‘Ought Twenty-Six barely got started And Trump has already departed From previous norms Of post-Cold War forms Now socialists are broken-hearted

Their man in Caracas is gone With outrage from Beijing to Bonn But folks on the street Believe it’s a treat Please welcome this year’s first black swan

I certainly didn’t have the exfiltration of Venezuelan strongman Nicholas Maduro from his palace in the middle of the night on my bingo card, did you? But that is what we all woke up to Saturday morning. In a way, we cannot be surprised as President Trump indicated several weeks ago that he spoke with Maduro, told him if he left, he could have safe passage, and be left alone, but ostensibly Maduro turned him down. I’m guessing old Nick is questioning that decision right now.

As this all took place Saturday morning, no financial markets, other than cryptocurrencies, are open and based on Bitcoin’s movement of 0.1% as I type, it appears the issue is not seen as a major concern. There is much discussion regarding what will happen to the price of oil, as unquestionably, Venezuelan oil was part of the decision equation. But the Venezuelans have been producing less than 1 million bpd, far below their pre-socialist levels, and given they sit on the largest known oil reserves on the planet, far below what their ultimate capabilities can be. If you’re Chevron’s CEO, you must be thrilled this morning, as they are already operating in country there.

Too, remember that Venezuelan crude is heavy and sour, which is what most Gulf Coast refineries are tuned to utilise to distill diesel, gasoline and other products. It is too early to know what will happen to oil prices in the short run, but I would suggest that the longer-term view has to be lower prices going forward. Consider that the US already is the largest producer of oil and oil equivalents (about 20mm bpd) in the world. I would expect that Venezuela will be exiting OPEC under a new administration there, and with US oil expertise, will be seeking to expand that sector as rapidly as possible. In fact, achieving 10mm bpd within a few years does not seem unrealistic.

Now consider that by the end of the decade, the Western hemisphere could well be producing half the world’s oil supply, as already, despite degradation of capabilities in both Venezuela and Mexico, it produces more than one-third of the oil pumped. That would certainly put a crimp in Russia’s war machine as the price seems far more likely to head toward $50/bbl than $80/bbl or higher, and by all accounts, that would be hard on Russia’s budget.

Too, consider the geopolitical ramifications if China were suddenly paying full price rather than whatever discounts they currently get for sanctioned oil purchases. As well, what does a lower price do to the Iranian regime’s finances? Probably not very helpful.

It is way too early to know how things will evolve, but between growth in production in Guyana and Argentina, and the prospects for significant growth in Venezuela going forward, it should become cheaper to fill up your tank going forward.

We will see how markets open Sunday night, and I would not be surprised to see oil rally at the start, but I would contend the politics points to lower prices not higher ones.

Source: visualcapitalist.com

Note that neither Venezuela nor Argentina make this list individually. I would wager that by 2027, both will be prominent producers, along with Guyana.

Welcome to 2026! It is going to be an interesting year.

The question on tariffs today Is what will the Court, Supreme, say Will they agree Trump Has power to pump Up taxes with no Senate sway?

Or otherwise, will the top court Decide to, Trump’s tariffs, abort? And if they decide That Trump is offside Is it time to buy or go short?

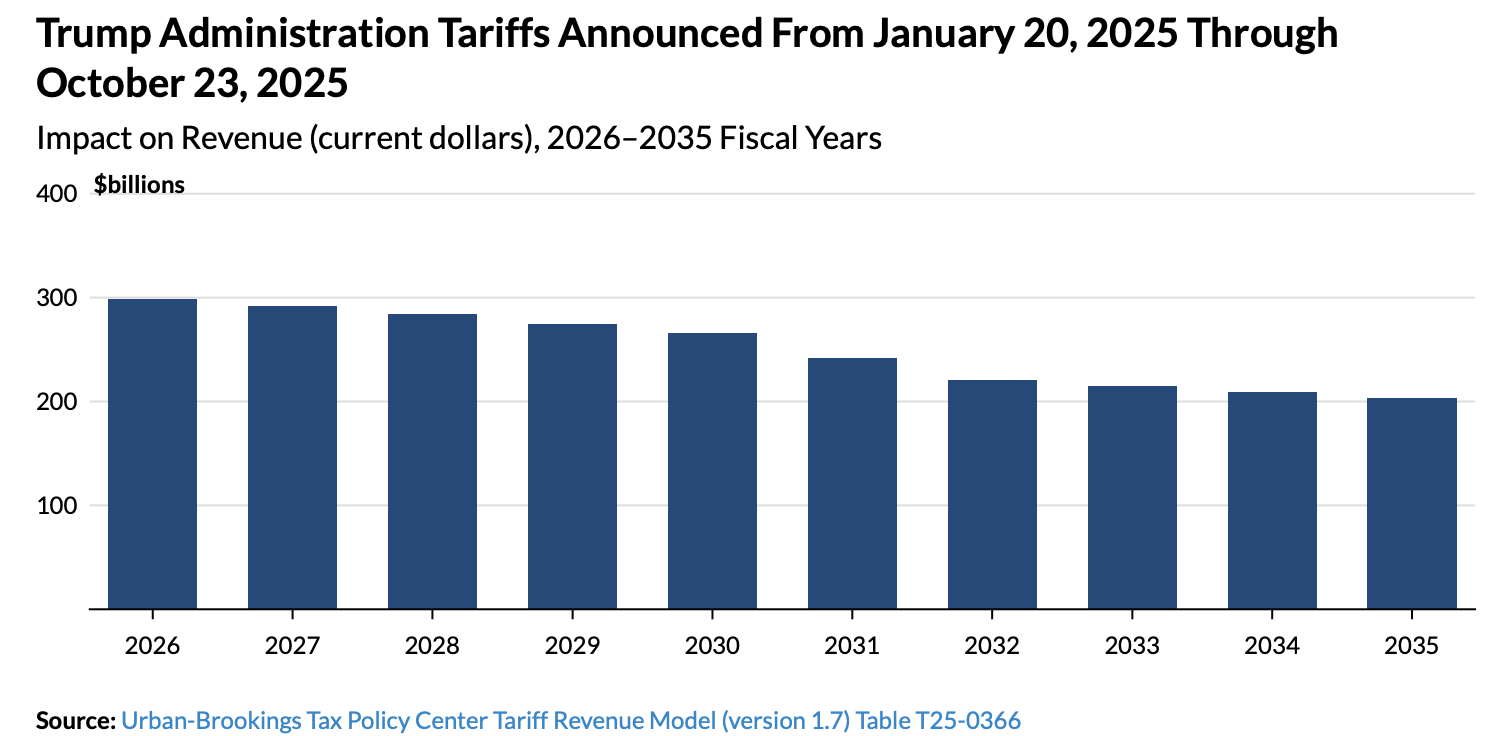

As testament to the idea that no matter the shock to a system, if it is a dynamic system, it will manage to adapt to the new reality, today’s existential question is, what happens if the Supreme Court decides that President Trump’s tariffs are unconstitutional? Let’s forget for a moment, the fact that they have generated approximately $200 billion in government revenue since their imposition and are forecast to generate upwards of $300 billion next year and $2.5 trillion in the next decade, at least according to the Tax Policy Center (see chart below from taxpolicycenter.org). Obviously, this is a good chunk of change for a government that has been running $2 trillion annual deficits.

Rather, let us consider the features that have accompanied the tariff negotiations, notably the promised inward investment to the United States. Although there are several figures that have been mooted, with President Trump claiming $10 trillion, it appears that a fair estimate of the number is half that, so $5 trillion, to be invested in the US, notably in manufacturing capabilities, over time. That, my friends, is a lot of money.

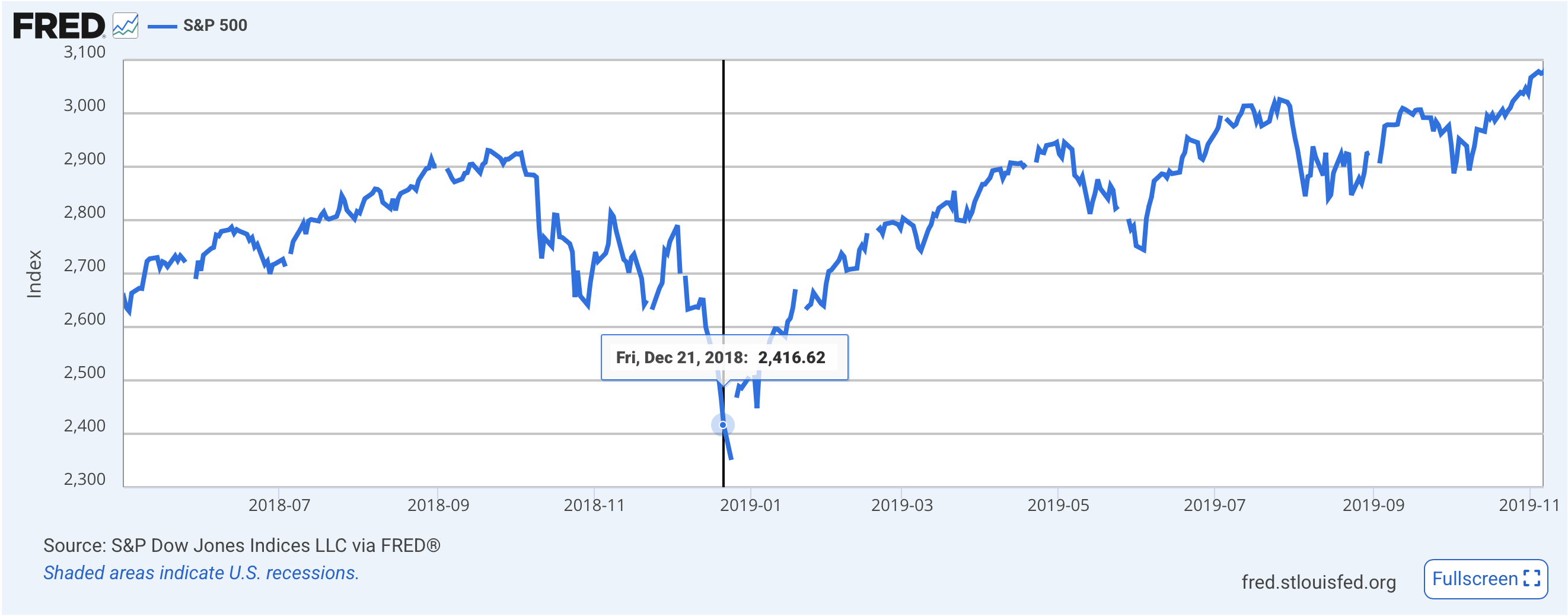

Now, we all remember what happened when Mr Trump announced those tariffs on Liberation Day back in April, but here is a chart of the S&P 500 to remind us of the size of the initial decline in equity markets.

