A cut has been all but assured

Though since last time we have endured

Some fears Jay’s a hawk

So, when he does talk

Will this cut, at last, be secured?

And now there’s a narrative view

Though rates will fall, what he will do

Is try to convey

Now it’s out the way

Another one may not come through

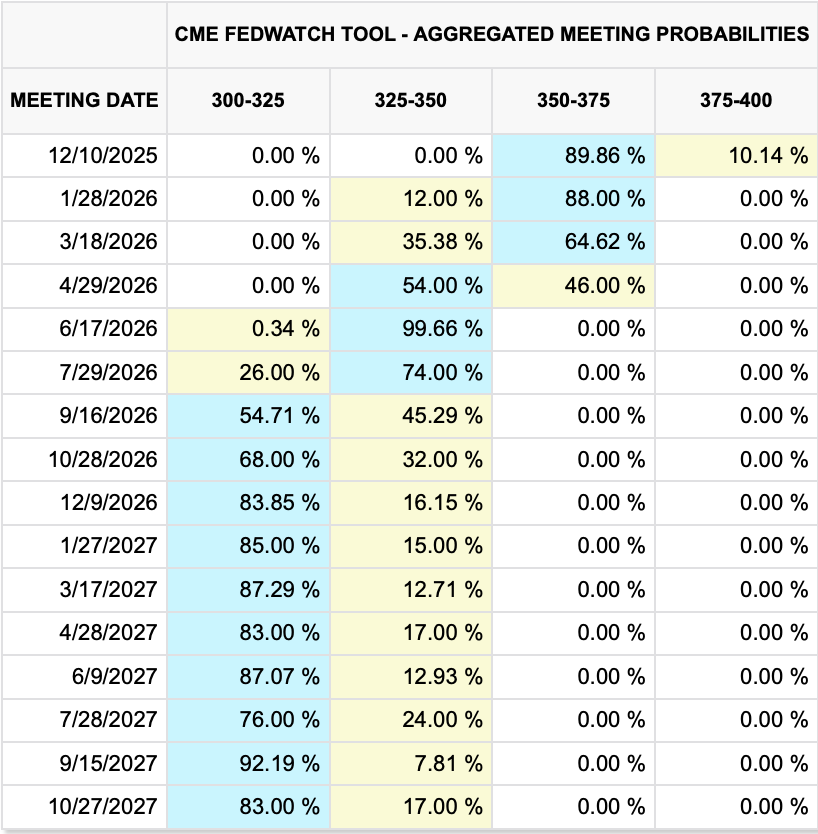

Good morning all and welcome to Fed Day. The question, of course, is will this be a frabjous day? As I write this morning, the Fed funds futures market continues to price a roughly 90% probability of a 25bp cut this afternoon, but the prospects for future rate cuts have greatly diminished as you can see in the table below from the CME.

It wasn’t long ago when the market was pricing 100bps more of rate cuts by the end of 2026, meaning a Fed funds rate of 2.50% – 2.75%. However, the narrative has shifted over the past several weeks after very mixed signals from FOMC speakers and data releases that have indicated the economy is not cratering (e.g. yesterday’s JOLTS data printing at 7.658M, >400K higher than expected). You may recall that shortly after the last FOMC meeting at the end of October, the probability of today’s rate cut had fallen to just 30%.

It appears that the new discussion point is this will be a hawkish cut, an idiom similar to jumbo shrimp. At this point, the bulk of the discussion has been around how many dissents will be recorded with the subtext being, what will Chairman Powell have to promise potential dissenters in order to bring them along to his side of the ledger. My take is if you thought the last press conference was hawkish, you ain’t seen nothin’ yet. In fact, I would not be surprised to see a virtually categoric call to this being the end of the cutting cycle for the foreseeable future.

