Investors have been inundated

By news that has been unabated

There’s tariffs and war

Plus rate cuts and more

With stocks and bonds depreciated

Now looking ahead to today

The payroll report’s on its way

As well, later on

With nothing foregone

We’ll hear from our own Chairman Jay

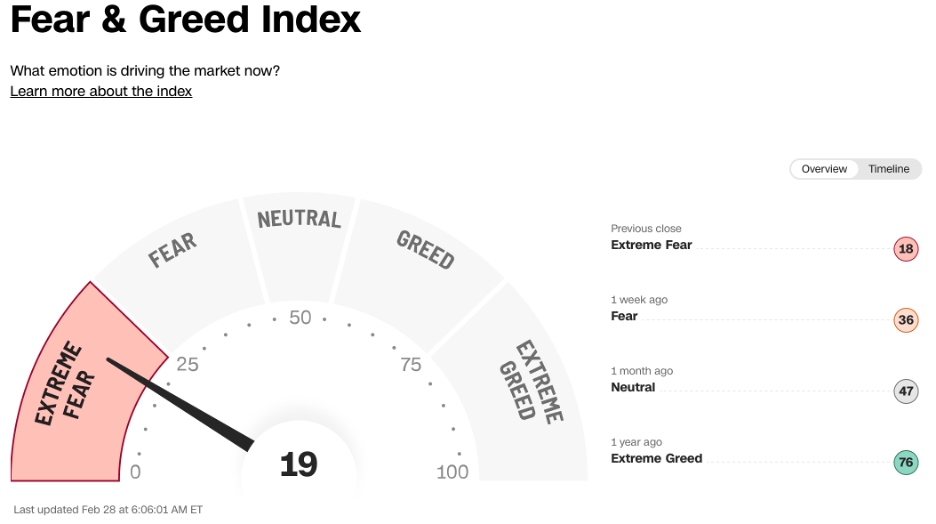

It has certainly been an interesting week in both markets and the world writ large. So much has happened and yet so much is still unclear as to how things may evolve going forward. Through it all, volatility is the only constant. To me, what has become abundantly clear is the post WWII order is being dismantled, and every nation is trying to determine its place in the future. This is a grave threat to those who benefitted from flowery words and limited action, which covers a wide swath of government leaders around the world. I’m not sure if this is the 4th Turning, or if this is merely the prelude, with the impacts of all these changes what brings the 4thTurning about. Regardless, history is clearly in the making.

