats.finance shows the last 10 years of the growth in the global money supply and the corresponding move in the S&P 500. You may not be surprised at the tight correlation.

My point is that all the news items that draw our attention may not matter at all in the broad scheme of things. As long as money continues to be printed and injected into the financial system, while some assets will outperform others, the trend remains sharply from the lower left to the upper right. Going back to my discussion yesterday, since the overriding goal of every global central bank is to ensure that their governments can issue bonds to finance their spending, I see no end to this trend. While the speed of the increase may ebb and flow slightly, the direction will only change under the most egregious circumstances, something like the aftermath of WWIII.

In a funny way, this highlights that FX markets have the opportunity to be the most interesting trading markets going forward given the relativity of their underlying basis. Assets, whether debt, equity or commodity, are all priced on demand functions while FX is priced on relative demand for each side of the cross. Perhaps FX will be the last bastion of macroeconomic analysis.

But not today! Starting with FX, the dollar is little changed to slightly higher this morning, consolidating yesterday’s gains but things are quiet. In fact, across the main markets, the largest movement in either direction is NZD (+0.25%) after the RBNZ cut rates as expected by 25bps, but the market reduced the probability of another rate cut in July. But away from that move, +/-0.1% is the norm today. Discussion about tariffs continues to be the major talking point, but as of now, it appears nobody has a clue as to how things will evolve, so everybody is just hunkering down.

Turning to equities, while yesterday saw a very large rally in the US, that sentiment was absent overnight with Asian markets generally drifting slightly lower although New Zealand (-1.7%) was clearly unhappy with the RBNZ mild hawkish view. But elsewhere, movement was far less than 1.0%. In Europe, it is a similar tale, very modest declines across the board as data showed German Unemployment rising slightly, Eurozone Consumer Inflation Expectations also rising slightly while French GDP disappointed on the downside, just 0.6% Y/Y. You can appreciate the lack of enthusiasm there, although the story that Madame Lagarde is considering stepping down from the ECB to take over WEF should put a spring in the step of European investors as perhaps the next ECB president will understand economics and central banking. As to US futures, they are little changed at this hour (7:35).

