The Minutes explained twenty-five

Would likely still let markets thrive

But Powell demanded

A half, lest they landed

The ‘conomy in a crash dive

Yesterday’s release of the FOMC Minutes was enlightening to the extent it showed Chairman Powell did not have everybody in agreement for his 50bp rate cut last month. In the Fed’s own words, “…a substantial majority of participants supported lowering the target range for the federal funds rate by 50 basis points to 4-3/4 to 5 percent. However, noting that inflation was still somewhat elevated while economic growth remained solid and unemployment remained low, some participants observed that they would have preferred a 25 basis point reduction of the target range at this meeting, and a few others indicated that they could have supported such a decision.”

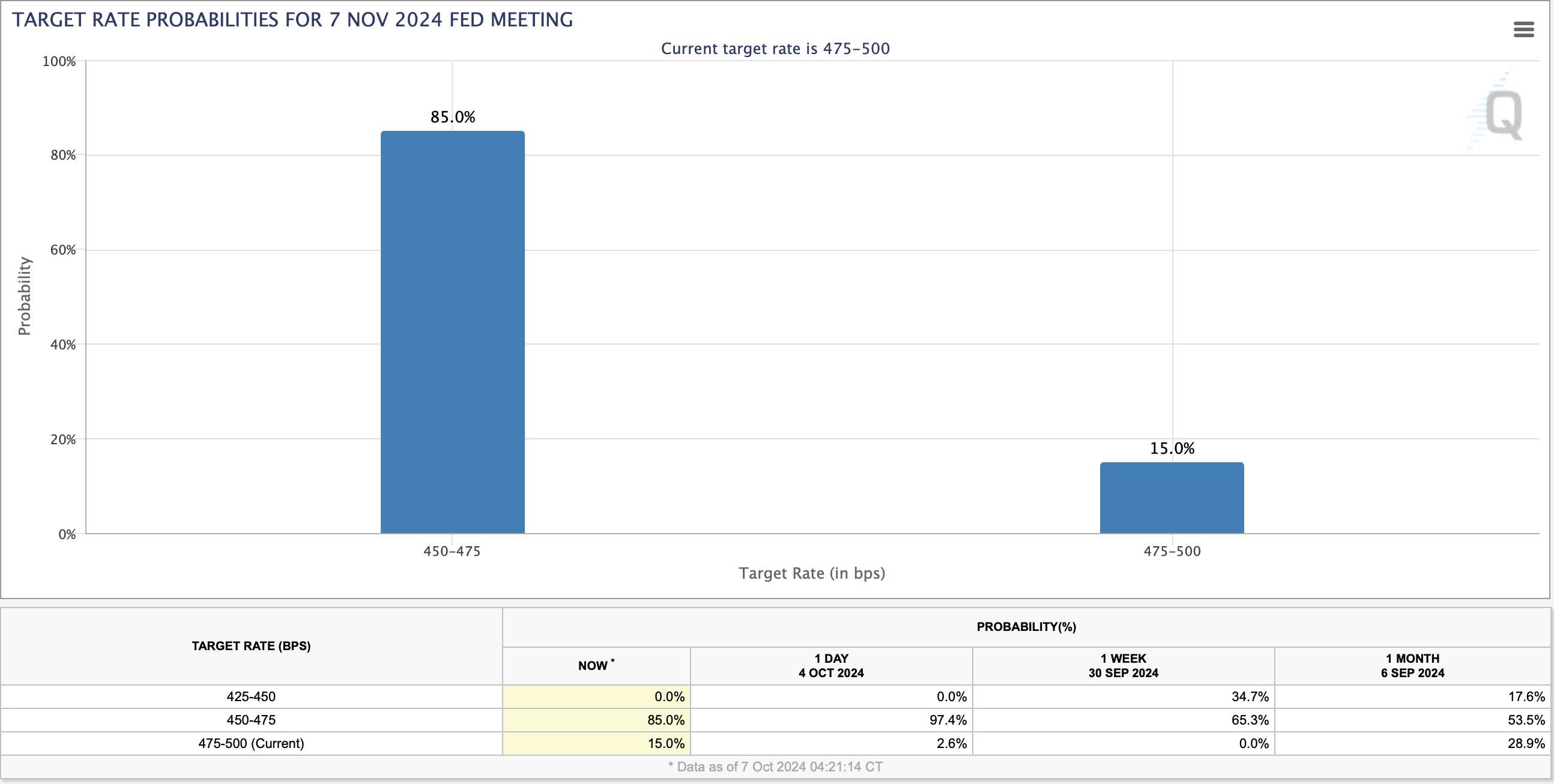

Remember, too, that this meeting was held two days prior to the NFP report which changed a great deal of thinking on the subject, not least by the Fed funds futures market which as of this morning is pricing a 20% probability of no cut at the November meeting. Looking at the GDPNow calculation from the Atlanta Fed, that NFP number increased the estimate to 3.4%, although recent inventory data has seen it slip back a tick as you can see below.