Source: tradingeconomics.com

The decline from the close on April 2nd to the low on April 7th was ~12%, at which point, things were put on hold for 90 days and a series of furious negotiations began. But we saw similar dramatic moves across all markets. For instance, 10-year Treasury yields fell 33bps during that time, before rebounding sharply.

Source: tradingeconomics.com

Oil also collapsed on the news, falling from nearly $72/bbl to $56/bbl in that stretch as the announcement shook up virtually all financial markets around the world.

Source: tradingeconomics.com

Perhaps the most surprising outcome was that the dollar actually fell about 3% during that period despite every economist and every textbook explaining that the impact of tariffs on currency markets would be that those countries whose goods were tariffed would see their currencies decline while the one imposing the tariffs would see strength. (Yet another reason to pay little heed to economists and their theories which sound great but rarely seem to describe reality.)

Source: tradingeconomics.com

I highlight all this movement because the market behavior since then has been nothing but positive. Equity markets have decided that things are great and rallied dramatically. Bond markets have absorbed the information and decided it doesn’t matter that much or perhaps priced in the new revenue model as part of finding a new equilibrium around 4%. Oil markets have other things about which to worry, with the current theme the alleged glut of oil that is around, and the dollar, while it continued to decline a bit further over the ensuing three months, has now seemingly found a bottom, and if anything looks like it is preparing to climb.

But…what if the tariffs must go? And what if the government must repay those already collected? If you recall, the narrative about tariffs back in April was that they were the end of the US economy and a disaster. Obviously, that has not turned out to be the case. Is the new narrative that the end of tariffs will be a disaster? That feels like a pretty big reversal of opinion.

To my thinking, one of the keys to the recent optimism for the US economy, at least for those who are optimistic, is that the inward investment is going to have very positive medium- and long-term impacts on the economy. They are going to be critical in the reshoring of American manufacturing, whether Japanese investment into US Steel, or Korean investment into shipbuilding or Taiwanese investment into semiconductor manufacturing. All these things are unalloyed positives for the nation and its future. But if the tariffs are revoked, will the investments disappear? That is the $5 trillion question, and one that I believe would be incredibly detrimental to both the nation and its financial markets. Stocks would fall sharply and so would bonds as growth prospects would shrink and the fiscal imbalance likely grow even further. The dollar would suffer between the capital outflows, and the fiscal problems and oil would likely fall amid a dramatic reduction in US demand. Arguably, the only thing that would prosper would be gold, the historic safe haven.

Which brings the question back to the Supremes (not these Supremes, although the sentiment is right!), will they unleash that chaos? Or will they find a way to avoid it?

With so much to consider, let’s do a brief twirl around the world overnight. Yesterday saw a solid US equity rally across the board which was followed by strength throughout most of Asia (Nikkei +1.3%, Hang Seng +2.1%, CSI 300 +1.4%) with generally lesser gains elsewhere in the region. Europe, though, is on its back foot with modest declines (UK -0.4%, Germany -0.1%, France -0.4%) after weaker than expected Construction PMI data across the board. As to US futures, at this hour (7:00) they are very slightly firmer across the board, 0.1% or so.

In the bond market, yesterday saw US yields climb about 6bps after the ADP Employment data was released at a stronger than expected 42K with modest revisions higher to the previous months. Remember, last month’s revisions lower were for an entire year, not specifically the past two months, so it appears that job growth is still decent, just not quite as strong as last year. That data helped push yields up around the world, notably with JGB yields higher by 3bps. But this morning, yields have backed off -3bps in the US and are unchanged across the entire continent and UK. As to the UK, they left rates on hold at 4.0%, as expected, but the vote was 5 – 4 with 4 votes looking for a cut, so a more dovish signal.

In the commodity markets, oil (+0.8%) is rebounding after a decline yesterday based on a much larger than expected build in EIA inventories while NatGas also climbed on forecasts for colder weather and increased LNG demand in Europe and Asia. Gold (+0.9%) and silver (+1.4%) continue their rebound from recent lows and seem like they are getting comfortable in their new “homes” of $4000 and $48.00 respectively.

Finally, the dollar is under modest pressure this morning, with the DXY slipping barely below the 100.00 level (currently 99.94) while the euro (+0.25%) and pound (+0.2%) both edge higher. It appears that the dollar’s recent strength is on hold for today, although my take is it will resume shortly. While a negative Supreme Court ruling on tariffs is likely to really undercut the greenback, I don’t see anything else in the near term to do the job.

There is no data of note to be released today, but we have an onslaught of Fed speakers, six in total starting at 11:00 this morning. The Fed funds futures contract is now pricing just a 65% probability of a rate cut next month, as the ADP number encouraged some folks to change their views. My take is we are going to hear a lot about caution given the absence of data, but I might contend the market is already somewhat cautious, at least the bond market is.

The thing about the tariff issue is it won’t be decided for at least several weeks, if not months, so may hang over the market like the Sword of Damocles. I have no idea how they will rule, and the commentary from observers of the hearing gave different views based on their political biases, so it is hard to know. But it is going to matter a lot. In the meantime, I expect the recent trends to remain in place, so equity strength, little bond movement, little oil movement and dollar strength.

Though data is scarce on the ground This week has the chance to astound Four central banks meet And when it’s complete Two cuts and two stays ought abound

Meanwhile, Mr Trump’s signing deals In Asia, an act that reveals His fervent desire To drive markets higher As foes let out curses and squeals

Some days, there’s very little to note, with the news cycle a rehash of stories that have been festering for weeks. This is especially true in the political sphere, but also on the economic front. As well, given the ongoing government shutdown and the lack of government data being released, a key market focus is missing. But not today!

News across the tape moments ago is that President Trump has agreed a trade deal with South Korea, although the details of the deal are yet to be revealed. When it comes to Trump and trade deals, it is always difficult to get through the hype to determine if things will actually improve, but if we use the KRW as a proxy for market sentiment, as you can see in the chart below, the announcement was seen as a benefit to the won.

Source: tradingeconomics.com

This is hardly definitive, and the nature of a trade deal is that it takes time to be able to determine its benefits for both sides, but for now, it appears markets are giving it the benefit of the doubt. As well, it continues to be reported that Presidents Trump and Xi will be sitting down tomorrow (tonight actually) and that a trade framework has been agreed by Secretary Bessent and Chinese Vice Commerce Minister Li Chenggang which includes reduced tariffs, fentanyl, soybeans, semiconductors and rare earth minerals as key pieces of the puzzle.

The ongoing competition between the US and China is not about to end with this deal, but perhaps it will be able to revert to a background issue rather than a headline one, and that is likely a positive for all. Certainly, equity markets continue to believe that this dialog is a benefit as evidenced by their daily trips to new highs.

Which takes us to the other key discussion point in markets, central banks. Over the next twenty-seven hours (it is 6:30am as I type) we are going to hear four major central banks explain their latest policy steps starting with the Bank of Canada (expected 25bps cut) at 9:45 this morning, then the FOMC at 2:00 this afternoon with their 25bps cut. This evening at 11:00, NY time, the BOJ is expected to leave rates on hold, although there are those who believe a 25bps hike is possible, and then tomorrow morning at 9:15 EDT, the ECB will also leave rates on hold.

While this is certainly a lot of new information, the question is, will it have any market impact? Given the market pricing of these events, if any of the central banks do something different, you can be sure its markets will respond. If I had to assess what might be different, both the BOC and FOMC could cut more than 25bps, and the ECB could cut 25bps rather than standing pat. In all those cases, the currency would likely weaken sharply at first, although if all those things happened, I suppose it would simply create a new equilibrium. But understand, I don’t think any of that WILL happen.

Regarding the Fed, though, there is another question and that is, what is going to happen to QT and the balance sheet. Lately, there has been a great deal of discussion regarding how much longer the Fed will allow the balance sheet to shrink. Last week I discussed the difference between ample and abundant reserves, but in numeric terms, the signals are coming from the SOFR (Secure Overnight Financing Rate) market, the one that replaced LIBOR. It seems that there is increasing concern over the recent rise in the rate. This is seen by numerous pundits, as well as by some in the Fed, as a signal that the reserve situation is getting tighter, thus offsetting the Fed’s attempts at ease.

The below chart from the NY Fed shows the daily wiggles, but also, it is pretty clear that the recent trend has been higher. You can see the September Fed funds cut in the sharp drop, and the first peak after that was September 30th, the quarter-end when banks typically look to spruce up their balance sheets, so borrow more aggressively. But since then, this rate has been edging higher, an indication that there may not be sufficient reserves available for the banking system.

This begs the question; will the Fed end QT today? Or wait until December? My money is on today as they are growing concerned about the employment situation with the uptick in recent layoff announcements, and the pressure on SOFR is the best indicator they have that things have reached the point where their balance sheet no longer needs to shrink. One other thing to keep in mind, at some point, it seems likely that the Fed is going to need to find more buyers of Treasuries as the market may develop indigestion given the amount being issued. That pivot back to QE, whatever it is called, is easier if they are not simultaneously reducing their own balance sheet.