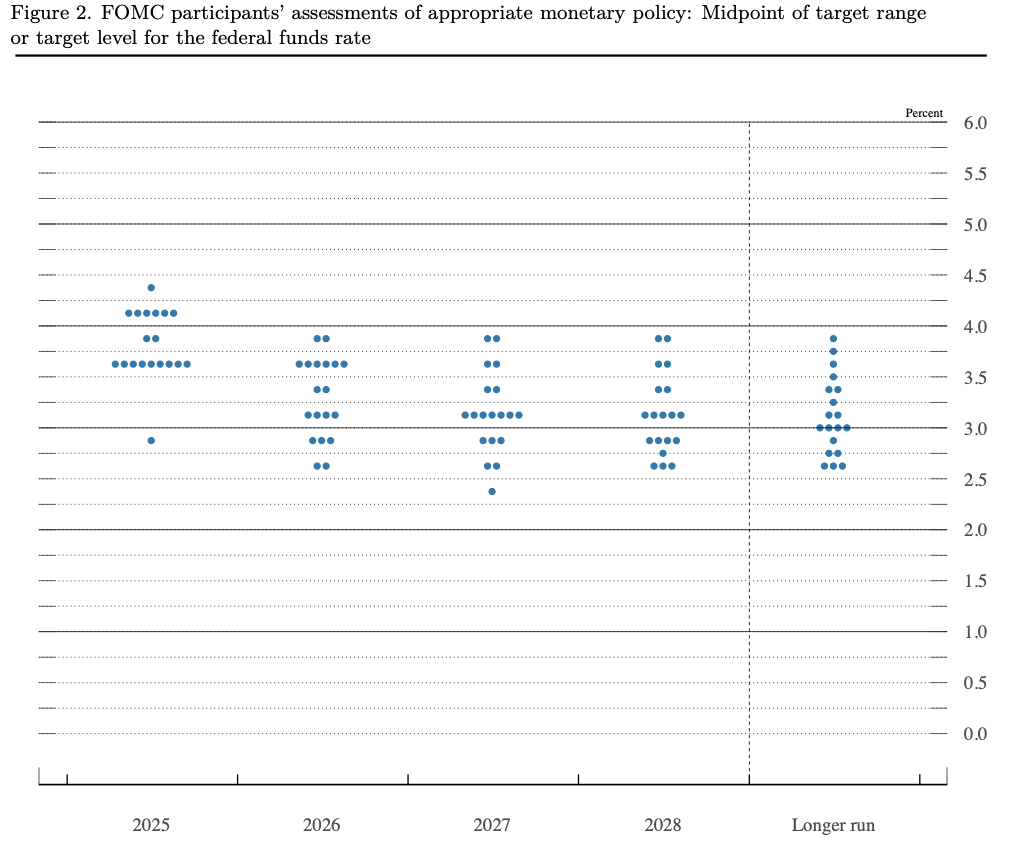

Remember, we also will see the new dot plots and SEP which will help us understand the broad picture of where FOMC members currently stand on the matter. Personally, I expect to see a wide disparity between the ends of the distribution, and it wouldn’t surprise me to see some expectations of no rate changes for 2026 with other calls for 150bps of cuts and no consensus view at all.