Source: atlantafed.org

Despite that last little dip, though, the estimate remains far stronger than economists’ forecasts and paints a picture of a resilient economy. (Perhaps adding $1.8 trillion via the budget deficit has something to do with that, but that is a story for a different time.). While the Fed is clearly anxious, if not desperate, to cut rates further, the economic case, with inflation remaining above their targets and the employment situation looking better amid solid economic growth, seems to be waning.

Three weeks ago, Jay and the Fed

Said joblessness was their, flag, red

Explaining inflation

Had taken vacation

So, more cutting rates was ahead

This morning we’ll learn if that’s true

Or if, like employment, their view

Is clouded and blurry

Which could cause some worry

For bulls and for Biden’s whole crew

Which leads us to the other key market story today (clearly the devastation from Hurricane Milton is the most important news of the day and my thoughts and prayers go to all those in its path), the CPI report. Current consensus expectations are for a 0.1% rise in the monthly headline reading which translates to a 2.3% Y/Y increase and a 0.2% rise in the monthly core reading which translates into a 3.2% Y/Y increase.

Looking at some obvious pieces of the puzzle, gasoline prices fell 8.4% in September, which is one of the reasons the headline number is below the core number. The thing is, gasoline prices this morning are almost exactly where they were at the beginning of September, which informs us that the headline number could easily retrace somewhat next month. The point is, we need to keep our eye on the core number (after all, the reason they created it was because food and energy prices were volatile and monetary policy’s impact on them virtually nonexistent, so they needed something that might give them a better feel for the reality elsewhere). And I don’t know about you, but if the target is 2.0% then 3.2% doesn’t seem that close. I know they are focused on core PCE, but even that remains well above their target.

One of the stories around this morning is that used car prices have stopped declining and that could have an outsized impact resulting in a higher than otherwise reading. But in reality, I question whether this matters at all. What we have learned from the Fed over the past month is that they are going to cut rates no matter what. While the pace of those cuts may be faster or slower depending on some data, every Fed speaker this week, and even a review of the Minutes, points to the fact that they are all desperate to keep cutting rates.

But you know who is taking exception to that stance? The bond market. Perhaps the bond vigilantes of late 90’s fame have been resurrected, or perhaps investors are simply looking at the fiscal situation in the US, where deficit spending continues to increase which means more and more Treasury debt will need to be issued and decided that even 4.0% is no longer a reasonable nominal return on their investment.

