The talks twixt the States and Iran

Collapsed like a climate straw man

Now there’s a blockade

In Hormuz, arrayed

As Trump pivots to a new plan

The first move in oil was higher

But I would beware as a buyer

If Trump rules the Strait

That could be checkmate

And force a much longer cease fire

As of 8:00pm last night, after the peace talks fell apart in Islamabad and President Trump announced the US would be blockading the Strait of Hormuz so no ships carrying oil, especially Iranian oil, would be able to pass the blockade, the price of oil spiked immediately as the futures markets opened. You can see the last week’s roller coaster in the below chart from tradingeconomics.com

The question that needs to be answered at this point is, is there a substantive difference between the US blocking traffic in the Strait and Iran doing so? I would contend there is a huge difference, especially if you are China. But also, if you are Iran. After all, you just lost your trump card (pun intended) and not only that, if Iranian oil is not able to be sold, then Iran runs out of money pretty quickly. Remember, oil revenues represent approximately 90% of Iranian total revenues. How long can the IRGC last with no money to pay their soldiers?

In the meantime, the Saudis are pumping 7 mm bpd across the East-West pipeline now, and the UAE is pumping 1.5 mm bpd to Fujairah, taking a decent sized bite out of the missing barrels. I read this morning that upwards of 7mm bpd are now exiting the gulf via pipeline reducing the overall reduction in oil flow. Granted, it is still a huge disruption but shrinking. On top of that, if this continues, the Strait loses its strategic importance, which cements Iran’s loss of power. In the short-run, oil prices can go in either direction in my view, but this has the opportunity to completely emasculate Iran’s ability to have an impact on the global oil markets in the future.

