The war in the Gulf shows no sign

Of ending by any deadline

Some victims now bleeding

Are bonds, with yields speeding

To levels no longer benign

Already we’ve seen, efforts, great

By nations, impacts, to abate

So, price caps on gas

Worldwide came to pass

But will central banks raise their rate(s)?

Nothing of note has changed in the Iran war as the US continues to refrain from further attacks while negotiations to end the conflict ostensibly continue. Both sides have made their demands, but from what I have read about them, neither side can accept the others wishes. If pressed, my take is the ongoing US pause is simply allowing the Marines and 82ndAirborne to get into place for their attempt to take over and control Kharg Island and the other small islands in the Strait. Frankly, I would not bet against their tactical success in that endeavor. However, it is not clear how Iran will respond in that situation. After all, if the US does control Kharg Island, that means Iran no longer controls their own revenue stream, and that is truly existential for the regime. However, I could be completely wrong about this, which is why I am not a military strategist.

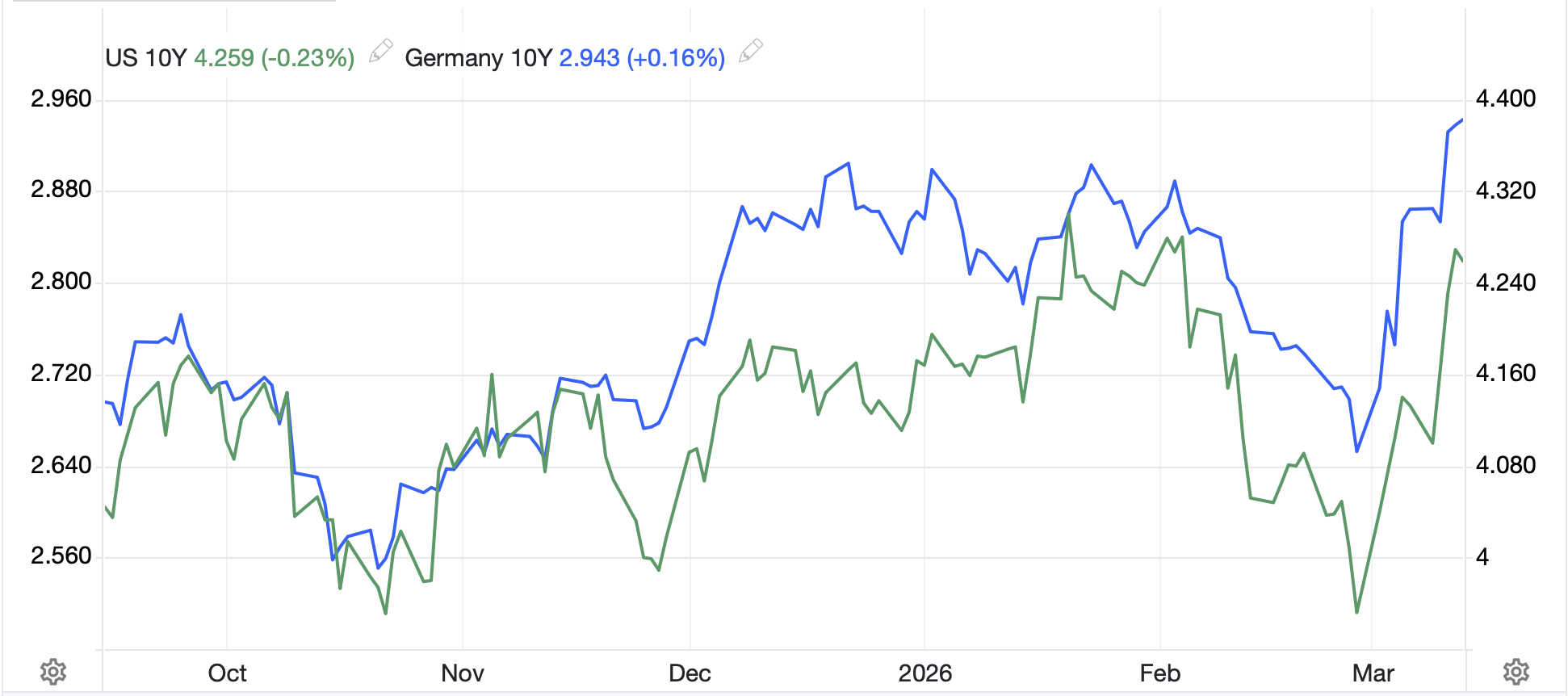

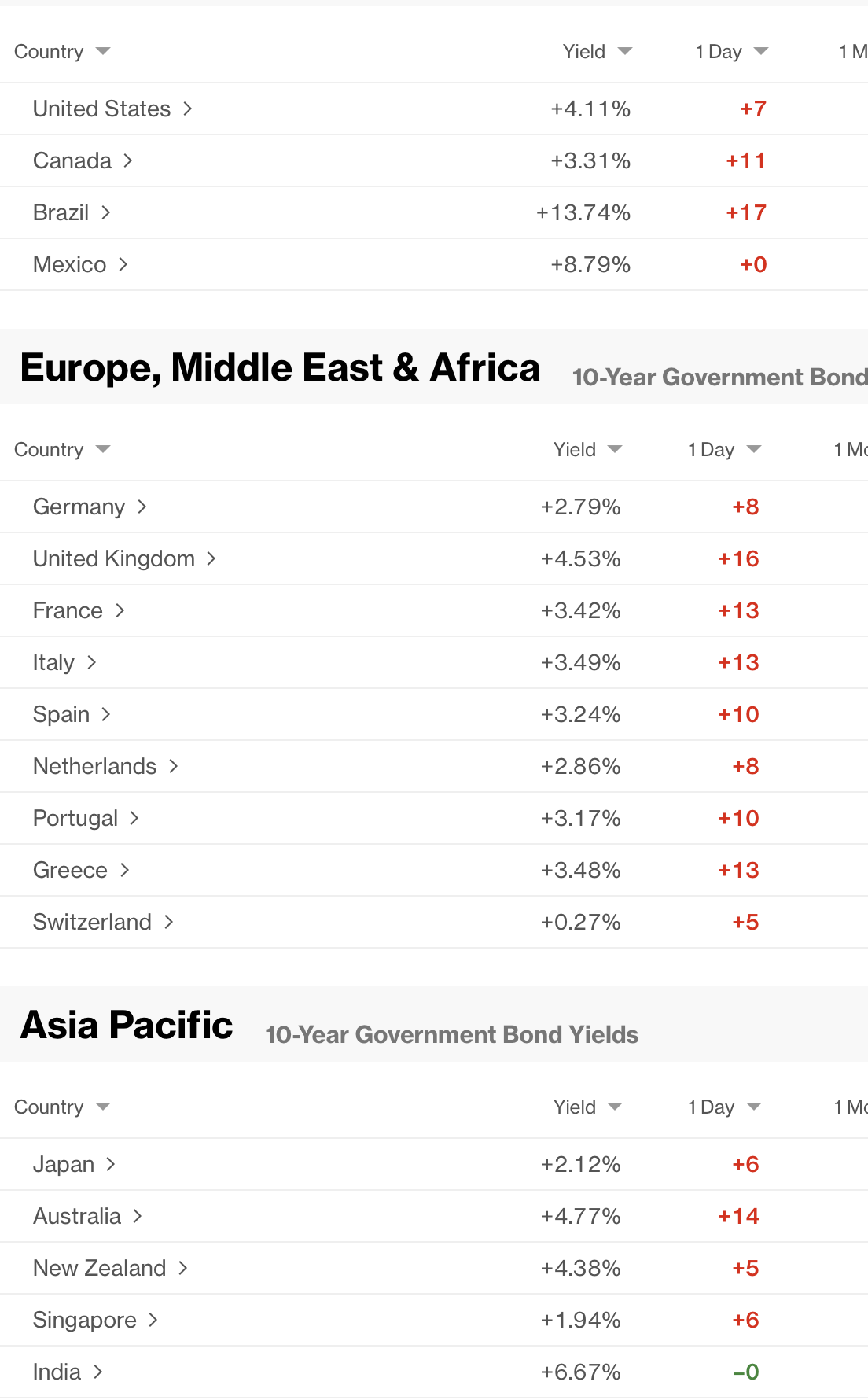

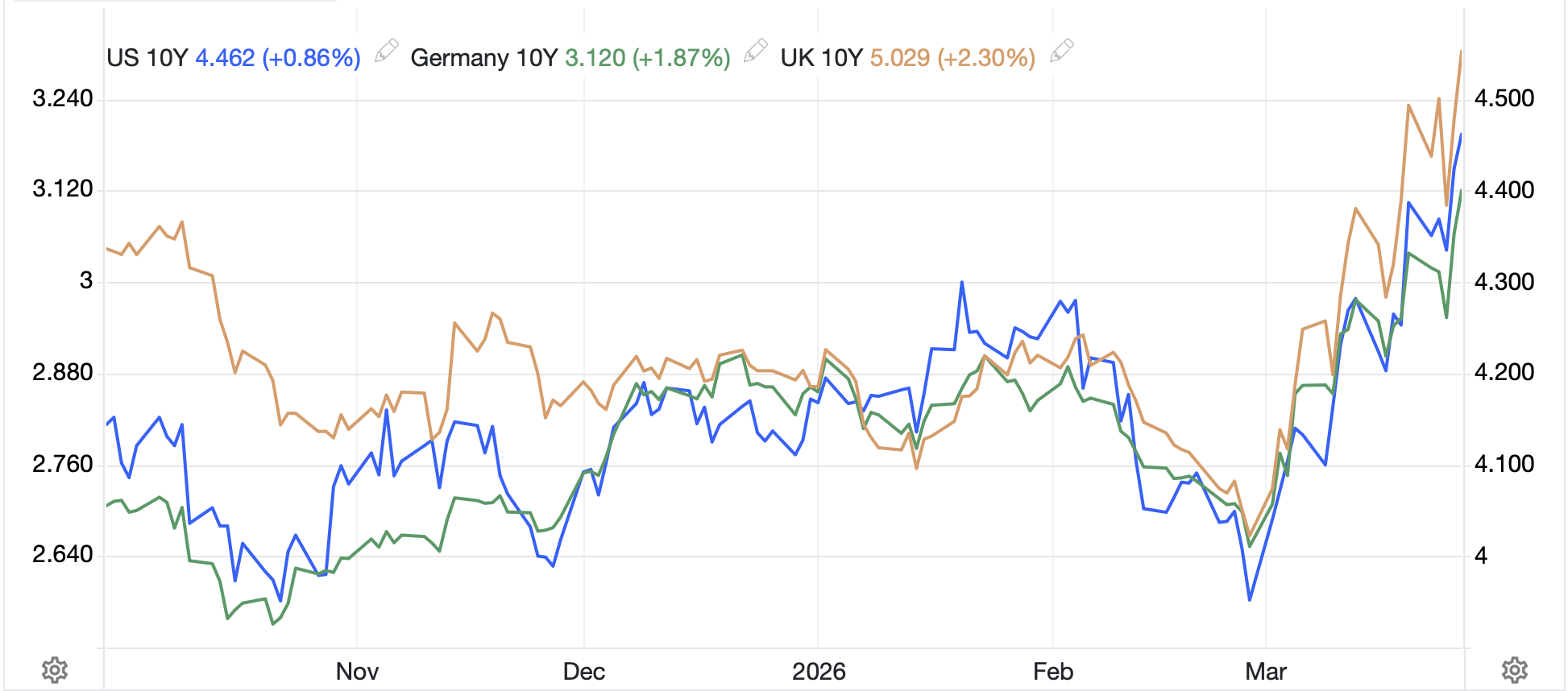

But I think it is worthwhile taking a peek at the bond market this morning. For the first few weeks of the war, while yields edged higher, there was no indication that investors were getting terribly nervous about the longer-term impacts of the war. However, that no longer seems to be the case. I have several charts below showing US, UK and German 10-year yields over the past six months, and then a longer-term perspective showing those same yields over the past 20 years.

Six months of yields

