Said Jay, I will not be ignored

And so, I ain’t leaving the board

When my time as Chair

Is up, and I swear

I will see the president gored

So first off, we ain’t cutting rates

‘Cause here in the United States

Inflation’s a worry

And I’m in no hurry

To help Trump escape dire straits

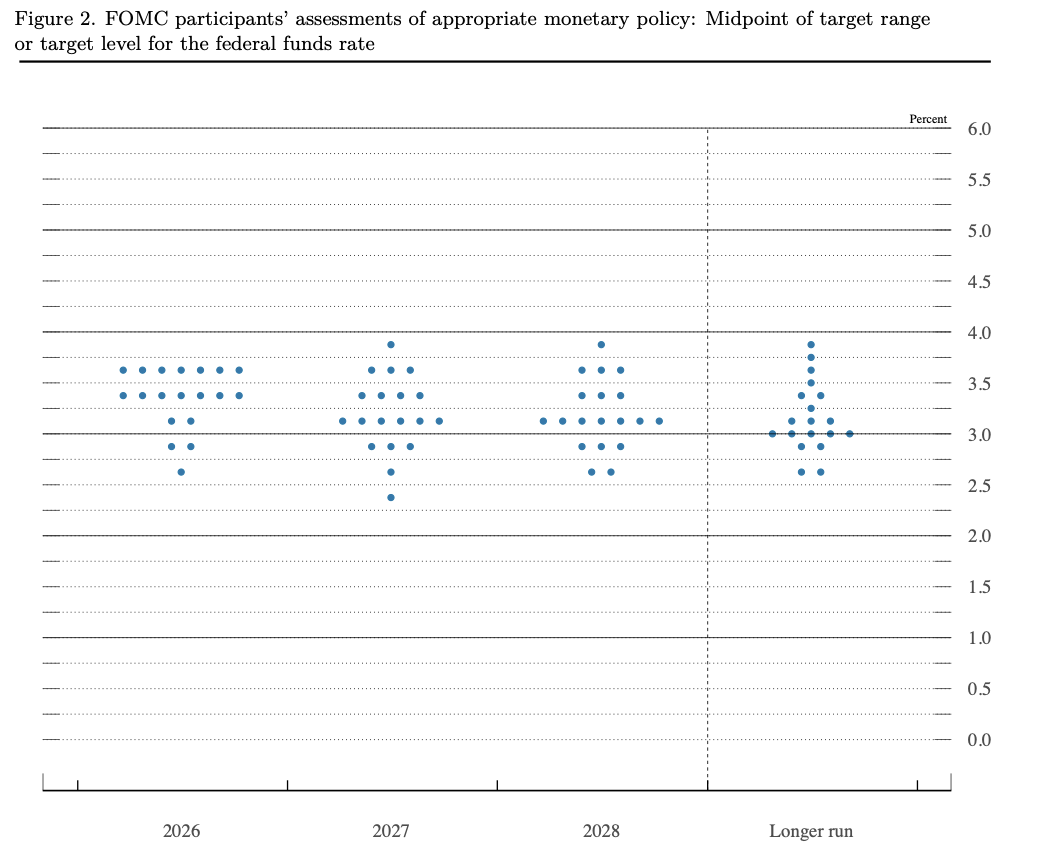

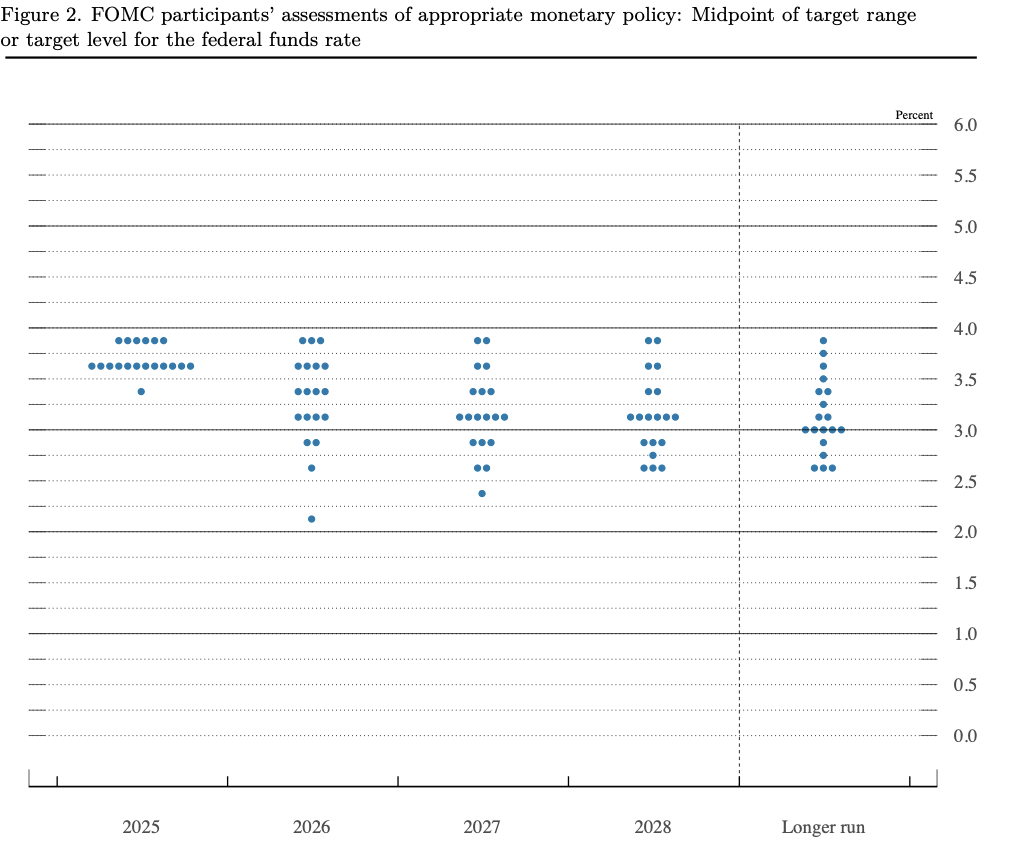

I guess we cannot be surprised that Chairman Powell was combative during his press conference yesterday after the Fed left rates on hold, as expected. There was only one dissent this month, Governor Miran, still looking to cut rates. However, while standing pat given the high level of uncertainty that exists from the war situation makes sense, compare the dot plot from this meeting to the December meeting below it. The dispersion of views on the committee has really tightened up a lot. While the median for 2026 continues to point to one cut, it appears that the Fed now believes we are near r*, although they didn’t say that exactly.

March 2026 dot plot

December 2025 dot plot

The other noteworthy comment from the Chair was when he explained he had “no intention of leaving” the Fed until the Justice Department investigation is completed. And, if Kevin Warsh is not confirmed by the Senate by the end of Powell’s term as Chair on May 15th, he will remain as Chairman pro tempore, the same situation as his previous nomination when the Senate delayed his confirmation.

The market response to both the combative tone and the hawkish rhetoric overall was a further 1% decline in the S&P 500 from an already weak place as per the below chart where I highlighted the time of the Statement release. You can see how things behaved thereafter.