And one final point on the Fed. Apparently, when they cut today, it will be the twenty-second time the Fed will have cut with stock indices at all-time highs, and of those previous twenty-one, twenty-one times equity markets were higher one year later. Let’s keep that party rolling!

Ok, let’s look at how things have gone overnight. Tokyo (+2.2%) was basking in the glow of all the love between President Trump and PM Takaichi, as it, too, traded to new all-time highs. China (+1.2%) gained on the news of the trade framework, but interestingly, HK (-0.3%) did not follow suit. And it should be no surprise that Korea (+2.1%) rallied on that trade news with India and Taiwan rising as well. Australia (-1.0%) though, had a rougher go after a higher than forecast inflation print (3.5%) put paid to the idea that the RBA would be cutting rates again soon.

In Europe, Spain (+0.65%) is rallying on solid GDP data (1.1% Q/Q) although the rest of the continent is doing very little with virtually no change there. In the UK, the FTSE 100 (+0.6%) is rallying on stronger corporate earnings from miners (metals are higher) and pharma companies. As to US futures, at this hour (7:30) they are all nicely in the green, about 0.35% or so.

In the bond market, Treasury yields have backed up 2bps, but are still just below the 4.00% level, hardly signaling major concern right now. European sovereign yields are all essentially unchanged this morning and overnight, only Australia (+5bps) moved after that CPI data Down Under.

Turning to commodities, oil (+0.5%) is bouncing after a couple of weak sessions, but net, we are right back to the $60 level which appears to be a comfortable level for both buyers and sellers. It is also a high enough price to encourage continued exploration, so my take is we are likely to trade either side of this level for quite a while going forward. My previous bearish views are being somewhat tempered, although I don’t foresee a major rally of any note.

Source: tradingeconomics.com

In the metals markets, gold (+1.7%) is bouncing off its recent trading low and currently back above $4000/oz. A look at the chart for the past month shows just how large the movements have been as the parabolic blow-off to near $4400 was seen through the middle of the month, and after a second try, the rejection was severe. I don’t believe the long-term story in the precious metals has changed at all, the idea that fiat currencies are going to maintain their current status as reserve assets is going to be more and more difficult to defend with gold the natural replacement. But in a market with a history of manipulation, don’t be surprised to see many more sharp moves ahead.

Source: tradingeconomics.com

As to the rest of the metals, they are all higher this morning with silver (+2.1%) leading the way and copper (+0.6%) and platinum (+1.6%) following in its wake.

Turning to those fiat currencies, the dollar is broadly firmer this morning, with only AUD (+0.15%) managing any gains against the greenback after that inflation print got traders thinking about higher rates Down Under. But otherwise, in the G10, the dollar is ascendant. In the EMG bloc, we already discussed KRW, but ZAR (+0.2%) is also gaining today on the back of the metals bounce. Elsewhere, though, modest dollar strength is the rule. What makes this interesting is the dollar is back to rallying alongside precious metals.

Ahead of the Fed, we only see EIA oil inventories with a small draw expected. In theory, with President Trump in South Korea, one would expect him to be sleeping throughout most of today’s session, but apparently the man rarely sleeps.

The big picture is that run it hot remains the play, and that means equities should benefit, bonds should have a bit more trouble, but the dollar and commodities should do well. I see no reason for that to change soon.

The pundits are still talking gold But what is the reason it sold? Liquidity drying Means selling, not buying Of havens. Has, now, the bell tolled?

One of the great things about FinX (FKA FinTwit) is that there are still a remarkable number of very smart folks who post things that help us better understand market gyrations. The recent parabolic rise and this week’s reversal in the price of the barbarous relic seem unrelated to any concept of fundamentals one might have. After all, perhaps the only fundamental that impacts gold is the rate of inflation, and since we haven’t seen a reading there in a month, it seems unlikely that had anything to do with this price action. However, there is a far more likely explanation for the move lower, which has been very impressive in any context. First, look at the chart below from tradingeconomics.com which shows the daily bars for the past 6 months. The rise since early September has been nothing short of remarkable.

This begs two questions; first, why did it rise so far so fast, and second, what the heck happened on Friday to turn it around so dramatically?

The first question has several pieces to its answer including ongoing concerns over fiat currencies in general (the debasement trade that became popular), increased central bank buying and a recent change in financial advisors’ collective thought process about the merits of holding gold in an investment portfolio. In fact, I think it was Bank of America (but I could be wrong) that recently suggested that the 60:40 portfolio should really be 60:20:20 with the final 20% being gold! Given the human condition of jumping on bandwagons, it is no surprise that this type of ‘analysis’ has become more popular lately. Whatever the driver, or combination of drivers, the price action was remarkable and clearly overdone. After all, compare the current price, even after the recent sharp decline, to the 50-day moving average (the blue line on the chart) as an indicator of the extreme aspect of the price action.

But let’s focus on the last few days and the sharp reversal, which takes me back to X. There is an account there (@_The_Prophet_) who put out an excellent step by step rationale of what led up to yesterday’s dramatic decline and why it is important. I cannot recommend it highly enough as a short read.

In sum, his point is, and I fully subscribe to this idea, that when things get tough, investors/traders/speculators sell what they can sell, not what they want to sell. If liquidity is drying up for the funding of speculative assets that are highly leveraged, then when margin and collateral calls come, and they always do, those owners sell whatever they have that they can liquidate. In this case, given the massive run up in the price of gold, there was a significant amount of value to be drawn down and utilized to satisfy those margin calls.

History has shown this to be the case time and again. I would point to the Long-Term Capital Management fiasco back in 1998 where the Nobel Prize winning fund managers quickly found out that liquidity was much more important than ideas and they were forced to sell out their Treasury holdings rather than their leveraged positions because the former had prices and the latter didn’t. This ultimately led to the liquidation of their fund along with some $5 billion in capital.

There has been much discussion as to the nature of the recent rise in asset prices with many pundits calling it the everything bubble. Bubbles are created when central banks pump significant liquidity into the system and this is no different. We know the Fed has allegedly (look at the graph of M2 below to see how much they have been increasing money supply during their tightening) been trying to reduce its balance sheet (i.e. liquidity) but this could well be a sign that phase is over. Typically, the next step is QE in some form, so beware. And when that comes, you can be sure that gold will rally sharply once again!

Of course, while the gold move has been the most spectacular, we have seen a lot more market volatility in the past several sessions, so let’s look at how things behaved overnight. Yesterday’s mixed US session was followed by more laggards than leaders in Asia with Japan essentially unchanged, while HK (-0.9%) and China (-0.3%) both slid a bit. Recent comments by President Trump that he may not sit down with President Xi next week have investors and traders there nervous. Elsewhere, Korea (+1.5%) and Thailand (+1.1%) had solid sessions while the rest of the region (Indonesia -1.0%, Malaysia -0.9%, Australia -0.7%) all lagged.

In Europe, the UK (+0.9%) is benefitting this morning from softer than expected inflation readings (3.8% vs 4.0% expected) which has tongues wagging that the BOE will now be cutting rates. The market priced probability has risen to 60% for a cut this year, up from 40% yesterday, before this morning’s data release. However, on the continent, only Spain (+0.6%) is showing any life on local earnings performance while the rest of the markets are all lower by varying degrees between -0.1% and -0.5%. As to US futures, at this hour (7:20) they are unchanged.

Bond markets continue to see yields slide lower with Treasuries (-1bp) now nicely below 4.00% and trading at their lowest level in more than a year (see below)

Source: tradingeconomics.com

European sovereign yields have seen similar movement, edging lower by -1bp except for UK gilts, which have fallen -10bps this morning after that inflation report. Perhaps more interesting is the fact that despite Takaichi-san becoming PM, with her platform of increased fiscal spending, JGB yields are 2bps lower this morning.

Turning to the rest of the commodity space, oil (+2.1%) is rising on the news that the US has started to refill the SPR. While the initial bid is only for 1 million barrels, this is seen as the beginning of the process with the administration taking advantage of the recent low prices. Arguably, given they want to see more drilling as well, it is very possible that $55/bbl is as low as they really want it to go. As to the metals beyond gold (-2.4% this morning), silver (-1.6%) is still getting dragged along but copper (+0.6%) and platinum (+0.9%) seem to be consolidating after sharp declines in both. My sense is gold remains the liquidity asset of choice given its far larger market value. (One other thing to note is that there was much discussion how gold has replaced Treasuries as the most widely held central bank reserve asset. That was entirely a valuation story, not a purchase story. In other words, the dramatic rise in the price of gold increased the value of its holdings relative to other assets on central bank balance sheets.)

Finally, the dollar is doing just fine. It continues within its recent trading range and basically hasn’t gone anywhere in the past six months. In fact, of you look at the DXY chart below from Yahoo Finance, it is arguably in the upper quintiles of its long-term price action. It is very difficult for me to listen to all the reasons that the dollar is going to be replaced by some other reserve currency and take it very seriously.

As to specific currency moves today, the pound (-0.3%) is slipping on the increased belief in a rate cut coming soon and ZAR (-0.5%) is suffering on the ongoing gold price decline but away from those two, +/-0.1% is the story of the day.

EIA Crude Oil inventories are the only data of the day with a modest build expected. Yesterday, Governor Waller discussed payment systems and cryptocurrencies never straying into monetary policy so we will need to wait for CPI on Friday, the FOMC next Wednesday and whenever the government reopens, which I sense is coming sooner rather than later as the Democrats have been completely unsuccessful in making the case this is President Trump’s fault.

It appears the cracks in the leverage that has accompanied the recent rally in asset prices are beginning to appear. If things get worse, and they probably will, look for the Fed to respond and haven assets to be in demand. Amongst those will be the dollar.

Said Xi, we’ll sell rare earths no more Said Trump, well that means we’re at war The stock market puked As traders got spooked And Trump imposed tariffs galore

The question is just why would Xi Get feisty when things seemed to be Improved for both sides With fewer divides Did Mideast peace kill his esprit?