Source: tradingeconomics.com

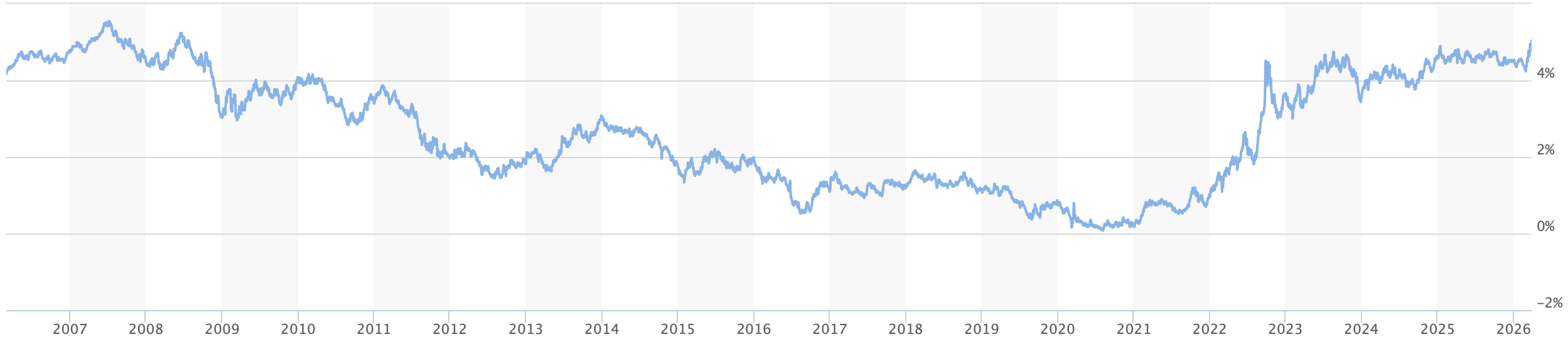

Long-term charts (source marketwatch.com)

UK Gilts

German bunds

US Treasuries

As you can see from the first chart, yields across all three of these nations have risen sharply now in the past month. In fact, the numbers are US (+52bps), UK (+83bps) and Germany (+47bps). It is very clear that fixed income investors are getting worried, and reasonably so given the idea that inflation readings, at least in the short-term, are going to be much higher. As to the longer-term view, though there is certainly a similarity amongst the movement of yields of all three nations, UK yields are currently at their highest level since the GFC, July 2008; German yields are at their highest level since the Eurozone bond crisis in 2011, but Treasury yields were higher at the beginning of this year, and 25bps higher in late 2023.