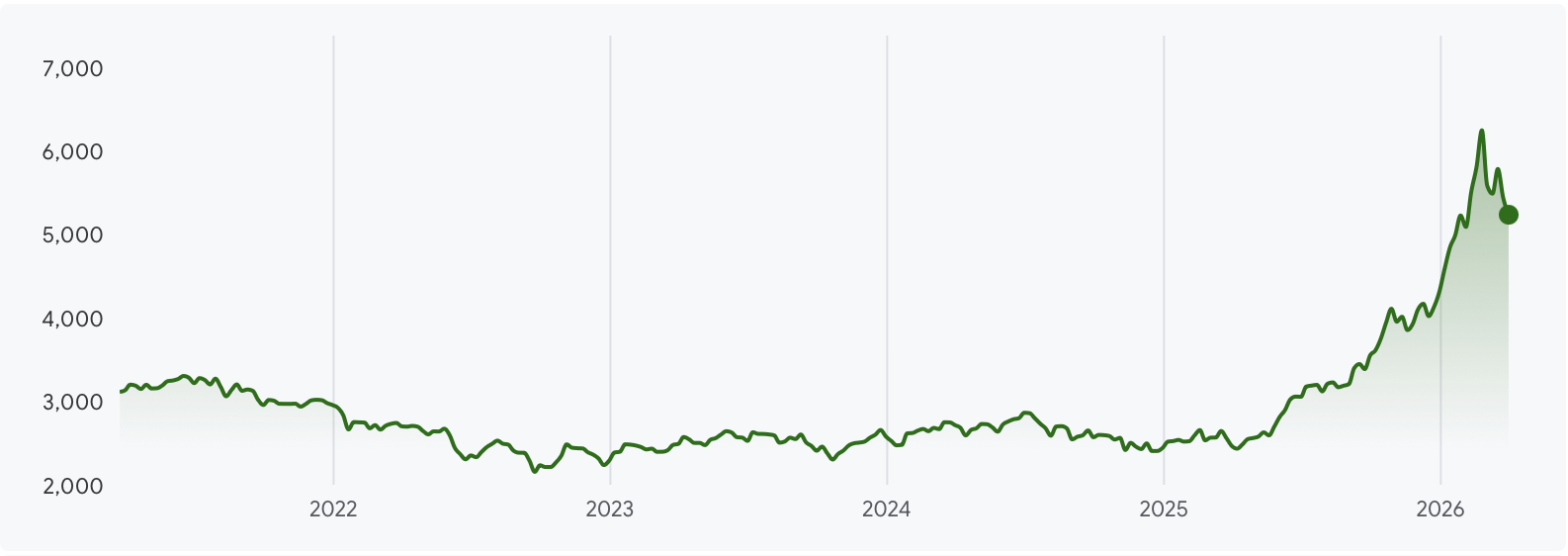

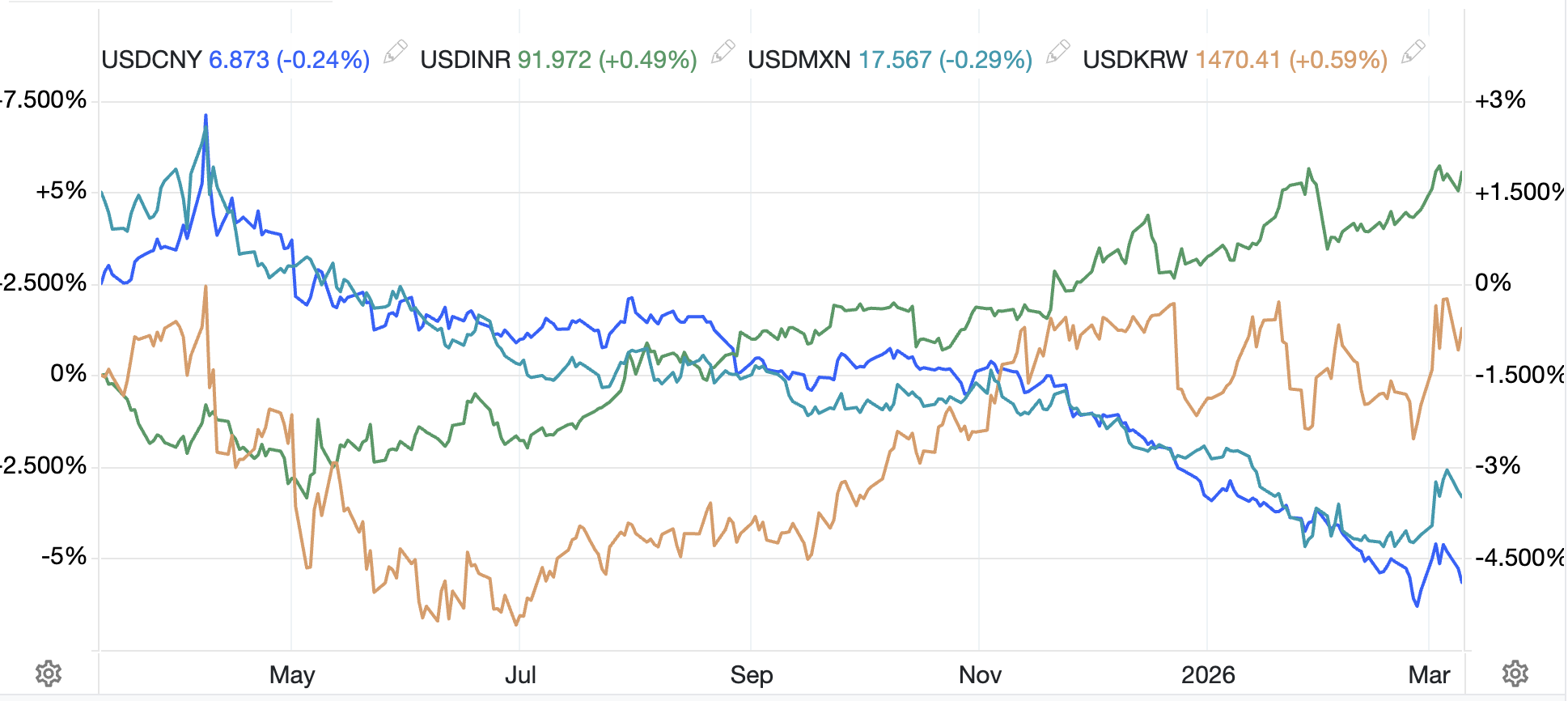

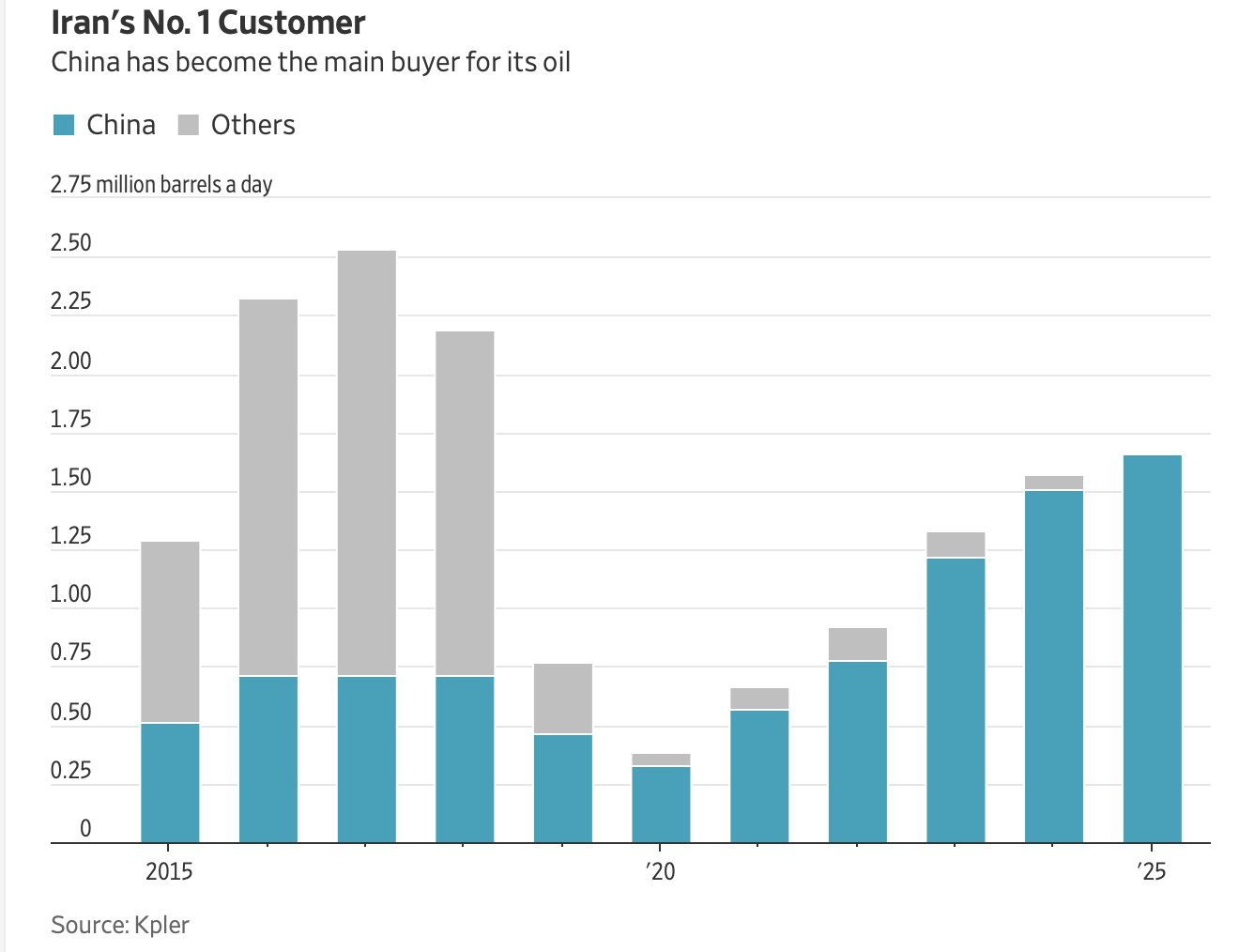

And I would not be surprised if President Xi is burning up the lines to Washington because he just lost a key source of cheap oil, and oil he paid for in CNY. (see WSJ chart below.)

There are many twists and turns here, and I’m sure there will be more. But as of Sunday night, from what I have read, Iran is in a much worse position than they were on Friday. Of course, things could all go pear-shaped from here, and this could turn out to be a complete failure. Our goal here is to try to track how markets will evolve.

The remarkable thing, still, to me is that equity markets remain so blithe about the entire situation. I make this claim based on the VIX Index, which remains relatively docile despite everything that is happening in Iran and the likely eventual knock-on effects. But look at the chart of the VIX below which shows that markets are nowhere near as stressed as they have been in the past and are actually much nearer their long-term average. (The two spikes are the JPY intervention in August 2024, which lasted for just a few hours, and then the Liberation Day tariffs in April 2025 which quickly reversed as well.

Source: tradingeconomics.com

It is worth noting that even the oil VIX, is off its highs and, while somewhat elevated, not running away.

Source: finace.yahoo.com

The thing about the VIX indices to remember, though, is that options decay and holding them is a losing proposition if the underlying market is not moving. So, to maintain a high VIX, we need to see significant intraday as well as day-to-day price movement.