Let’s talk about markets for a moment. Sometimes they go down and go down fast when you’re not expecting it. That is their very nature, so it is important to understand that Friday’s price action, while dramatic relative to what we have seen over the past 6 months, is not that uncommon at all over time. It appears the proximate cause of the market decline was the word from China that they would stop selling and exporting rare earth minerals.

It can be no surprise that President Trump immediately responded by threatening an additional 100% tariffs on all Chinese exports and new controls on software, all to be implemented on November 1st. There is a lot of tit-for-tat in the dueling messages from China and the Trump administration and it is hard to tell what is real and what isn’t. However, equity markets clearly weren’t prepared for a break in the previous expectations that the US and China were closing in on a more lasting trade stance.

But weekends are a long time for markets as so much can happen while they are closed. This weekend was a perfect example. After the carnage on Friday, we cannot be that surprised that both sides of this new tiff modified their responses.

First we saw this on Truth Social:

Then China backed off clarified that what they are really doing is require licensing for all rare earth minerals and products that contain them in exports. China claims that applications that meet regulations will be approved although the regulations have not yet been defined. Ostensibly this is for national security reasons, and it is unclear exactly who will receive licenses, but this is clearly not the same as ending exports.

And just like that, many of the fears that were fomented on Friday have been alleviated as evidenced by this morning’s equity market moves in the futures markets.

Source: tradingeconomics.com

But why did Xi make this move in the first place? I have no idea, nor does anyone but Xi, although here are two completely different thought processes, one very conspiratorial and one rooted in the broader escalation of geopolitical affairs.

As to the first, (Beware, you will need your tinfoil hat here!) consider if the Israel-Gaza peace settlement, (with the hostages returned as of the time I am writing this morning at 5:30) does not serve China’s interest. First, the one Middle East nation that will be on the outside is their ally, Iran. Second, the ongoing problems there were always a distraction for the US, something that clearly suits Xi and China. After all, if the US is focused there, they will have more difficulty paying attention to things Xi cares about like Taiwan and the South China Sea. If the peace in Israel-Gaza holds, and the Abraham Accords extend to the bulk of the rest of the region, Xi loses a major distraction that cost him virtually nothing. Plus, this opens the door for tightening sanctions on Iran even further, which could negatively impact China’s oil flows.

The second is much more esoteric and I read about it this weekend from Dr Pippa Malmgren, someone who has a deep insight into global politics from her time as a presidential advisor as well as from her father, Harold Malmgren, who advised four presidents. In her most recent Substack post she explained the importance of Helium-3 (3He), a rare isotope of helium that has major energy and military implications and where the largest deposit of the stuff known to man is on the moon. Her claim is this is the foundation of the recent acceleration in the space race between the US and China and without rare earth minerals, the US ability to achieve its goals and obtain this element would be greatly hampered opening the door for China to get ahead.

Are either of these correct? It is not clear, but I would contend each contains some logic. In the end, though, as evidenced by the quick retreat on both sides, I suspect that the trade situation between the US and China will move forward in a positive manner, although there could well be a few more hiccups along the way. And those hiccups could easily see equity markets decline such that there is a real correction of 15% to 20%. Just not today.

So, what is happening today? Let’s look. First, I would be remiss if I didn’t highlight the following Bloomberg headline: ‘Buy the Dip’ Call Grows Louder as China Selloff Seen Contained, as it perfectly encapsulates the ongoing mindset in equity markets. At least in US equities. Asia had a much rougher session despite the backtracking with HK (-1.5%) and China (-0.5%) under pressure and weakness virtually universal in the time zone (Korea -0.7%, India -0.2%, Taiwan -1.4%, Australia -0.8%). Tokyo was closed. It appears there are either still concerns over the trade situation, or perhaps the fact that globally, markets have had long rallies has led to some profit taking amid rising uncertainties.

European bourses, though are all in the green, with the continent seeing gains of 0.5% or so across the board although the UK is lagging with a miniscule 0.05% gain at this hour (6:30). As to US futures, as seen above, gains range from 1.0% (DJIA) to 2.0% (NASDAQ).

Meanwhile, bond yields also saw a dramatic move on Friday, tumbling -8bps and back to their lowest level seen in a month as per the below chart from tradingeconomics.com

This morning, those yields are unchanged. European sovereign yields, which followed Treasury yields lower on Friday are also little changed at this hour, down another -1bp as concerns begin to arise that economic growth is going to be impaired by the escalation in trade tension between the US and China.

I would argue that commodities are the one area where the back and forth is raising the most concern. At least that is true in metals markets, with gold, which rallied 1% Friday amid the equity carnage, higher by another 1.6% this morning, to more new highs and we are seeing silver (+1.6%), copper (+4.2%) and Platinum (+3.6%) all in sync. To me, this is the clearest indicator that there is an underlying fear pervading markets. Oil (+1.8%) has rebounded from Friday’s rout as the easing of trade tensions appears to have calmed the market somewhat, although WTI remains just below $60/bbl at this point.

Finally, the dollar is firmer again this morning as, although it softened slightly Friday, it has since regained most of those losses and is back on its recent uptrend as you can see below.

Source: tradingeconomics.com

While Tokyo was closed overnight, we did see further JPY weakness as the yen retraced most of its Friday gains like the rest of the market. The biggest G10 mover was CHF (-0.9%) followed by AUD (-0.7%) and JPY (-0.7%) with other currencies less impacted and NOK (+0.2%) benefitting from the oil rally. However, the EMG bloc has seen a much wider dispersion with MXN (+0.5%), ZAR (+1.1%) and CLP (+0.8%) all rallying sharply on the metals rally while PLN (-0.5%) and CZK (-0.4%) lag as they follow the euro lower.

And that’s enough for today. With the government still on hiatus, no official statistics will be released although we do get a little bit of stuff as follows:

Tuesday

NFIB Small Business Index

100.5

Wednesday

Empire State Manufacturing

-1.8

Fed’s Beige Book

Thursday

Philly Fed Manufacturing

9.1

Source: tradingeconomics.com

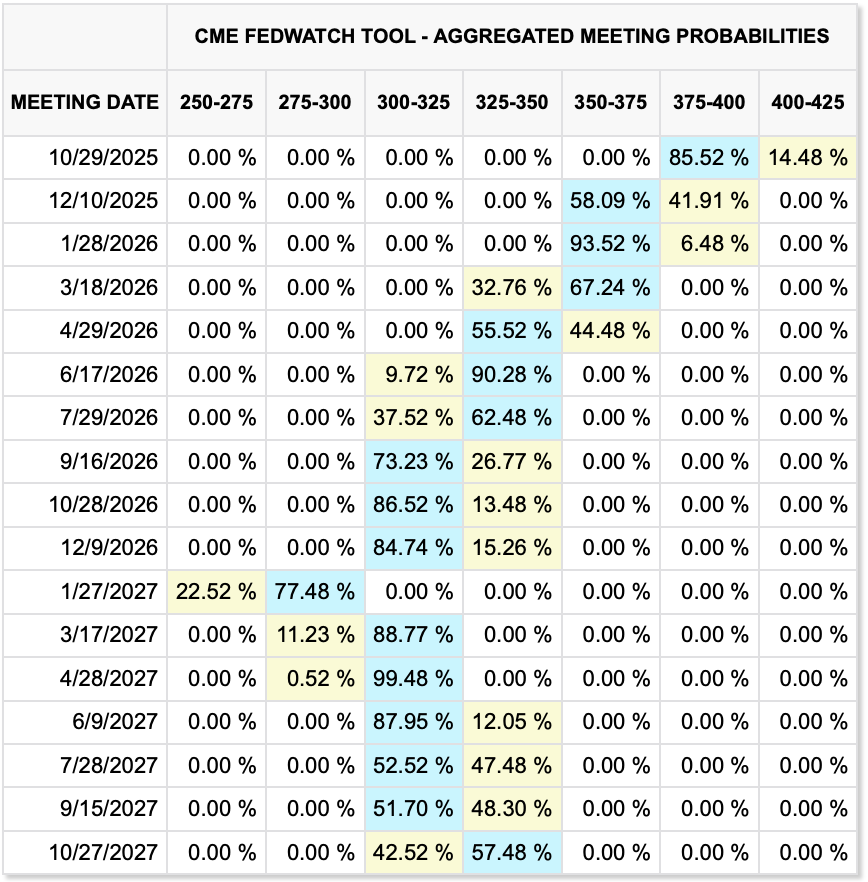

But, with the lack of data, it appears Chairman Powell has instructed his minions to flood the airwaves with a virtual cacophony of speeches this week, I count 18 on the calendar including the big man himself on Tuesday afternoon. It seems difficult to believe that their opinions on the economy will have changed very much given the lack of new data. The market is still pricing a 98% chance of a cut at the end of this month and another 91% chance of a cut in December. With the increased trade tension, there is much more discussion regarding a slower economic course ahead, which would play into further rate cuts. However, while that would clearly help precious metals as it ends any ideas of an inflation fight, it is not clear it will weaken the dollar very much as everybody else will almost certainly follow along.

The news of the day is that gold Is actively bought, never sold The Four Thousand level Led some folks to revel And drew many more to the fold

But weirdly, the dollar keeps rising Which based on the past is surprising The problems in France And Sanae’s stance Have been, for the buck, energizing

A month ago, many Wall Street analysts came out with forecasts that gold could trade as high as $4000/oz by mid 2026 as they reluctantly jumped on the bandwagon. But, by many accounts, although my charts don’t show it, the barbarous relic’s futures contract traded a bit more than 120 lots at $4000.10 last night, nine months earlier than those forecasts.

Source: Bloomberg.com

Right now (6:20), the cash market is trading at $3957 (-0.1%) but there is absolutely no indication that the top is in. Rather, I have been reading about the new GenZ BOLD investment strategy, which is buying a combination of Bitcoin and gold. Mohammed El-Arian nicknamed this the debasement trade, which is a fair assessment and a number of banks have been jumping on this theme.

