Investors are starting to shun

The riskiest things one-by-one

So, stocks feel the pain

And bonds, too, feel strain

The dollar, though’s, on quite a run

It’s nearly two weeks since this started

And so far, no ending’s been charted

The impact o’er time

Will not be sublime

Thus, trading’s not for the faint-hearted

Another day and there is no end in sight for the ongoing military action in Iran. US strikes continue apace and Iranian retaliation also continues, albeit at a lesser rate it seems. However, the information from the war zone remains difficult to trust as all of it is spun for various audiences with no sense of objective truth. As such, it is difficult to have an opinion on how long this will continue.

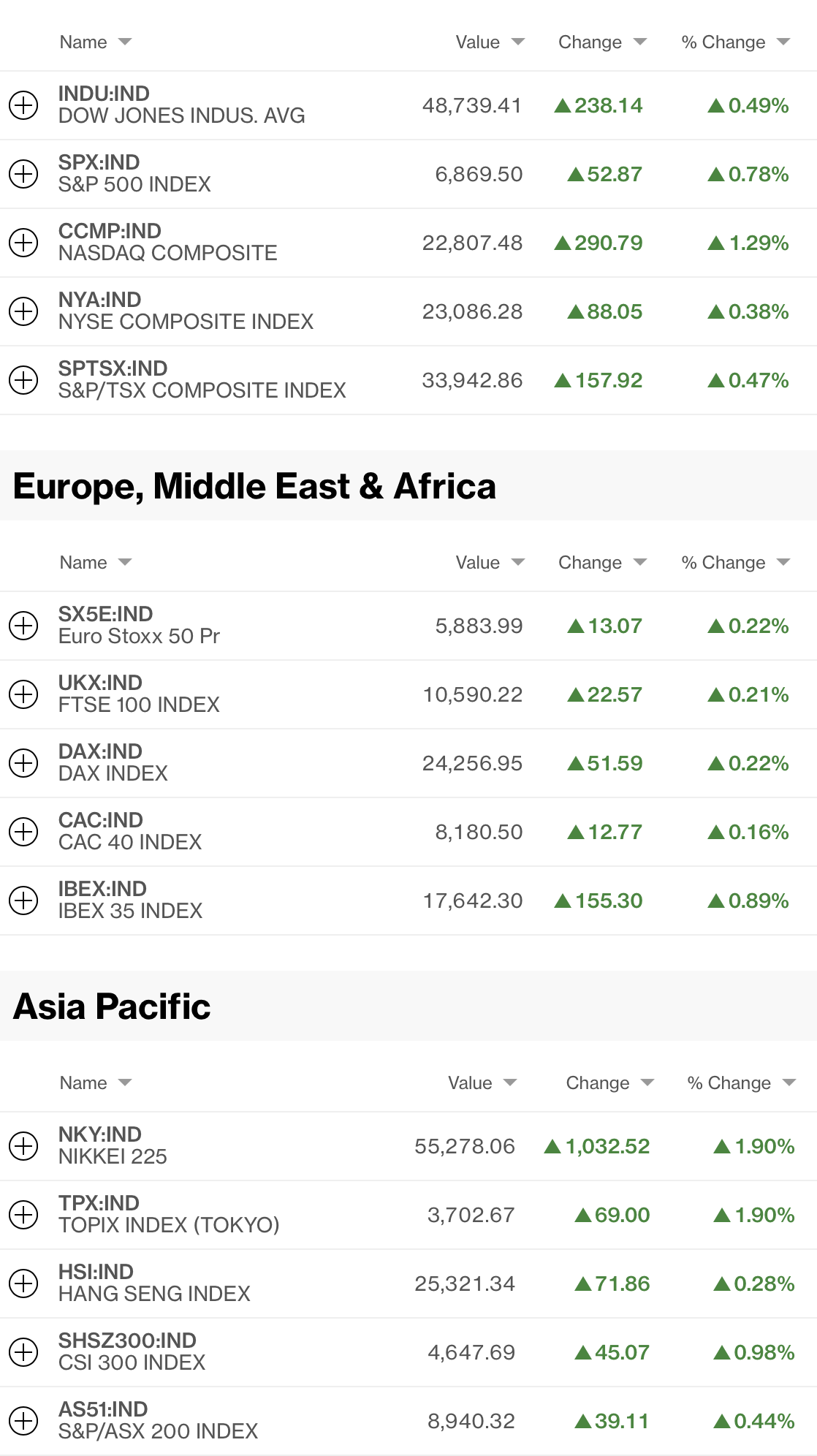

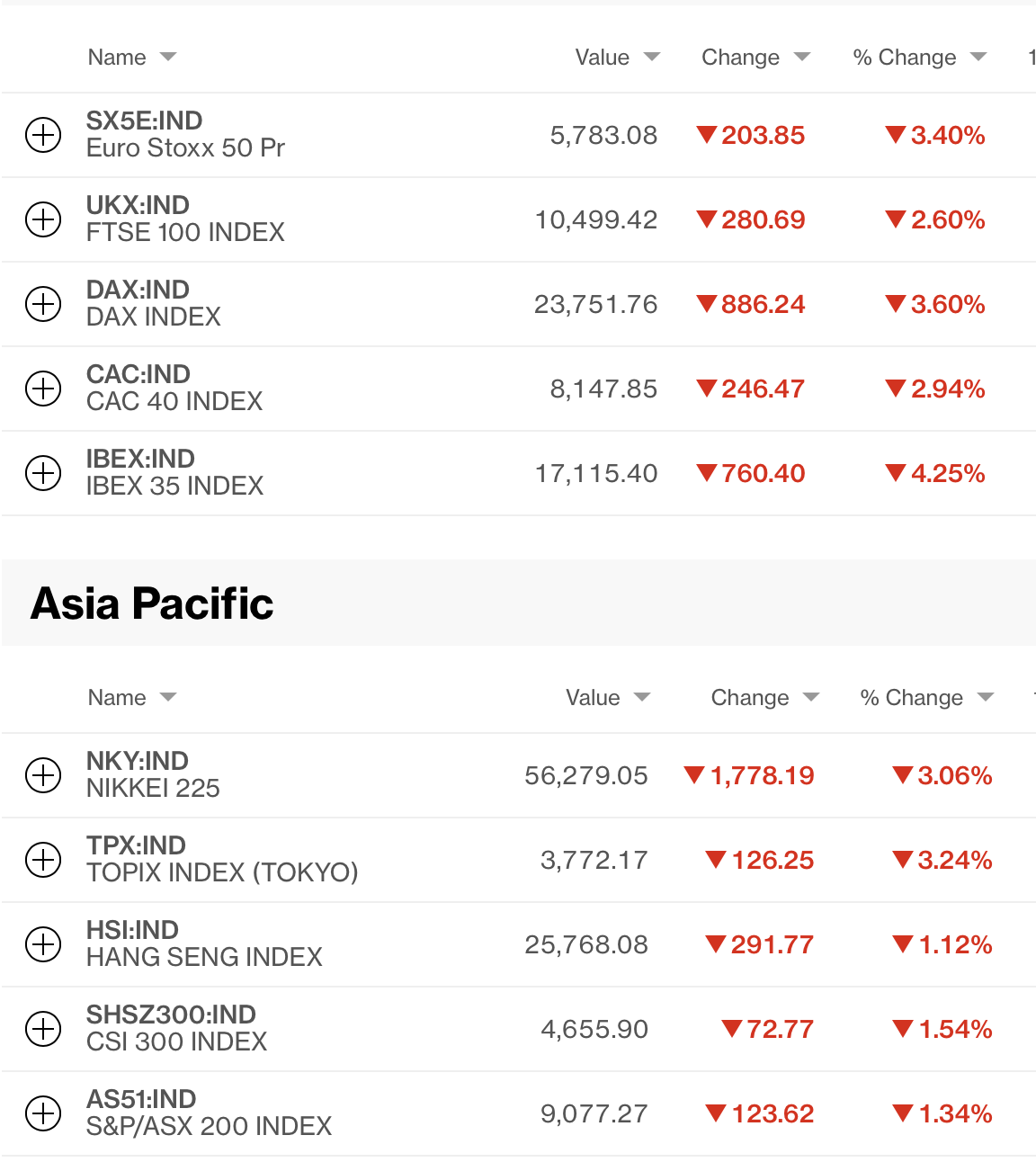

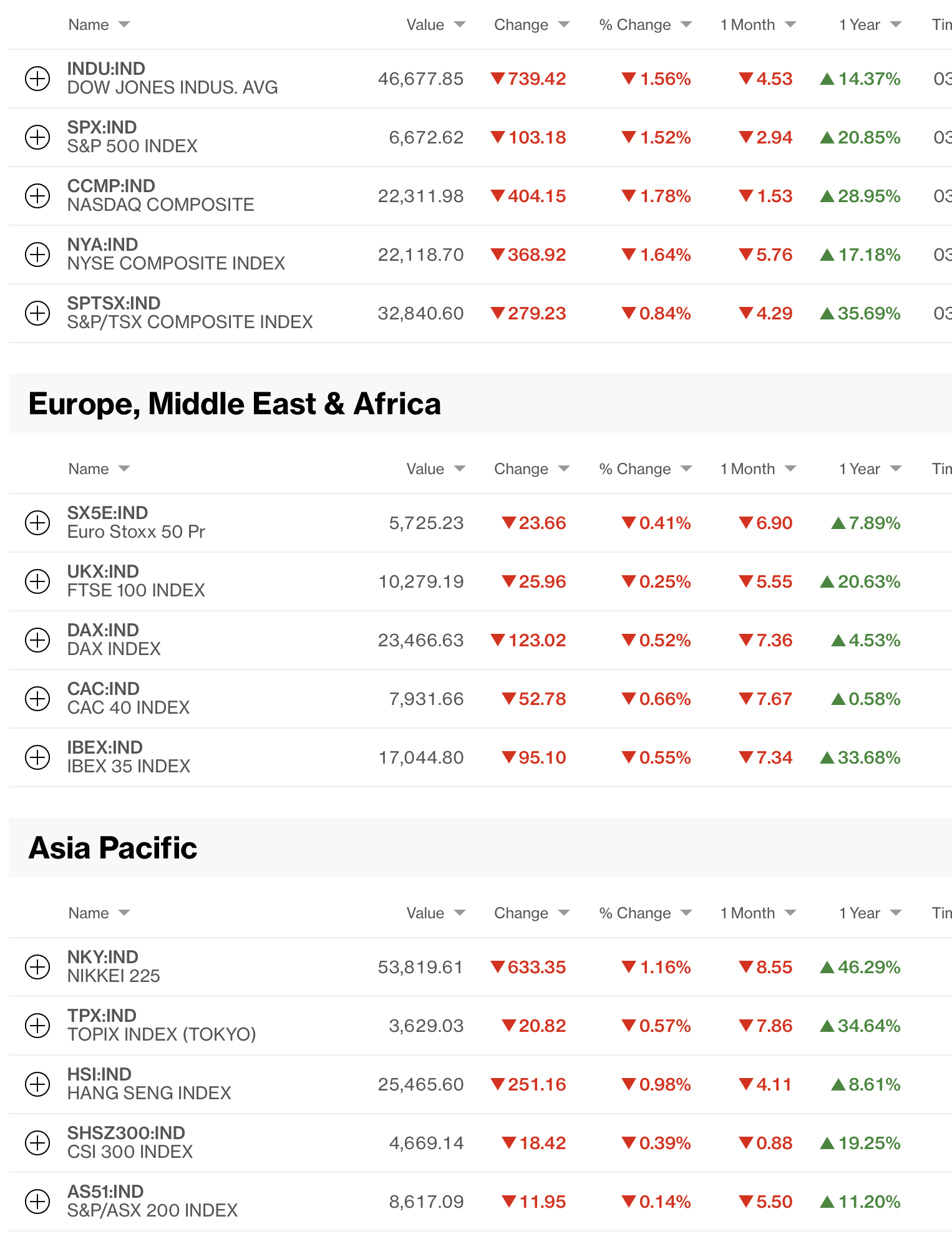

With that in mind, all we can do is observe market behavior and see what we can glean. Starting with equity markets around the world, the below screenshot from Bloomberg.com this morning shows that risk is clearly off, although not catastrophically so, at least not yet.

So, weakness in the US yesterday was followed by weakness overnight in the major markets in Asia as well as in other regional markets (Korea -1.7%, India -1.9%, Indonesia -3.1%) with the rest having declined by lesser amounts. It is important to see that all the Asian markets (and European and US markets) have fallen in the past month, but remain higher, in some cases substantially so, since this time last year. The point is that this move can still rightly be considered corrective, rather than a dramatic change in opinion.

European bourses are demonstrating similar behavior although US futures at this hour (6:45) are slightly higher, about +0.15% across the board. Thinking about equity markets overall, one of the main features of the US market was that it maintained a relatively high P/E ratio, no matter whether measured on a forward looking or historical basis. Thus, a correction in equity prices, even absent the war, would not have been that surprising. The same could not be said about European or Asian markets, which trade at much lower valuations, but then, in Europe especially, prospects for growth remain hampered by individual national domestic policies along with EU wide policies, notably in the energy sector. Under the rubric a picture is worth 1000 words, it is not hard to understand why US equity markets dominate global markets.

