Investors don’t know where to hide

As Trump lands another broadside

Last night he did roil

All those who buy oil

From Vene, with tariffs applied

But yesterday, too, he amended

How tariffs would soon be extended

The lesson to learn

Is you’ll ne’er discern

His methods, so don’t be offended

Once again, the tariff game changed yesterday, although this time in two directions. The first, and newest idea is that the US will impose “secondary” tariffs on all nations that buy oil from Venezuela. The idea is to pressure Venezuela to concede to US demands by reducing the market for their one exportable commodity, at least the only one in demand (Tren de Aragua gang members, while a key export, have limited demand it seems). This decision is being described as a new tool of statecraft, but it strikes me this is no different than previous international efforts like the apartheid movement, by isolating a nation for its behaviors. Regardless, this was seen as bullish for oil prices. The reason, as eloquently explained by Ole Hanson, Saxo Bank’s Head of Commodity Strategy, as per the below, is that Venezuelan and Iranian oil production has risen significantly over the past 4 years, offsetting the production cuts of the rest of OPEC+. Take that oil out, and the demand/supply balance tips toward more demand.

It remains to be seen how this impacts specific countries, but apparently, China is the largest importer of sanctioned crude, so obviously, not a positive for President Xi. Alas for Chevron, the deal they cut with the Biden administration to restart activity in Venezuela is looking shakier by the day.

But that is only one of the tariff stories. The other was that there may be changes to previously expected actions come April 2nd, with imposition of tariffs being a bit more gradual nor as widespread as initially feared. Recall, the idea of the reciprocal tariffs was almost every other nation charges higher tariffs on US goods than the US charges on their goods, so simply raising US tariffs to their levels would be effective. The next step was focusing on the so-called “Dirty 15” nations that run the major trade surpluses with the US, but now he has indicated that some nations will get breaks. I particularly loved this comment, “I may give a lot of countries breaks. They’ve charged us so much that I’m embarrassed to charge them what they’ve charged us, but it’ll be substantial, and you’ll be hearing about that on April 2.”

In any event, Trump’s specialty is his ability to think outside the box, or perhaps more accurately, break the box and move to a different container. There is much consternation amongst business managers, and understandably, since planning is much more difficult in this environment. However, as I have repeatedly written, the one thing on which we can count is continued higher volatility across all markets. That condition requires a robust hedging plan for all those who have exposures, that is your only realistic protection.

Other than the tariff story, though, we have not seen much new information so let’s take a look at how markets have handled the latest tariff saga. Yesterday’s broad US equity rally, on the back of a reduced tariff outlook, was followed by less positive price action in Asia. While the Nikkei (+0.5%) rallied, potentially on the yen’s recent weakness, Hong Kong (-2.4%) was under great pressure on a weaker tech sector as earnings there were disappointing last quarter. However, the CSI 300 (0.0%) which has far less tech in its makeup, didn’t budge. As to the rest of the region, there were more gainers (Taiwan, Malaysia, New Zealand, Indonesia) than losers (Korea, Philippines, Thailand), so arguably the US rally and tariff story helped a bit.

In Europe, though, things are looking solid this morning with green everywhere on the screen and generally substantially so. The DAX (+0.9%), CAC (+1.2%) and IBEX (+1.1%) are all having solid sessions after German Ifo Expectations data was released a touch better than expected at 87.7, but as importantly, 2 points better than last month. However, a look at the history of this index shows that while recent data has turned mildly positive, compared to its long-term history, things in Germany remain in lousy shape.

Source: tradingeconomics.com

As to US futures, at this hour (7:10), they are little changed on the day as traders await the next pronouncements with great uncertainty.

In the bond market, though, yields have been climbing everywhere with Treasury yields higher by 2bps this morning after jumping 5bps yesterday. In fact, we are back at the highest levels in a month, although still well below the peaks seen in early January or last spring. But this move has dragged European sovereign yields along for the ride with across-the-board gains of 4bps-5bps and similar movement in JGBs overnight. One of the alleged reasons for this bond weakness were hawkish comments from two ECB members, Slovakia’s Kazimir and Estonia’s Müller. However, dovish comments from Greece’s Stournaras and Italy’s Cipollone would have seemed to offset that, and did so in the FX markets, but not in the bond market.