Source: tradingeconomics.com

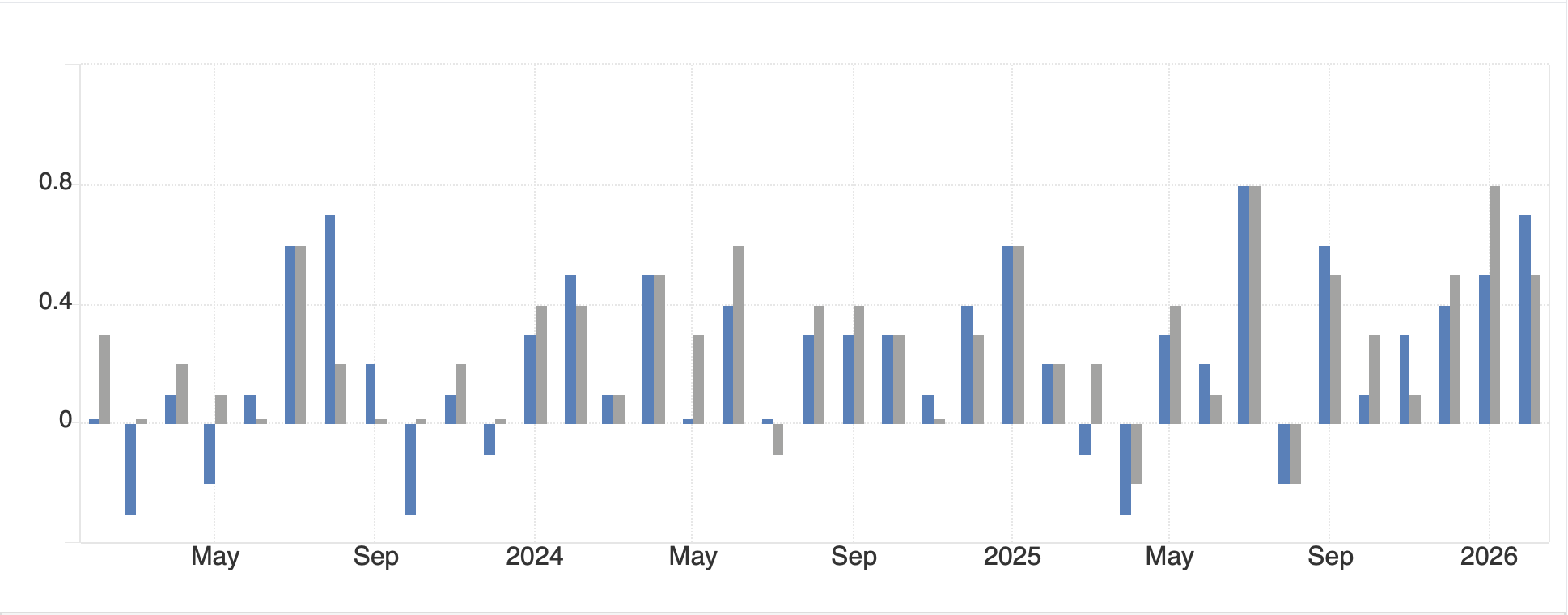

But that wasn’t all that happened yesterday, PPI came out MUCH hotter than forecast with headline at 0.7% (3.4% Y/Y) and core at 0.5% (3.9% Y/Y) as inflation concerns rose to the fore. If you look at the PPI chart below showing both headline (blue bars) and core (gray bars), it is very difficult to discern a pattern of declining producer prices.

Source: tradingeconomics.com

In fact, it is hard to look at this data and reconcile it with the Fed’s SEP forecasts describing the view that inflation, even their measure of core PCE, is going to smoothly return to their 2% target over any particular timeline.

One last event of note was the Iranian response to an attack on its main Natural Gas field, South Pars, where they inflicted serious damage to the Ras Laffan LNG facility in Qatar, which happens to be the largest in the world and is on the wrong side of the Strait of Hormuz to boot. The result has been a significant rise in the price of European (and UK) natural gas, with both soaring more than 20% this morning while, Brent crude has jumped 7.2% as opposed to WTI’s unchanged status today. This has taken European NatGas to ~$22.MMBtu compared with the US price of $3.15. Ask yourself how long Europe can afford to pay 7x US prices for NatGas and maintain any competitive ability to manufacture anything. (As an aside, this remains a key reason that I see long-term prospects for the euro so dimly.) But if we look at the longer-term chart of European NatGas, despite the dramatic increase since the Iran conflict began, it is nothing compared to what we saw in the wake of Russia’s invasion of Ukraine.

Source: tradingeconomics.com

Summarizing yesterday’s session in one word, I would say, Aaaaaaggggghhhhhh!

