Said Jay, ‘twas a FAIT accompli

As all of his minions agree

The average was flawed

And now our new god

Is maximum jobs, don’t you see

But really, what pundits all heard

Was rate cuts would not be deferred

Instead, twenty-five

Next month is alive

And fifty would not be absurd

Although Chairman Powell clearly wanted to focus on the new Monetary Policy Framework, as it has evolved, market practitioners really don’t care much about that. All they care about is what is going to happen to interest rates. So, here is the paragraph from Powell’s speech on Friday that got pulses quickening and led to another set of new all-time highs in equity markets [emphasis added]:

“Putting the pieces together, what are the implications for monetary policy? In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate. Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

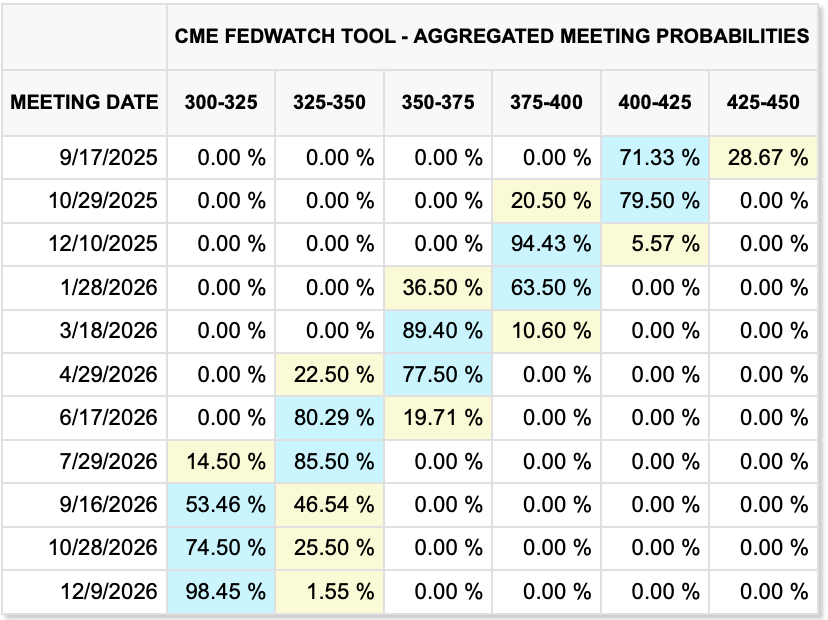

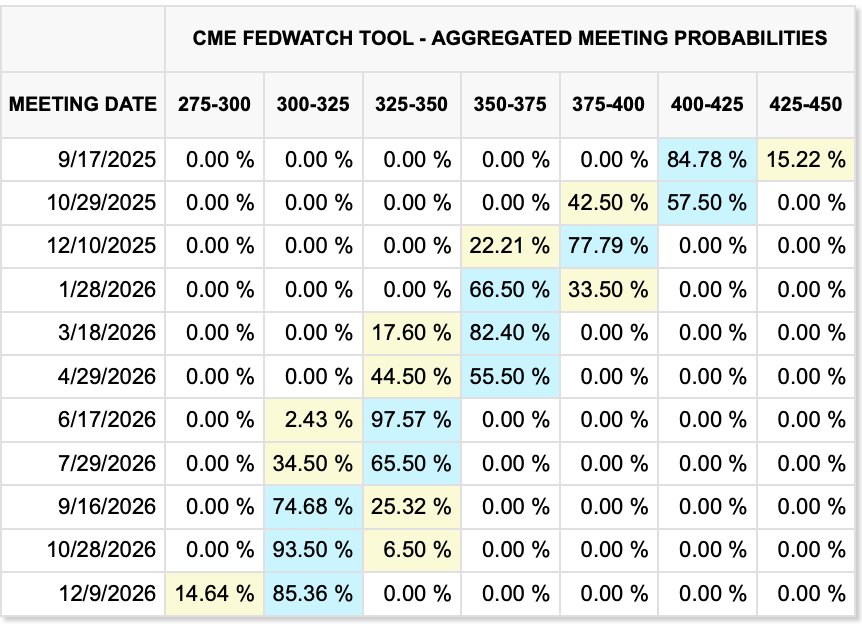

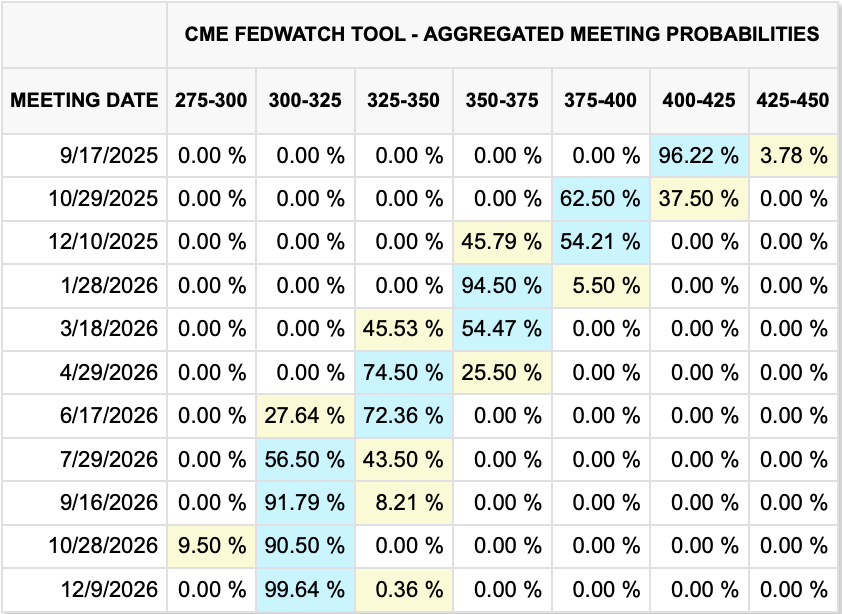

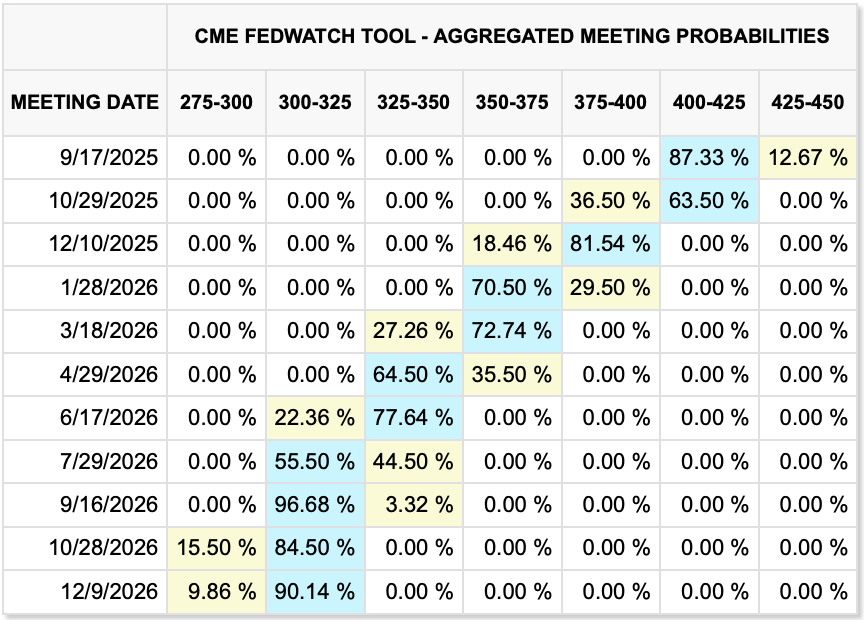

The market was quick to reprice the probability of that cut as well, with the current view up to an 87% probability, compared to 71% prior to Powell’s speech.

Source: cmegroup.com

While I personally believe a cut is unnecessary, it does feel like he just promised one.

However, for the economists out there, those who feel above such mundane issues as the price of some stock, they were far more concerned about the Policy Framework. It was the last review of this framework, back in 2019 which was released in early 2020 (pre-Covid) that Powell and friends harped on their concern over the Effective Lower Bound (ELB) aka zero interest rates. Their fear was that with the then current rate structure so low, if a recession came about, they wouldn’t have the tools to address it. So, in their definitively finite wisdom, they came up with Flexible Average Inflation Targeting (FAIT) which was designed to allow them to keep policy accommodative even if inflation was somewhat above their 2.0% goal, instead relying on the average inflation rate over time. Of course, they didn’t describe what time constituted the period of averaging, but everyone understood that the idea was to run the economy hot. Oops! It turns out that wasn’t a really good idea once Covid hit, and the federal government responded by shutting down production while pumping some $5 trillion extra into the economy. We are all still feeling the sting from that particular mistake.

Here is the pertinent commentary regarding the changes in the policy framework with shortfalls referreing to the shortfall of employment vs. full employment:

“We still have that view, but our use of the term “shortfalls” was not always interpreted as intended, raising communications challenges. In particular, the use of “shortfalls” was not intended as a commitment to permanently forswear preemption or to ignore labor market tightness. Accordingly, we removed “shortfalls” from our statement. Instead, the revised document now states more precisely that ‘the Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability.’ Of course, preemptive action would likely be warranted if tightness in the labor market or other factors pose risks to price stability.”