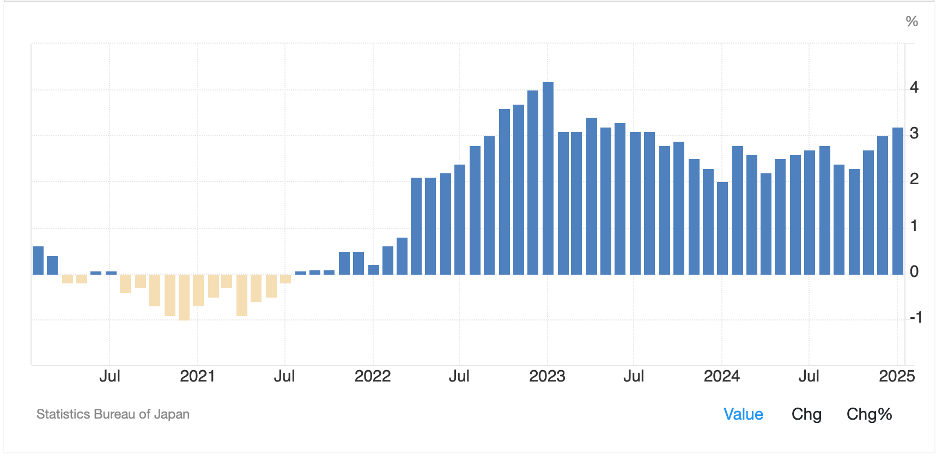

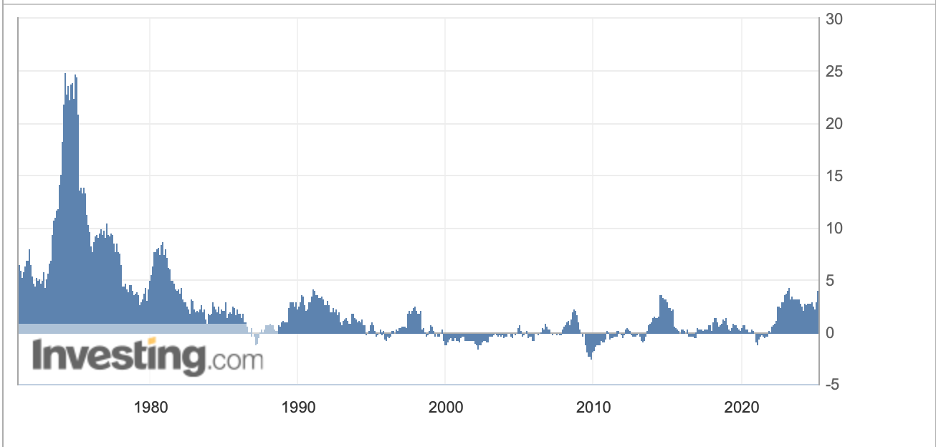

I do not have the bandwidth to continuously follow the tariff story, although yesterday’s news was there will be more delays for both Canada and Mexico. China received no such relief and at their National People’s Congress they seemed resolute in their pushback and highlighted their own achievements. The data from China, though, tells me that their goals for more domestic consumption remain far in the distance. Last night they reported their Trade Balance for the January/February period (they always combine because of the Lunar New year disruptions) and it jumped to $170.5B, far greater than anticipated. While exports underperformed slightly, growing only 2.3% compared to a 5% estimate, it was the imports that really tells the story. Imports fell -8.4%, a significant shortfall from both last year and consensus estimates, and an indication that the Chinese consumer is not yet the type of force that President Xi would like to see.

In fact, a look at the chart below showing imports for the past 10 years demonstrates that very little has changed on this front. As I wrote yesterday, converting a mercantilist economy into a consumer-focused one is a huge lift, and one that the CCP has not yet figured out. It is not clear that they ever will. Meanwhile, the obvious explanation for the huge jump in the trade balance was companies pre-ordering things to get ahead of the tariffs.

Source: tradingeconomics.com

Moving on to the Ukraine situation, while yesterday’s news was of the “whatever it takes” moment for defending Europe, this morning it seems there are some caveats attached. Of course, the first caveat is the changing of the German constitution to allow them to spend all that money. The second seems to be that not every European nation is on board for the massive spending increase and continuation of the war. There are many political and financial hurdles to overcome in this story in Europe, and this morning’s European equity markets are indicative of the idea that this is not a straight-line higher. In fact, every equity market in Europe is lower this morning, led by the DAX (-1.5%) although with solid declines elsewhere as well (CAC -1.0%, FTSE 100 -0.5%). This, too, is a story with no clear end in sight. One unconfirmed story I saw was that the group convened by the UK last weekend has not been able to agree terms for additional support.

Meanwhile, yesterday the ECB cut their short-term rates by 25bps, as widely expected, with the Deposit Rate now down to 2.50%. The funny thing is nobody really noticed. This is of a piece with my observation that central bankers just don’t have that much sway on market activity these days, it is all about politics and statecraft, not monetary policy. This morning, Eurozone GDP for Q4 was released at 0.2%, a tick higher than forecast but still lower than Q3’s 0.4%. There is no doubt the financial mandarins of Europe are keen to get this defense spending going, because otherwise they will continue to preside over a stagnant economy.

But here’s an interesting thing to consider. Germany has made a big deal about this new willingness to spend €500 billion outside the bounds of their budget framework on defense. However, they continue with their Energiewende policy which has been the Achilles Heel of the German economy and will prevent them from actually producing armaments if they seek to continuously reduce fossil fuel powered energy for renewables. It is almost as if this is theater, rather than policy, but that may just be my cynicism speaking.

Moving on to the US, this morning brings the Payroll Report with the following current median estimates:

| Nonfarm Payrolls | 160K |

| Private Payrolls | 111K |

| Manufacturing Payrolls | 5K |

| Unemployment Rate | 4.0% |

| Average Hourly Earnings | 0.3% (4.1% Y/Y) |

| Average Weekly Hours | 34.2 |

| Participation Rate | 62.6% |

Source: tradingeconomics.com

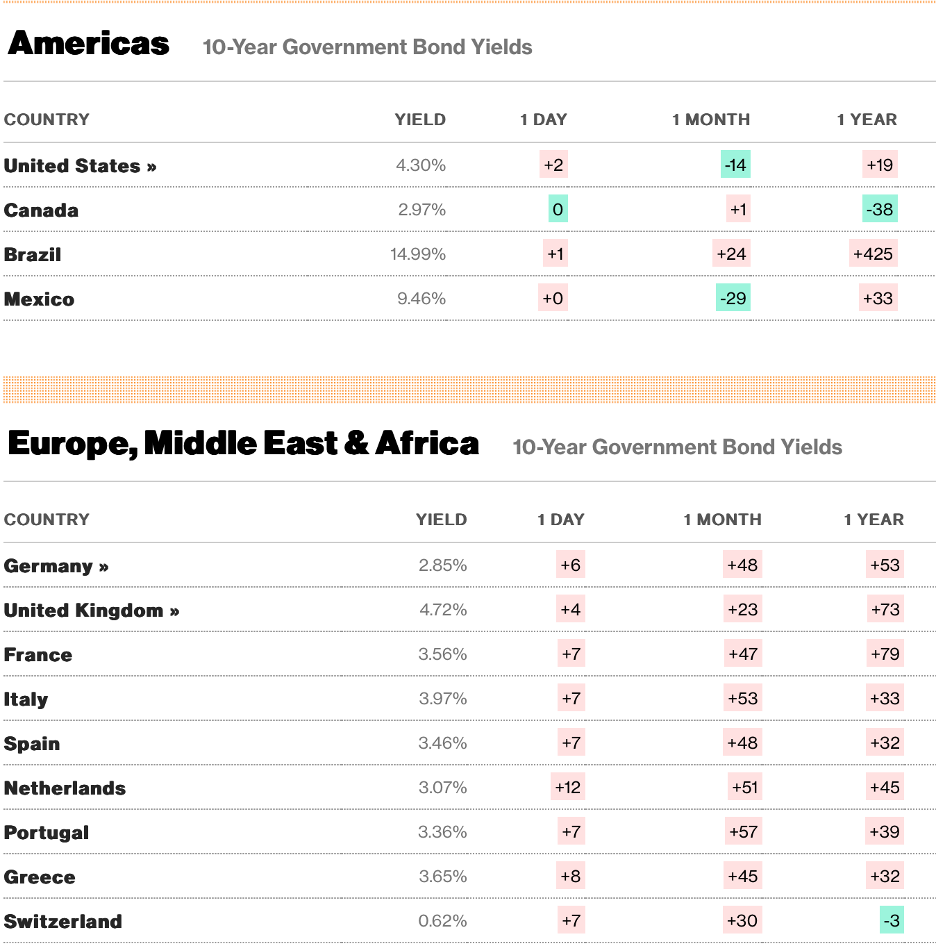

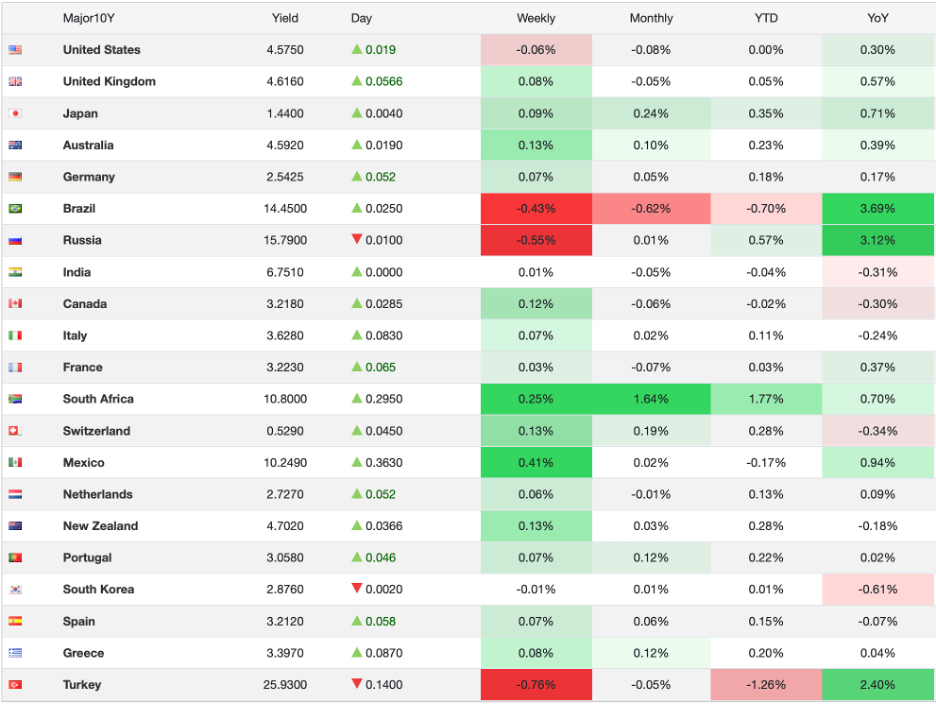

As well, we hear from Chairman Powell at 12:30pm, along with Bowman, Williams and Kugler in the hours leading up to that. But again, I ask, do they matter to the markets right now? Certainly, there is much discussion that the US economic data is starting to show more weakness, and there are many who are saying that long-anticipated recession is going to become evident. If that is the case, we could certainly see the Fed cut rates, but again, my take is markets are far more attuned to 10-year yields than Fed funds. And remember, while 10-year yields are clearly quite inflation sensitive, what we also know that questions over budget deficits and supply are critical to their pricing as well. This was made evident yesterday in Germany.