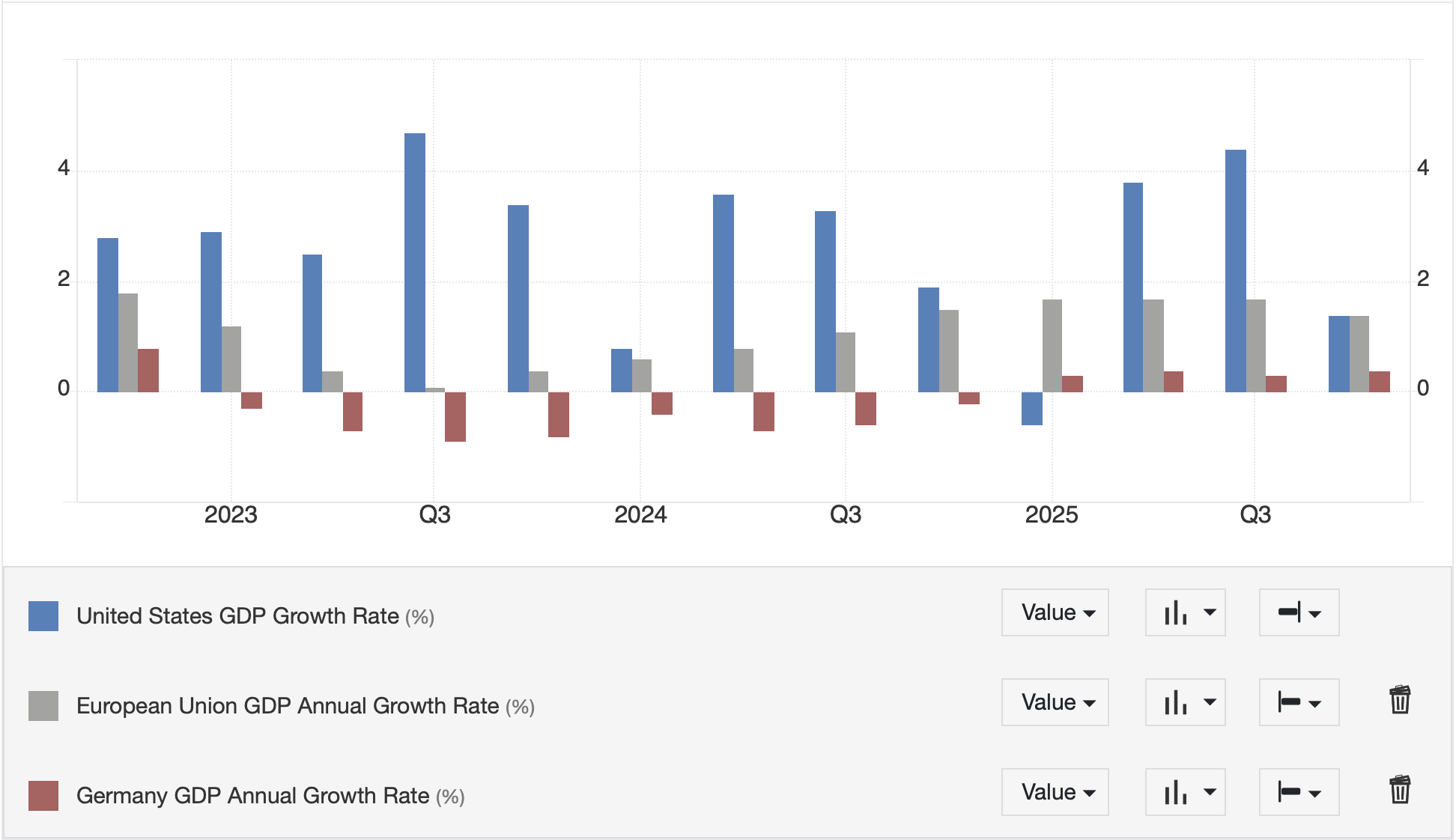

Source: tradingeconomics.com

Germany has averaged -0.3% GDP growth over the past 3 years, and the EU is just above it at +0.4%. Meanwhile, this morning’s UK GDP data showed weaker than expected outcomes, with Y/Y of 0.8% after a stagnant January. Are US markets richly priced? Sure, but what prospects do you have elsewhere?

