The CPI data was hot

Or cool, all depending on what

It is that you buy

Though pundits will try

To tell you that Trump’s a tosspot

But stock markets don’t really care

Though bond markets are quite aware

Inflation’s not dead

Which means that the Fed

Relies on a wing and a prayer

These were the headlines yesterday in the wake of the CPI report:

WSJ – Inflation Picks Up to 2.7% as Tariffs Start to Seep Into Prices

NY Times – U.S. Inflation Accelerated in June as Trump’s Tariffs Pushed Up Prices

Washington Post – Inflation picked up in June as tariffs began to lift prices across the economy

And here are a couple from this morning:

WSJ – Trump Effect Starts to Show Up in Economy

Bloomberg – US Trade Wars Will Hit Households Worldwide, BOE’s Bailey Warns

As I forecast yesterday, the higher inflation would be blamed on President Trump’s actions regardless of the outcome. In fairness, that was not a hard prediction to make given the current state of the mainstream media and their general views of the president. But is that an accurate representation? As always, on matters of CPI I turn to @inflation_guy, Mike Ashton, to get his take, which has generally been the least hysterical and most cogent of analysts around. Here is his summary of yesterday’s CPI data.

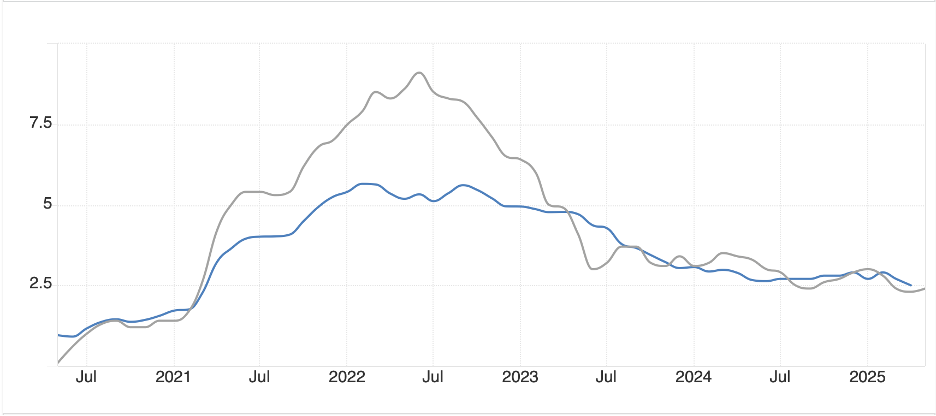

In essence, the higher Y/Y readings are partially due to base effects (the number twelve months ago that is leaving the calculation was very low so even a moderate number will result in a higher print) and partially due to ongoing price changes in the economy. Goods prices did rise, but services prices were not as affected. Notably lodging away from home (i.e. hotels) saw prices fall -2.5% on the month, likely perhaps a result of less illegal immigrants being housed in cities around the country. In the end, as Mike explains, median inflation has been running at ~3.5% annually for the past several years and shows no signs of declining much further. I fear, that is the new normal for inflation going forward.

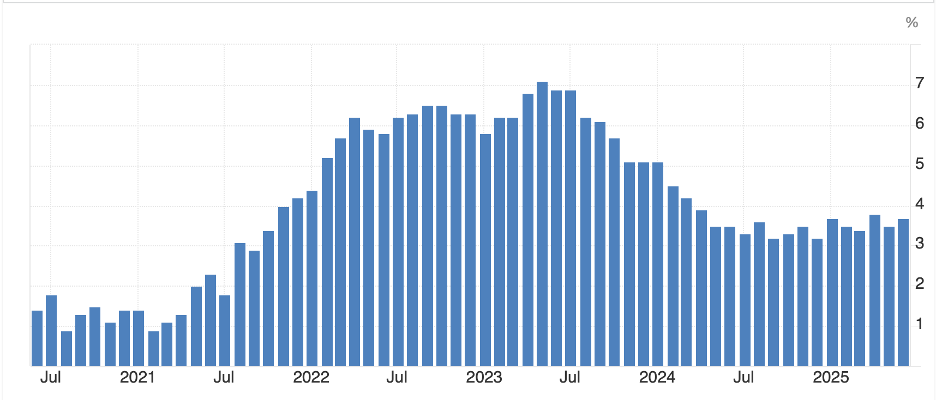

(This is a good time to mention that one way to maintain the purchasing power of your money is to own USDi, the only inflation-linked stable coin around which accretes the rise in CPI to its price on an ongoing basis. Below is a chart showing how this has performed (and by extension what has happened to inflation) since the coin was initiated on March 1st of this year. (And yes, we know exactly where the price will be going forward through the rest of the summer based on the mechanics of the way CPI is reported.)

