Down Under the latest decision

To raise rates was made midst division

Inflation there’s rising

So, it’s not surprising

The two sides have had a collision

But elsewhere this week I’d expect

That central banks all will reject

A hike in their rate

As long as the Strait

Stays closed, though inflation’s unchecked

For a while now, I have been making the case that central bank activities, at least in the West, had a diminishing impact on market behavior, and that was before the war in Iran began. My thesis had been based on the idea that fiscal policies had become so overwhelming that market participants realized that the odd 25 basis point rate move was not going to move the needle, at least not on a short-term horizon.

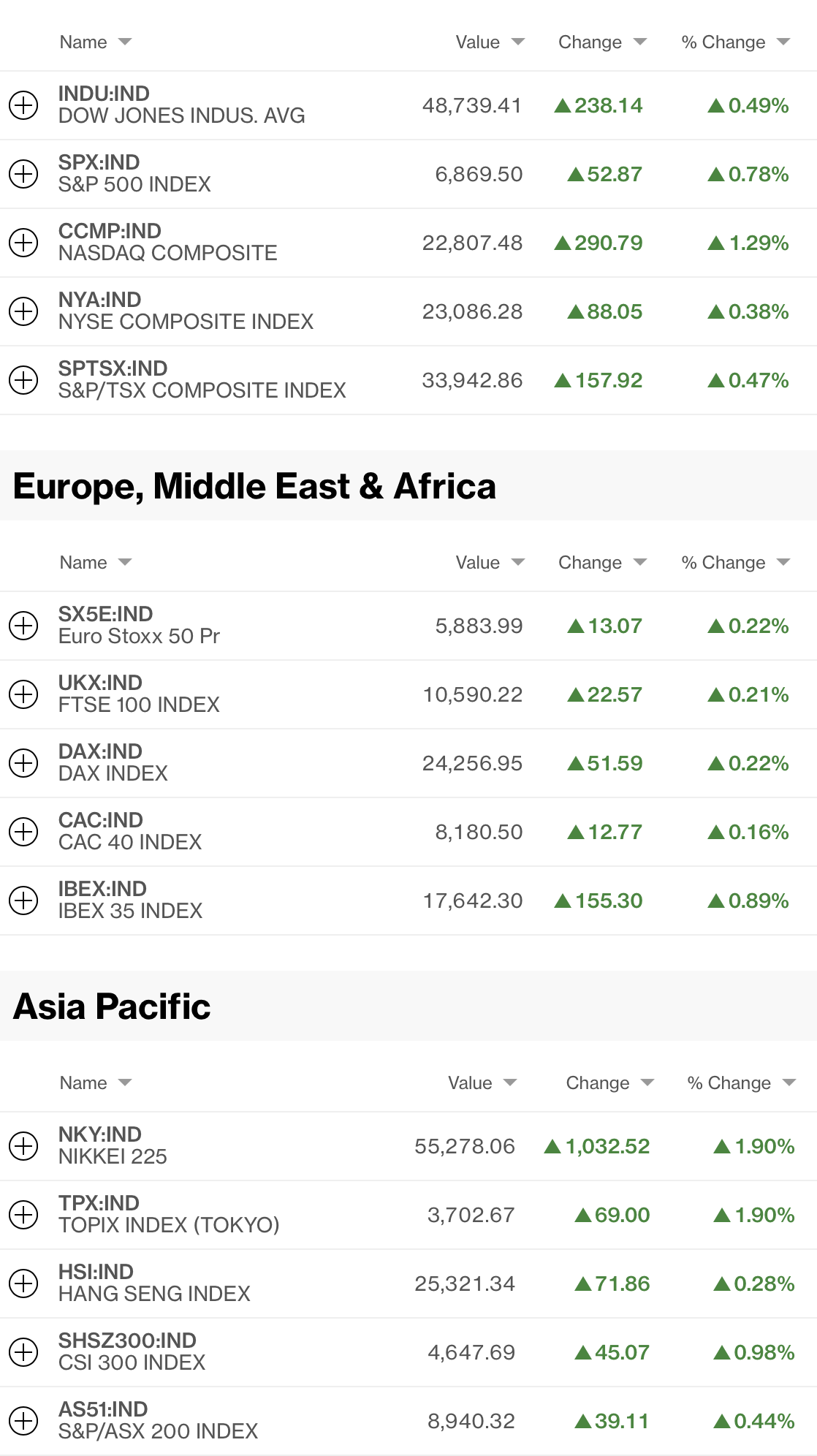

Then, of course, at the beginning of the month, the Iran conflict began which garnered all the market’s attention, rightfully so. But here we are, 17 days into the conflict and suddenly, investors seem far less concerned with the situation. Naturally, the halting of ~20% of daily oil flows through the Strait remains a critical issue, but arguably, until something there changes, the market seems to have absorbed that in its price. Consider the following screen shot of equity markets from 6:30 this morning. it is very difficult to look at this and conclude there is any sense of panic.

Source: tradingeconomics.com

Sure, equity markets have slipped over the past month, but the magnitude of that decline has been pretty modest considering oil prices have jumped 50% during that period. The lesson I take from this is that speculative positioning has been substantially reduced because, frankly, we have not seen nearly as much fear response as I would have anticipated heading into this situation. If we look at the CNN Fear & Greed Index below, sure it says we are in extreme fear (below 25 on the chart), although this is nowhere near the lows seen during the past year as per the below chart from cnn.com

But if you go to the link above, it shows a series of charts covering different facets of the stock market, and frankly, none of them demonstrate to me that fear is that rampant, despite their labels. After all, most of the charts show the current readings right in the middle of the range over the past year.