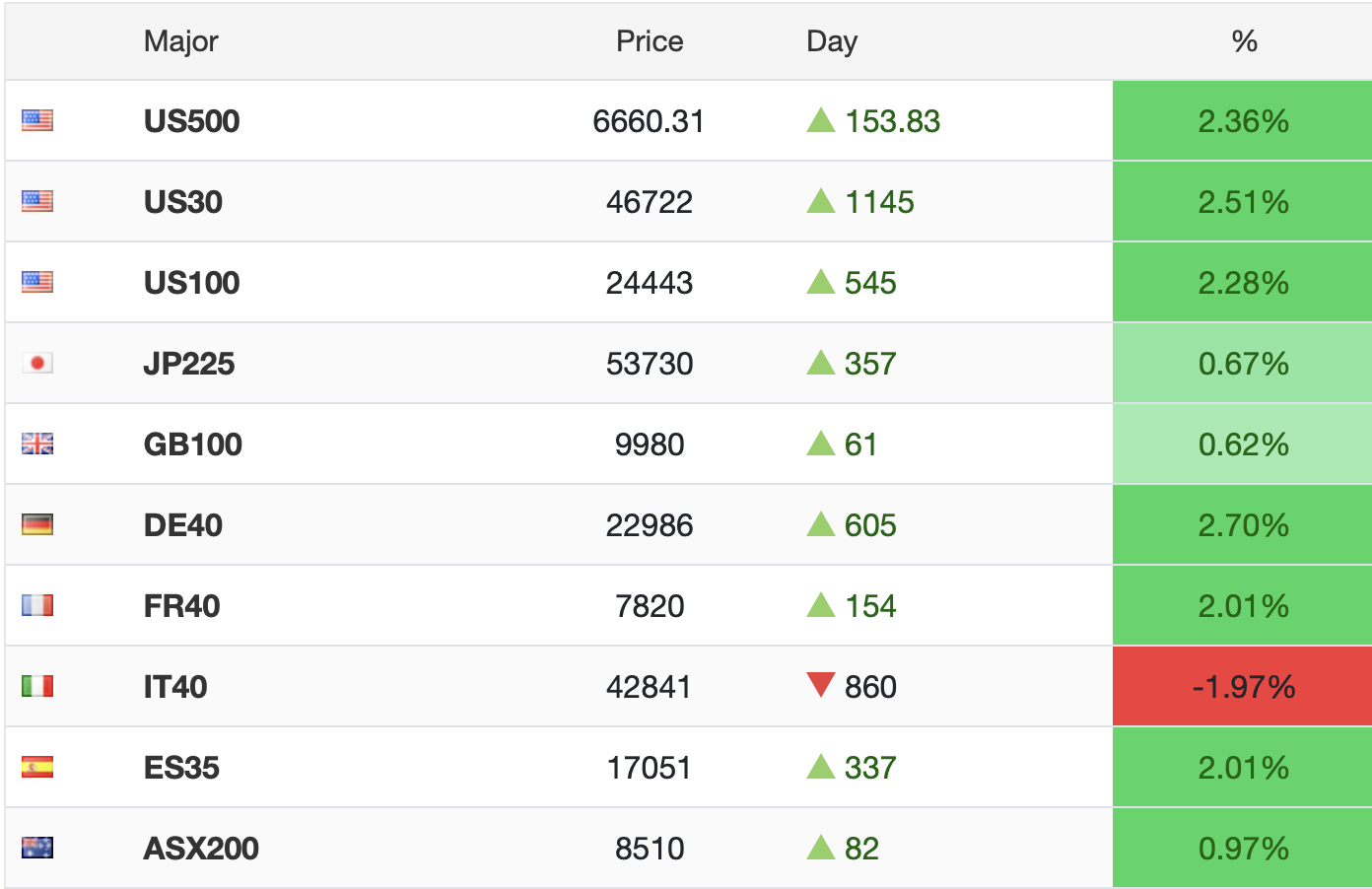

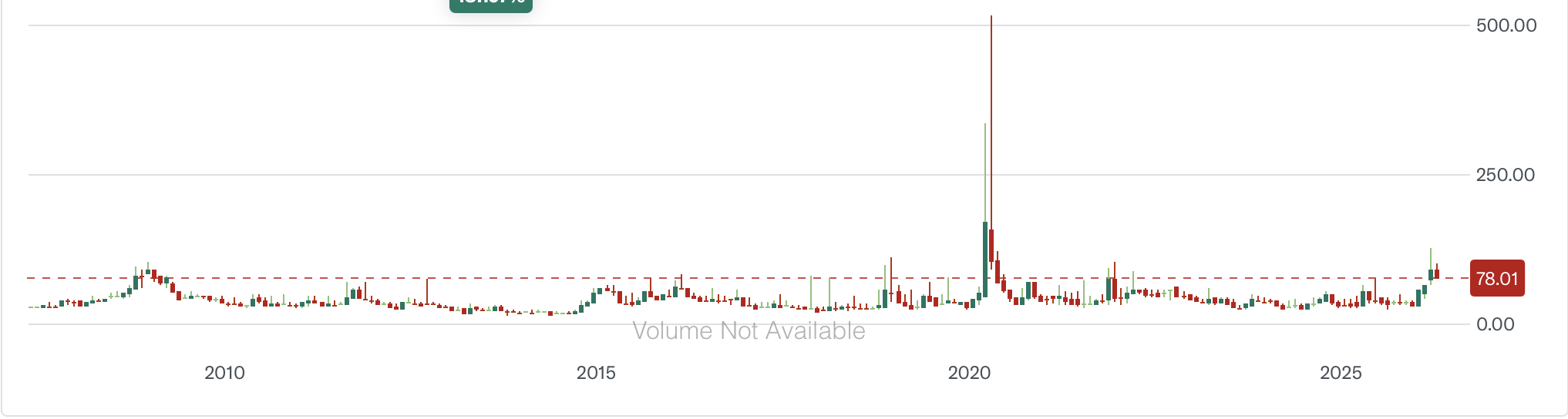

As Iran remains the major storyline for markets, let’s take a look at how things are behaving this morning. Oil (+8.2%) has maintained its initial gains but not moved since last night. NatGas (+1.7% in US, +9.0% in Europe) has also been impacted as there is no movement of LNG tankers through the Strait either. Interestingly, both gold (-0.6%) and silver (-1.7%) while lower are well off the lows seen in the early overnight session as per the below chart of silver.

Source: tradingeconomics.com

I reiterate that the market perception of the current situation has not nearly matched the hysteria evident in much of the commentary. I’m not sure whether to attribute that to market insight or market ignorance at this point, although I lean toward the former. The problem with commentary these days is that hysterical takes generate clicks, and that is the goal of many commentators.

