At this point, I think we’d agree

It’s oil that seems to be key

As it keeps on rising

It’s not that surprising

That markets elsewhere lack much glee

So, how might the narrative shift?

One way is a noteworthy rift

Twixt Trump and our friends

Who seek different ends

And might, sometime soon, become miffed

The war continues to be the only story that matters to markets right now, although this morning we will be seeing the payroll report. And no matter the information we receive from ordinary news sources, all of which have their own biases, the one thing that rings true is market prices. People can say whatever they like, but when it comes to money, the truth will out.

With that in mind, a look at the oil market this morning is not very optimistic as the black, sticky stuff is sharply higher once again, up by 5.25% as I type at 6:45. I have highlighted this week that thus far, the rise had not been excessive, but as we look at the chart this morning, that claim may no longer be correct. While we remain far below the levels seen shortly after Russia invaded Ukraine in 2022, the price has risen 25% this week.

Source: tradingeconomics.com

As others have highlighted, while the price of crude gets all the market press, for the man on the street, it is really the price of gasoline that matters, and that has risen some 17% this week. Arguably, markets are beginning to price the idea that this war will continue longer than initial thoughts, and that the key chokepoint, the Strait of Hormuz, will remain closed for longer than initially expected. I have seen several models that indicate the impact on measured inflation if gasoline continues to rise in price, which indicate that we should expect CPI to be jumping in the next few months. The upshot there is that do not be surprised if inflation is suddenly running above the Fed funds rate by the summer, a forecast that I don’t believe was on any bingo card at the beginning of the year.

Remember, though, the narrative prior to the onset of this military action that there was an oil glut. Remember, too, there is a significant amount of oil in storage around the world, and as I continue to say, the Western Hemisphere is pumping as fast as they can. (As an aside, I saw this morning that the US is going to restart diplomatic relations with Venezuela, an indication that things there are working far better than the critics implied.) Clearly, fear is rampant in the oil markets right now, but that is subject to change in a heartbeat.