Perhaps more interesting than this story, which after all is simply rehashing the fact that gold is seen as a long-term hedge against inflation, is the fact that the dollar is trading higher alongside gold, which is typically not the case. In fact, for the bulk of my career, gold was effectively just another currency to trade against the dollar, and when the dollar was weak, foreign currencies and gold would rise and vice versa. But look at these next two charts from tradingeconomics.com, the first a longer term view of the relationship between gold and DXY and the second a much shorter-term view.

The one-year history:

Compared to the one-month history:

I believe it is fair to say that while there is a clear concern about, and flight from, fiat currencies, hence the strength of precious metals as well as bitcoin, in the fiat universe, the dollar remains the best of a bad lot. Yesterday I described the problems in France and how the second largest nation in the Eurozone was leaderless while trying to cope with a significant spending problem amid broad-based political turmoil. We have discussed the problems in Germany in the past, and early this morning, the fruits of their insane energy policies were shown by another decline in Factory Orders, this time -0.8%, far less than the 1.7% gain anticipated by economists. I don’t know about you, but it is difficult for me to look at the below chart of the last three years of Germany’s Factory Orders and see a positive future. Twenty-two of the thirty-six months were negative, arguably the driving force behind the fact that Germany’s economy has seen zero growth in that period.

Source: tradingeconomics.com

Meanwhile, the yen continues to weaken, pushing toward 151 now and quite frankly, showing limited reason to rebound anytime soon. Takaichi-san appears to be on board with the “run it hot” thesis, looking for both monetary and fiscal stimulus to help Japan grow itself out of its problems. The JGB market has sussed out there will be plenty more unfunded spending coming down the pike if she has her way as evidenced by the ongoing rise in the long end of the curve there. While the 30-year bond did touch slight new highs yesterday, the 40-year is still a few basis points below its worst level (highest yield) seen back in mid-May as you can see in the chart below. Regardless, the chart of JGB yields looks decidedly like the chart of gold!

Source: tradingeconomics.com

In a nutshell, there is no indication the fiscal/financial problems around the world have been addressed in any meaningful manner and the upshot is that more and more investors are seeking safety in assets that are not the responsibility of governments, but either private companies or have inherent intrinsic value. This is the story we are going to see play out for a while yet in my view.

Ok, so, let’s look at how markets overall behaved in the overnight session. China remains on holiday, but it will be interesting to see how things open there on Thursday morning local time. Japan, was unchanged overnight, holding onto its extraordinary post-election gains. As to the other bourses there, holidays abound with both Hong Kong and Korea closed last night and the rest of the region net doing very little. Clearly the holiday spirit has infected all of Asia! In Europe, though, we are seeing very modest gains across the board despite the weak German data. The DAX (+0.2%) has managed a gain and we are seeing slightly better performance in France (+0.4%) and Spain (+0.4%) with the UK (+0.1%) lagging slightly. On the one hand, these are pretty benign moves so probably don’t mean much, but it is surprising there are rallies here given the ongoing lousy data coming from Europe. As to US futures, at this hour (7:20), they are all pointing higher by just 0.1%.

In the bond market, yields are continuing to edge higher with Treasuries (+2bps) leading the way and European sovereigns following along with yield there higher by between 2bps and 3bps. There continues to be a disconnect between what appear to be government policies of “run it hot” and bond investors, at least at the 10-year maturity. Either that or there is some surreptitious yield curve control ongoing to prevent some potentially really bad optics.

In the commodity markets, oil (+0.1%) is still firmly ensconced in its recent range with no signs of a breakout. I read a remarkably interesting article from Doomberg (if you do not already get this, it is incredibly worthwhile) this morning describing the methods that the Mexican drug cartels have been heavily involved in the oil business in Mexico, siphoning billions of dollars from Pemex and funding themselves, and more importantly, how the US was now addressing this situation. This is all of a piece with the administration’s view that the Americas are its key allies and its playground, and it will not tolerate the lawlessness that has heretofore been rampant. It also implies that if successful, much more oil will be coming to market from Mexico, and you know what that means for prices. As to the metals markets, they are taking a breather this morning with gold (-0.1%) and sliver (-0.3%) consolidating after yesterday’s rally. We discussed gold above, but silver is about $1.50 from the big round number of $50/oz, something that I am confident will trade sooner rather than later.

Finally, the dollar is rallying again with the euro (-0.5%) and pound (-0.6%) both under pressure and dragging the rest of the G10 with them. If the DXY is your favorite proxy, as you can see from the chart below, this is the 4th time since the failed breakout in late July that the index is testing 98.50 from below. It seems there is some underlying demand, and I would not be surprised to see another test of 100 in the coming days.

Source: tradingeconomics.com

It should be no surprise that the CE4 currencies are all under pressure this morning and we have also seen weakness in MXN (-0.3%) and ZAR (-0.3%) although given the holidays in Asia, it is hard to make a claim there other than that INR (-0.1%) continues to steadily weaken and make new historic lows on a regular basis.

With the government shutdown continuing, there is still no official data although there is a story that President Trump is willing to have more talks with the Democrats. We shall see. I think the biggest problem for the Democrats in this situation is that according to many polls, nobody really cares about the shutdown, with only 6% registering any concern. It is a Washington problem, not a national problem. Of course, FOMC members will continue to speak regardless of the shutdown and today we hear from four more. Interestingly, nothing any of them said yesterday was worthy of a headline in either the WSJ or Bloomberg which tells me that there is nothing coming from the Fed that matters.

Running it hot means that we will continue to see asset prices rise, bond prices suffer, and the dollar likely maintain its current level if not rally a bit. We need a policy change somewhere to change that, and I don’t see any nation willing to make the changes necessary. I have no idea how long this can continue, but as Keynes said, markets can remain irrational longer than you can remain solvent. Be careful betting against this.

Though stocks worldwide this year are higher Investors have sought to inquire If their dreams of riches Might have a few glitches And if they all sell, who’s the buyer?

Meanwhile, the key news of the day Revolves around government pay Will seven Dems buck The warnings of Chuck Or will the “resistance” hold sway?

Midnight tonight is the deadline for Congress to pass a continuing resolution to keep the government funded. Democratic leaders, Representative Hakeem Jeffries and Senator Chuck Schumer, met with President Trump yesterday but came to no agreement. The House has passed a clean CR, meaning it continues funding exactly as currently laid out, but the Senate needs 60 votes and Minority leader Schumer wants to increase spending by upwards of $1.5 trillion over the next 10 years to support the CR.

Looking at the list of Senators, I count 9 democrats in states that President Trump won in the 2024 election and who may feel it is in their best interest to consider voting for the resolution than shutting down the government although history shows elected Democrats vote the party line regardless of the consequences.

I asked Grok what happens in a shutdown and reading through what occurs in each cabinet department, it will take several weeks, I believe, before anybody really notices. The War Department and Homeland Security continue to function, so ICE agents are not going to disappear from the streets anytime soon. Too, Social Security, Medicare and Medicaid are untouched. I would argue those are the biggest issues. The FBI and prisons remain active as does the FAA and TSA. Maybe the biggest short-term issue is economic data will be delayed so there will be no NFP on Friday. Given its recently demonstrated inaccuracies, that may be a benefit, although I’m sure that’s not the case.

Of course, the most important question is, will a government shutdown cause the stock market to decline, as we all know a rising stock market is the MOST important thing ongoing! Thus far, it doesn’t appear investors are that worried, but perhaps that will change today. After all, all the major US indices rallied yesterday although as of this morning (6:25) futures are pointing lower by about -0.1%.