I assume I have depressed you enough with yesterday’s activities, but I will run through market responses overnight. You won’t be surprised to learn they have not been positive.

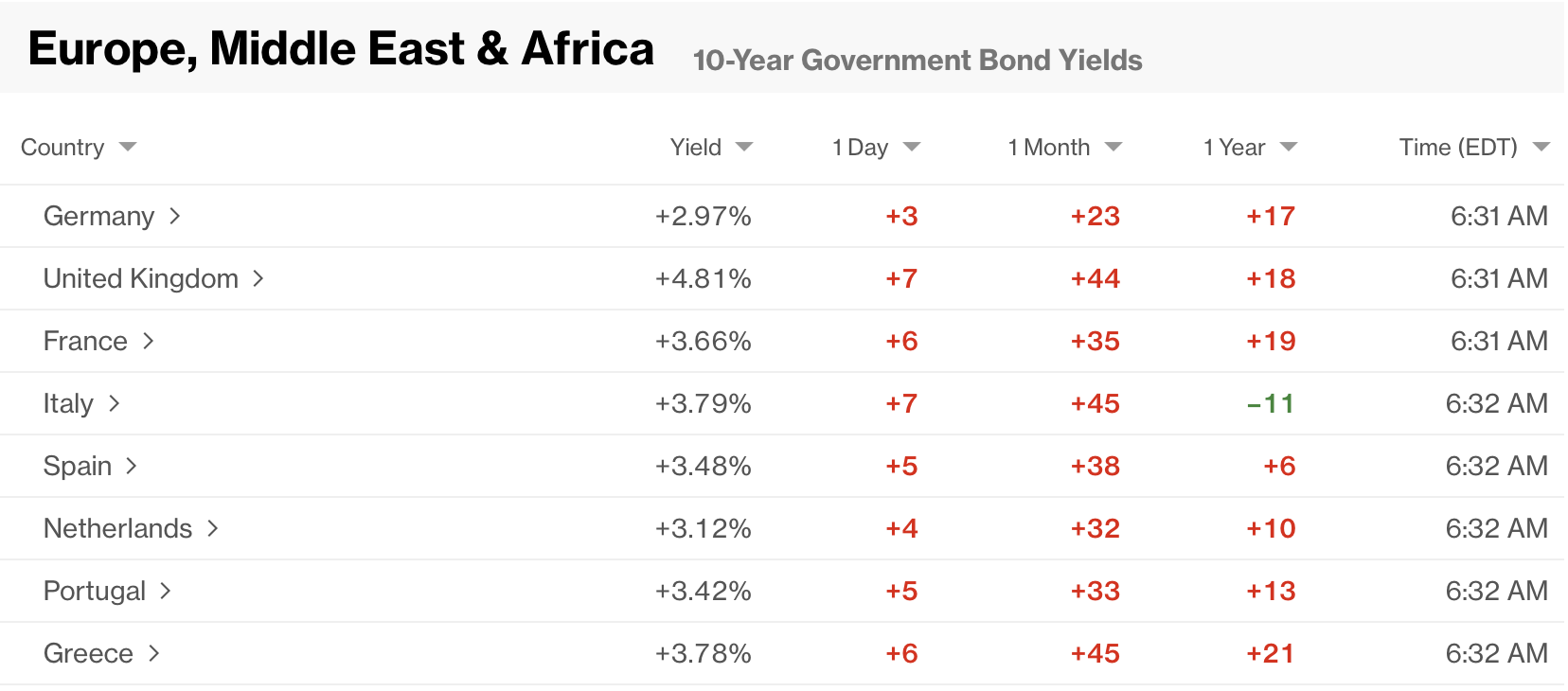

In fact, I guess I will start with bonds this morning, which I didn’t discuss above, but not surprisingly given the high PPI readings and the sharp rise in oil and gas prices, have suffered a lot. Yesterday, Treasury yields reversed their early declines and closed higher on the day by 6bps. They have edged up another 1bp this morning and are back above that 4.20% range I have focused on. Meanwhile, European sovereign markets were all closed when the FOMC meeting concluded, which added to the pressure on bond yields which started with the US PPI data. Net, yesterday, German bunds rose 4bps and this morning they are higher by a further 3bps. But as you can see from the below Bloomberg screenshot, they are the champs in Europe today.