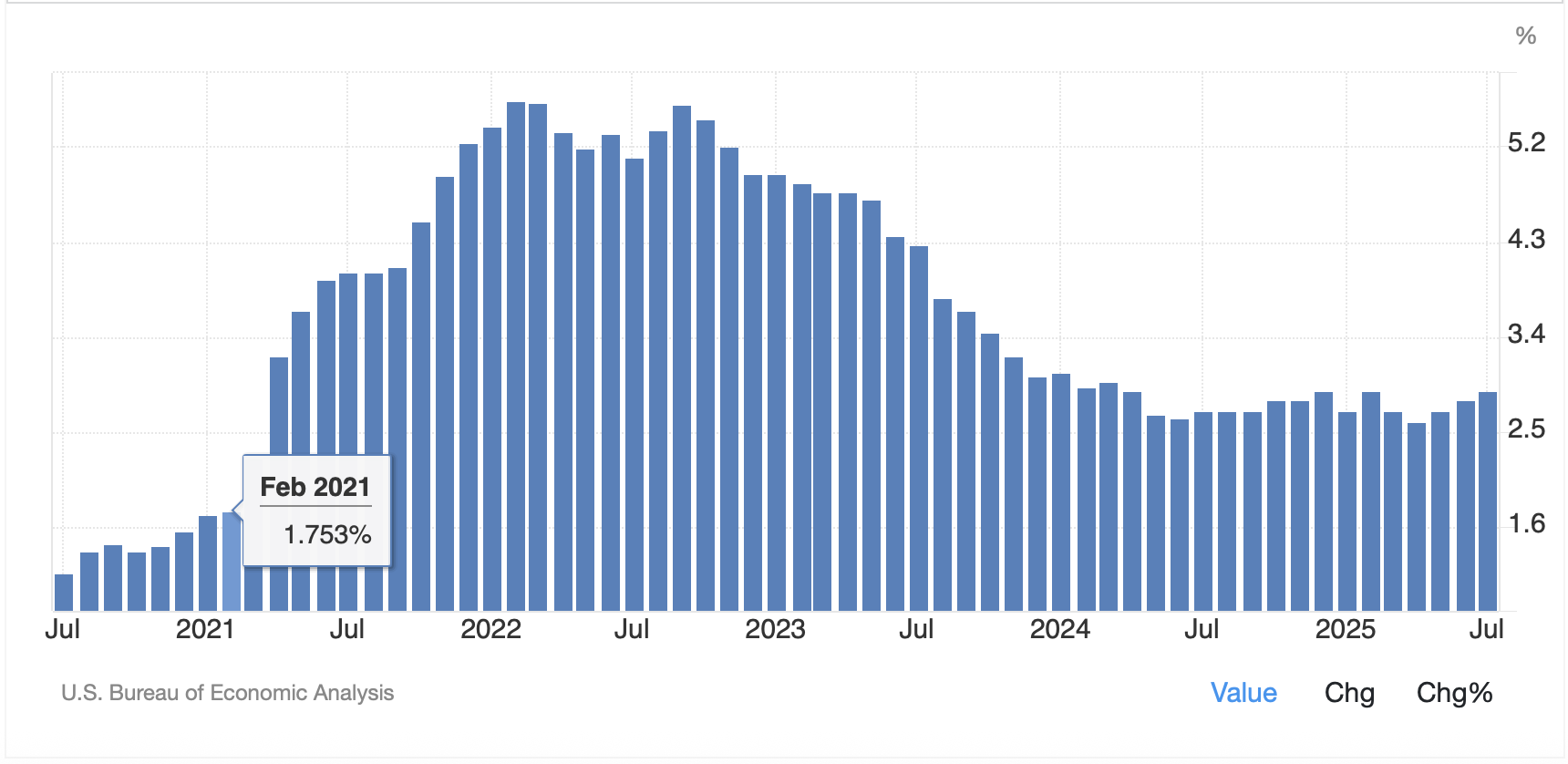

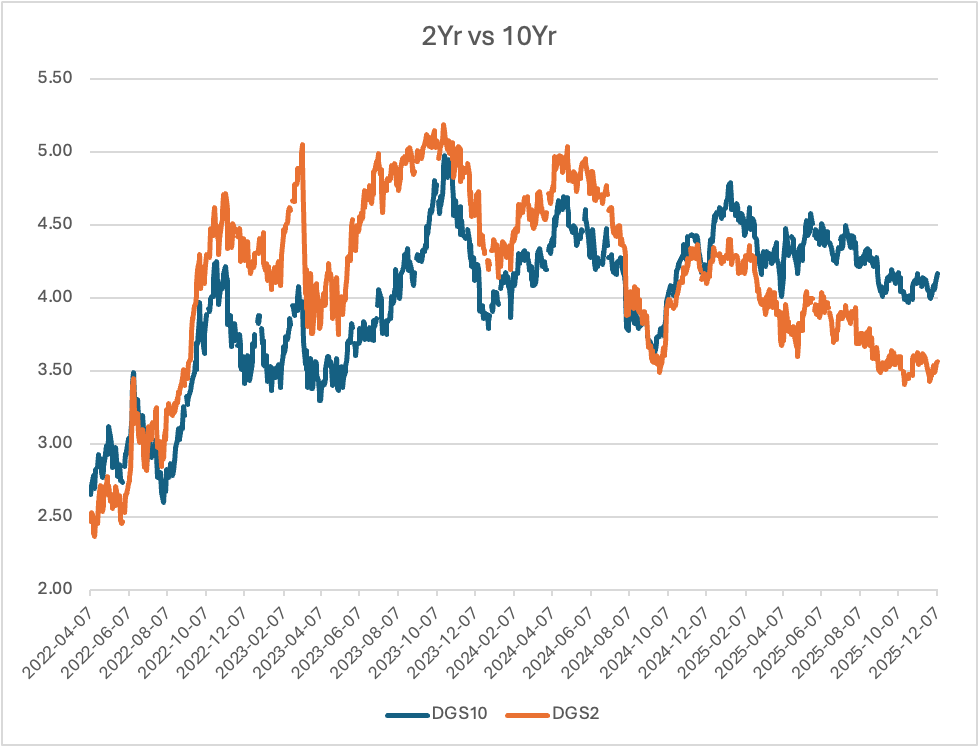

At this point, all we can do is wait. However, the market discussion has centered on the fact that 10-year Treasury yields (+1bp) have been climbing lately, and that this morning they have touched 4.20% again while, at the same time, 2-year Treasury yields (no change) have been slipping as per the below chart I created from FRED data.