This is not to dismiss the potential problems that may arise if government bond yields continue to rise, especially given the already extraordinarily high debt/GDP ratios that exist throughout the G10. However, I am not prepared to concede that the US is going to collapse because 10-year yields are back at 4.50%.

What we have seen, though, almost everywhere in the world, is government attempts to cap prices on energy, whether gasoline, diesel or even electricity, to help moderate some of the obvious pain that higher energy prices are inflicting on their populations. We have also heard a great deal from central bankers about needing to tighten monetary policy to combat the rising inflation, despite the fact that inflation is coming from a supply shock in energy rather than either excess demand or money supply. I fear that will not work out that well if they do so, but as is often the case, central banks (and governments in general) feel they must “do something” when an exogenous event, out of their control, occurs. Ultimately, history has shown that is when policy mistakes are made. Here’s hoping the hostilities end quickly enough so nations don’t make those mistakes.

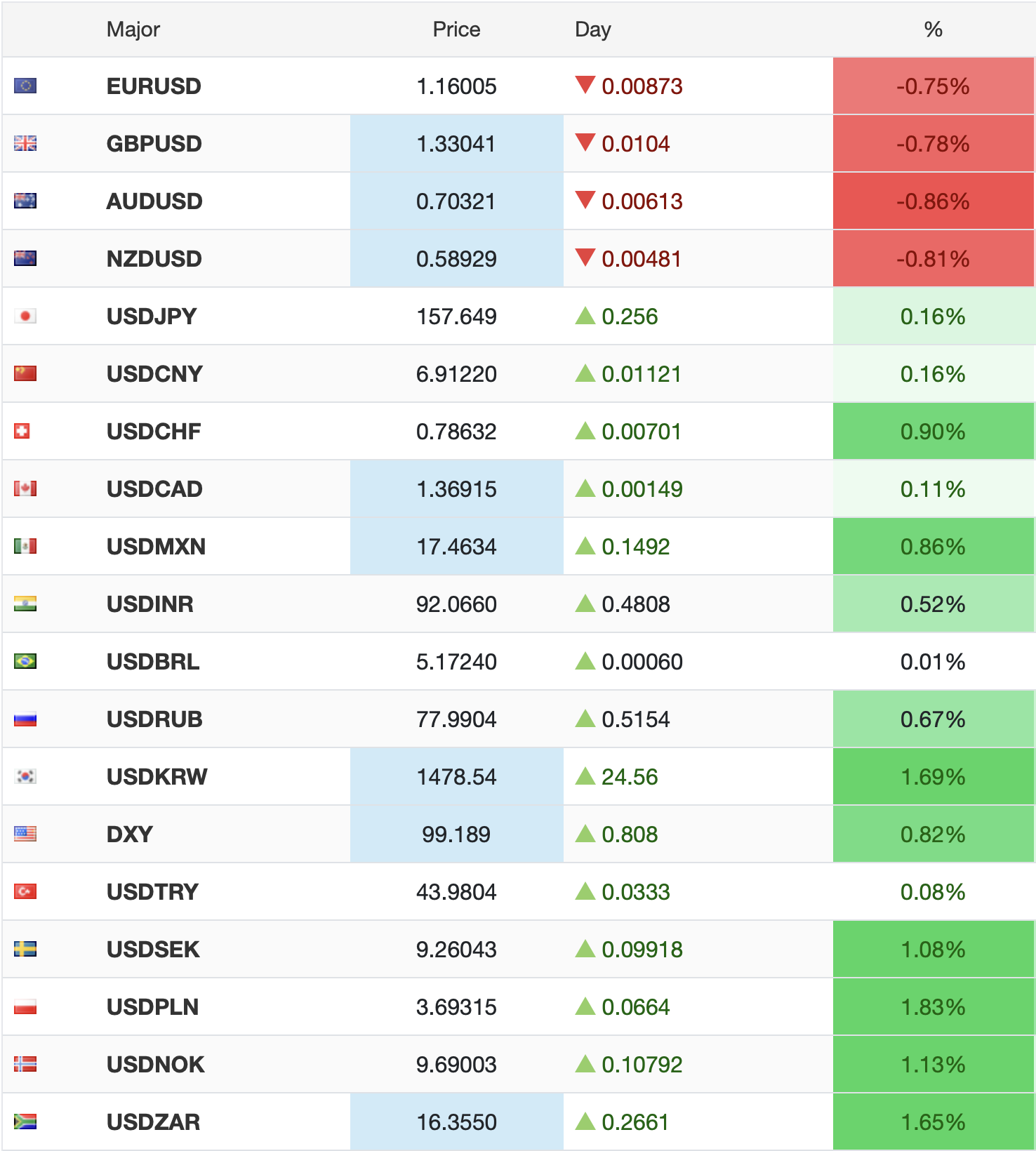

Away from bonds, with yields higher this morning across the board (US +5bps, Germany +5bps, UK +11bps, Japan +11bps) and the rest of the European sovereigns somewhere in between, if we turn to oil (+2.7%), WTI is pushing back up to $100/bbl this morning, which I take as an indication market participants are getting nervous things will last longer than they thought a few days ago. You can see the chart below that oil has rallied steadily all week since the Tweet that things were going to be ending soon back on Monday.

Source: tradingeconomics.com

The more interesting price action to me, this morning, is that gold (+0.7%) is also higher this morning, which may be the first session since the first day of the attacks, where both have risen in sync. There is a story around that Turkey sold 58 tons of gold right when things began, but even at $5000/oz, that is only about $9 billion of gold compared to average daily trading volumes of between $200 billon and $300 billion (according to Grok). My point is that would not be enough to move markets like we have seen in gold, but it could well be a harbinger of what other nations did as well. Again, there is no sense that the long history of gold’s role is changing here.