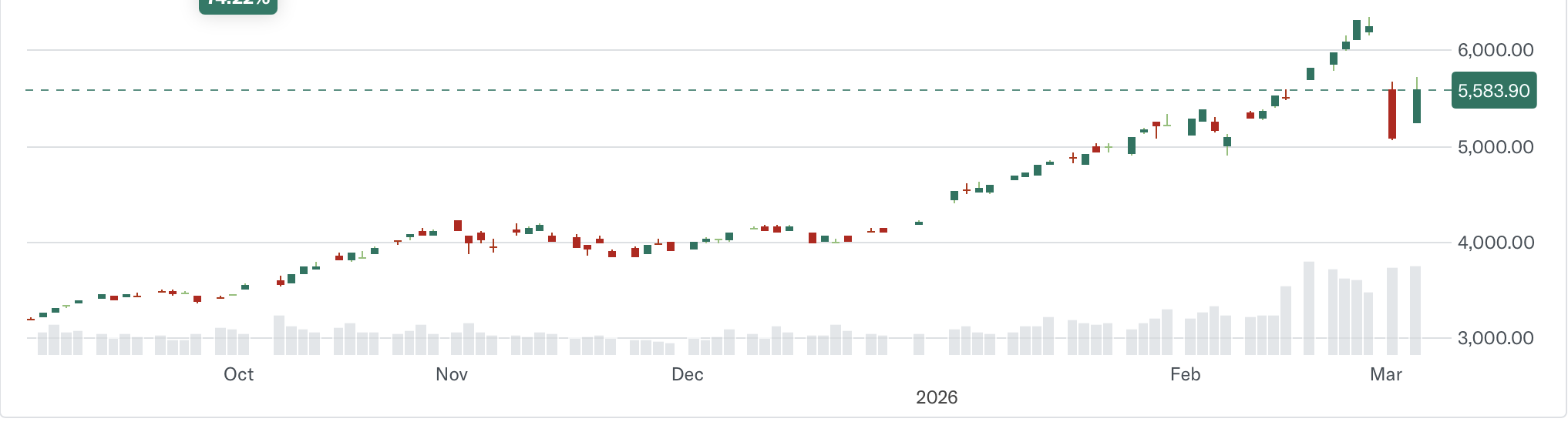

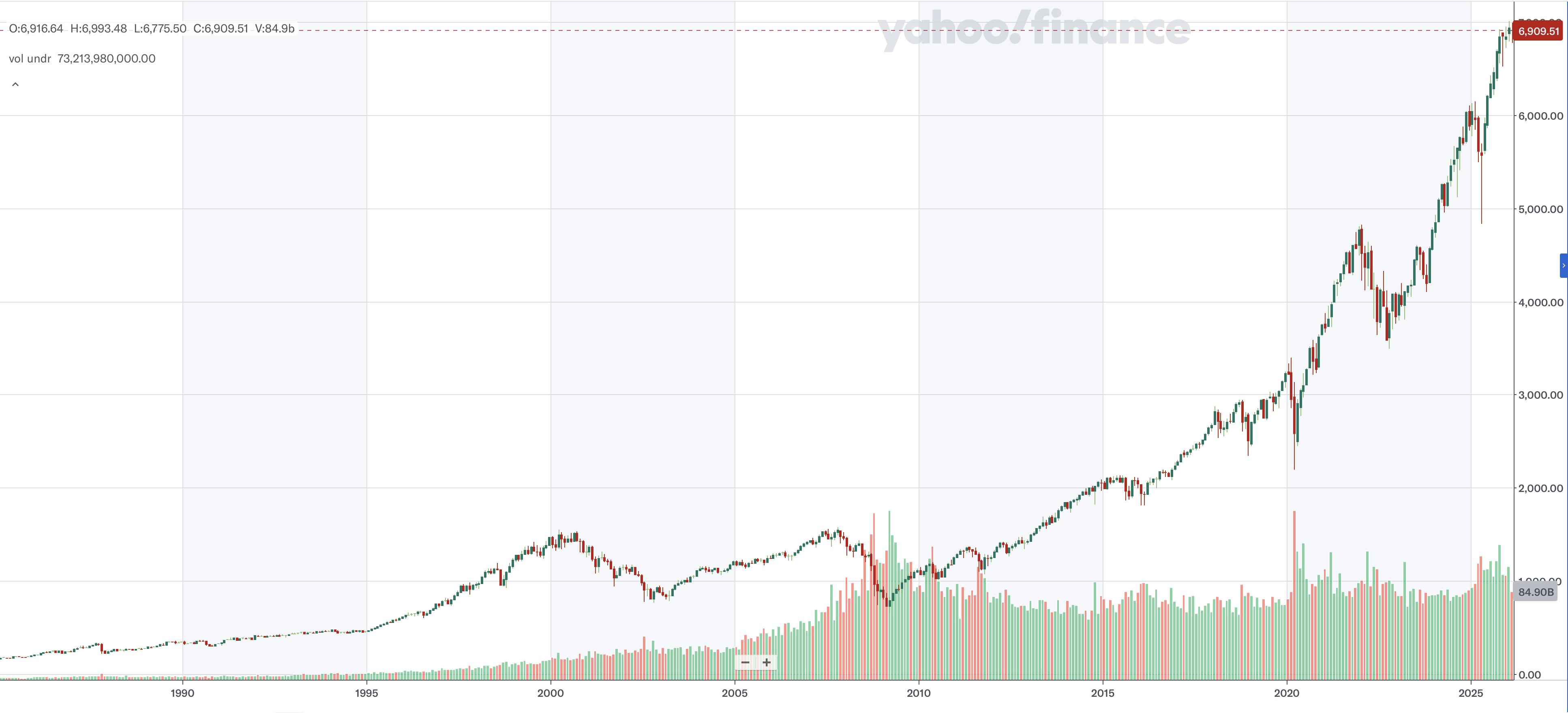

In the meantime, let’s see how markets have responded to the latest rise in oil prices. Stocks cannot make up their mind, it seems, as the below chart of the S&P 500 shows the price action over the past week, since this started.