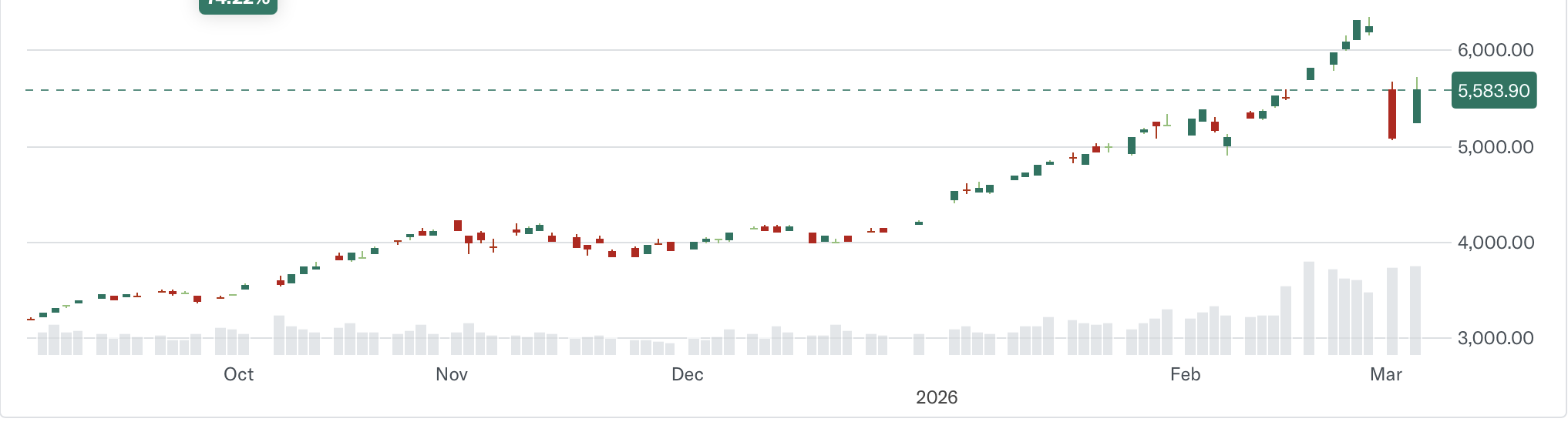

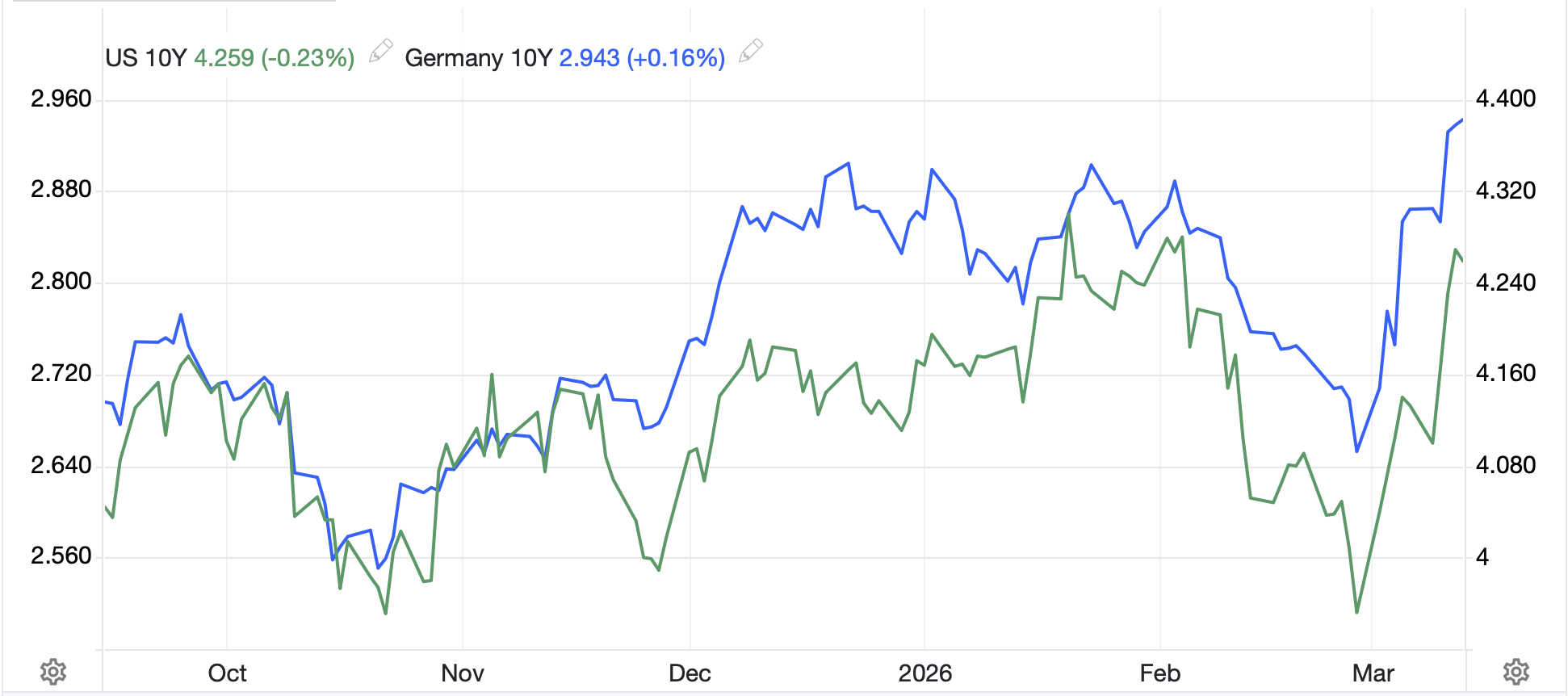

Turning to bond markets, the traditional safe haven appeal of bonds, especially Treasuries and Bunds, is MIA. While this morning, Treasuries (-1bp) and most European sovereigns (-1bp across the board) have seen prices stop declining, the picture over the past two weeks has not been encouraging. The chart below shows the price action in both Treasuries and Bunds and, as you can see, both have seen yields rise sharply since the beginning of the month/war. Given the ongoing stress in oil markets, and the implications that has for inflation worldwide going forward, it should not be a surprise that bonds don’t appear to offer their ordinary haven characteristics.

Source: tradingeconomics.com

The big question here, and around the world truthfully, is how will central banks respond to the rise in energy prices and subsequent rise in headline inflation? If they try to address price pressures by raising rates in this scenario, it will almost certainly lead to recessions everywhere. But will their models allow them to hold their policies if inflation starts to rise sharply? It’s funny, I have been remarking how central bank policies have lost their luster recently, having been overwhelmed by fiscal policies, but suddenly, monetary policy is back in the limelight. We shall see how they perform.

In the commodity markets, WTI (-1.3%) rallied sharply yesterday but is giving back a bit this morning. The big headline yesterday was that Brent crude closed above $100/bbl for the first time since 2022 in the wake of Russia’s invasion into Ukraine. Of course, that was more about the big, round number feature, than the percentage rise. After all, is there really a difference of $98/bbl or $100/bbl in the broad scheme of things? Oil continues to be THE driving factor in all markets right now and that is not likely to change anytime soon. As long as the Strait remains closed to traffic, this pressure will continue to build.

In the metals markets, both gold and silver continue to consolidate around their recent levels ($5100 in gold, $85 in silver) and it appears we are going to need another catalyst of note to get that to change. I see no change in supply metrics, that’s for sure, but if there is a recession, silver demand may well be reduced given its industrial uses.