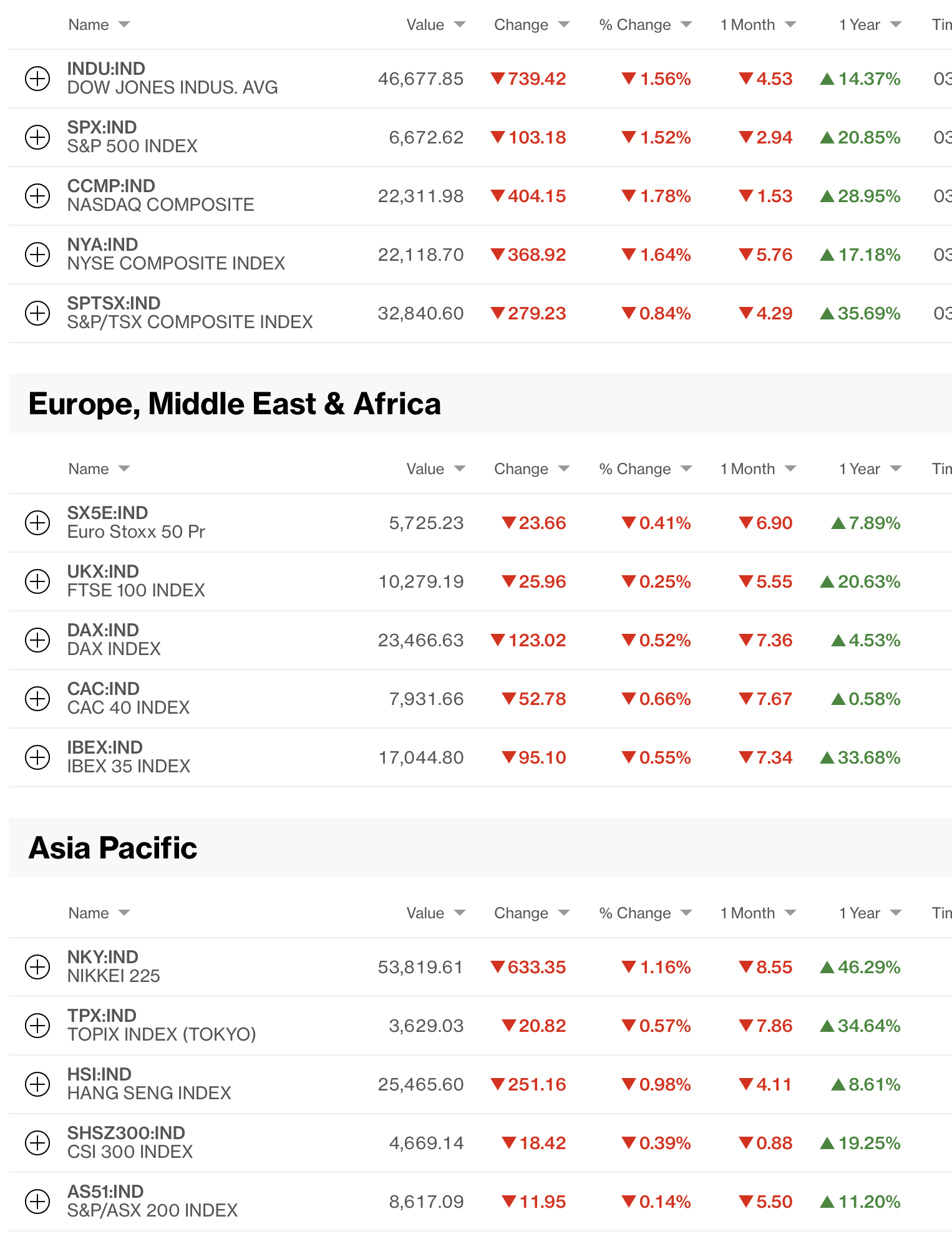

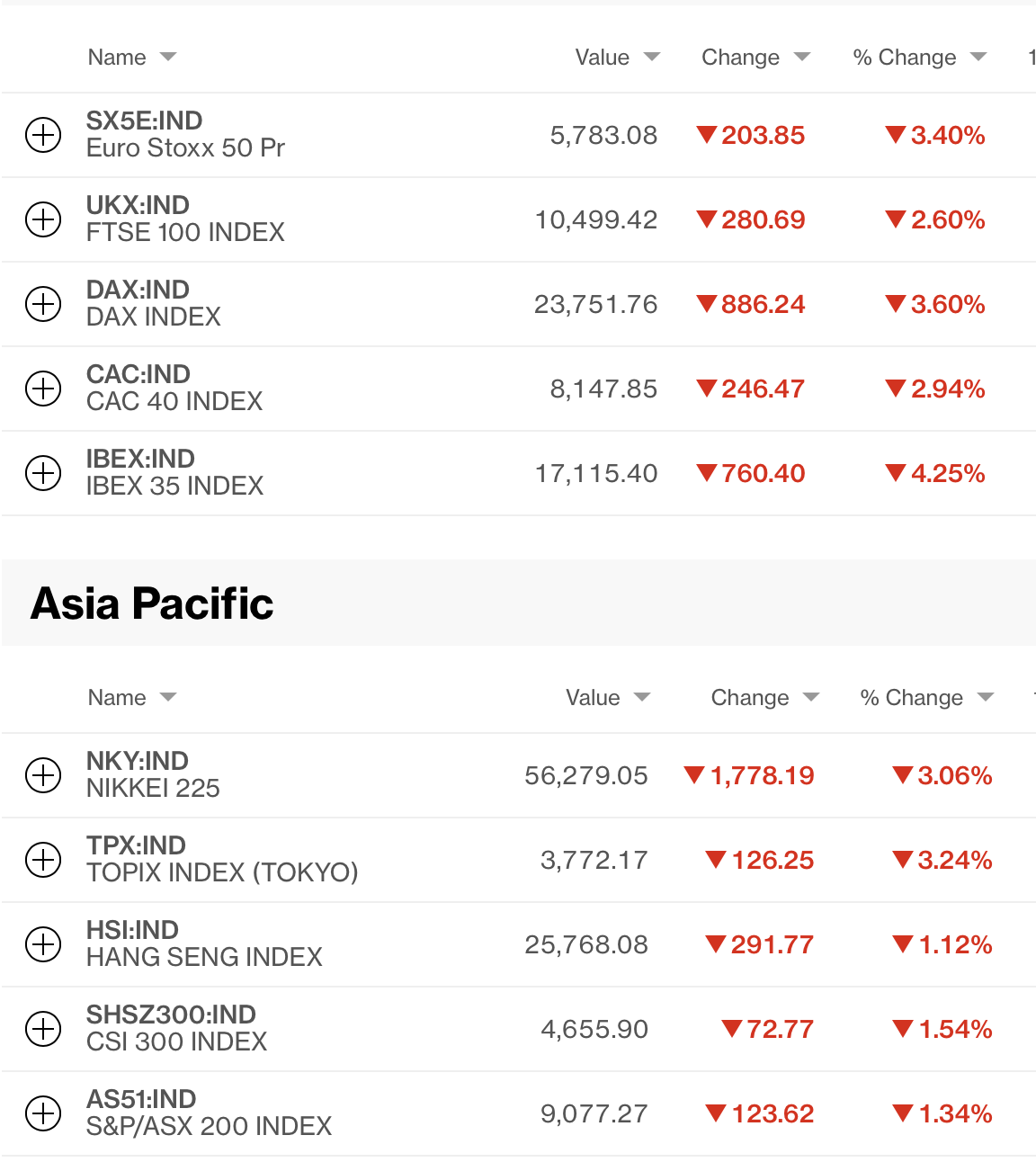

As to equity markets, yesterday’s weakness in the US has been followed across Europe (DAX -1.6%, CAC -1.1%, FTSE 100 -0.75%, IBEX -1.4%) but the picture in Asia was more nuanced. While the Nikkei (-0.4%) slipped a bit, both China (+0.6%) and HK (+0.4%) managed to rally as did Malaysia, Singapore and Thailand albeit not very much. On the downside, though, India (-2.2%) made up for the fact it was closed on Thursday, while Korea (-0.4%) and Taiwan (-0.7%) both slipped and the rest of the region edged lower by lesser amounts. As to US futures, at this hour (7:30) they are lower by about -0.35%.