I have glossed over market activity overnight so will give a really short update here. Yesterday’s weakness in the US was followed by broad weakness throughout Asia, with most markets there lower on the day, notably Japan (-2.2%), but declines almost everywhere. We have already discussed European bourses and at this hour (7:30) US futures are basically unchanged ahead of the data.

In the bond market, Treasury yields are slipping back -3bps this morning and we are seeing similar price action across most of Europe although Spain (+1bp) is bucking the trend on some domestic issues. It is easy to believe that the Germany story was a bit overblown, and remember, if they cannot change the constitution, I expect a rally in Bunds (lower yields) along with a selloff in the DAX and the euro.

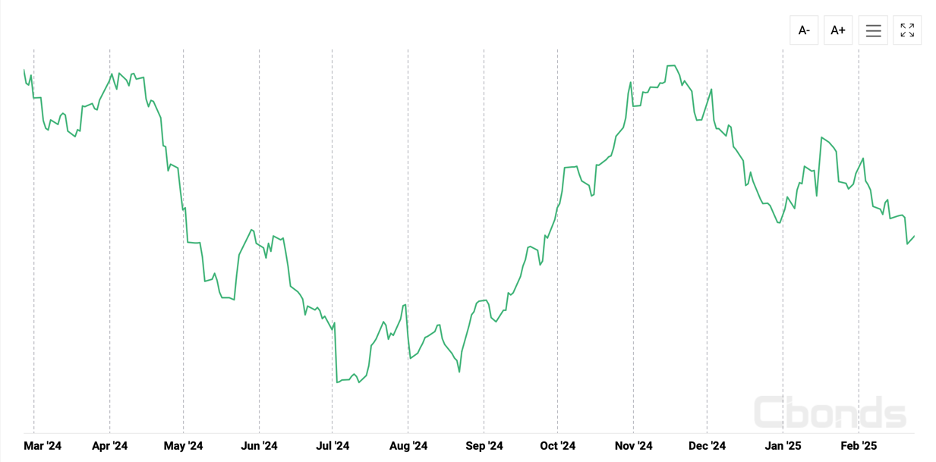

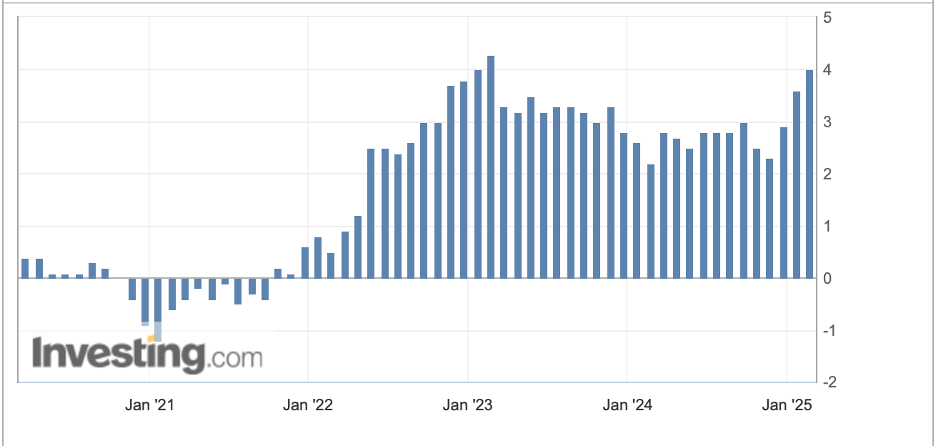

Speaking of the euro, it is continuing its sharp ascent, up another 0.6% this morning. however, something to keep in mind regarding all the huffing and puffing about the euro is that with this sharp move higher in the past week, it is merely back to the middle of its 3-year trading range. So, is this as big a deal as some are saying?

Source: tradingeconomics.com

But the overall currency picture is more mixed with both AUD (-0.6%) and NZD (-0.5%) lower along with CAD (-0.2%). There are other gainers (GBP +0.2%, SEK +0.7%) and other laggards (ZAR -0.2%) although I would say the broad direction is still for dollar weakness.

Finally, oil (+1.5%) is bouncing this morning, although this could well be a trading bounce as I have seen no new news on the subject. I guess the delay on Canadian tariffs probably played a role as well. Gold (+0.4%) is also firmer although both silver (-0.4%) and copper (-1.2%) are lagging. In fairness, the latter two have had significant up weeks so are likely seeing some profit taking.

Once again, I will remark that for those who have real flows and exposures, the current market situation is why hedging is critical to maintain financial performance. Nobody really knows where anything is going to go, but right now, it feels like the one thing we know is prices will not remain where they currently are for very long.

Good luck and good weekendAdf