JGB yields also rose sharply, up 6bps and we saw similar rises throughout Asian bonds. Right now, it is very clear that inflation is a bondholder’s concern, not recession.

As to equity markets, you will not be surprised to know that every market in Asia declined, most by more than -1.0% with the Nikkei (-3.4%) the worst performer followed closely by India’s Sensex (-3.1%), but there was no place to hide in Asia. In Europe, the damage is equally broad, although there is one outlier, Norway (+0.5%) which is obviously benefitting from the sharp rise in oil prices. But otherwise, -1.5% to -2.5% is today’s story across the board there. Interestingly, at this hour (6:45) US futures are little changed to slightly lower, just -0.1%. Perhaps this is a sign that all is not lost. Or maybe the algorithms just haven’t started their day yet. One noteworthy decline is South African shares (-4.0%) which is suffering from gold getting sold off yet again yesterday and today.

Since we already touched on energy, a quick trip through metals markets sees a major rout ongoing with gold (-2.75%) and silver (-5.2%) both suffering greatly, as is copper (-2.5%) and platinum (-6.1%). I continue to believe that gold is being liquidated to pay for other losses as the primary attraction of the barbarous relic remains. One thesis is that Middle Eastern central banks are liquidating their holdings as, given the dramatic decline in their oil revenues, they need money for continuing operations, and arguably, that’s what the gold is for. Essentially, gold is the rainy-day fund. As to the other three metals, those hint more at slowing economic activity rather than forced liquidation. After all, there was a lot of euphoria on the way up, so if the narrative is changing, as that dissipates, so will demand.

Finally, the dollar has given back a small portion of yesterday’s solid gains but remains at the top of its 96.00 / 100.00 trading range as defined by the DXY and shown in the chart below.

Source: tradingeconomics.com

Again, considering energy policies and availability around the world, the US, which is the largest energy producer in the world and a net exporter of energy products, seems better positioned than any of its competitors to weather the current economic gyrations. However, if we look across specific currency pairs this morning, we see relative strength elsewhere on the order of 0.2% to 0.3%. Frankly, it is a bit surprising to see ZAR (+0.4%) rally given what is happening in both gold and the South African equity market, but stepping back slightly, given the rand’s weakness since the end of January, I guess we cannot be that surprised that there is consolidation. Certainly, there is nothing about the chart for the last month that indicates the rand is about to reverse course and strengthen dramatically.

Source: tradingeconomics.com

The big picture here remains, in my view, that the US has more pluses than minuses vs almost all its counterparts.

On the data front, I didn’t even mention last night’s BOJ meeting, where they left policy on hold, as it didn’t seem to have a major impact. Perhaps, Ueda’s mildly hawkish comments have helped the yen a bit this morning. As well, the Swedish Riksbank left policy on hold and in a short while we expect both the BOE and ECB to leave policy rates on hold. The one which might move is the UK, where last time they voted 7/2 to leave policy unchanged but analysts think 4 members could vote for a cut. However, my sense is that cutting rates at this time, before there is evidence that the economy is truly suffering from the war, would be a surprise. Otherwise, we get the weekly Initial (exp 215K) and Continuing (1850K) Claims as well as the Philly Fed (10.0) and then at 10:00 we see New Home Sales (720K). One other thing to note is that yesterday’s EIA data showed a substantial build in crude inventories, but a large draw in gasoline and distillates. It is this activity that helps explain the rise in crack spreads, and why the refiners should be having a very good quarter.

And that’s it for today. Quite frankly, that’s enough for me. As it happens, there will be no poetry tomorrow, so I will get to recap today and tomorrow on Monday and see what has changed in the Persian Gulf as well as any other new news.

Good luck and good weekend

Adf