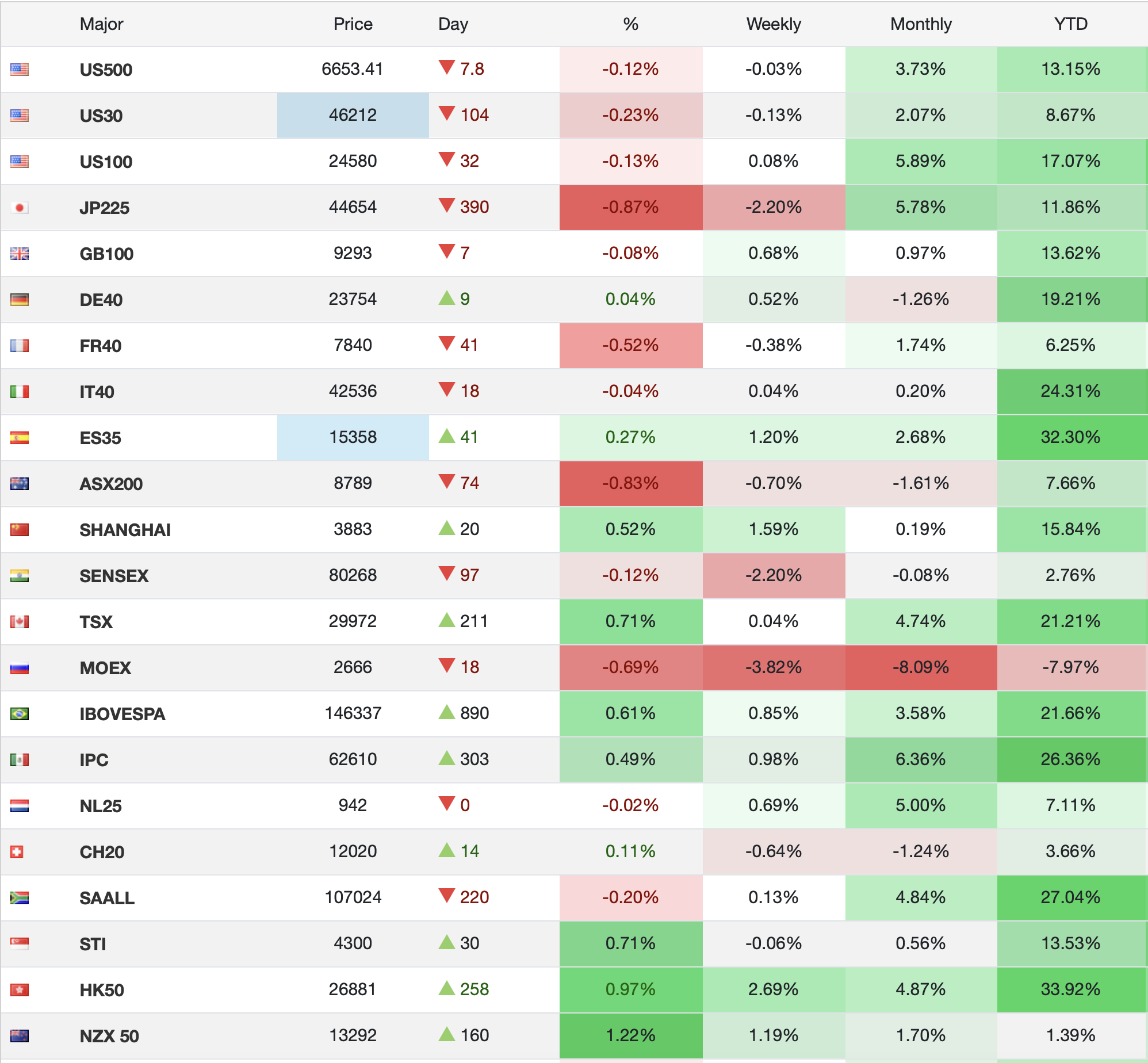

But here’s the thing about stocks, no matter how much angst some folks have had, and how many calls for recession have been made, and how much people may hate President Trump, below is a table from tradingeconomics.com showing most major stock market indices and their performance YTD at the far right. Take away Russia, which isn’t really major, and there is an awful lot of green!

Perhaps the proper question is, why has this been the case and can it continue? Certainly, the fiscal underpinnings of almost every nation are deteriorating as debt grows rapidly alongside government spending while the prospects of repaying said debt diminishes. So, the macroeconomic backdrop in many nations is shaky, at best (France, UK, US, Germany, Australia, Japan, to name a few).

Of course, any individual company will typically reflect the prospects of that company, the very fact that markets have rallied so strongly this year continues to support the rally. Remember, there have been numerous recession calls, and even the Fed has begun to look at the employment situation as becoming a bigger issue than inflation, indicating they, too, are concerned over future economic growth prospects. Hence, the widespread expectations for further rate cuts. in fact, looking at the futures market, not only is it pricing two more cuts this year, but a further two more by September 2026, and then a long period of 3.0% Fed funds afterwards.

Thus, it appears the equity market is counting on rate cuts to support future earnings even though those rate cuts imply weaker economic activity which will undermine future earnings. Quite the balancing act! But then, I’m just an FX guy, so the intricacies of equities are clearly lost on me.

Ok, you’ve already seen the overnight equity movement with Chinese shares the largest beneficiary of PMI data showing modest growth. Combining that with the news of further stimulus yesterday and things in China look pretty good right now.

Turning to bonds, yields fell yesterday despite any noteworthy data. Perhaps it was the Fed speakers who highlighted the need to ease policy further as their concerns grow over slowing employment. At any rate, this morning, 10-year Treasury yields are unchanged at 4.14%, while a few bps above the lows seen last week, hardly demonstrating a major move higher. European sovereign yields have edged higher by 1bp this morning across the board, also not really demonstrating much concern about things. We did see some Eurozone data this morning with French inflation soft (1.2% Y/Y) while German Unemployment rose slightly and German state inflation data has generally been higher than last month. The nationwide number is released at 8:00 this morning. Meanwhile, Italian inflation was a bit softer than forecast (1.6%), so bond investors seem satisfied for now.

As has been the case for a while now, the biggest moves have come in the commodity space with oil (-0.7%) falling back to the middle of its trading range as per the below chart from tradingeconomics.com.

For whatever reason, the end of last week had oil bulls out in force, but they are an unhappy lot this morning. Apparently, President trump and Israeli PM Netanyahu have agreed a Gaza peace plan, although the Palestinians were not privy to the details. Perhaps peace there is reducing concerns in the oil market although I would have thought the Russia/Ukraine situation has a more direct impact. As to metals, after another series of new highs across the precious space yesterday, this morning we are finally seeing a bit of profit taking (Au -0.7%, Ag -1.7%, Pt -2.8%, Cu -1.0%). However, it is difficult to look at the chart and sense that this is over.

Source: tradingeconomics.com

Finally, the dollar is a touch softer this morning, essentially unchanged vs. the euro and pound although the yen (+0.4%) and Aussie (+0.4%) have both managed to rally. The RBA met last night and left rates on hold, as expected, although their commentary afterwards had a hawkish tilt regarding the future of inflation which undermined equities and helped the currency. As to the yen, their ‘Minutes’ were released and indicated there was growing support for a rate hike in October, although I will believe it when I see it. But away from those two, there was virtually no movement and no news of note.

On the data front, I will lay out the alleged releases, although with the shutdown, the BLS and BEA ones will likely be delayed.

Today

Case Shiller Home Prices

1.6%

Chicago PMI

43.0

JOLTs Job Openings

7.2M

Consumer Confidence

96.0

Wednesday

ADP Employment

50K

ISM Manufacturing

49.0

ISM Prices Paid

63.2

Thursday

Initial Claims

223K

Continuing Claims

1930K

Factory Orders

1.4%

-ex Transport

0.1%

Friday

Nonfarm Payrolls

50K

Private Payrolls

60K

Manufacturing Payrolls

-7K

Unemployment Rate

4.3%

Average Hourly Earnings

0.3% (3.7% Y/Y)

Average Weekly Hours

34.2

Participation Rate

62.3%

ISM Services

51.7

Source: tradingeconomics.com

Today’s data will be released, and tomorrow’s is privately sourced, so shouldn’t be a problem, but come Thursday and Friday, that’s when things will go missing. Ironically, the biggest impact will be on options traders who frequently place trades in anticipation of a data point, and with that data point missing, those premia are likely to diminish quickly. Too, spare a moment for the algorithms who won’t have anything to trade against without data. Poor programs 🤣.

History has shown the dollar tends to decline through government shutdowns, if they last any length of time (>3 or 4 days), so if we shut down and are still that way next week, I expect we could see some weakness. But I’m sure there will be one more vote today to see if it will happen. My take is a shutdown is in the cards but for how long, I have no idea.

The battlelines are being drawn On one side, the dollar is gone ‘Cause debt will explode And once down that road They claim folks would rather the yuan

But others are making the case That dollar debt has much more space To grow and expand As it can withstand More stress since it’s used everyplace

And finally, one thing left to note Is Europe appears set to float A digital euro That ought to ensure-oh The market, its price, will demote

Friday, I highlighted an idea which I had toyed with, but never explained eloquently, but that was done so by Michael Nicoletos (@mnicoletos on X). While I offered a link to his work Friday, I know that many never click on links in notes like this, so I am copying his page showing this perspective. It is clear, clean and asks the proper questions.

The reason I am doing this is because this weekend, I listened to a podcast with another very smart macro guy, Luke Gromen (@lukegromen) who has a very different take on the state of the world. In short, Luke’s belief is that the US is already past the point of no return and that a potential downward spiral, caused by excessive US debt, is going to kick off soon. The result is that we will see the dollar decline severely (as described by the DXY), gold, bitcoin, and equities rally, and that Treasury debt, especially long dated debt, will get killed. In essence, he is explaining the inflation trade, higher US inflation will lead to those outcomes.

Let me start by saying, I agree with Luke on certain things, like the fact that we are likely to see higher inflation going forward as the government is in no mood to cut off the liquidity taps. If you look at the below chart of M2 from the FRED database of the St Louis Fed, you can see that this measure has set a record high and risen 7.8% since its local nadir on October 30, 2023.

So, in a bit less than 2 years, it has grown about 8% after having shrunk that much in the prior 2 years during the first phases of the Fed’s QT program. But now, despite the fact the Fed continues to slowly shrink their balance sheet, money supply is growing again, and my take is it will continue to do so for the foreseeable future as the government needs to essentially monetize the debt.

Back to the argument, I believe that in this scenario of run it hot, gold and equities will do well while bonds will do poorly, but the question of the dollar on the FX markets is very different. And this is where the Nicoletos’s theory comes into play. If he is correct, and we adjust our idea about what constitutes excess leverage for the US, then expecting the dollar to fall in the FX markets may not be the best idea. Rather, the news that the ECB is seeking to institute a digital euro, as per a speech by Madame Lagarde two weeks’ ago, and UK PM Starmer is claiming digital ID is necessary, to be followed by a digital pound, leads me to believe that institutions and individuals may decide they want more control over their own finances, rather than governments who have proven themselves exceptionally incompetent across numerous areas (energy, finance, and defense come to mind). That implies that the dollar is likely to find a lot more support than those claiming it is set to collapse.

Again, I ask, will developing nations really want to keep their reserves in the CNY, or store their reserves of gold in Shanghai given the long history of capriciousness that the CCP has demonstrated. People may hate the US; yet more people want to come here than go anyplace else because they have a higher degree of faith that their property will remain their property.

This is not to say things are great, there are huge problems worldwide, just to say that my medium- and longer-term views are the dollar will be seen as TINA if other nations go down the road they are currently claiming they will follow.

The overnight narrative’s turned To government shutdown concerns As Trump and Dems meet The word on the Street Is too many bridges are burned

As to this morning’s market activity, the most noteworthy story is the question of whether the Senate will pass a continuing resolution (CR) to keep the government operating past midnight on Tuesday when the current spending authority runs out. The House of Representatives have passed a ‘clean’ resolution which leaves the spending levels exactly where they are and lasts for 6 weeks allowing Congress time to pass the individual spending bills. However, in the Senate, they need 60 votes to overcome the filibuster, and the Republicans only have 53 seats. Minority Leader Schumer has promised to shut down the government unless he gets spending promises in the CR of upwards of $1 trillion over the next 10 years, and that feels unlikely. Too, the House of Representatives is in recess, so no changes to their bill can be made on a timely basis.

