It wasn’t all that long ago

When data would headline the show

As traders would wait

For each release date

And then recount trades blow-by-blow

But now there is only one thing

That matters, Trump’s latest cha-ching

He speaks off the cuff

Which makes it quite tough

To plan from Berlin to Beijing

As the morning of the third day of President Trump’s second term dawns, it is nigh on impossible to keep up with all the things he is doing and their actual and potential impacts on markets going forward. Arguably, the main FX market driver continues to be the tariff discussion and the question of if, and when, he may be imposing said tariffs. You will recall that on Monday, the mere absence of his reaffirmation that tariffs were coming resulted in a major dollar decline, which was subsequently reversed when he finally mentioned them in the evening.

Of course, those were aimed at Canada and Mexico with China, significantly, left out of the mix. Last night he remedied that situation declaring that China and Europe were also in his sights for tariffs, although he mooted a 10% initial level, far below the 60% he discussed during the election campaign. Once again, I would argue it is not possible at this point to make any serious market prognostications based on the lack of information as to the products to be impacted, the exact timing and what he is seeking in return for a reduction or elimination of those threats.

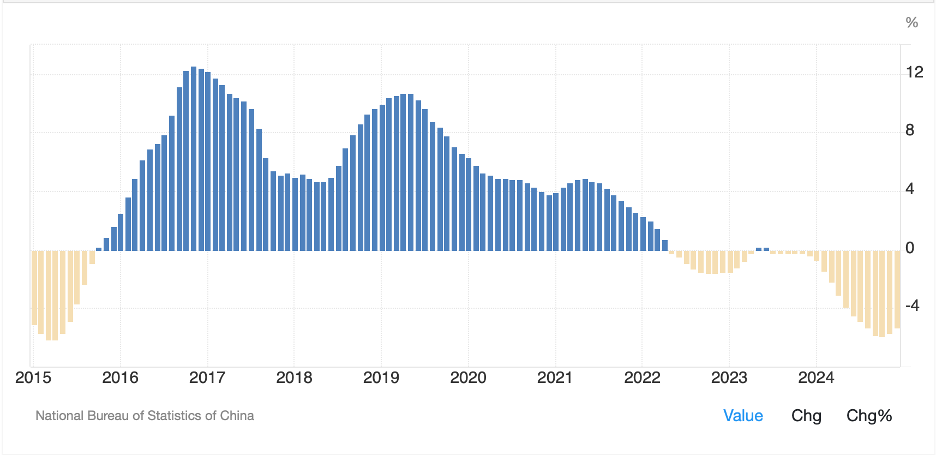

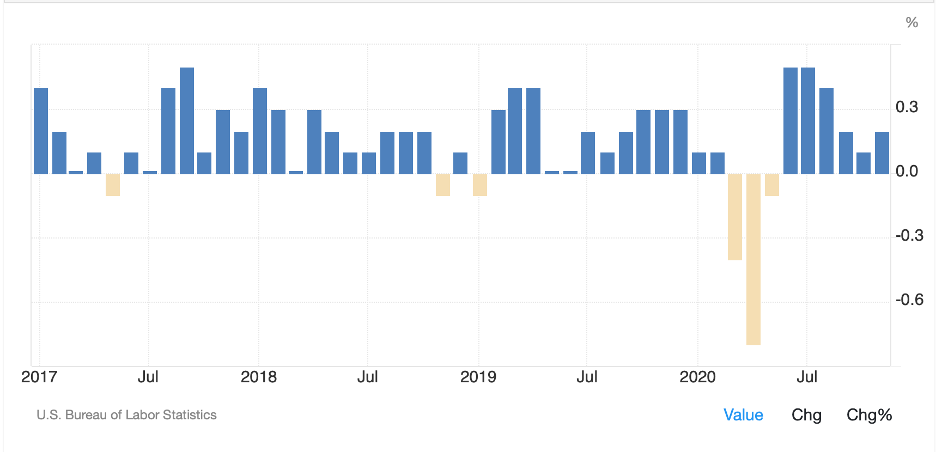

At the same time, I find the strait-laced approach that ‘tariffs are bad and a tax on Americans which will lead to inflation’ which continues to be promulgated by orthodox academic economists, typically from a left-leaning lens, to be almost comical at this point. We all should remember that during his first term, he imposed many tariffs, especially on China, and yet inflation was quiescent, with CPI averaging 1.9% during the entire term. This is not to say things will be identical in 2024 and beyond, just that in fairness, his record demonstrates that tariffs are not necessarily inflationary. Below is a chart of the monthly readings showing only 8 of the 48 months he was in office that headline CPI rose more than 0.3%, implying the rest of the time it was at or below that level. Those were the days.