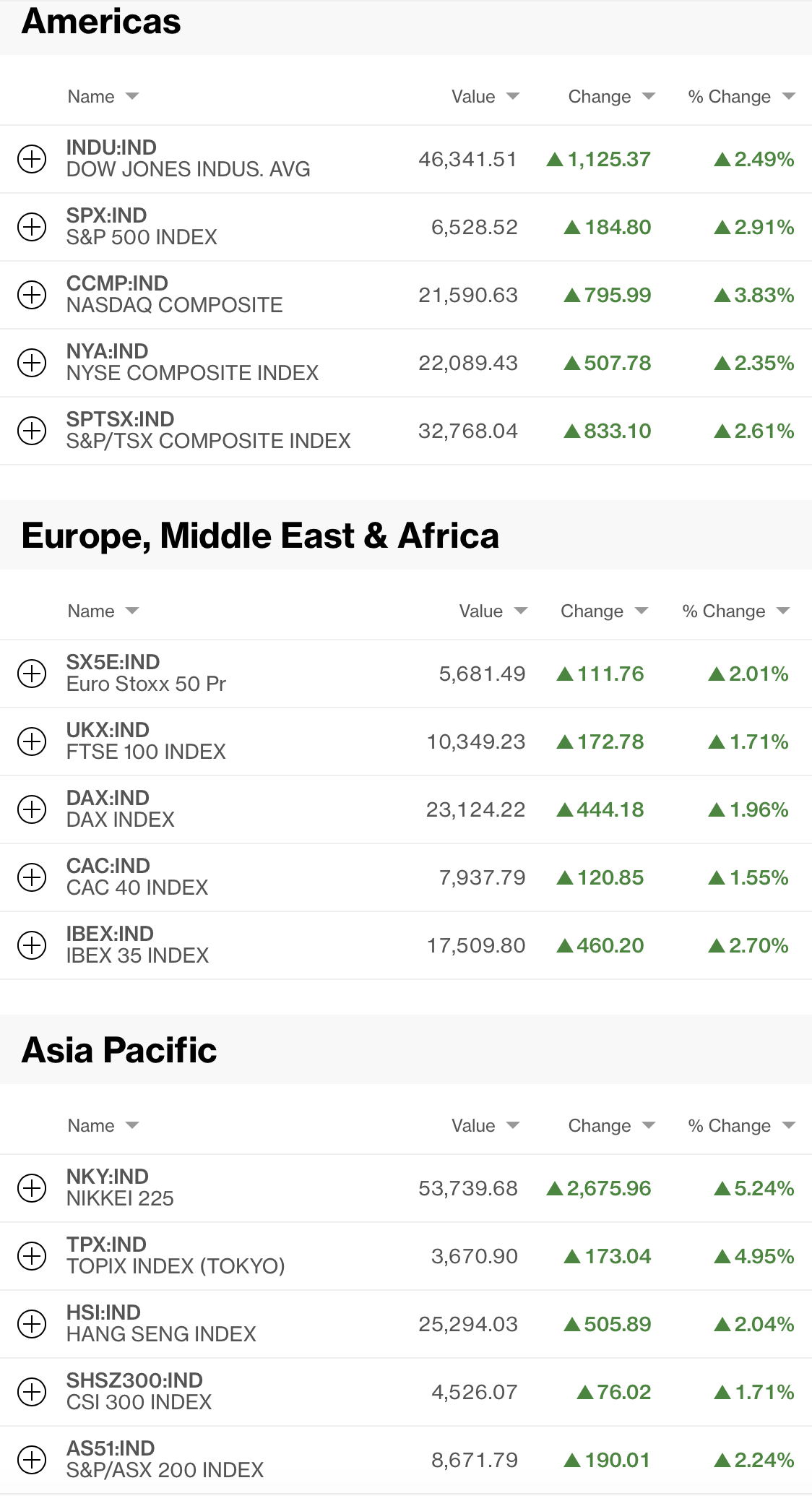

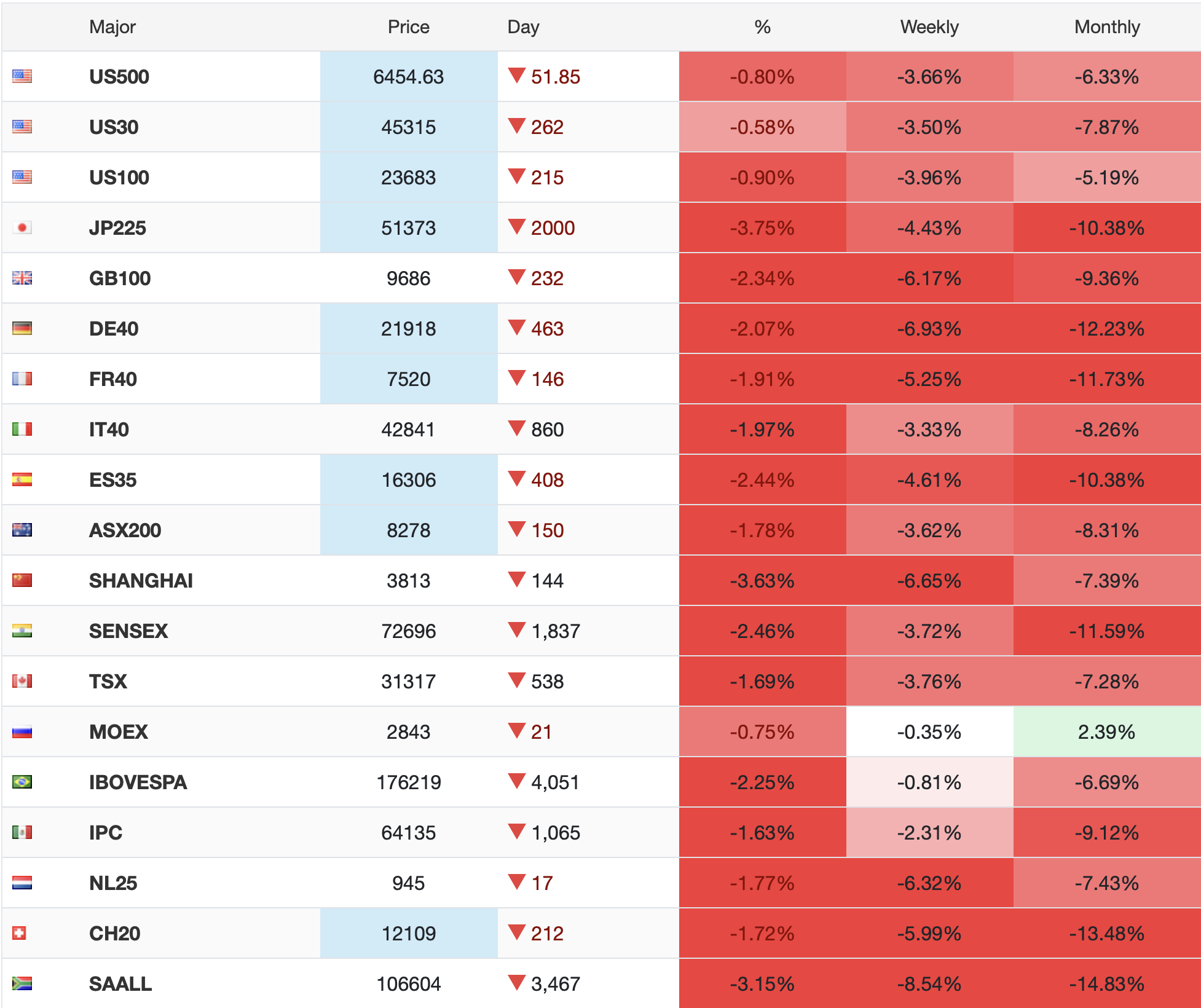

Turning to equity markets, Asian markets were generally, though not universally, lower. Tokyo (-0.7%), HK (-0.9%), Korea (-0.9%) and India (-0.9%) all suffered on the breakdown in talks and the new blockade news. New Zealand (-1.2%) was the worst performer, largely because their energy situation is deteriorating more quickly than anyone else’s. But China (+0.2%), Taiwan (+0.1%) and Indonesia (+0.6%) all managed some gains despite the news. Again, markets appear to be pricing a fairly benign outcome here. Either the news is going to get better soon, or there is going to be a massive rerating of equity markets. Something’s gotta give.