My take is the Senate will cave in, but if not, they will not be able to withstand the pressure for very long as I believe that they will ultimately receive the blame for the outcome. Turning to the market impact of this story, the most notable move overnight has been in precious metals where Gold (+1.3%), Silver (+1.8%) and platinum (+0.8%) are all continuing their recent runs and all at recent (and for gold all-time) highs. However, it is difficult for me to understand this as a response to the potential shutdown in isolation.

Perhaps, if we turn to the dollar, which is lower, but only by -0.2% on the DXY, we can have a better understanding as at least it would make some sense that the dollar declines if the government does shut down. And certainly, a weaker dollar manifests as stronger commodity prices, but the metals moves are so much larger, I have to believe there is another driver there. Some talk focuses on the fact that Friday’s PCE data was not too hot thus keeping alive the hopes for further Fed rate cuts. Personally, I lean toward the idea that the combination of concerns over increased military activity and the ensuing inflation are much more likely to be the drivers of precious metals’ rally.

Weirdly, despite concerns over inflation, bond yields are not responding in the manner one might expect as Treasuries are lower by -3bps and we are seeing similar moves throughout all the European sovereigns this morning. As well, there was a very interesting article in the WSJ this morning about the fact that credit markets are incredibly strong, meaning the spread between corporate and Treasury yields has shrunk to the lowest levels on record for investment grade, and near that for junk bonds.

To sum this up, bond markets are completely unconcerned with future inflation while precious metals markets are screaming inflation is coming soon. Of course, one possible explanation for this seemingly divergent behavior is that the amount of liquidity that continues to be pumped into markets globally by central banks is driving fixed income investors to seek investments within their remits, i.e. bonds, while others are watching and trying to prepare for the inevitable. In a funny way, the fixed income folks may be doing the right thing because if YCC comes into play, and I am almost certain it will, then yields will be lower still!

As to the rest of markets, equities are all about more liquidity as Friday’s US rally, which is continuing this morning with futures higher by 0.5% at this hour (7:15) demonstrates. In Asia overnight, Japan (-0.7%) did not follow suit as a BOJ member hinted that a rate hike was coming at the October meeting, and we all know how much equities hate rate hikes. But China (+1.5%) and HK (+1.9%) both rocked as word of a new government plan to inject CNY 500 billion into local governments to spur investment made the news. Korea also benefitted from the combination of those things although India was unchanged and Taiwan (-1.7%) seemed to respond to a story that President Xi is seeking to get President Trump to agree that Taiwan is part of China.

As to Europe, the UK (+0.55%) is the leading gainer amid stories about pharma giants there raising prices, while continental markets are +/-0.2%, really not showing much life at all.

Oil (-1.8%) is slipping on news that Kurdish oil in the amount of up to 180K bbl/day is going to start flowing to the market again, adding to supply as OPEC is also talking of increasing production. There was, however, an interesting article in the WSJ about the fact that Russian production is starting to turn down as 3 years of war and sanctions has reduced their capability of producing absent Western technology.

Finally, the dollar, as mentioned above, is a bit softer this morning with JPY (+0.4%) and NZD (+0.4%) the G10 leaders although the rest of the bloc has seen gains on the order of 0.1% or 0.2% only. In the EMG bloc, KRW (+0.6%) is top dog with CNY (+0.2%) actually the next best performer. So, overall, movement here has not been that impressive despite the narrative.

I’ve gone on far too long and as there is no front-line data today, I will post it tomorrow. Of course, payrolls come Friday and be aware of five Fed speakers today and a total of ten this week.

While many have called for stagflation The ‘stag’ story’s lost its foundation Q2 turned out great With growth, three point eight While ‘flation showed some dissipation

Meanwhile, Mr Trump’s on a roll As he strives to still reach his goal It’s tariff redux On drugs and on trucks While ‘conomists tally the toll

Analysts worldwide have decried President Trump’s policies as setting up to lead the US to stagflation with the result being the dollar would ultimately lose its status as the world’s reserve currency while the economy’s growth fades and prices rise. “Everyone” knew that tariffs were the enemy of sane fiscal and trade policy and would slow growth leading to higher unemployment and inflation while the Fed would be forced to choose which issue to address. In fact, when Q1 GDP was released at -05%, there was virtual glee from the analyst community as they were preening over how prescient they were.

But yesterday, we learned that things may not be as bad as widely hoped proclaimed by the analyst community after all. Q2 GDP was revised up to +3.8% annualized growth, substantially higher than even the first estimate of 3.0% back in July. Not only that, Durable Goods Orders rose 2.9% with the ex-Transport piece rising 0.4% while the BEA’s inflation calculations, also confusingly called PCE rose 2.1%. Initial Claims rose only 218K, well below estimates and indicative that the labor market, while not hot, is not collapsing. Finally, the Goods Trade Balance deficit was a less than expected -$85.5B, certainly not great, but moving in President Trump’s preferred direction.

In truth, that was a pretty strong set of economic data, better than expectations across the entire set of releases, and clearly not helping those trying to write the stagflation narrative. Now, Trump is never one to sit around and so promptly imposed new tariffs on medicines, heavy trucks and kitchen cabinets to try to bring the manufacture of those items back into the US. Whatever your opinion of Trump, you must admit he is consistent in seeking to achieve his goal of returning manufacturing prowess to the US.

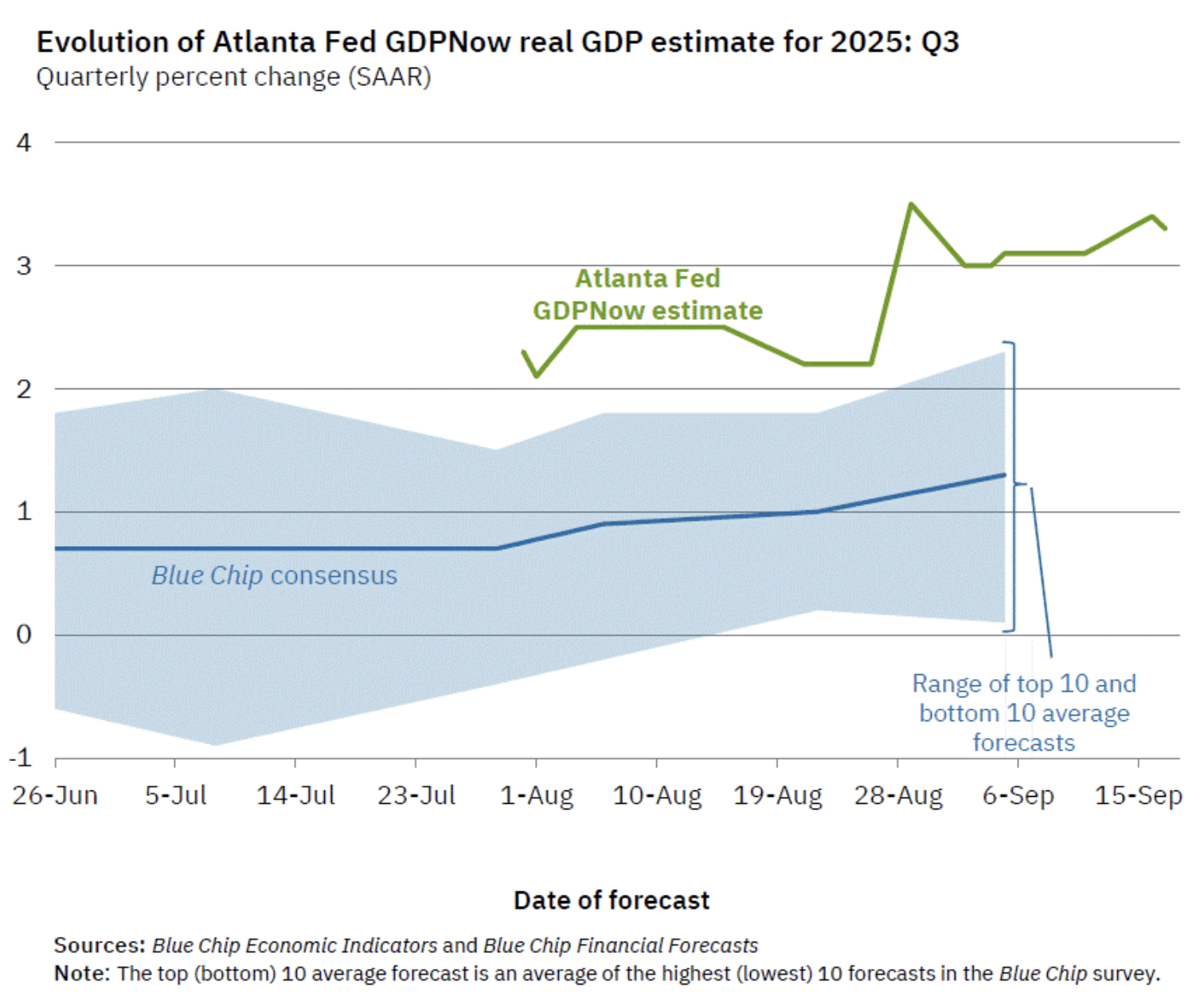

Meanwhile, down in Atlanta, their GDPNow Q3 estimate is currently at 3.3%, certainly not indicating a slowing economy.

In fact, if that pans out, it would be only the 14th time this century that there were two consecutive quarters of GDP growth of at least 3.3%, of which 4 of those were in the recovery from the Covid shutdown.

It would be very easy to make the case that the US economy seems to be doing pretty well, at least based on the data releases. I recognize that there is a great deal of angst about, and I have highlighted the asynchronous nature of the economy lately, but what this is telling me is that things may be syncing up in a positive manner.

So, what does this mean for markets? Perhaps the first place to look is the Fed funds futures market as so much stock continues to be put into the Fed’s next move. Not surprisingly, earlier exuberance over further rate cuts has faded a bit, with the probability of an October cut slipping to 85%, down about 10 points in the wake of the data, and a total of less than 40bps now priced in for the rest of the year. Recall, it was not that long ago that people were considering 100bps in the last three meetings of the year.