But the US is not the only place where inflation is starting higher. Exhibit A here is the UK, which reported its CPI figures this morning where they rose to 3.6% headline and 3.7% core. Now, looking at the chart of CPI in the UK, it is abundantly clear that prices have been consistently rising for the past twelve months, at least. Interestingly, while the Starmer government has demonstrated remarkable incompetence across many factors, they have not been imposing tariffs on all their trade partners and yet inflation is still rising. Perhaps tariffs are not necessarily the inflation driver that the punditry is keen to describe. But a look at the last five years of core inflation in the UK shows pretty clearly that price rises, while having slowed from their fastest levels in the wake of the pandemic, have bottomed and appear to be accelerating again. (Arguably, that is why BOE Governor Bailey was explaining Trump was to blame for his failures.)

Source: tradingeconomics.com

In the end, though, the market adjusted to the inflation data yesterday and overnight things have been far more muted. This is true, even in the UK, where gilt yields have edged up only 2bps and the pound (+0.1%) is barely higher after having fallen more than 2% since the beginning of July. In fact, my take is that markets are just not that interested in very much these days as evidenced by the much-reduced volumes that we see across all markets.

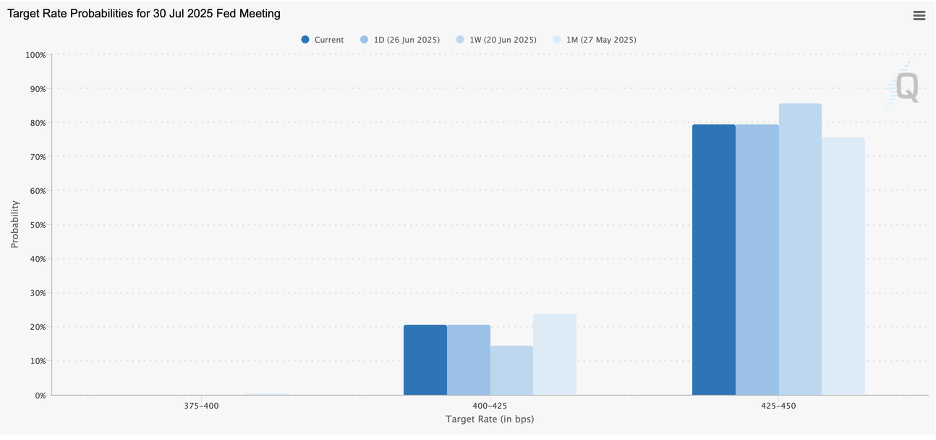

So, with that in mind, let’s see how things behaved overnight. Starting with the bond market, treasury yields have slipped -1bp this morning, but that is after having gained 6bps yesterday after the data. As well, Fed funds futures are now pricing less than a 3% probability of a rate cut at the end of this month with far less discussion about the Waller and Bowman comments regarding those cuts. Meanwhile, in Europe, away from the UK, yields have also slipped -1bp across the board, although yields there did rise about 3bps after the US CPI report. Remember, all these bond markets are tightly linked. As to Asia, JGB yields edged higher by 1bp overnight.

In the equity markets, yesterday’s broad down session in the US (Nvidia rose on China sales news which propped up the NASDAQ) was followed by modest weakness throughout most of Asia (China -0.3%, HK -0.3%, Korea -0.9%, Australia -0.8%) although Japan was essentially unchanged. European shares, though, are mostly a touch firmer led by the IBEX (+0.5%) although the DAX (+0.3%) and FTSE 100 (+0.2%) are also in the green despite there being no obvious catalysts here. US futures are essentially unchanged at this hour (7:10).