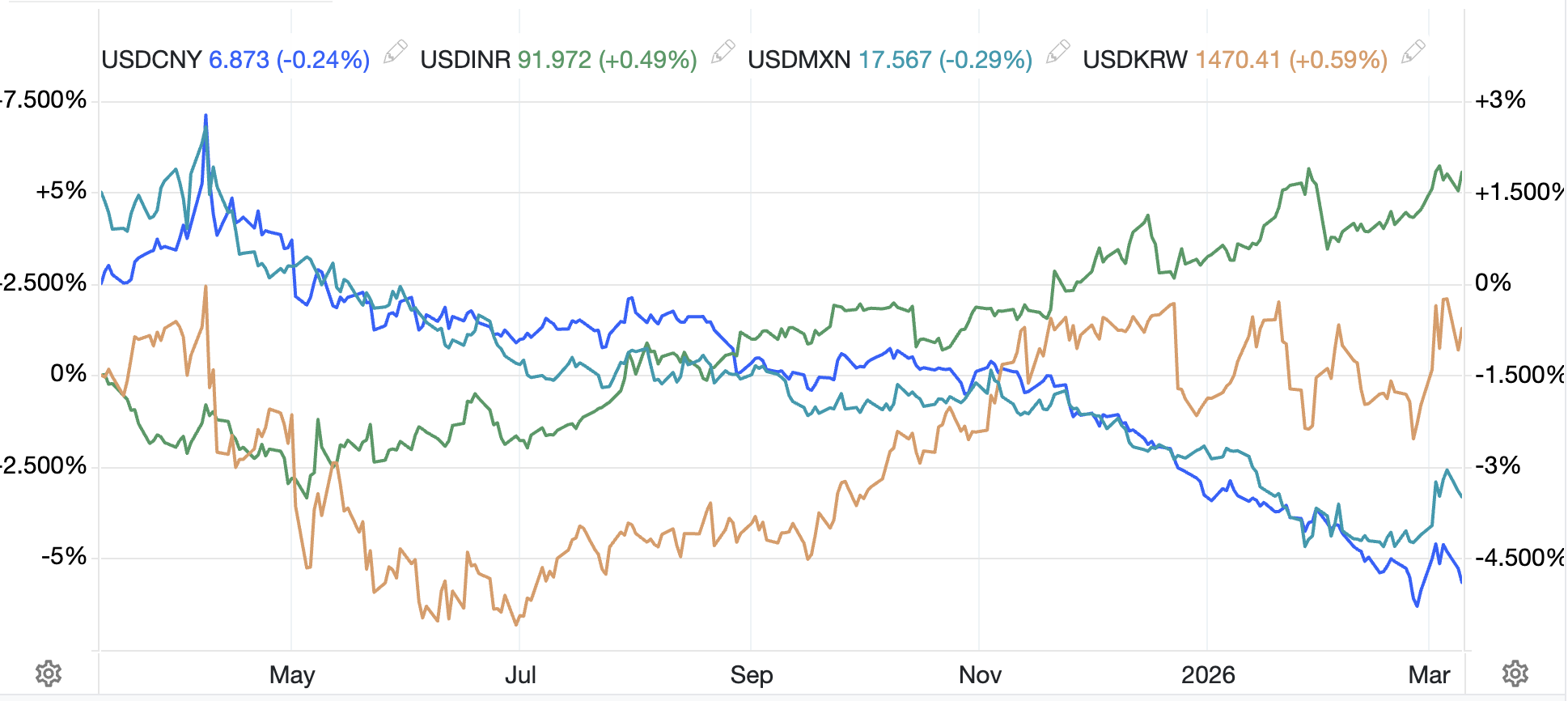

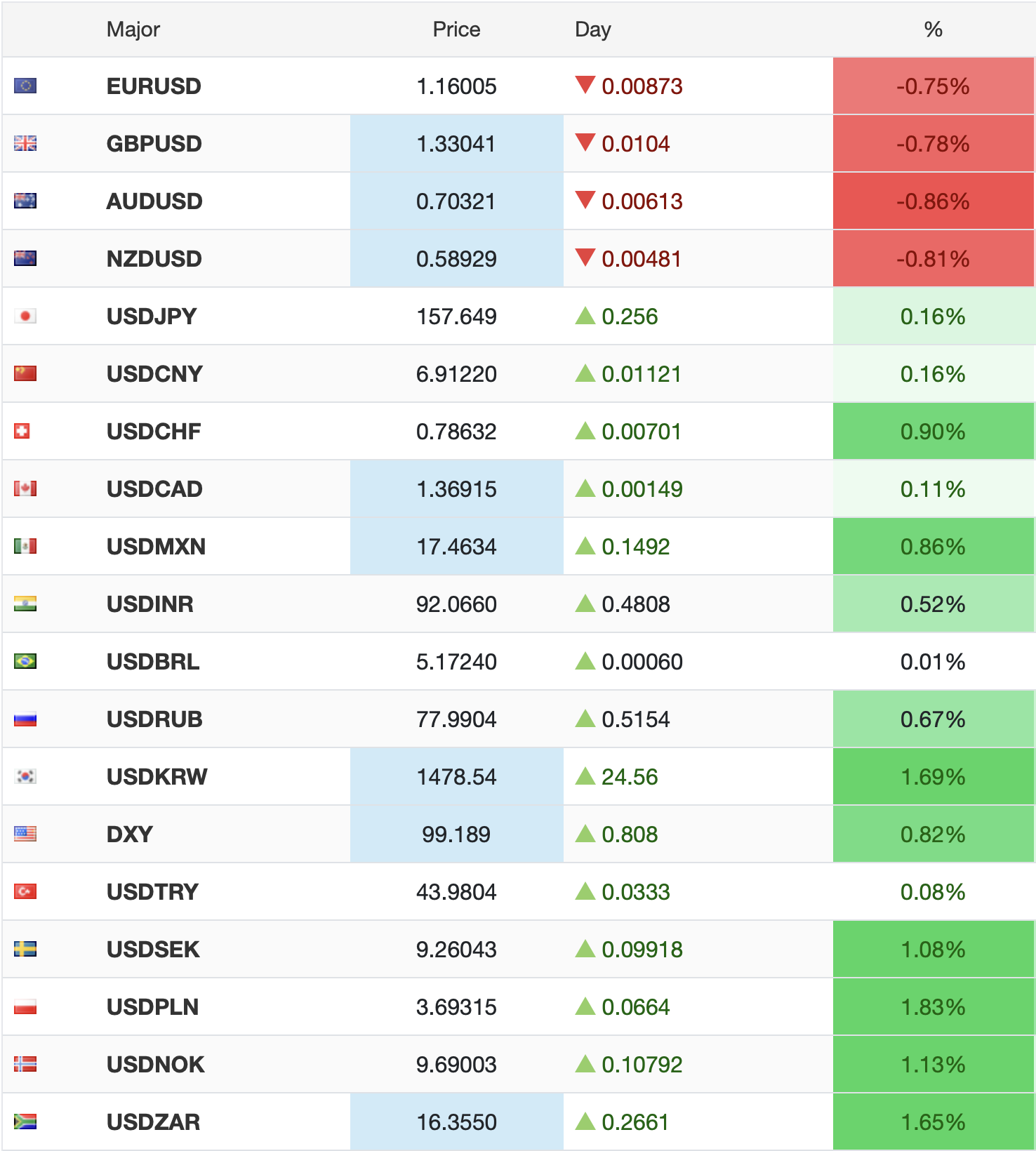

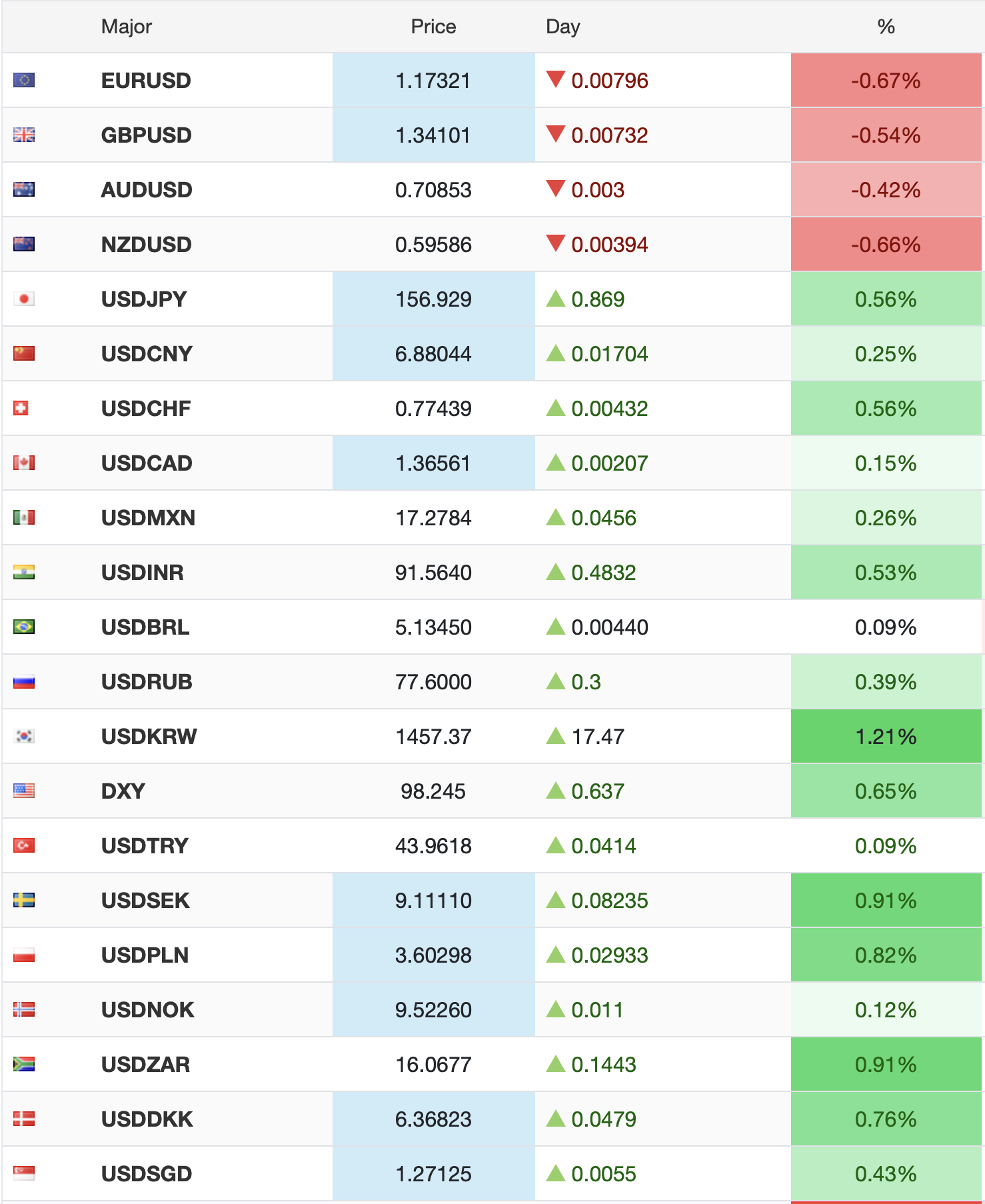

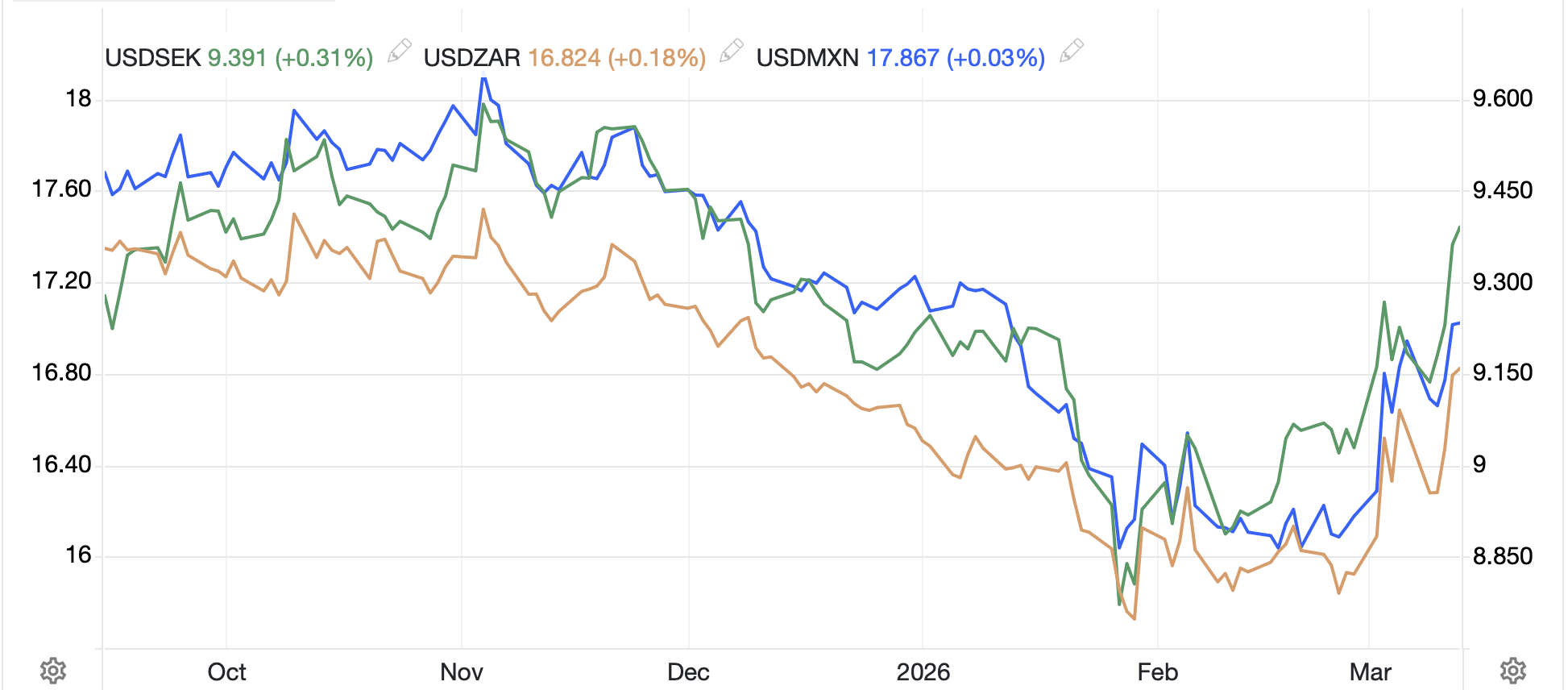

Finally, the dollar is king of all it surveys, at least in the FX markets. The euro is below 1.15 (it seems like only last week that pundits were talking about the consequences of the euro trading above 1.25. The DXY has broken above 100, although we will need to see an extension of this move to be convinced that it is going to head much higher, and USDJPY is now pushing near 160 again, which brought out comments from Katayma-san, the Japanese FinMin, about closely monitoring the yen’s value. Of course, given the broad-based rise in the dollar, the current yen weakness cannot be seen as that troubling.