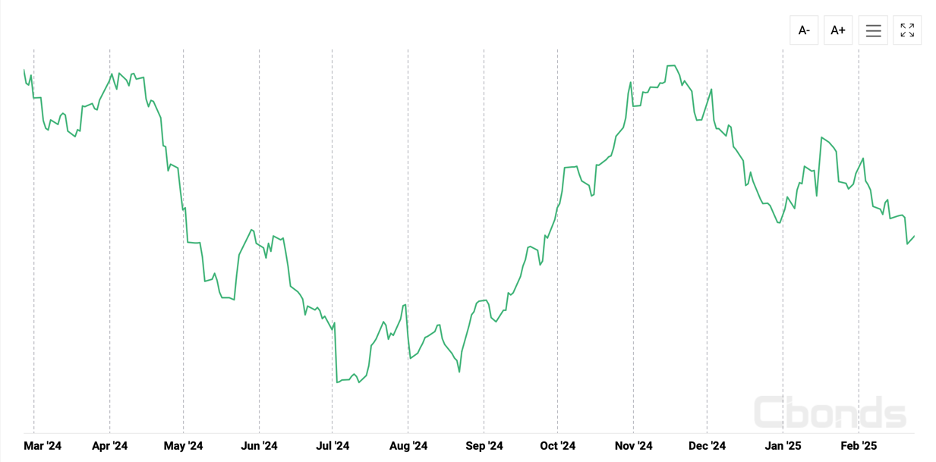

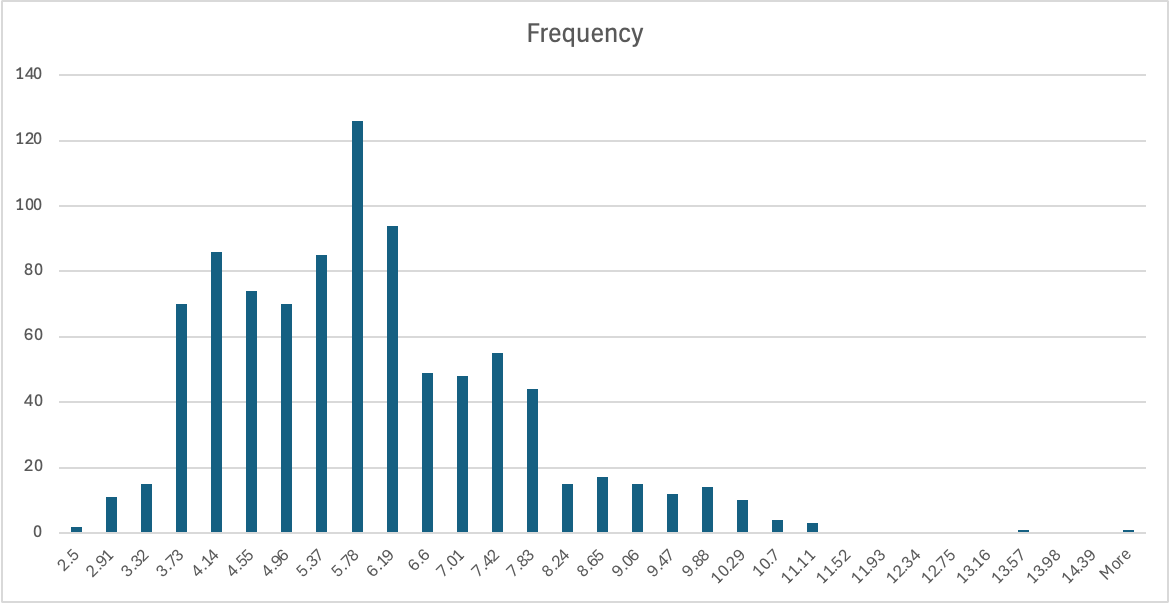

Turning to commodities, oil (+0.4%) continues to climb and is once again approaching $70/bbl. In fact, since that fateful day, March 11th, it has rallied consistently as can be seen below. I still don’t understand why that date seemed to offer a change of view, but there you go.

Source: tradingeconomics.com

In the metals markets, this morning is once again seeing a bullish tone with both precious and industrial metals in demand. Gold (+0.5%) continues to be one of the best performing assets around, although so far this year silver (+1.5%) and copper (+1.15%) have been amongst the few things to beat it. I believe this trend has legs.

Finally, the dollar is softer this morning, falling against both its G10 and EMG counterparts almost universally. SEK (+0.9%) is the leader in the clubhouse, although we have seen solid gains from AUD (+0.5%) and NZD (+0.6%) with both the euro (+0.2%) and pound (+0.2%) lagging the pace but in the same direction. JPY (+0.4%) which has suffered a bit lately, is following the broad dollar move this morning. in the EMG bloc, the CE4 (+0.4% across all of them) is setting the tone with ZAR (+0.4%) right there. Otherwise, the movement has been a bit more modest (MXN +0.2%, KRW +0.15%), but still putting pressure on the dollar.

Turning to the data, as I never got to show the week ahead, here we go:

| Today | Case-Shiller Home Prices | 4.8% |

| Consumer Confidence | 94 | |

| New Home Sales | 680K | |

| Wednesday | Durable Goods | -1.0% |

| -ex Transport | 0.2% | |

| Thursday | Initial Claims | 225K |

| Continuing Claims | 1890K | |

| GDP Q4 Final | 2.3% | |

| GDP Final Sales Q4 | 3.2% | |

| Goods Trade Balance | -$134.6B | |

| Friday | Personal Income | 0.4% |

| Personal Spending | 0.5% | |

| PCE | 0.3% (2.5% Y/Y) | |

| Core PCE | 0.3% (2.7% Y/Y) | |

| Michigan Sentiment | 57.9 |

Source: tradingeconomics.com

Obviously, the PCE data Friday will be the most interesting piece of data released, although we cannot ignore Case-Shiller today. I keep looking at prices rising there at nearly 5% and wondering why economists expect inflation to fall. If home prices are rising 5% per year, and they represent one-third of the CPI, it doesn’t leave much room for other prices to rise to achieve 2.0%. Just sayin’. In addition, we hear from seven different Fed speakers this week. Now, I have been making a big deal about how Fedspeak doesn’t seem to matter as much anymore. Perhaps this week, given the overall uncertainty across markets, it will matter. However, the Fed funds futures market continues to price a bit more than two rate cuts for the rest of the year, which has not changed very much at all in the past month. I still don’t think the Fed speakers matter right now.

Markets are highly attuned to whatever Trump says about tariffs. Absent a new war, and maybe even if one starts, I suspect traders (or algos) will focus on that exclusively. But despite all this, nothing has altered my longer-term view that the dollar will weaken, and commodities remain strong going forward.

Good luck

Adf