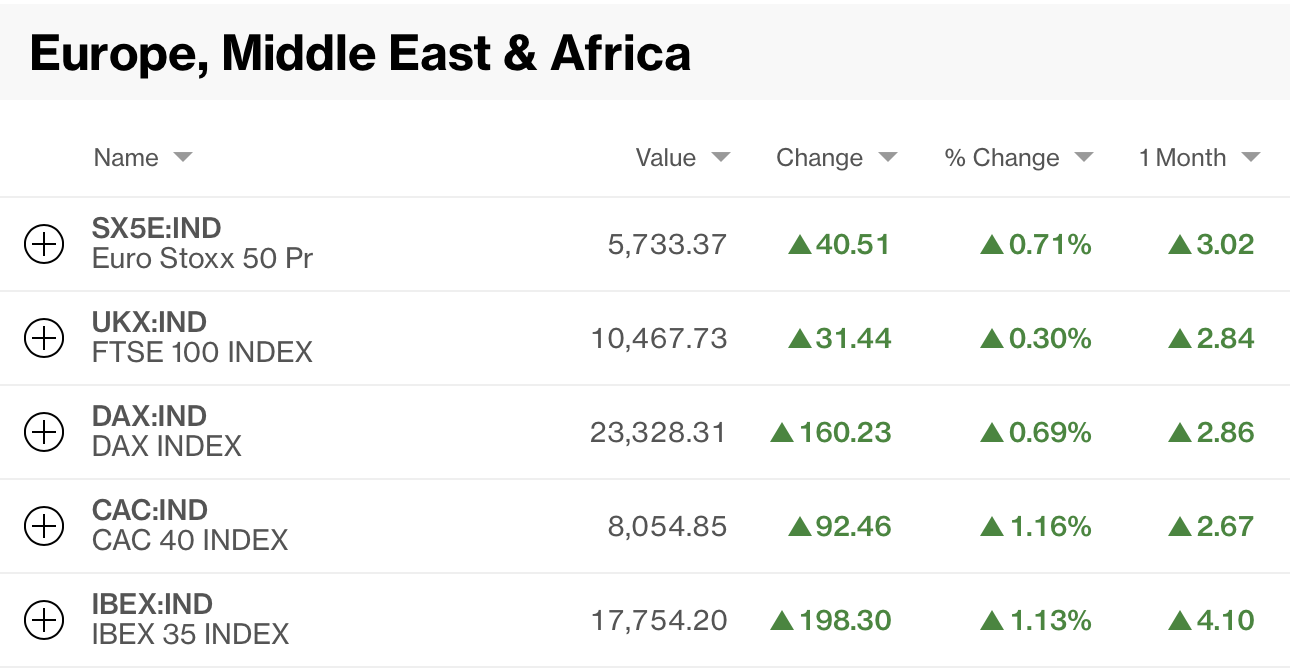

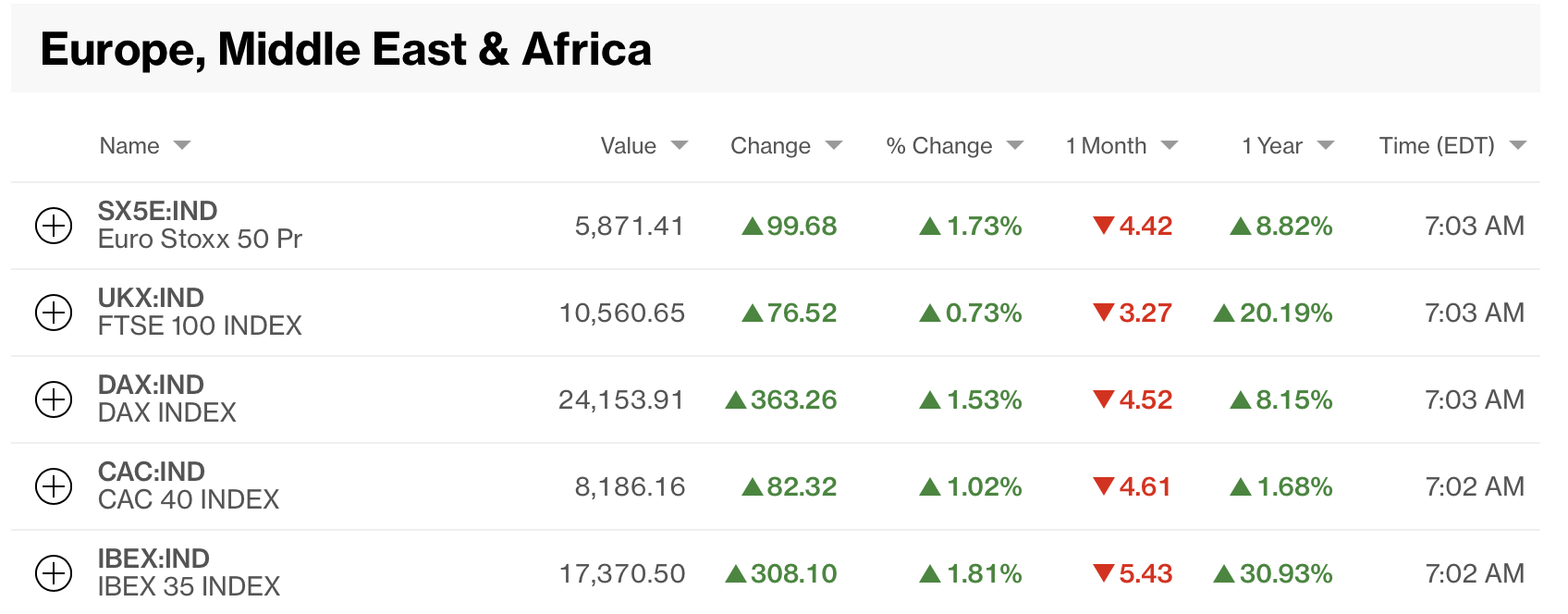

In Europe, things are a bit worse overall with Spain (-1.4%) leading the way lower although Germany (-1.0%), France (-0.9%) and Italy (-0.8%) are all under real pressure as well. There has been a lot more press lately about how Spain’s PM Sanchez is cozying up to China as he seems to be pulling Spain away from the EU in several areas. Of course, he is an avowed socialist, so perhaps this should not be that surprising. However, this is further proof that NATO is surely going to die soon.

One market that has outperformed, though is Hungary (+2.8%) which is rallying sharply on the weekend’s election results that sent President Victor Orban into retirement. Certainly, most others in Europe are thrilled as Orban had been a thorn in the side of the EU with respect to their Russia stance, but the economy there has been underperforming so new leadership is widely lauded, for now. The forint (+1.9%) also benefitted from the election outcome.

As to US futures, as I type at 7:00, the major indices are lower by -0.3% or so, well off the initial levels seen last night that were as much as -1.4% below Friday’s closing levels. Again, markets remain sanguine over the weekend changes to the story.