Source: tradingeconomics.com

Beyond the tariff discussion, the bulk of his time currently seems to be focused on the size of the government workforce, which is certainly due to shrink, and the border and immigration. What will market impacts of these issues be like? For the former, I would suggest that less government employees will lead to less government interference in the workplace, and arguably, be beneficial for productivity if nothing else. As to the latter, it is a much more difficult problem to solve as there will likely be reductions in both labor supply but also demand for services like housing. It seems quite possible that there will be a reordering of the economy, although it is unclear if that will lead to a net positive or negative from an overall growth perspective, or at least an inflation perspective. Growth, of course, is the product of the size of the workforce * productivity, so a smaller workforce, if that is the outcome, will weigh on topline GDP, but not necessarily on per capita GDP. As I mentioned above, there are far more unknowns than knowns at this time, so forecasting the future is a mug’s game.

As we keep in mind that nobody knows anything about the future, let’s take a look at what happened overnight amid all the knee-jerk reactions to the latest Trump comments.

Yesterday saw US equity markets continue in their winning ways seemingly trying to achieve new highs. In Asia, the follow on was broad with Japan (+1.6%), Korea (+1.2%) and India (+0.75%) all nicely higher although Chinese shares suffered. This should be no surprise now that Trump has squarely put China on the tariff map again, but there are other things happening here as well. Perhaps the most confusing is the word that financial workers would be seeing pay cuts of up to 50% as President Xi no longer sees them as critical workers for the nation. I’m sure this will help rebalance the consumption-production equation…not! So, it should be no real surprise that both mainland (-0.9%) and Hong Kong (-1.6%) shares were under pressure.

Not so the case in Europe where the DAX (+1.2%) is leading the way higher although gains are universal, after comments from several ECB bankers that rate cuts were coming next week and likely will continue during the year. While inflation remains the sole ECB mandate, the weak economic situation plus the threat of tariffs certainly has Madame Lagarde under pressure to do something to support the economy there. Finally, it should be no surprise that US futures are nicely higher this morning with the NASDAQ (+0.9%) leading the way at this hour (7:15).

In the bond market, yields have stabilized after their recent 20bp decline in the past week and have edged higher by 1bp this morning. The same price action has been seen in Europe where sovereign yields are little changed to higher by 2bps across the continent. As to JGB yields, they, too, were unchanged on the session despite an increase in chatter that the BOJ is set to hike rates on Friday.

In the commodity space, gold continues to rally and is now within 1% of its all-time highs set back in late October. This has dragged silver along for the ride, and copper, in truth, although today copper is ceding -0.6%. however, a look at the price movement over the past month shows all three metals nicely higher (Au +5.3%, Ag +3.7%, Cu +6.2%). Oil (0.0%) is flat today as it consolidates its recent retracement. Recall, for the first two weeks of the year, it rallied sharply, up nearly $10/bbl, although it seems that may have been more of a short squeeze than a fundamental shift in thinking. Since then, it has given back about $4/bbl as market participants try to decide if the theorized Trumpian demand increase will offset the supply increase of drill, baby, drill.

Finally, the dollar is little changed this morning overall. That said, net over the past week, it has given back about 1.5% although that was from recent highs. This price movement feels far more like consolidation than a change in view especially given that the tariff story remains front and center. Now, it is possible that the market pushed the dollar higher ahead of the inauguration on a ‘buy the rumor’ idea and is now selling the news, but it remains difficult to see what has changed in the US economy relative to its counterparts that would encourage a change in rate expectations. As to today’s movement, there are more gainers than laggards vs. the dollar, but nothing of any real significance.

On the data front, the only US data is the Leading Indicators (exp 0.0%) so traders will continue to look at corporate earnings and listen to the president for the next pronouncement. I assure you; I have no idea what that will entail. Once again, I am a strong proponent of being hedged because the one thing we have learned lately is that markets can turn on a dime.

Good luck

adf