Source: tradingeconomics.com

I am hard pressed to discern a trend here, with the movement more akin to a sine wave than anything else. Interestingly, yesterday’s weakness in the US was followed by a mix of strength and weakness in Asia with Tokyo (+0.6%), China (+0.3%) and HK (+1.7%) all gaining although there were declines in India (-1.4%), Australia (-1.0%) and Indonesia (-1.6%). Not surprisingly, each nation in Asia is impacted by the war differently, although higher oil prices would seem to me to be quite a negative for the big 3 markets given how reliant each one is on imported oil, and how much of it transits the Strait of Hormuz.

As to Europe, this morning is all red, with losses between -0.1% (UK) and -0.5% (Spain) and everywhere in between. I read a charming article in Bloomberg about how recent unseasonably mild and sunny weather in Germany has resulted in solar power generating more than 40GW of electricity for the 5th consecutive day this week, helping to keep prices in check despite the rise in energy prices elsewhere. I hope, for the Germans’ sake, the weather stays more like Phoenix than Frankfurt going forward. But reality is going to be a problem for them going forward, and high energy prices not only hurt consumers, but they are destroying what’s left of Europe’s industry. As to US futures, at this hour (7:15) they are lower by -0.6% across the board.

Bonds continue to shun their safe haven role in this conflict with yields continuing to climb. Treasuries are higher by a further 3bps this morning and approaching the 4.20% level that had been the top of the trading range. European sovereign yields are all higher by between 3bps and 6bps as inflation concerns percolate amid higher energy prices. Alas for Europe, this morning they released Eurozone GDP growth for Q4 at a softer than expected 1.2%. I expect we will begin to hear more about stagflation there if the war continues.

In the metals markets, both gold (+0.1%) and silver (+0.1%) are marginally higher this morning although both suffered yesterday. My friend JJ who writes the Market Vibes Substack made a very prescient statement last evening, “However, when the shit is hitting the fan, you don’t want safe assets, you want safe prices.” Thus far, gold has not proven to have safe prices, as evidenced by the daily chop you see below, but my belief remains that it will continue to maintain its value over time, especially in a situation like this.