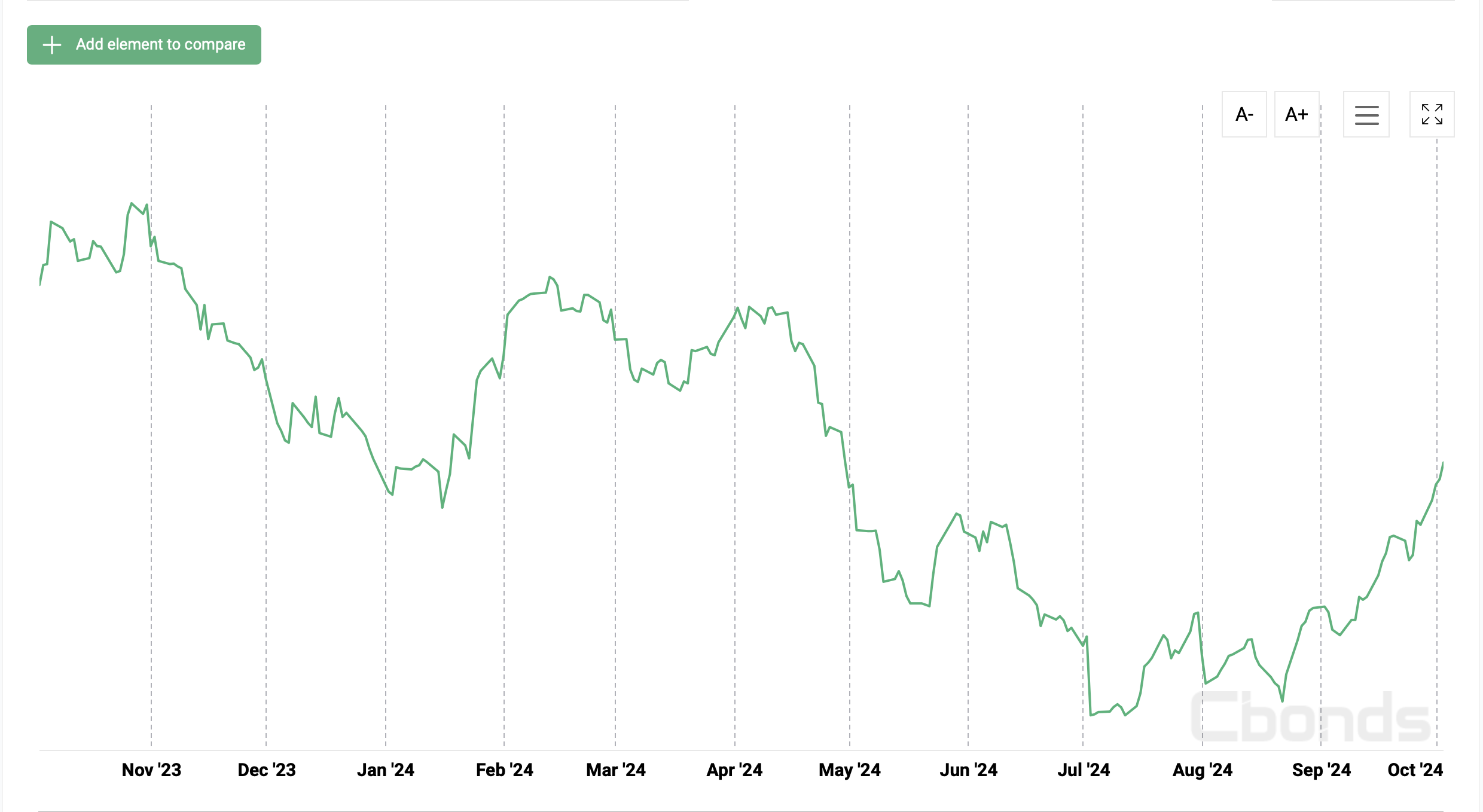

As you can see below, 10-year Treasury yields have risen 46bps since just before the last FOMC meeting as the stronger US data combined with the Fed’s clear focus on cutting rates has made investors nervous.

Source: tradingeconomics.com

You may recall the discussion about the inverted yield curve, where 2yr yields traded above 10yr yields for more than two full years, a record amount of time. This fostered many recession calls as historically this has been a harbinger of a future recession. However, a key question was whether the disinversion would be a bull (falling 2yr yields) or bear (rising 10yr yields) steepener. Things started as a bull steepener with the Fed cutting rates, but lately, as we watch 10yr yields rise, fears are growing that inflation is making a comeback and the bond bears are going to drive this process. A bear steepening is not going to be a welcome result for Powell and friends, nor especially for Ms Yellen, as the cost of debt will continue to rise. It also speaks to concerns that the Fed has lost control of the narrative. It is still too early to declare the outcome, but the original, widely held view of a bull steepener is fraying at the seams.