The steepening yield curve, which now appears to be turning into a bear steepener (when long dated yields rise more quickly than short-dated yields) is ringing alarm bells in some quarters. The narrative is that there are growing concerns over both the quantity of debt outstanding and its rate of growth as well as the fact rate cuts will engender future inflation.

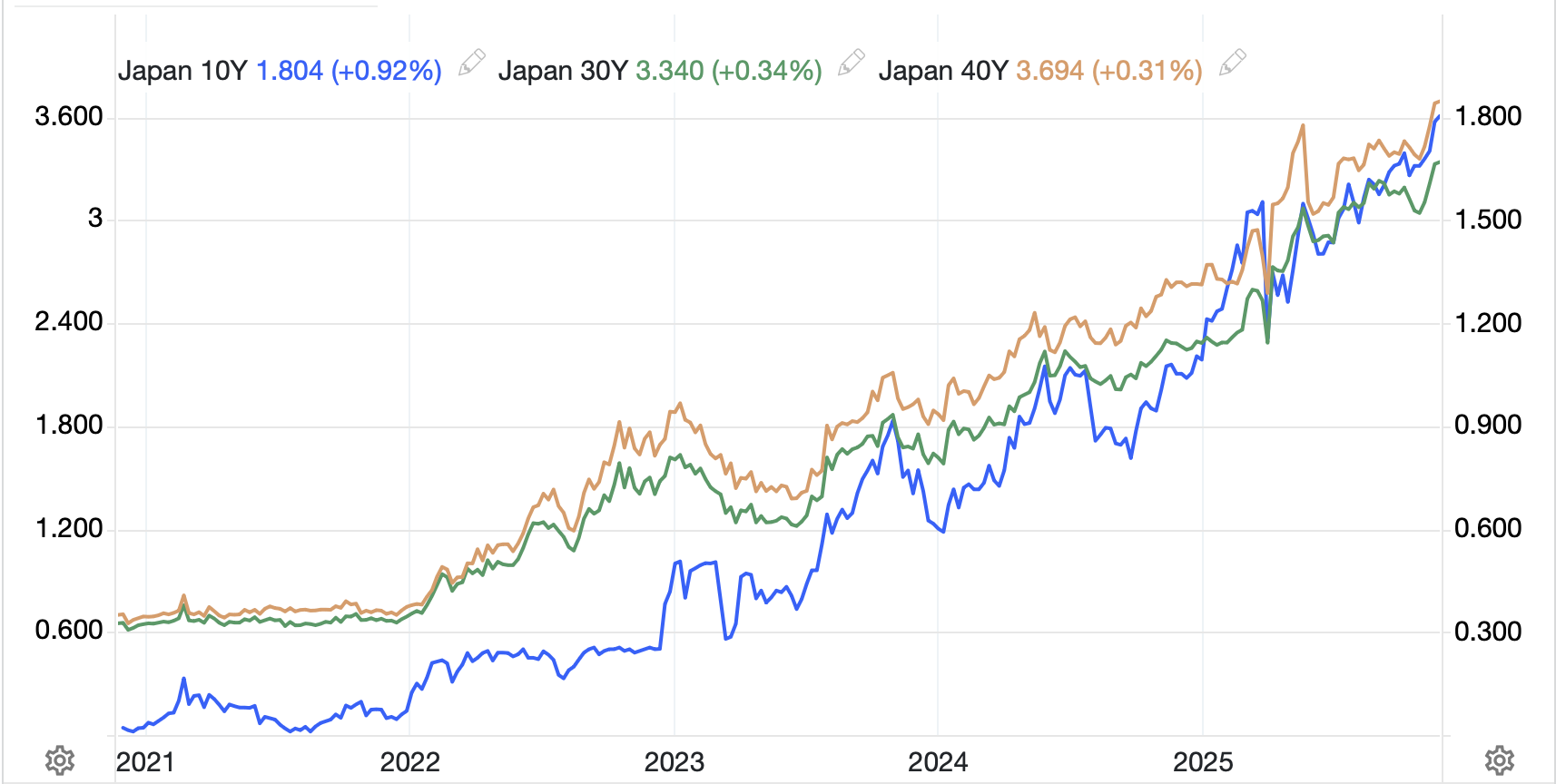

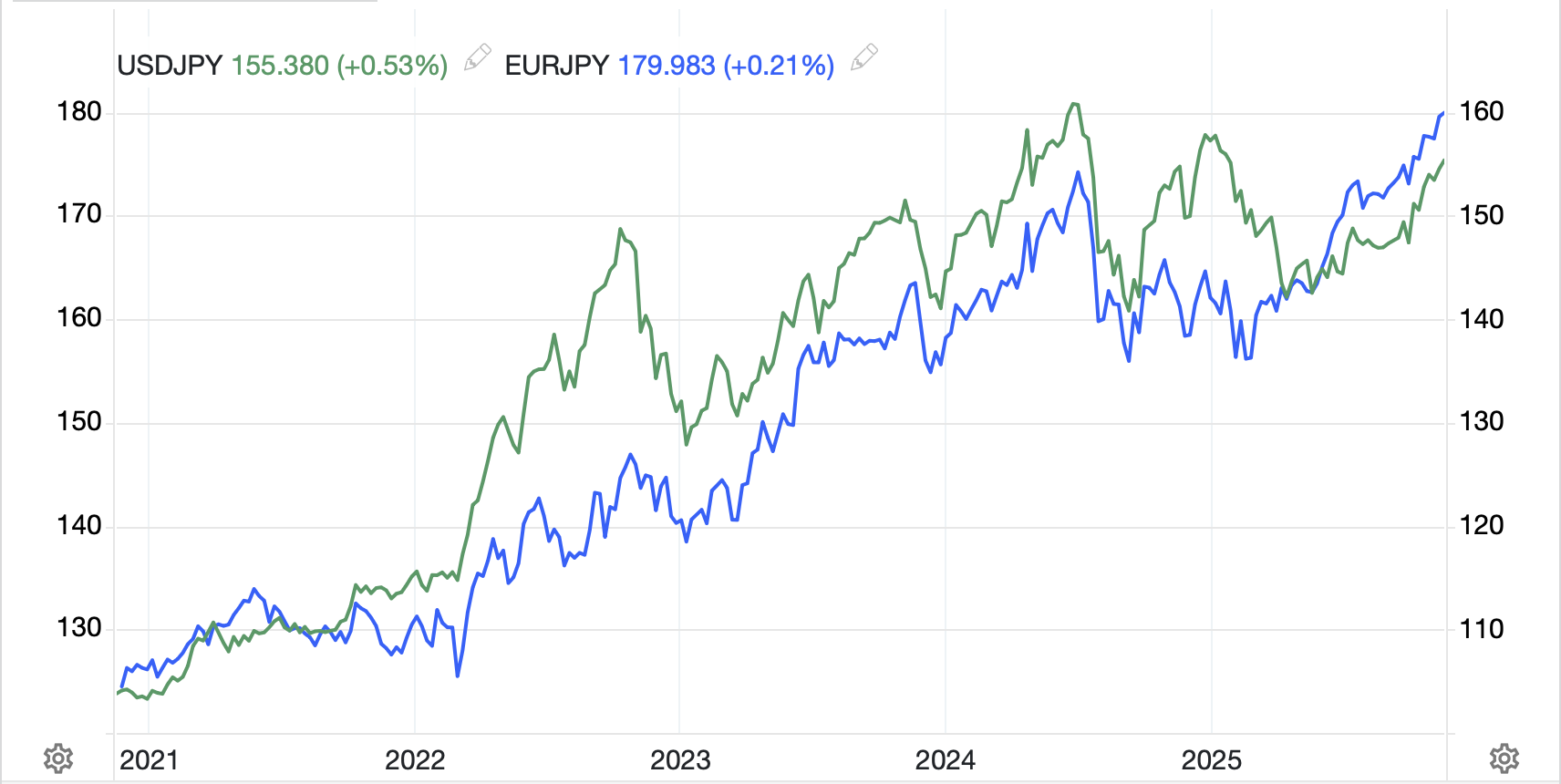

A key part of the discussion is the fact that what had been a synchronous system of global central bank policy easing is now starting to split up. While we have known the BOJ is in a hiking cycle, albeit a slow one, today, the BOC is not only expected to leave rates on hold but explain they have bottomed. We have heard that, as well, from the RBA earlier this week, and the commentary from the ECB may be coming along those lines. So, is the US the outlier now? And will that weaken the dollar? Those are the key questions we will need to address going forward.