Source: tradingeconomcis.com

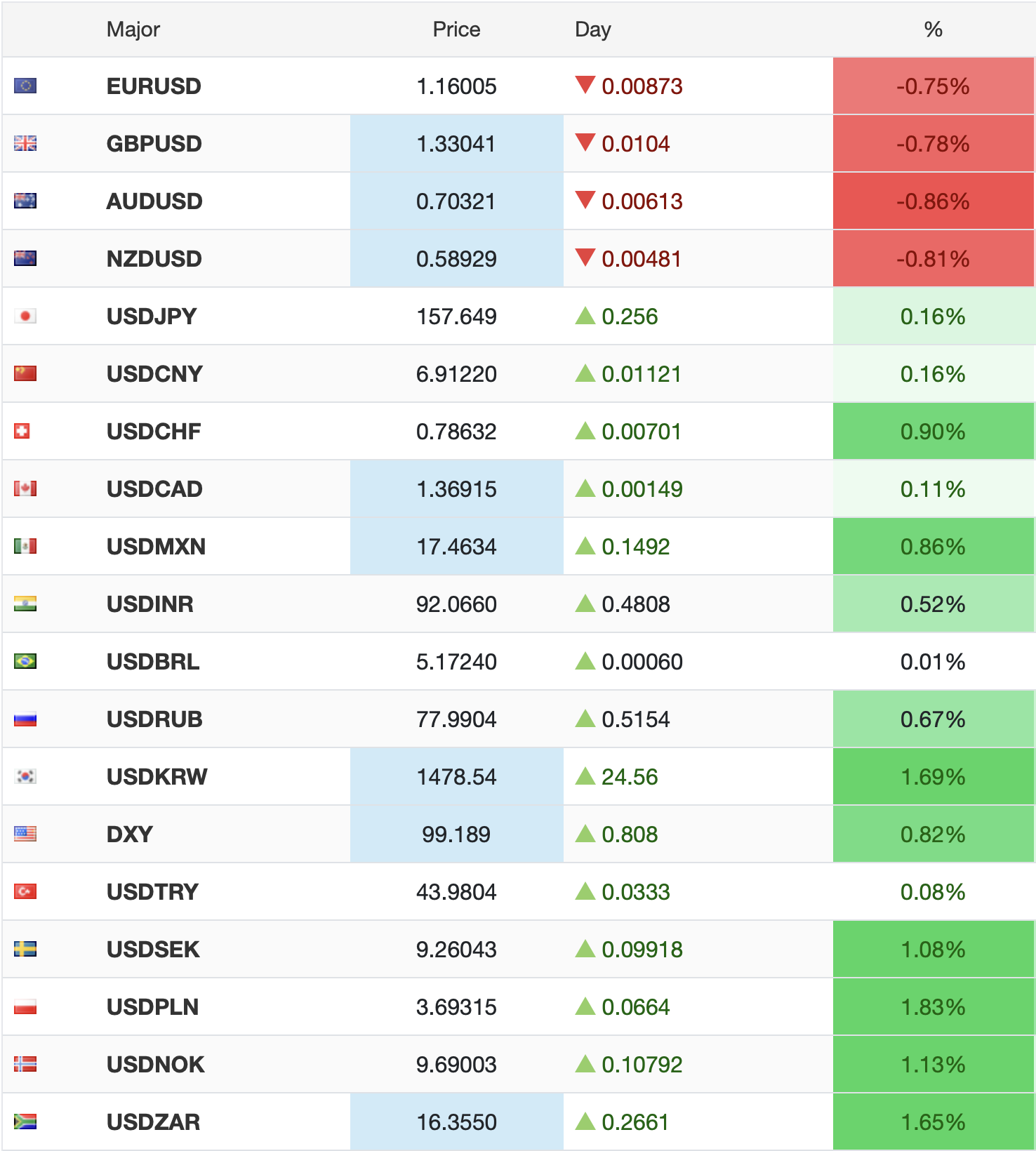

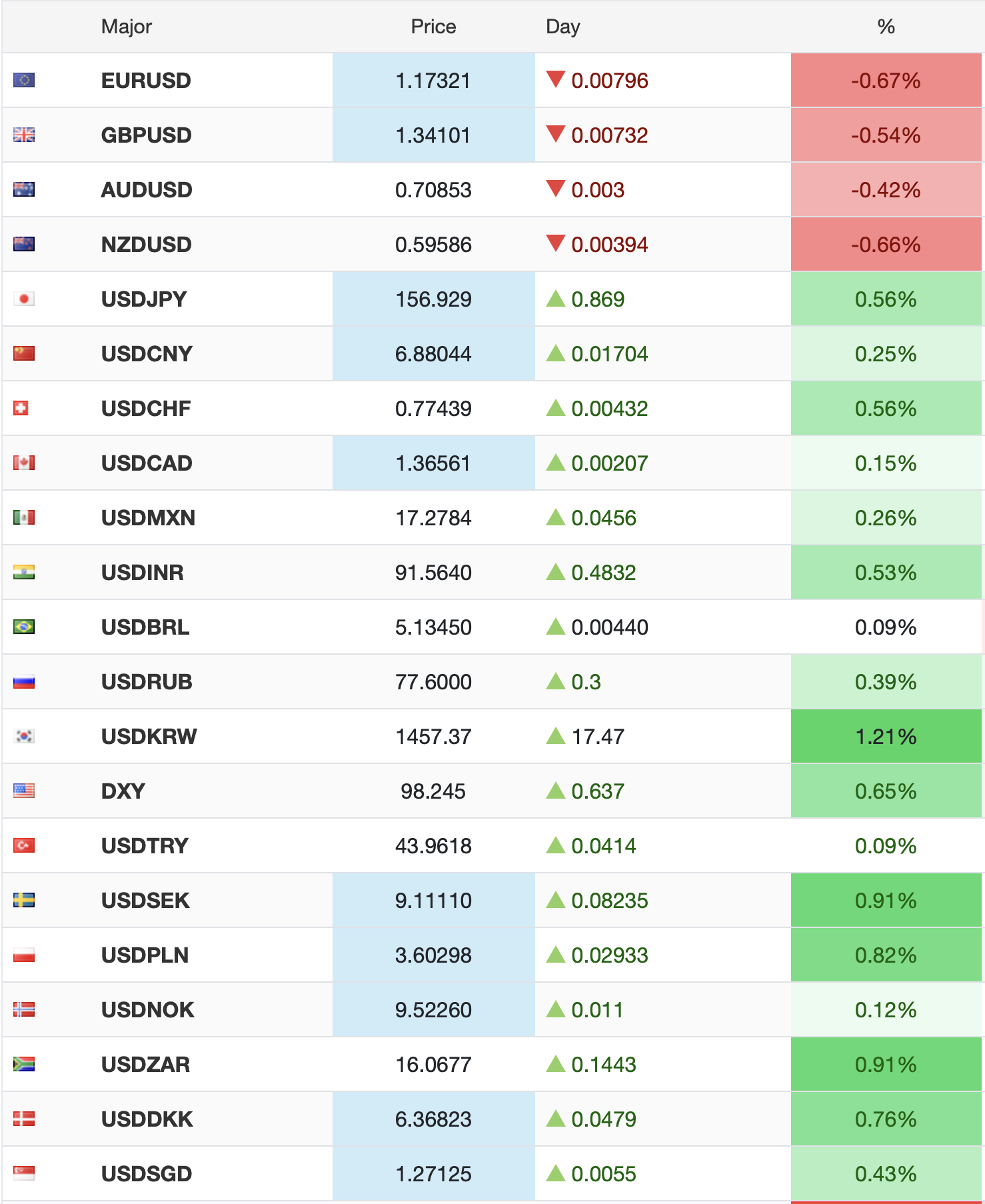

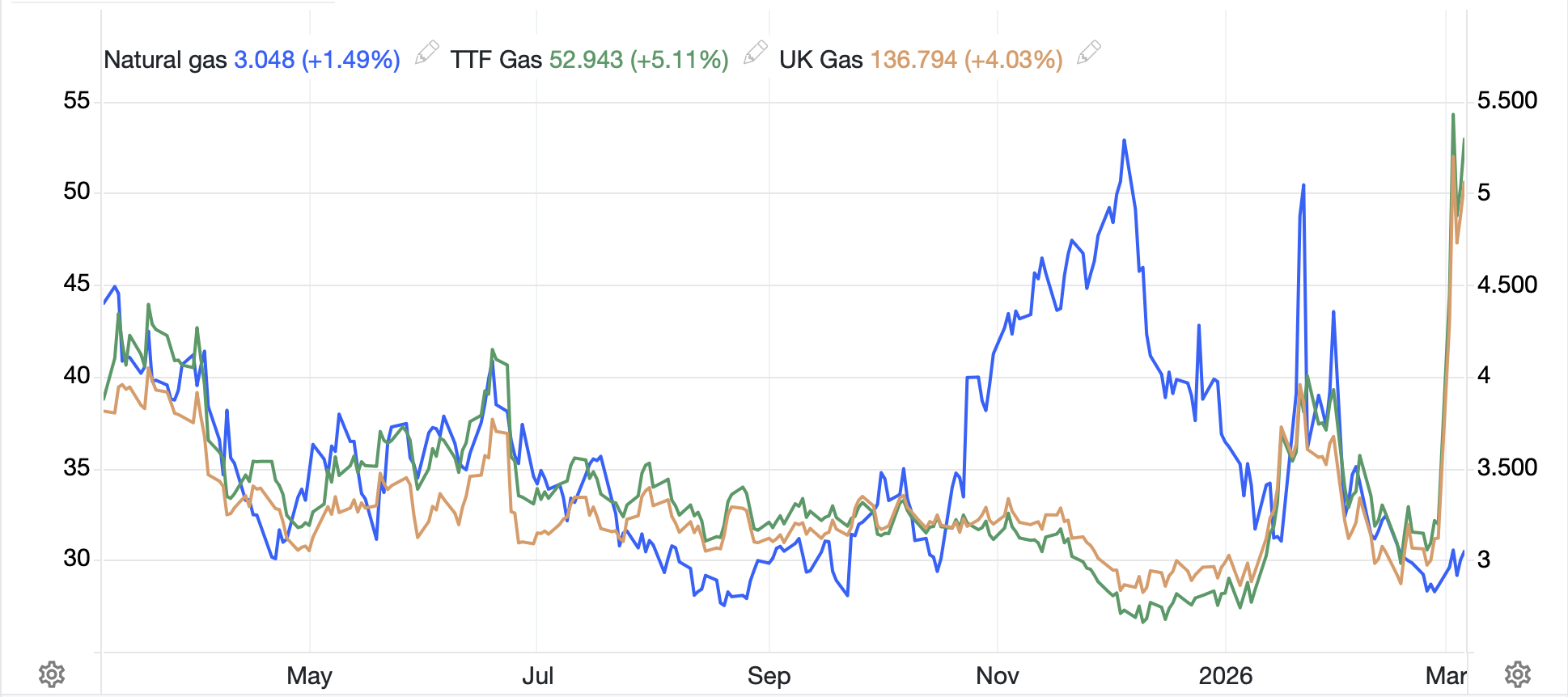

Finally, rumors of the dollar’s death continue to be exaggerated. This morning, it is stronger vs. virtually all its counterparts in both the G10 and EMG blocs, even the traditional havens of CHF (-0.2%) and JPY (-0.3%). As I have repeatedly written, I don’t believe you can look at the global energy equation without recognizing that the US combination of extraordinary resources and the willingness to exploit them is an unbeatable combination. After all, despite 25% of global LNG shipping stopped due to the closure of Hormuz, natural gas prices in the US are just over $3.00/MMBtu, certainly above their levels from two years ago, but incredibly cost competitive on a global basis. Just look at the chart below with European, UK and US gas prices and see how they have behaved.