Which takes us back to, what is driving markets these days? Two and a half weeks into the war, I presume that margin calls have been settled and those positions adjusted or reduced accordingly. After all, margin clerks demand settlement immediately, not in two weeks’ time, so they are done. Economic data has been underwhelming, although we are beginning to see the first inklings of war-related weakness with yesterday’s Empire State Manufacturing disappointment (-0.2 vs 7.1 last month and 3.2 expected), but even more so with this morning’s German and European ZEW Economic Sentiment Indices.

Actual Previous Forecast

Source: tradingeconomics.com

This is the first March data we are seeing, and I suspect all of it is going to be lousy. But again, that is already priced in, I believe, hence the relative lack of movement.

And so, I turn to the central bank community, with virtually the entire G7 having meetings this week. While I don’t anticipate any rate movement other than last night’s RBA hike of 25bps, which was priced in before the conflict began, I expect that we are going to need to listen to what they all say as our best indication of current expectations of future behavior, and whether they will react to the oil price rise, or recognize higher rates will not open the Hormuz Strait. At this point, especially since there has been insufficient inflation data to alter decisions, I expect a lot of talk about carefully monitoring the situation, but no promises to do anything. And remember, knock-on effects of higher oil prices into other things take time to be felt, so given the completely reactive nature of all central banks, that is not going to be a reason to raise rates. Ironically, central banks are back in the market discussion despite themselves!

Ok, let’s tour the markets and see how things have behaved overnight. Yesterday saw a very solid US session, although as in the table above, this morning futures are very modestly lower. In Asia, Tokyo (-0.1%) slipped a bit after Katayama-san, the FinMin, explained she was watching the yen closely and would consider “bold moves” (a euphemism for intervention) if deemed necessary. Elsewhere in the region, though, only China (-0.7%) failed to follow the US with Korea (+1.6%), India (+0.75%), Taiwan (+1.5%) and Singapore (+1.2%) representative of the price action. Other markets had lesser gains, but gains they were.

Meanwhile, European bourses are all in the green as well, albeit not as robustly as Asian exchanges showed. Spain (+0.8%) is the leader, but 0.5% gains in France and the UK are also extant while Germany (+0.1%) is still trying to shake off that horrible ZEW number.