Source: cmegroup.com

The next place to look is at the foreign exchange markets, where the dollar’s demise has been widely forecast amid changing global politics with many pundits highlighting the idea that the BRICS nations would be moving their business away from dollars. For a long time, I have highlighted that the dollar is currently within a few percent of its long-term average price, neither particularly strong nor weak, and that fears of a collapse were unwarranted. However, I have also recognized that a dovish Fed could easily weaken the dollar for a period of time. Short dollar positions remain large as the leveraged community continues to bet on that outcome, although I have to believe it is getting expensive given they are paying the points to maintain that view.

But if we look at how the dollar has performed over the past several sessions, using the DXY as our proxy, we can see that despite a very modest -0.1% decline overnight, it appears that the dollar may be breaking its medium-term trend line lower as per the chart below from tradingeconomics.com

Again, my point is that the idea that the US is facing a catastrophic outcome with a recession due and a collapsing dollar is just not supported by the data or the markets. And here’s an interesting thought from a very smart guy, Mike Nicoletos (@mnicoletos on X) regarding some of the key drivers of the current orthodoxy regarding the dollar, notably the debt and deficit. What if, given the dollar’s overwhelming importance to the world economy, we should be comparing those things to its global scale, not just the domestic scale. If using that framework, as he describes here, the debt ratio falls to 58% and the budget deficit is down to 2.9%, much less worrying and perhaps why markets and analysts are out of sync.

Markets are going to go where they will, but having a solid framework as to how the economy impacts them is a very helpful tool when managing money and risk. Perhaps this needs to be considered overall.

Ok, a really quick tour. Yesterday was the third consecutive down day in the US, although all told, the decline has been less than -2%, so hardly devastating. Asia mostly fell overnight as concerns over both tariffs and a Fed less likely to cut rates weighed on equities there with Japan (-0.9%), China (-1.0%) and HK (-1.35%) all under pressure. The story was worse for other regional bourses with Korea (-2.5%), India (-0.9%) and Taiwan (-1.7%) indicative of the price action.

However, Europe has taken a different route with modest gains across the board (DAX +0.3%, CAC +0.45%, IBEX +0.6%) as investors seem to be looking through the tariff concerns. US futures are also edging higher at this hour (7:45).

In the bond market, Treasury yields have slipped -1bp this morning, and while they remain above the levels seen immediately in the wake of the FOMC last week, they appear to be finding a home at current levels of 4.15% +/-. European sovereigns are all seeing yields slip -3bps this morning as today’s story is focusing on how most developed nations are reducing the amount of long-dated paper they are selling to restrict supply and keep yields down. This has been decried by many since then Treasury Secretary Yellen started this process, but as with most government actions, the expedience of the short-term benefit far outweighs the potential long-term consequences and so everybody jumps on board.

Turning to commodities, oil (-0.1%) is still trading below the top of its range and while it has traded bottom to top this week, there is no sign of a breakout yet. I read yet another explanation yesterday as to why peak oil demand is going to be seen this year, or next year, or soon, which will drive prices lower. While I do think prices eventually slide lower, I take the other side of that supply-demand idea and believe it will come from increased supply (Argentina, Guyana, Brazil, Alaska) rather than reduced demand. In the metals markets, yesterday saw silver (-0.2%) jump nearly 3% to yet another new high for the move as traders set their sights on $50/oz. Meanwhile gold (0.0%) continues to grind higher in a far less flashy manner than either silver or platinum (+10% this week) as regardless of my explanation of relative dollar strength vs. other fiat currencies, against stuff, all fiat remains under pressure.

And finally, the dollar after a nice rally yesterday, is consolidating this morning. The currency I really want to watch is the yen, where CPI last night was released at 2.5%, lower than expected and which must be giving Ueda-san pause with respect to the next rate hike. Most analysts are still convinced they will hike in October, but if inflation has stopped rising, will they? I would not be surprised to see USDJPY head well above 150, a level it is fast approaching, over the next month.

On the data front, this morning’s BLS version of PCE (exp 0.3%, 2.7% Y/Y) and Core PCE (0.2%, 2.9% Y/Y) is released at 8:30 along with Personal Income (0.3%) and Personal Spending (0.5%). Then at 10:00, Michigan Sentiment (55.4) is released and somehow, I have a feeling that could be better than forecast. We hear from a bunch more Fed speakers as well although a pattern is emerging that indicates they are ready to cut again next month, at least until they see data that screams stop.

The world is not ending and in fact, may be doing just fine, at least economically. Meanwhile, the dollar is finding its legs so absent a spate of very weak data, I think we may see another 2% or so rebound in the greenback over the next several weeks.

Right now, markets keep taking risk And lately, the pace has been brisk But coming next week We could see a peak If there’s no cash left in the fisc

A government shutdown would raise Concerns about ‘nomic malaise As well, what I see Is Trump’s OMB Is planning a RIF anyways

Volatility remains absent from most markets these days, metals excepted, and given the dearth of data until tomorrow’s PCE report, the focus is beginning to turn elsewhere. Perhaps the biggest story developing right now is the potential US government shutdown if no continuing resolution is passed by Congress. The government’s fiscal year runs from October 1 through September 30, and the rules are if Congress hasn’t passed appropriations bills by the end of the fiscal year, nonessential services are ended, and government employees are furloughed until that process is completed. As of right now, the House of Representatives has passed a clean bill, meaning it continues spending at the current rate, and we are all awaiting on the Senate. However, the Senate needs 60 votes to pass it to overcome the filibuster and right now, the Democratic Minority Leader, Chuck Schumer, claims they will not support the bill.

First, understand this is not unprecedented. In fact, according to Grok, it has happened 21 times since 1980 with the longest being 35 days in 2018-19 over funding for the border wall. Now, I ask you, can anyone remember the impact of any of those shutdowns, which in fairness typically last less than a week?

Next, it is worth understanding what actually happens during a shutdown. National Parks are closed, while passport services, HUD services, SBA services, scientific research and EPA inspections are the type of things that are put on hold. Also, the BLS will pause data collection and calculations, although given their recent track record, that may be seen as a benefit! But things like Social Security, Medicare, Medicaid and the Military are all unaffected.

Naturally, there is a lot of politicking ongoing with this process and apparently, President Trump has given marching orders for departments to begin a RIF if the government is shut down. So, when things reopen, there will be fewer federal employees, one of the goals of this administration, and something that is anathema to his opponents.

From a market perspective, the impact on equity markets during the December 2018 – January 2019 shutdown was actually a rally of just over 10%, although the market did decline in the month leading up to the shutdown. My point is, there is a lot more politics than economics in this process.

But away from that story, commodities remain the market with the most interest as oil (-0.5%) continues to trade within the range I highlighted earlier this week with a top at $65.50, but has made a technical break above its 50-day moving average, which has the bulls starting to get excited. As well, the backwardation of the curve is increasing, another bullish sign and much of this is being laid at the feet of President Trump’s seeming turn on the Russia/Ukraine war, where he is quite tired of President Putin’s dissembling. Certainly, a break above that range top would be at least short term bullish for crude.

Source: tradingeconomics.com

As to the precious metals, while gold continues to trade well, silver has taken the mantle and as you can see from the chart below, is accelerating higher at an even more impressive clip than the yellow metal. This is a common occurrence as silver historically outperforms gold, on a percentage basis, when both are in bull markets like this. Just wait until it reaches $50/oz, and makes new all-time highs, and you will see even more discussion of the metals and why they are rallying with inflation concerns a major part of that discussion.

Source: tradingeconomics.com

Meanwhile, financial instruments are far less exciting lately with equity markets stabilizing after their recent run and bond markets also doing little. Granted, we have seen two consecutive down days in US equity markets, but the magnitude of the decline was de minimis, so it is not really telling us very much. European markets appear more closely linked to the US, with all bourses there lower by between -0.1% and -0.5% this morning although we did see some modest gains in Asia (China +0.6%, Japan +0.3%). Net, it seems investors are not certain where to turn right now and are waiting for more clarity from the Fed as to whether more rate cuts are on the way.

The same is true of bond investors who apparently are unconcerned over the shutdown threats, with yields unchanged despite the increasingly combative rhetoric. We did hear from SF Fed president Daly yesterday, a known dove, who explained that she is coming around to the idea that more cuts are necessary, and they were simply waiting to see how tariffs were going to impact things. I might argue that she is anxious to cut rates but also doesn’t want to seem to support President Trump’s demands.

Finally, the dollar, after a pretty solid rally yesterday, is essentially unchanged this morning as well. (That seems to be the theme today, no change.). As I look across my screen, the largest move I see is 0.15%, which is how far CHF has declined on the session, otherwise things have been completely dead.

On the data front, this morning brings the weekly Initial (exp 235K) and Continuing (1930K) Claims data as well as Durable Goods (-0.5%, 0.0% ex-Transport) and the final Q2 GDP reading (3.3%) all at 8:30 with Existing Home Sales (3.96M) at 10:00. Yesterday saw New Home Sales rise dramatically more than expected at 800K although most analysts expect that number to be revised lower as the Census Bureau gets more information. Nonetheless, it is a sign that the economy is not collapsing, that’s for sure.

We also hear from four more Fed speakers today, Williams, Bowman, Barr and Daly again, and we will need to see how they all interpret the current situation. We learned from the dot plot that there are a lot of different opinions at the Fed right now, and personally, I am very glad to see that. Given the overall confusion, and the asynchronous nature of the economy right now, it would be more concerning if everyone was on the same page.

As far as the shutdown is concerned, you can be sure that this process will continue until next Tuesday night, at the earliest, if the Democrats cave, and if not, we will then be bombarded by both sides claiming it is the other side’s fault. Eventually a spending bill will be passed, and as we saw back in 2019, markets pretty much look through this stuff. Meanwhile, unless the data starts to really deteriorate and brings Fed comments along for that ride, I think the dollar is probably in a rough equilibrium space for now.