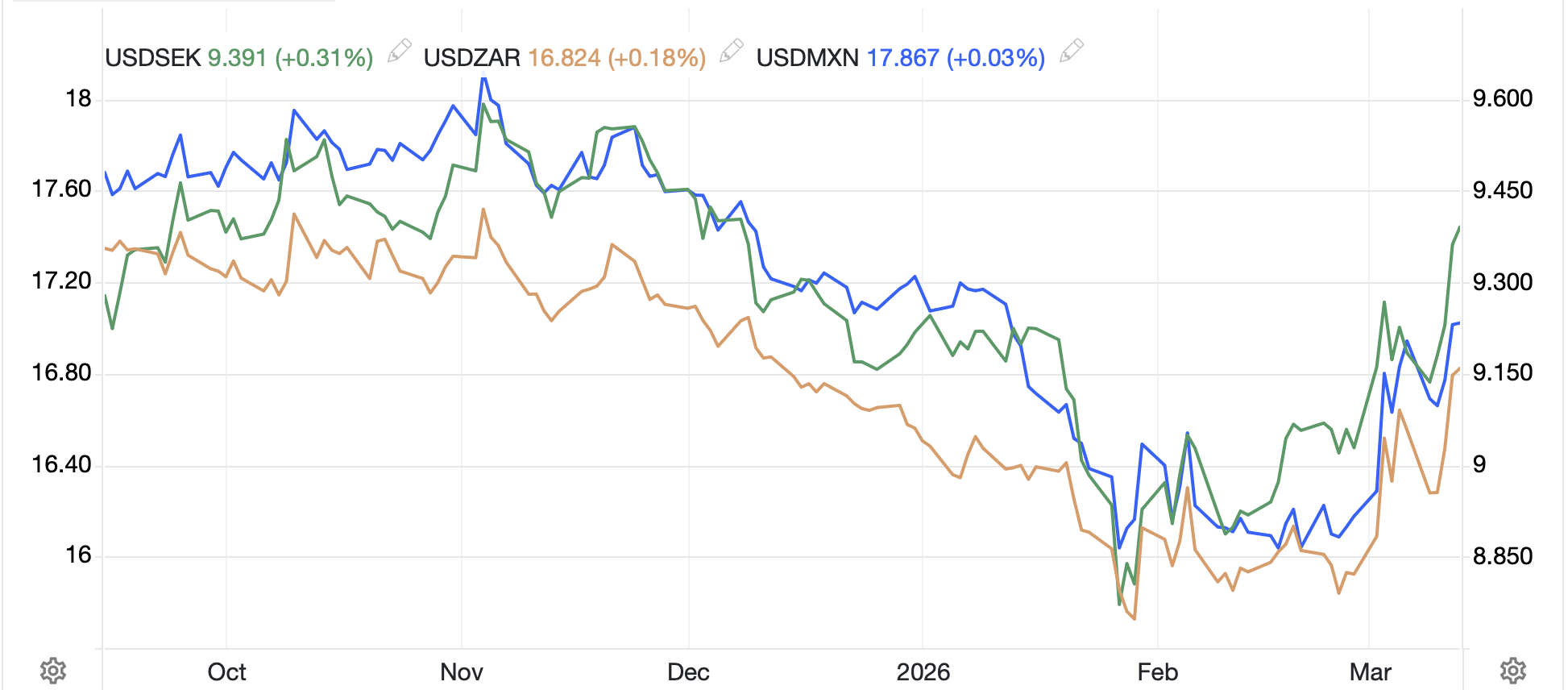

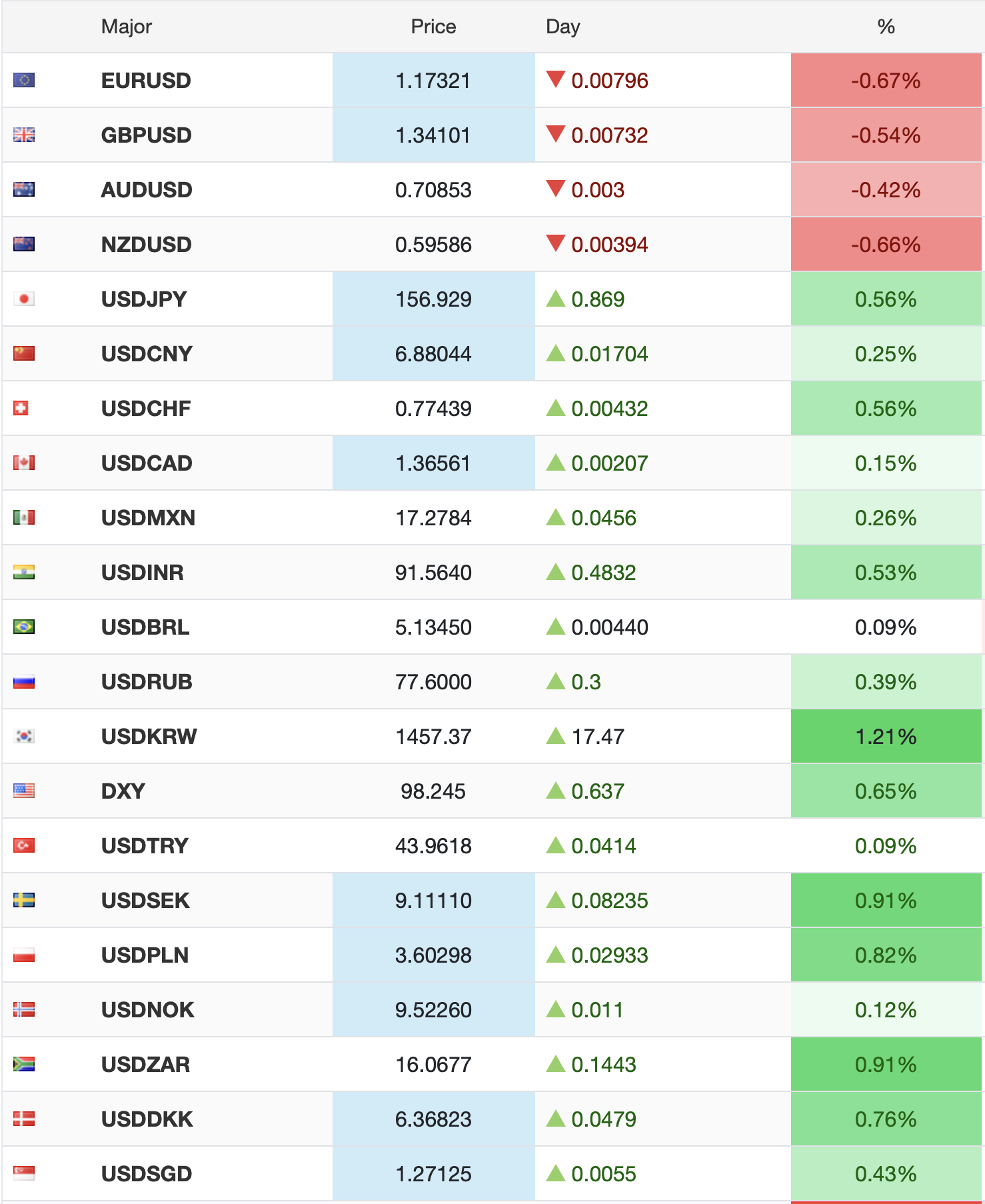

Finally, the dollar continues to be a major beneficiary of the war as the DXY is back above 100 this morning with several EMG currencies coming under greater pressure today. We see CLP (-1.1%) feeling the pain of copper’s inability to rally at all, as well as INR (-0.6%) and MXN (-0.5%) suffering this morning. NOK (+0.2%) continues to benefit from oil’s recent strength, and CAD (+0.1%) is holding its own on the same basis, but both the euro (-0.15%) and pound (-0.2%) are struggling as the energy problem there is a major detriment to their economies.

The only US data this morning is Michigan Sentiment (exp 54.0) while yesterday’s Jobs data continues to show that layoffs are not increasing in any meaningful way, which I believe is a result of the dramatic change in immigration policy as well as deportations. Like so much of what is ongoing these days, old models regarding the labor market are no longer representative of the new reality on the ground. I suspect this is true across large segments of the economy which just means that relying on econometric models will be a fraught exercise going forward. Here is a reason to pity the central bank community as they are truly flying blind now.

And that’s all there is today. To me, we are biding our time until the Marines land on Kharg Island and then we will see a new phase of the war. It is a high risk, high reward venture as success would certainly reopen the Strait of Hormuz and oil prices would plummet quickly. Failure, however, would leave Iran with greater control over that key chokepoint and potentially cause greater difficulties elsewhere in the world, not least because it would call into question the US ability to project power. War is not only hell, but also incredibly risky.

Good luck and good weekend

Adf