In the bond market, Treasury yields slipped again yesterday, down -3bps, and this morning, European sovereigns are showing similar activity, with yields sliding between -3bps and -5bps across the entire continent and the UK. This is certainly odd behavior if the market believes that oil prices are going to remain higher for longer. If I look at the combination of the early March data weakness and the fact that bond investors are not panicking in any sense, there is no indication that central banks are going to do anything for now, but I suspect that economic weakness will be the issue that arises going forward. After all, inflation has not seemed to be their driver for a while now.

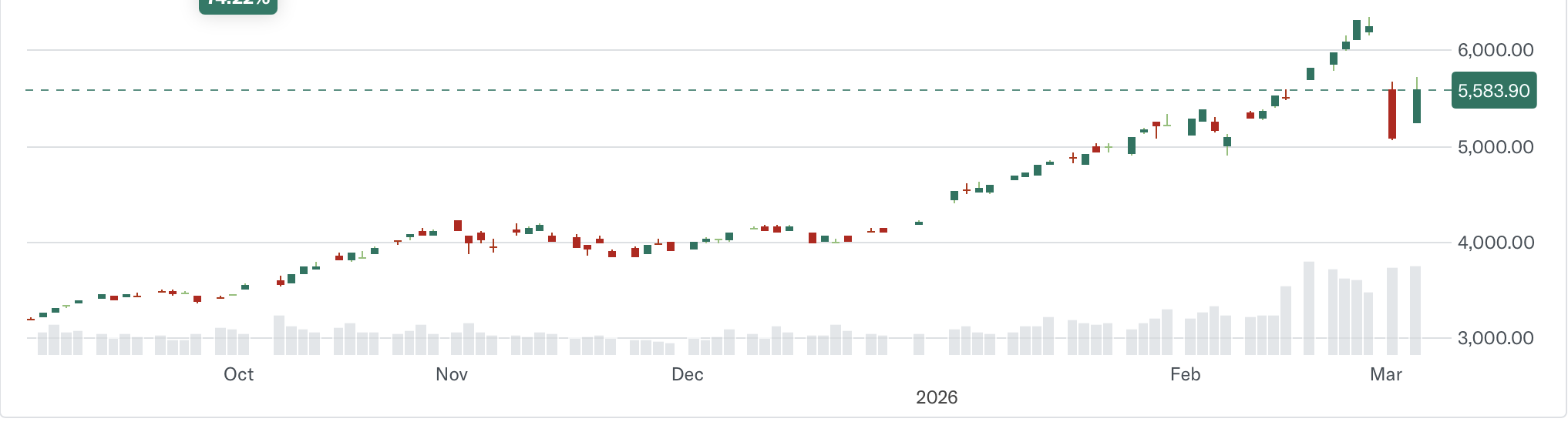

In the commodity space, yesterday saw oil prices slide about 4%, while this morning they are higher by 3.0%. but a look at the chart tells me that for now, they have found a new equilibrium just below $100/bbl +/- a bit.

Source: tradingeconomics.com

It is important to remember that despite the large jump in prices recently, on an inflation adjusted basis, the current level is still only half as high as the 2008 spike to $145/bbl. In other words, I might contend that it is not the price of oil, so much, right now, but rather its availability that is going to be the key issue going forward. Naturally, Europe has jumped in to explain that they believe high oil prices help them denounce the US removal of sanctions on Russian oil as they will not countenance such things despite the loss of their key suppliers. I’m glad I don’t live in Europe.