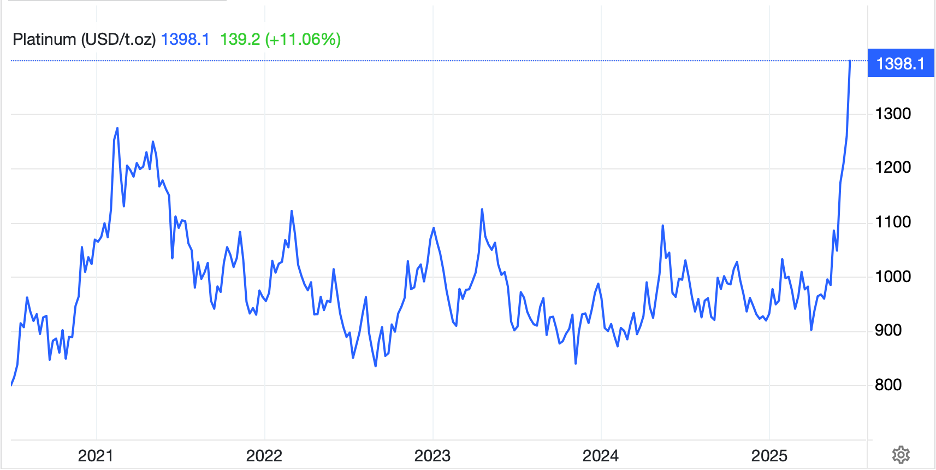

In the commodity space, oil (-0.9%) has been dragging lower over the past several sessions and is now down -3.5% in the past week. This is a reversal of the recent price action and accords far better with the fundamentals of supply coming on from OPEC with the still strong belief that economic activity is set to slow given the Trumpian tariff impact around the world. Metals markets continue to range trade as well, with gold (+0.3%) higher this morning, although it gave back yesterday morning’s gains and based on the way it has been trading, seems likely to do that again today. In fact, the entire metals complex has been showing similar behavior, gains overnight that retrace in the US.

Finally, the dollar is little changed this morning although it has been trending ever so slightly higher over the past several weeks. I haven’t discussed yen in a while, but all thoughts of the end of the carry trade have been banished as the yen has declined by more than 3% since the beginning of the month and is now back to levels last seen in April. On the day, as I look across the screen, NOK (-0.5%) is the largest mover in either G10 or EMG space, arguably responding to the fact that oil has been sliding over the past week. But here, as in the other markets, there is no excitement.

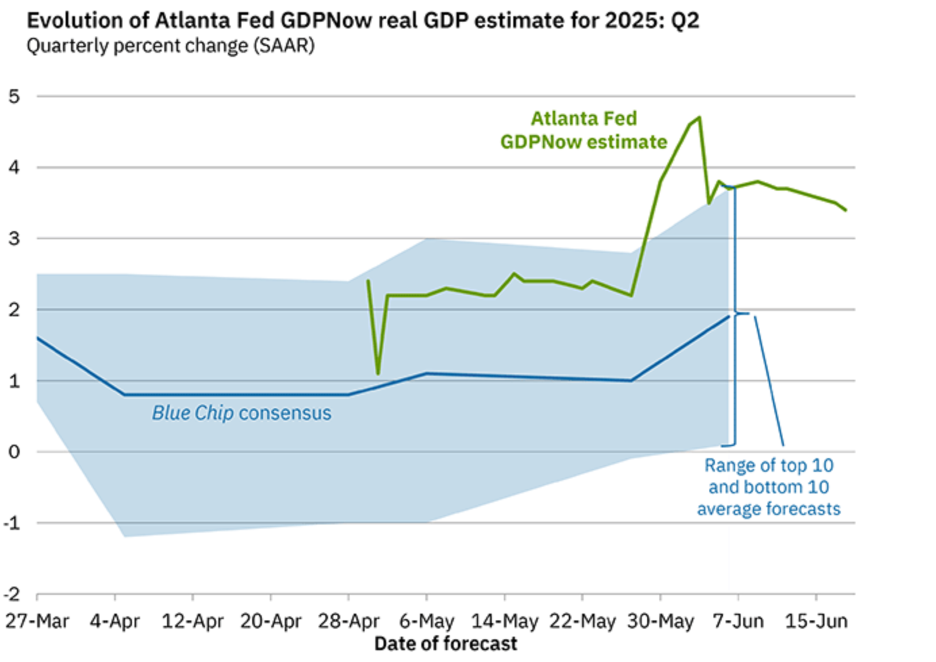

On the data front, this morning brings PPI (exp 0.2%,2.5% headline, 0.2%, 2.7% core) as well as IP (0.1%), Capacity Utilization (77.4%) and then the Fed’s Beige Book this afternoon. We also hear from three more Fed speakers today although yesterday’s group gave no indication that a move was in the offing. Instead, the only speaker with a differing opinion than the group, Waller, talked about stablecoins, not monetary policy.

I sincerely doubt that anything of note will happen today from either the data or market internals as pretty much the only thing that moves markets these days are White House announcements. And I have no idea if any of those are coming. Look for another quiet session overall.

Good luck

Adf