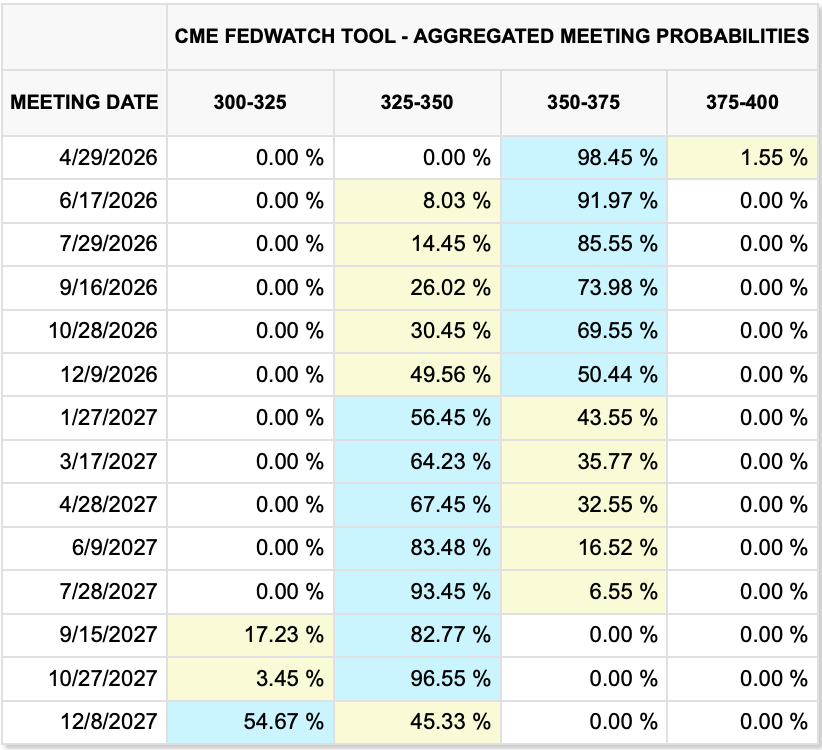

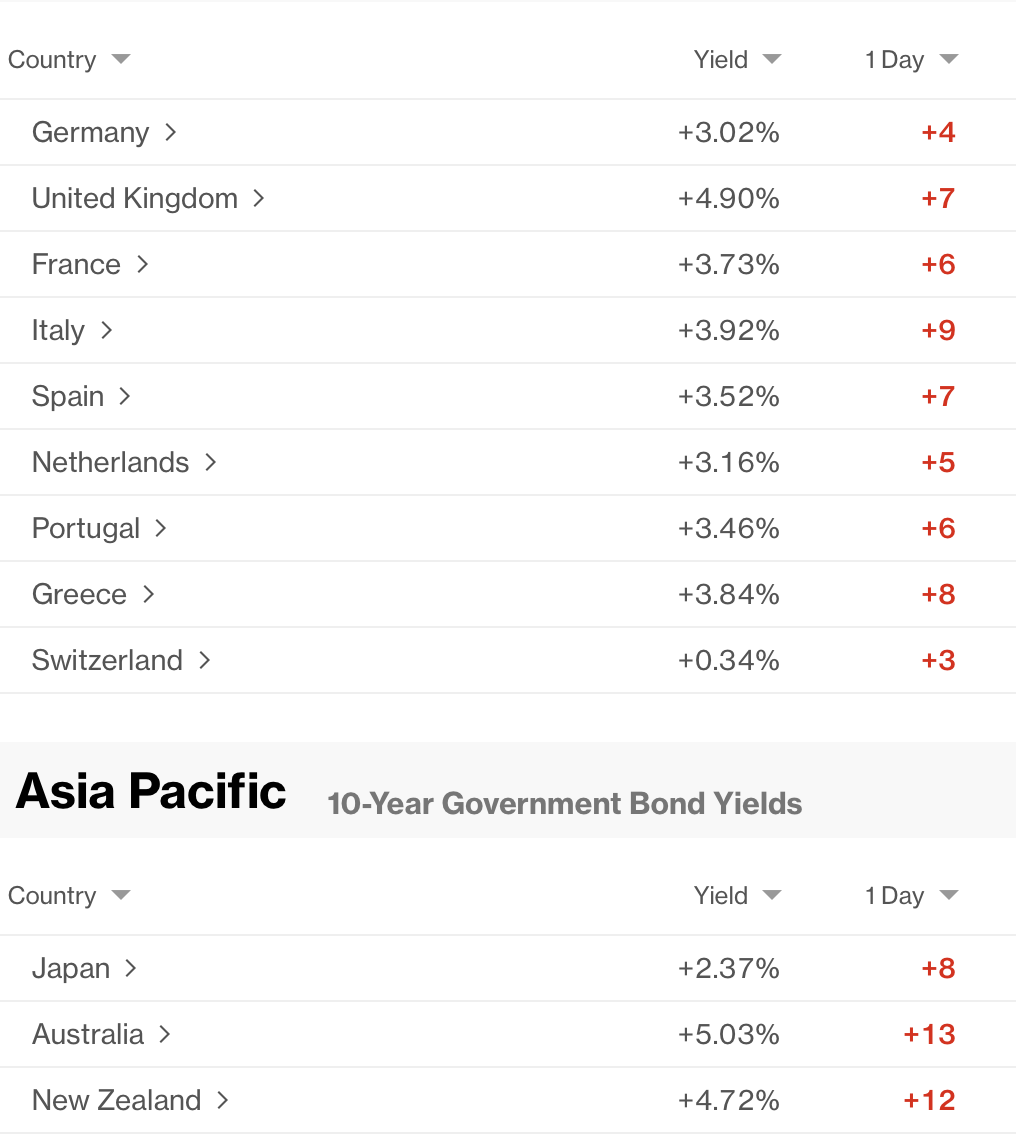

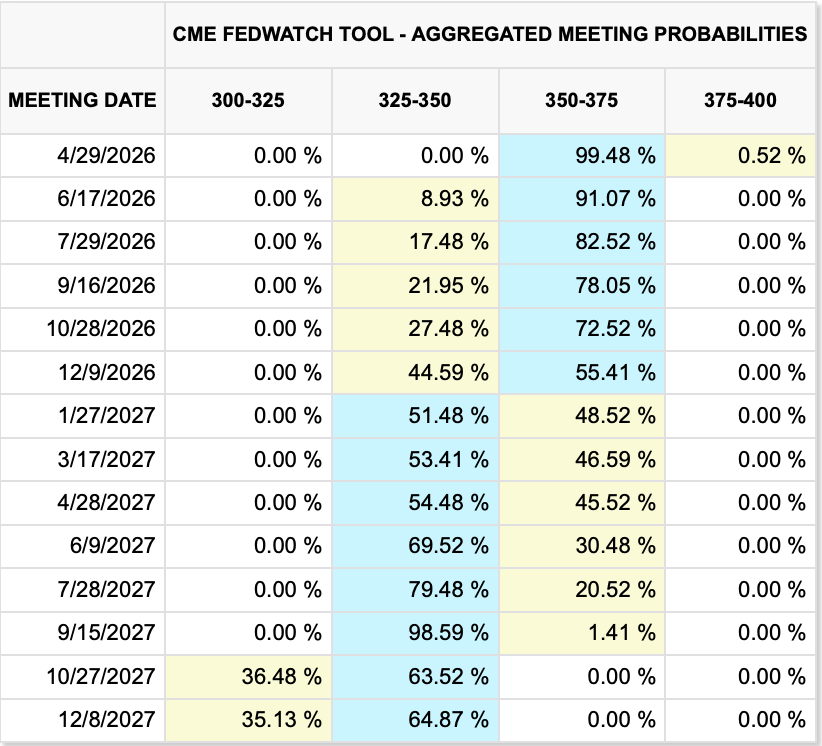

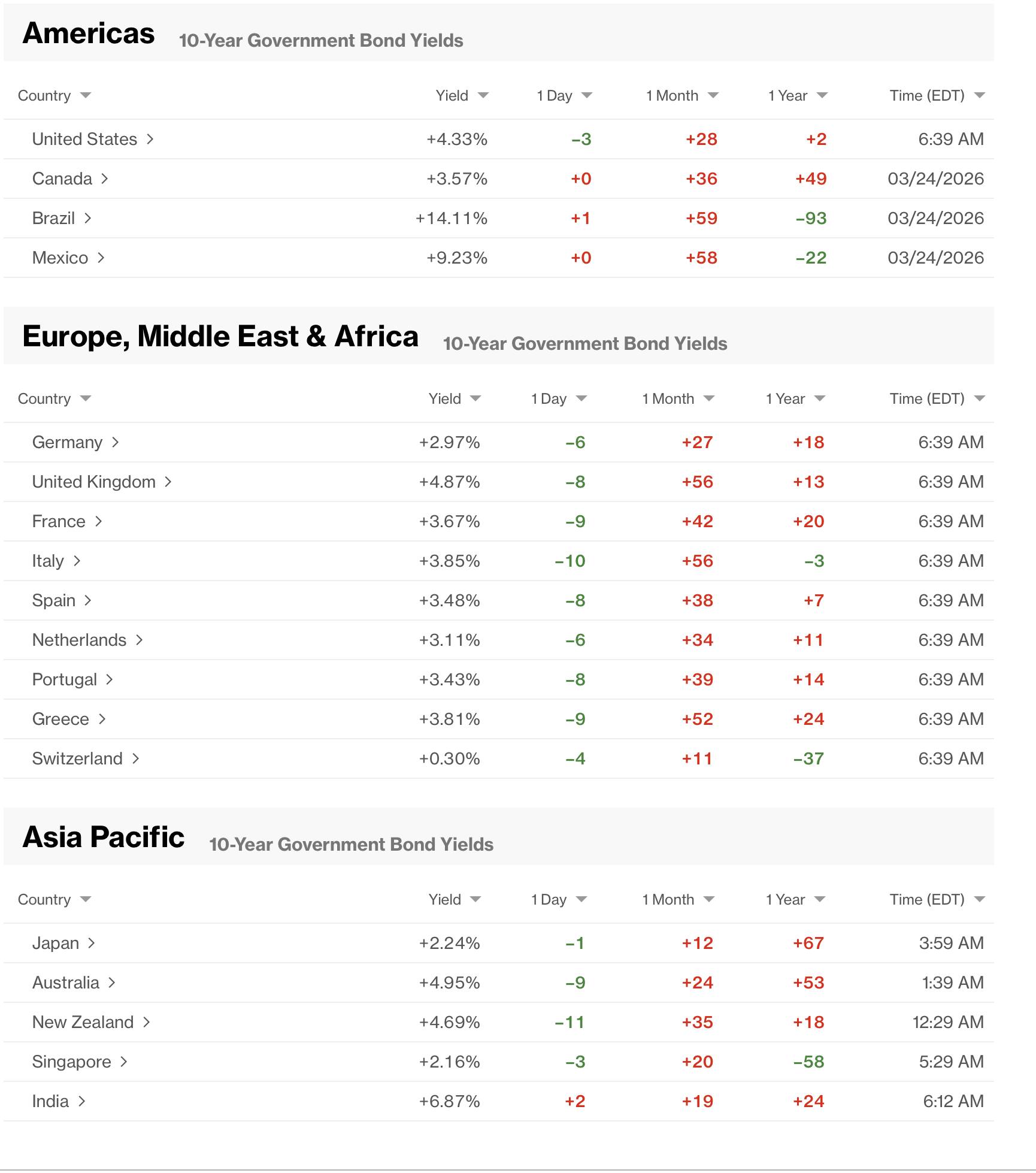

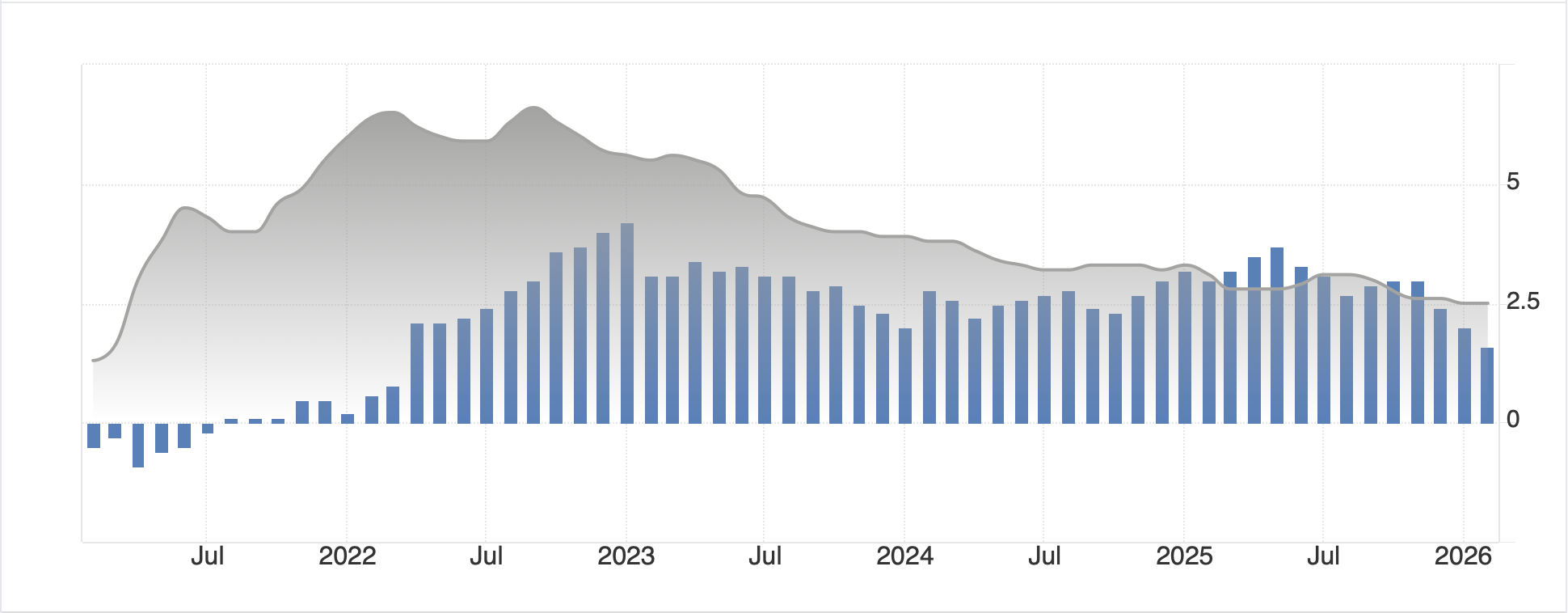

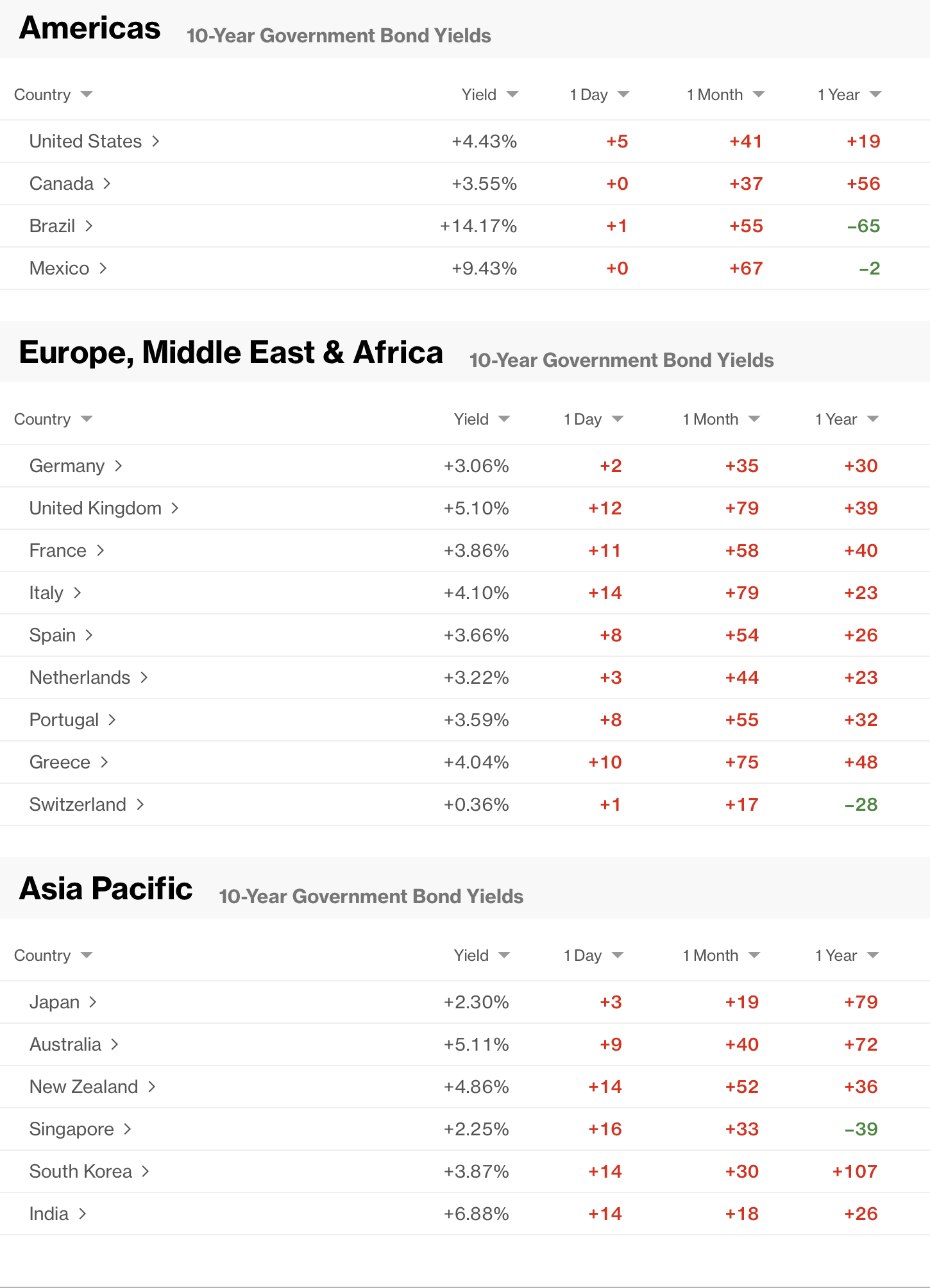

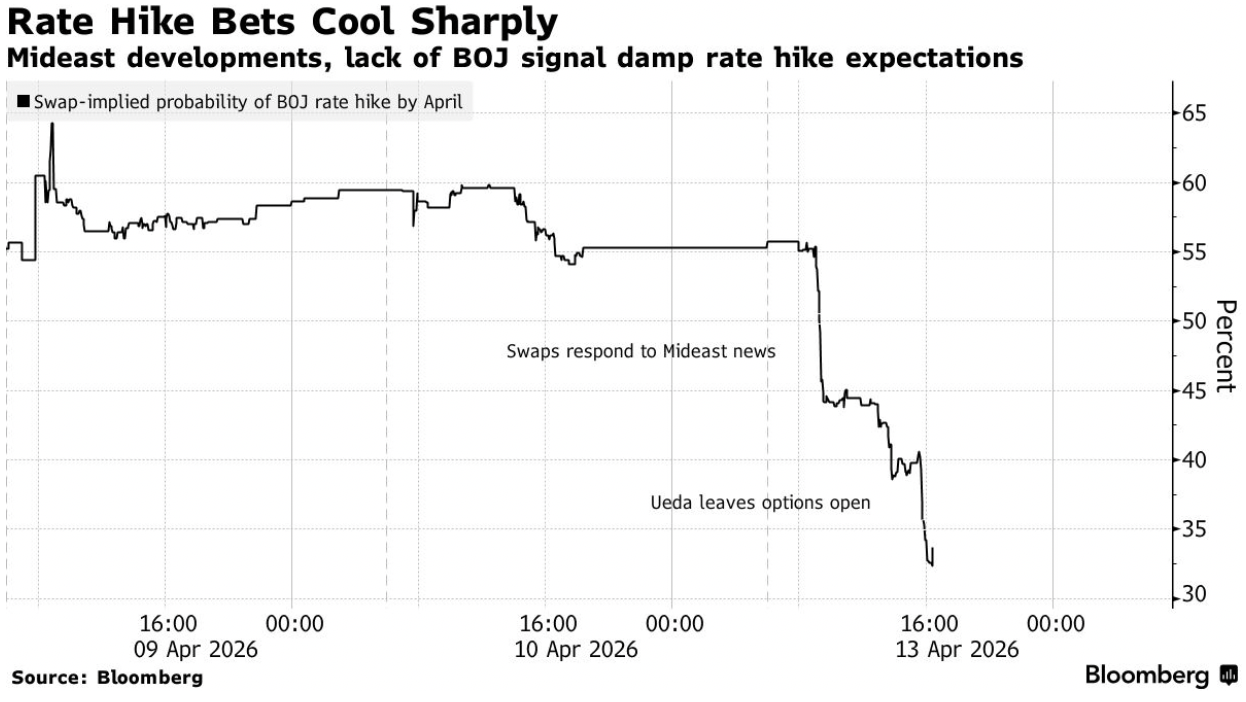

In the bond market, Treasury yields have edged higher by 1bp and in Europe, we are seeing rises of between 1bp and 3bps across the board. Here, too, it is hard to find panic in the streets. JGB yields (+2bps) have made a new high for the move and continue to edge higher as concerns over the path of inflation rise given the oil price rise. Last night, BOJ Governor Ueda gave a speech (actually his deputy did because he is in Washington for the IMF/World Bank meetings) and tried to quash the view that the BOJ was definitely going to hike rates at the end of this month, an outcome that had been priced at a 65% probability prior to his speech as you can see from the Bloomberg chart below.