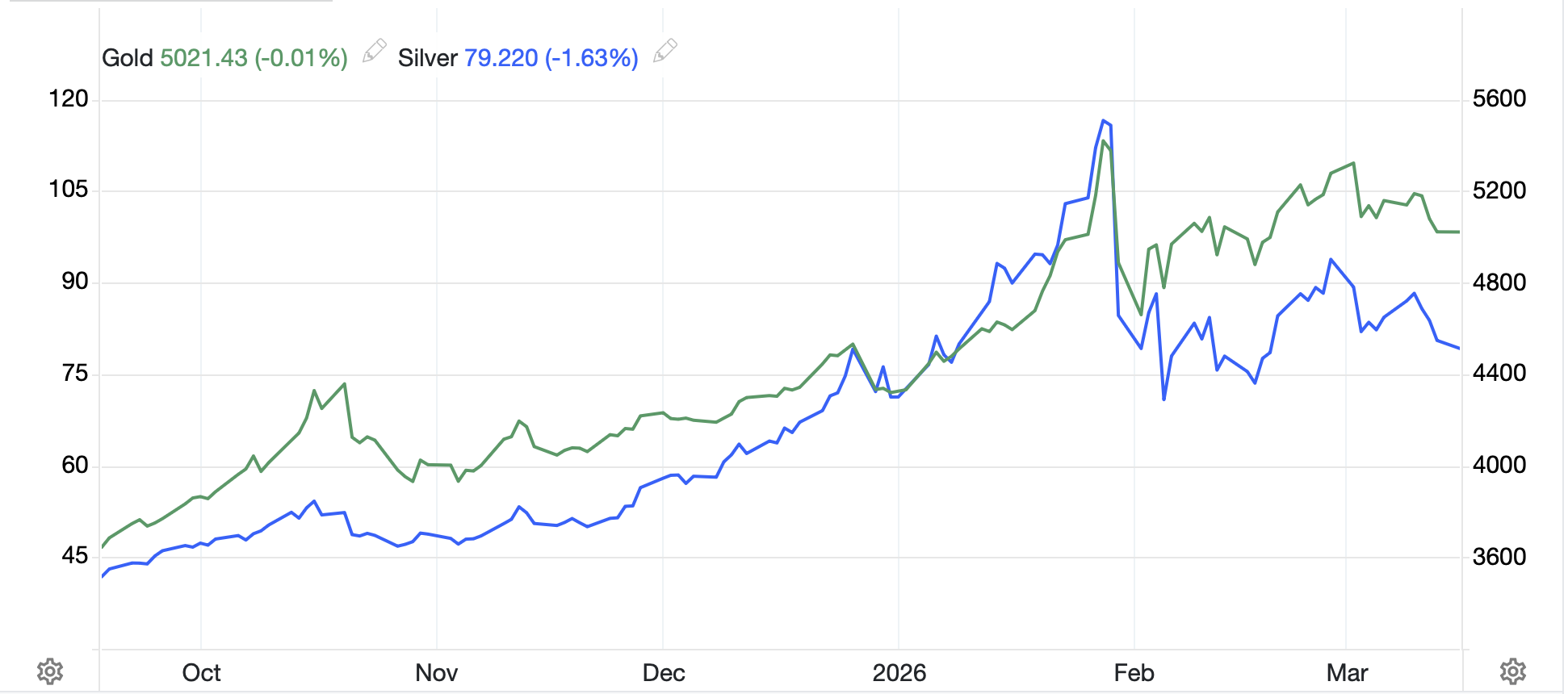

As to the metals markets, Zzzzzzz is the only way to describe them. While copper (-1.2%) has slipped, neither gold nor silver has moved overnight, and both remain essentially at their new homes of $5000/oz and $80/oz.

Finally, the dollar is also doing little this morning, essentially unchanged vs. most its major counterparts. NOK (+0.6%) is enjoying oil’s rally while ZAR (-0.5%) is suffering from the lack of gold movement. And otherwise, it is hard to get excited about anything with movement +/- 0.2% or less across both G10 and EMG currency blocs.

There is no primary data released this morning in the US. The FOMC begins its two-day meeting and tomorrow at 2:00 we will learn that policy is unchanged, but all eyes will be on the dot plot and the SEP report to try to better understand the potential future path. But for today, absent a major change in the Iran situation, I don’t imagine it is going to be very exciting anywhere.

Good luck

Adf