But before we move on, there is one market I must discuss, silver, which exploded to new historic highs yesterday, trading through $60/oz and is higher again this morning by 0.6% and trading at $61/oz. someone made the point yesterday that for the second time in history, you need just 1 ounce of silver to buy one barrel of WTI. The first time was back during the silver squeeze in January 1980, but that was quite short-lived (see chart below from macrotrends.com). This one appears to have legs.

I don’t know that I can find another indicator that better expresses my views of fiat currency debasement alongside an expanding availability of oil. To my mind, both these trends remain quite strong, and this is the embodiment of them both combined.

Ok, so as we await the FOMC, let’s see if anybody is doing anything in financial markets of note. As testament to the fact that virtually everybody is awaiting the Fed this afternoon, US equity markets barely moved yesterday, and Asian markets were similarly quiet, with only Taiwan (+0.8%) moving more than 0.4% in either direction. The large markets were +/- 0.2% overall. In Europe, the movement has been slightly larger, but still not impressive with Germany (-0.4%) the laggard of note while the UK (+0.3%) is the leader. A smattering of data released from the continent doesn’t seem to be having any real impact, nor did comments by Madame Lagarde claiming the rates are in a good place and displaying some optimism on future GDP growth. Of much greater concern is the headlong rush to a digital euro CBDC, where they are seeking to exert control over the citizenry. If for no other reason, I would be leery of expecting great things from the Eurozone going forward. Not surprisingly, at this hour (7:30) US futures are little changed ahead of the meeting.

In the bond market, yields are creeping higher all around the world with European sovereign yields higher between 2bps and 4bps this morning. Perhaps investors are taking Madame Lagarde’s views to heart. Or perhaps the fallout from the recently released US National Security Strategy, where the US basically dismisses Europe as strategic, has investors concerned that European governments are going to be spending that much more on defense without having the financial wherewithal to do so effectively, thus will be borrowing a lot and driving yields higher. At this point, European sovereign yields have risen to levels not seen since the Eurozone bond crisis in 2011, but it feels like they have further to climb (see French 10-year OAT yields below from Marketwatch.com).

In the commodity market, oil (+0.5%) cannot get out of its own way. While it is a touch higher this morning, it sits at $58.50/bbl, and that long-term trend remains lower. We’ve already discussed silver and gold (-0.25%) continues to trade either side of $4200 these days, biding its time for its next move (higher I believe). Copper (+1.4%) is looking good today, although it is hard to find economic news that is driving today’s price action.

Finally, the dollar is a touch softer this morning, about 0.1% in the DXY as well as virtually every major currency in the G10. Interestingly, today’s outlier is SEK (+0.4%) which is rallying despite data showing GDP (-0.3%) slipping on the month while IP (-6.6%) fell sharply. As to the EMG bloc, there is very little movement of note with the biggest news this evening’s Central Bank of Brazil meeting where they are expected to leave their overnight SELIC rate at 15.0% as inflation there, released this morning at a remarkably precise 4.46% continues to run at the top of their target range of 3.0% +/- 1.5%.

Ahead of the FOMC, we only see the Employment Cost Index (exp 0.9%), a number the Fed watches more closely than the market, and we hear from the BOC who are universally expected to leave Canadian rates on hold at 2.25%.

And that’s really it. I wouldn’t look for much movement ahead of the 2pm statement release and then the fireworks at 2:30 when Powell speaks can drive things anywhere. The most compelling story will be the number of dissents on the vote, as there will almost certainly be several. According to Kalshi, 3 is the majority estimate. With President Trump continuing to discuss the next Fed chair, I have a feeling there will be 4 and that will be a negative for bonds (higher yields) and a short-term negative for the dollar. In fact, it is just another reason to hold precious metals.

Good luck

Adf