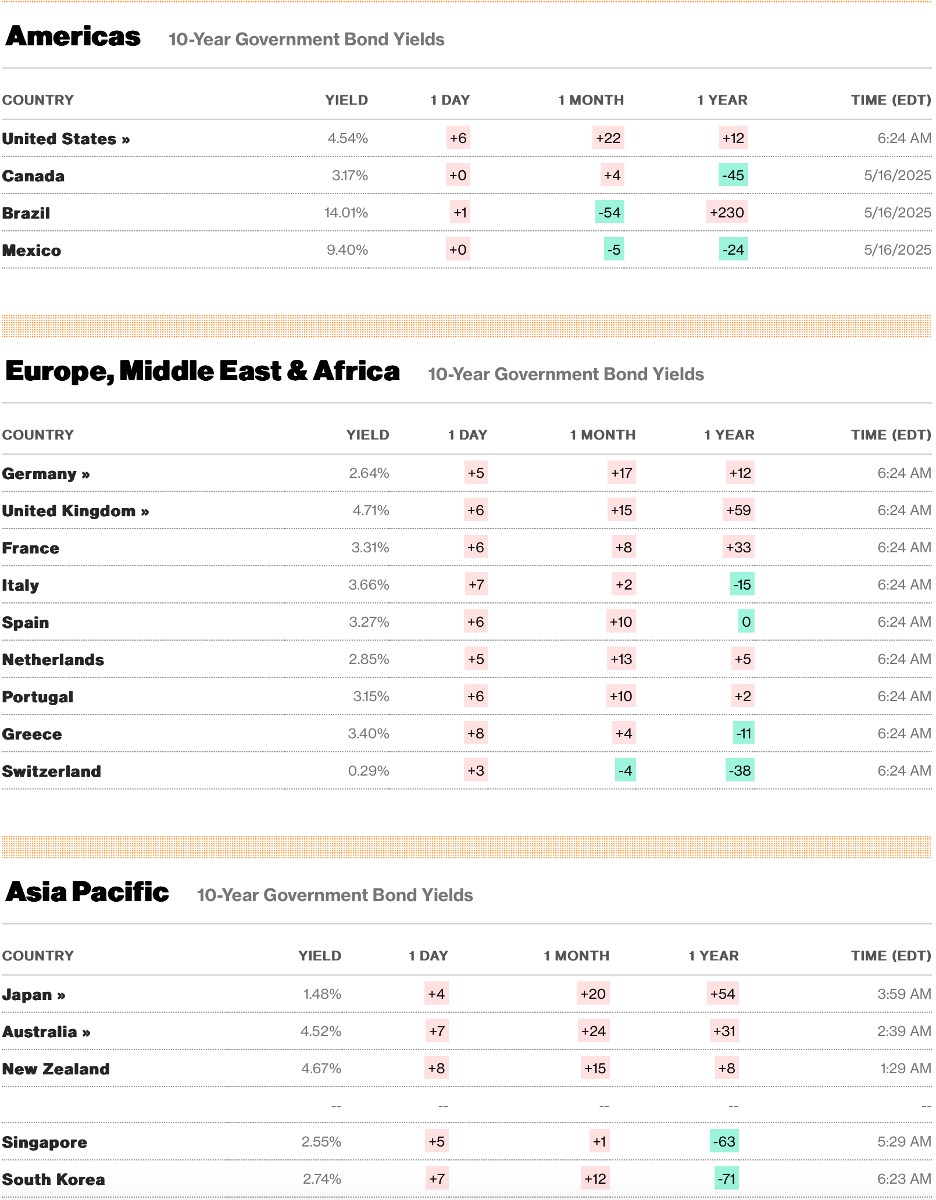

In the bond market, after a session where yields slid across the board yesterday, this morning brings a modest reversal with Treasuries (+2bps) right in line with most of Europe (+1bp across the board) although JGB’s (+5bps) suffered after another lousy long-dated auction last night where 40-year JGBs saw pretty weak demand overall. The Japanese bond market remains a serious issue for many and a potential signal for the timing of next big move. While risk assets rallied yesterday, nothing changed my description of the problems that exist globally.

Finally, in the commodity markets, oil (+0.7%) is modestly higher this morning but continues to trade within its range and shows no sign of breaking out in the near term. Metals markets, which sold off aggressively yesterday have stopped falling, but are hardly rebounding, at least as of now.

Let’s look at the data for the rest of the week though.

| Today | FOMC Minutes | |

| Thursday | Initial Claims | 230K |

| Continuing Claims | 1900K | |

| Q1 GDP (2nd estimate) | -0.3% | |

| Friday | Personal Income | 0.3% |

| Personal Spending | 0.2% | |

| PCE | 0.1% (2.2% Y/Y) | |

| Core PCE | 0.1% (2.5% Y/Y) | |

| Goods Trade Balance | -$141.5B | |

| Chicago PMI | 45.0 | |

| Michigan Sentiment | 51.0 |

Source: tradingeconomics.com

In addition to the data, with all eyes really on Friday’s numbers, we hear from six more Fed speakers, although, again, will they really change their tune about patience in watching what the impact of tariffs are going to be on the economy? I think not. In the Fed funds futures market, the probability of a cut in June has fallen to just 2% while the market is now pricing just 47bps of cuts this year, the lowest amount in forever. Unless the data completely fall off the map, I don’t see why they would cut at all, and that has just not happened yet.

The summer is upon us (although you wouldn’t know by the weather in the Northeast) and that typically leads to a bit less activity overall. At this point, much depends on Congress and its ability to complete the budget bill to move the legislative process along. Then the hard part of spending bills will be the next topic and you can expect a lot of screaming then. In the meantime, though, I expect that we will hear of a number of other trade deals getting completed and a good portion of the trade anxiety ebbing from market views. Alas, the peace/war equation is far more difficult to handicap as so many in power clearly benefit from war.

The prevailing view in the market is that the dollar has further to decline going forward as I think a majority of players are anticipating a recession in the US and the Fed to respond. Under that scenario, a softer dollar feels right. But is that the right scenario?

Good luck

Adf