Finally, in the FX market, other than HUF as described above, and NOK (+0.6%) responding to the oil move the dollar is firmer across the board. However, the movement is not too large, generally on the order of 0.2% or so across the G10 and perhaps a bit more in the EMG bloc. The worst performer today is ZAR (-0.8%) which is suffering the dual problems of a lower gold and higher oil price. The other noteworthy thing is JPY (-0.3%) is creeping back toward the 160 level, which remains the default setting for the market belief as an intervention level.

On the data front, Friday’s CPI was hot, but not quite as hot as forecast, although you can be sure that next month will remain hot. This week brings the following mostly secondary stuff.

| Today | Existing Home Sales | 4.06M |

| Tuesday | NFIB Business Optimism | 98.6 |

| PPI | 1.2% (4.6% Y/Y) | |

| -ex food & energy | 0.6% (4.2% Y/Y) | |

| Wednesday | Empire State Manufacturing | -2.0 |

| Fed’s Beige Book | ||

| Thursday | Initial Claims | 215K |

| Continuing Claims | 1840K | |

| Philly Fed | 9.0 | |

| IP | 0.1% | |

| Capacity Utilization | 76.3% |

Source: tradingeconomics.com

As well, we hear from eight different Fed speakers over 10 venues. An interesting aspect of the commentariat lately is that individual FOMC members are going to be far more important as there is a growing diversity of opinion. So, the monolithic Fed Chair running things and encouraging a vote in a particular way may evolve into an actual election, where the voters vote their hearts, not the Chairman’s views just to get along. If this is the case, and I think it would be far better than what we currently have, we will need to listen more closely to the individual speakers and start a scorecard to see who seems hawkish or dovish at any given time. The problem is, I fear it will encourage all of them to speak more frequently, which is a worse outcome, although any given voice will likely be given far less weight. We shall see if that is the case.

As to the broad scheme of things. My head tells me that the market is underpricing the risks out there, but my eyes explain that this is the current consensus. I hope they are right and I am wrong about things.

Good luck

Adf