In the end, I would argue all they have done is rejigger the wording of how they excuse running things hot and allowing inflation to rise. Hence, the nearly promised rate cut and the new framework that says unemployment is the key.

Enough about Friday. Overnight, the key story came from China, where the city of Shanghai eased policy restrictions on home ownership to help restart that moribund market by allowing more people to buy as many homes as they would like. (It seems odd to me that after at least three years of a property problem, there would still be restrictions on home purchases, but then I never professed to understand Chinese policies.). At any rate, the very fact that there was more action on one of the key problems in the economy was a distinct positive and helped drive Chinese equity markets much higher (CSI 300 + 2.1%, Hang Seng +1.9%) with that news, along with the perception that the Fed is going to ease next month pulling the entire region higher. While Japanese shares (+0.4%) had a modest rally, Korea (+1.3%) and Taiwan (+2.2%) went gangbusters and literally every major bourse there was higher in the session.

In Europe, though, things are less bright with all the main bourses on the continent lower (DAX -0.25%, CAC -0.6%, IBEX -0.6%) although the FTSE 100 (+0.1%) is bucking the trend. It appears there are concerns over the details of the ostensibly agreed trade deal with the US as well as concerns that the Russia-Ukraine peace negotiations are not progressing as well as hoped. As to US futures, at this hour (6:50), they are taking a breather from Friday’s rally and currently point lower by about -0.25% across the board.

In the bond market, Treasury yields have recouped 2bps of the -3bps they fell in the wake of Chairman Powell’s speech on Friday. However, they remain below 4.30% and continue to trade in a narrow range as per the below chart. FYI, the mean over this period is 4.33%.

Source: tradingeconomics.com

European sovereign yields have been rising this morning, with the entire continent seeing yields higher by between 4bps and 5bps amid concerns that the mooted Fed rate cuts will not see any appreciable impact on European yields as those nations struggle with financing their promised €1 trillion of defense and infrastructure spending amid a stagnant economy.

In the commodity markets, oil (+0.6%) is continuing its slow rebound from the lows seen early last week but at $64/bbl, remain well within their trading range. There were several Ukrainian attacks on Russian refineries overnight, which arguably helped the bulls’ case, but my take remains that the trend here is lower over time. Since shortly after the start of the Ukraine war, prices have been trending lower steadily.

Source: tradingeconomics.com

In the metals markets, Friday’s Powell speech goosed all of them higher and this morning, like equity indices, they are backing off a bit with gold (-0.2%) and sliver (-0.45%) still trading near their recent levels. We will need some outside catalyst, I think, to shake these markets up.

Finally, the dollar is a bit firmer this morning, also reversing some of Friday’s post-Powell decline, with both the euro and pound lower by -0.2% while the yen (-0.35%) is a touch softer than that. The biggest movers have been ZAR (-0.7%) responding to the weakness in precious metals and CZK (-0.8%) and HUF (-0.9%), both of which appear to be reflexive sales after strong moves Friday. If the Fed is really going to pay less attention to inflation, I see that as a distinct negative for the dollar. That has been my concern all year, although the offsetting feature was the promise of massive inward investment flows. But the short-term view is more focused on Fed policy, so beware more confirmation by Fed speakers that they are willing to cut.

On the data front this week, probably the most impactful number is NVidia earnings Tuesday after the close, but from an economic perspective, this is what we have coming,

| Today | Chicago Fed Nat’l Activity | -0.2 |

| New Home Sales | 630K | |

| Tuesday | Durable Goods | -4.0% |

| -ex Trasnport | 0.2% | |

| Case Shiller Home Prices | 2.2% | |

| Consumer Confidence | 96.4 | |

| Thursday | Initial Claims | 230K |

| Continuing Claims | 1975K | |

| Q2 GDP | 3.1% | |

| Q2 GDP Sales | 6.3% | |

| Q2 Real Spending | 1.4% | |

| Friday | Personal Income | 0.4% |

| Personal Spending | 0.5% | |

| PCE | 0.2% (2.6% Y/Y) | |

| Core PCE | 0.3% (2.9% Y/Y) | |

| Chicago PMI | 45.5 | |

| Michigan Sentiment | 58.6 |

Source: tradingeconomics.com

In addition to this, we only hear from Richmond Fed President Barkin (twice) and Governor Waller. We already know Waller wants to cut, so Barkin is the one who can give us new info.

And that’s what we have for today. The ongoing ructions from Powell’s speech and the question of how investors will interpret the probability of a rate cut. As I said, if they really are going to put inflation second, then the dollar will suffer.

Good luck

Adf