Source: tradingeconomics.com

Back to the dollar, both the euro (-0.4%) and the pound (-0.3%) have slipped to their lowest levels vs. the dollar since late November 2025. I believe that is a combination of both fear and the energy situation as it is aggravated by the war. There are two currencies holding up this morning, NOK (+0.15%) and CAD (+0.15%) with the similarity that both are major oil exporters. Oil continues to be the story driving everything. Quite frankly, as long as the war continues, I find it hard to devise a scenario where the dollar declines in any meaningful way.

On the data front, this morning brings the payroll report with the following expectations:

| Nonfarm Payrolls | 59K |

| Private Payrolls | 65K |

| Manufacturing Payrolls | 3K |

| Unemployment Rate | 4.3% |

| Average Hourly Earnings | 0.3% (3.7% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 62.5% |

| Retail Sales | -0.3% |

| -ex Autos | 0.0% |

Source: tradingeconomics.com

Yesterday’s Initial Claims data was in line and the productivity data was better than expected. Wednesday’s ADP Employment Data was better than expected. While there continues to be a lot of discussion about the economy setting to crack, at this point the data does not show that to be the case. Remember, the tax impacts of the OBBB are starting to be felt, and that is a huge stimulus. Remember, too, last month’s NFP was much stronger than expected. A strong number will certainly support the dollar, although it will probably support oil prices as if the economy remains strong, it will encourage President Trump that he can continue in Iran for a longer time.

Good luck and good weekend

Adf