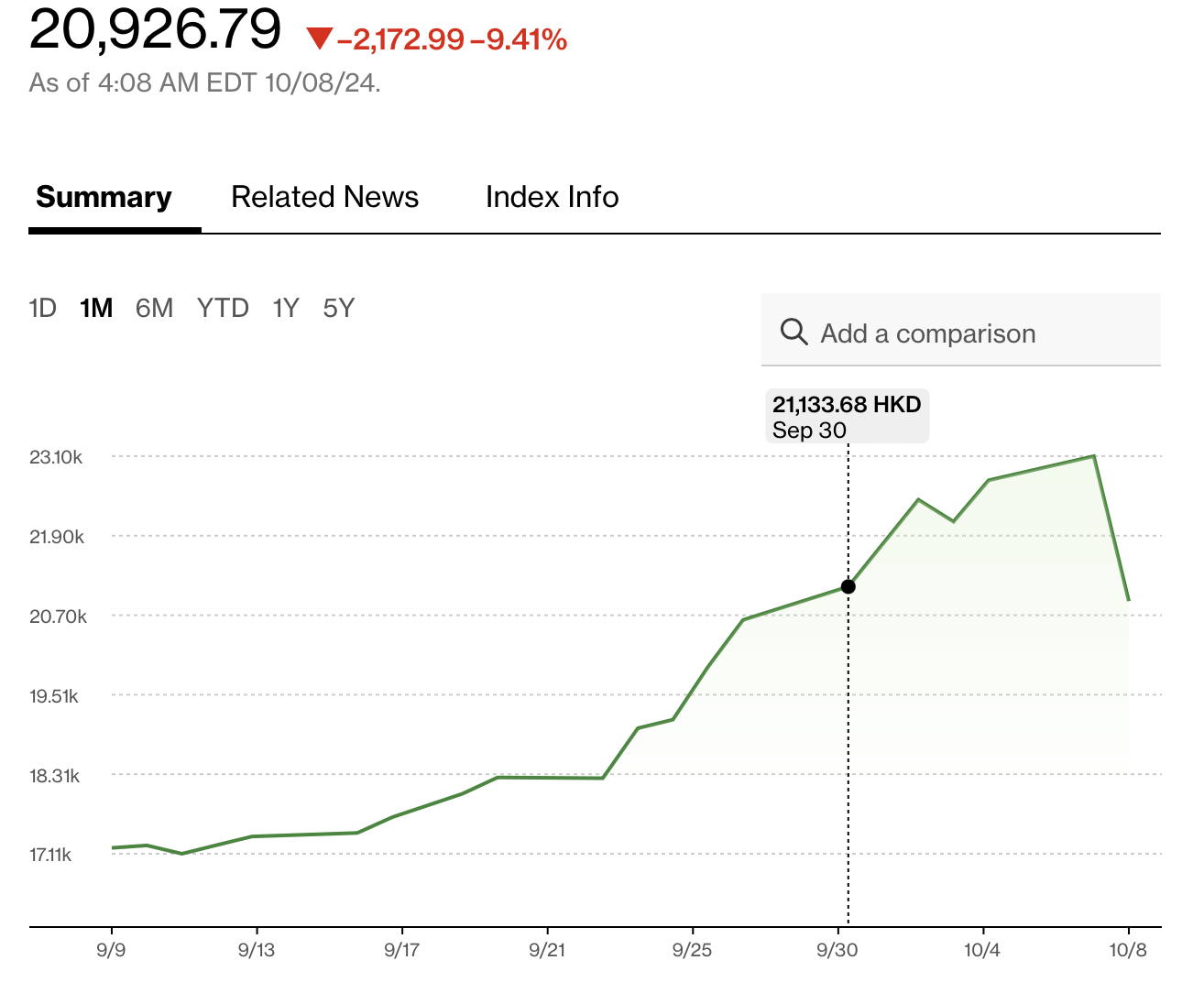

Ok, let’s quickly touch on overnight markets. Yesterday’s US rally saw follow through in Japan (+0.25%) alongside a weakening yen (-0.75% yesterday, +0.2% this morning) and in China (+1.1%) and Hong Kong (+3.0%) after the PBOC detailed the support they would be giving to equity market players and indicated that more could follow. As to the rest of the region, there were more gainers than laggards but nothing of real note. In Europe, although most markets are little changed on the day, if leaning slightly lower, Spain’s IBEX (-0.9%) is the outlier on what seems to be profit taking ahead of the US CPI number after a strong 5-day run higher. And at this hour (7:10) US futures are pointing slightly lower, about -0.2%.

In the bond market, yields continue to climb around the world with Treasuries adding 1bp and most of Europe seeing yields rise 2bps – 3bps. The largest mover there, though is the UK (+6bps) as the market there prepares for Chancellor Rachel Reeves’ first budget and implies they are not expecting fiscal prudence. In Japan, JGB yields rose 2bps and are now at 0.94% as given the turnaround in rates globally, expectations are growing for the BOJ to consider another hike. In fact, ex-BOJ member Kazuo Momma was quoted last night saying that if USDJPY goes back above 150, the BOJ is likely to move before the January meeting currently expected.

Commodity markets are taking a breather from their recent rout with oil (+1.4%) leading the energy group higher while gold (+0.4%) leads the metals complex. It has been a rough week for commodity bulls (this poet included) but nothing has changed the long-term picture in my view. This is especially true if the Fed does cut rates regardless of the stronger data.

Finally, the dollar is continuing to show strength with the DXY pushing back to 103 and the euro back down near 1.09. It seems clear the market is adjusting its views as to how much the Fed is going to cut based on the data, not the Fedspeak, and that turn, from an uber dovish Fed to one less dovish is going to support the greenback. ZAR (+0.45%) is this morning’s outlier as it follows gold prices higher, but that is the largest movement across either the G10 or EMG blocs. It seems everybody is awaiting the CPI data.

In addition to the CPI, we see the weekly Initial (exp 230K) and Continuing (1830K) Claims data and we hear from Gvoernor Lisa Cook, one of the more dovish Fed governors. But for now, it is all CPI all the time. My take is a soft number will be seen as a signal the Fed will be cutting aggressively and help stocks and commodities while undermining the dollar with a strong number doing the opposite. Bonds, though, are much trickier here as I think there are a lot of fiscal concerns being priced in, and lower inflation won’t solve that problem in the short run.

Good luck

Adf