But what is a bit more interesting to me, and more definitive proof that the dollar is not about to collapse, is the coincident moves higher in the dollar vs. a number of other currencies. Look at the chart below of ZAR (-0.15%), SEK (-0.3%) and MXN (0.0%). Each demonstrates virtually identical trade patterns, and all of them reached their respective peaks (dollar’s nadir) on January 29th. You may recall that was the day president Trump named Kevin Warsh as the next Fed Chair, and we saw a major reversal in stocks, gold, silver and other markets.

Source: tradingeconomics.com

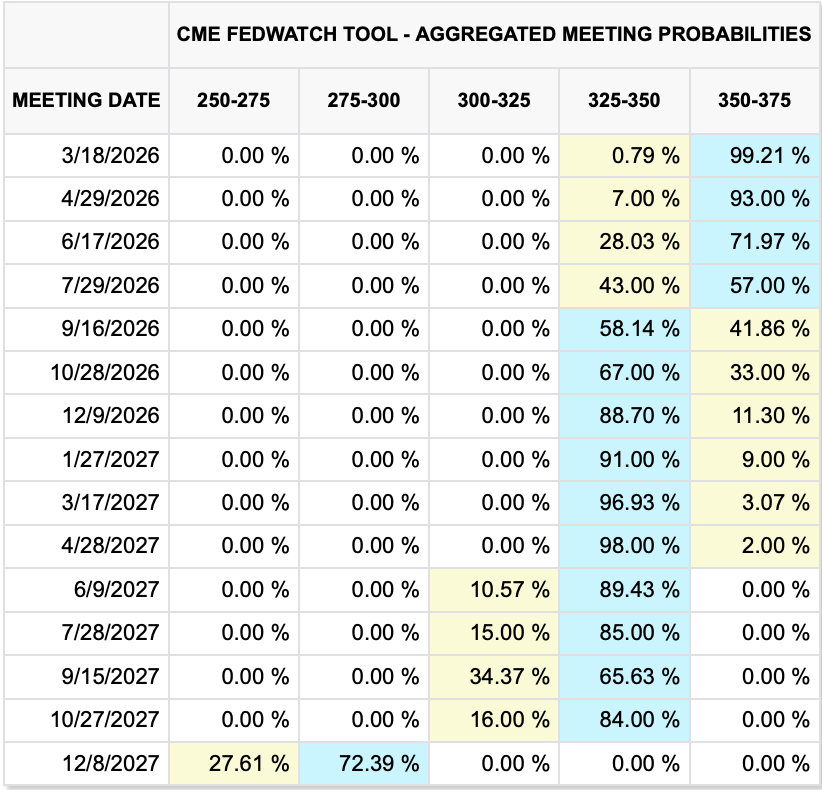

My best estimate is that FX markets are pricing in a tighter Fed at this point, which. Based on Fed funds futures, showing just one cut potentially this year in December, makes a lot of sense. I guess it remains to be seen how other central banks will respond to the ructions in markets caused by the war, but this is the first order consequence.

Source: cmegroup.com

Turning to this morning’s data, we see a bunch as follows:

| Q4 GDP (2nd estimate) | 1.4% |

| Personal Income | 0.5% |

| Personal Spending | 0.3% |

| Durable Goods | 1.2% |

| -ex Transport | 0.5% |

| PCE | 0.3% (2.9% Y/Y) |

| Cpore PCE | 0.4% (3.1% Y/Y) |

| JOLTs Job Openings | 6.7M |

| Michigan Sentiment | 55.0 |

Source: tradingeconomics.com

As with Wednesday’s CPI data, the PCE data does not include the war, so will be dismissed. My take is the Income and Spending numbers, and the JOLTs number will be the most impactful if they are a long way from estimates.

And that’s where we stand. Markets are still unsure of what to believe regarding the war, and when it comes to war, things happen that are unexpected all the time, the so-called unknown unknowns. In the end, it is hard to bet against the dollar for right now, but that could change in an instant based on the next headline.

Good luck and good weekend

adf